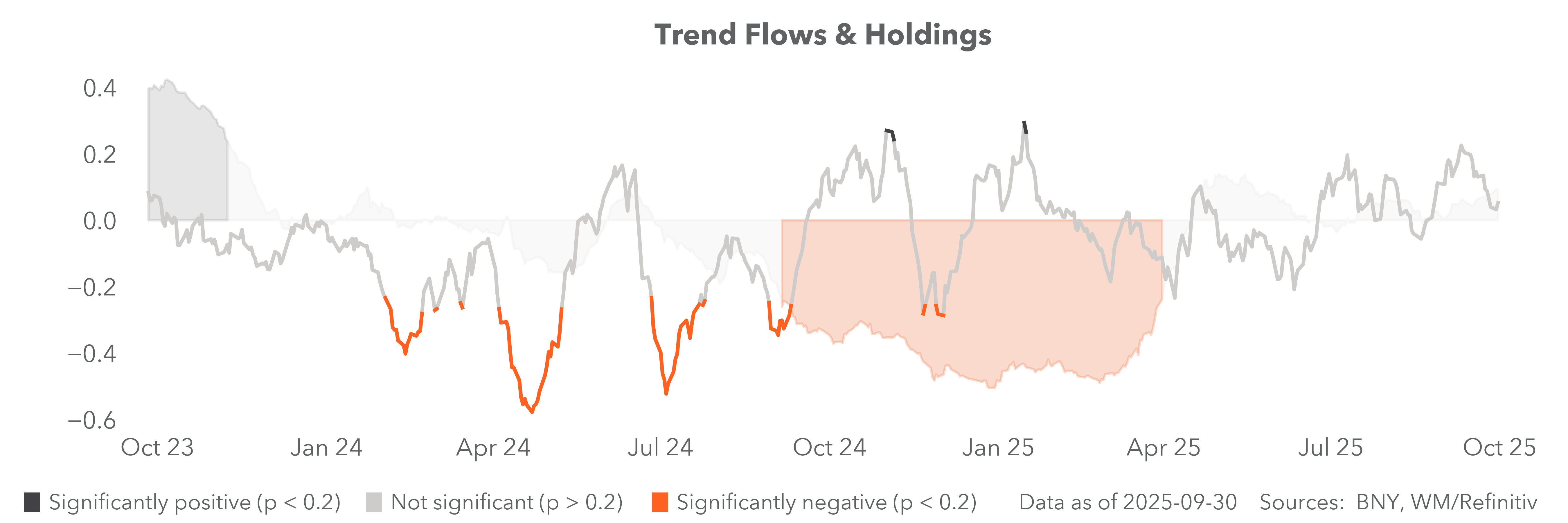

Carry’s failure to launch

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 4 minutes

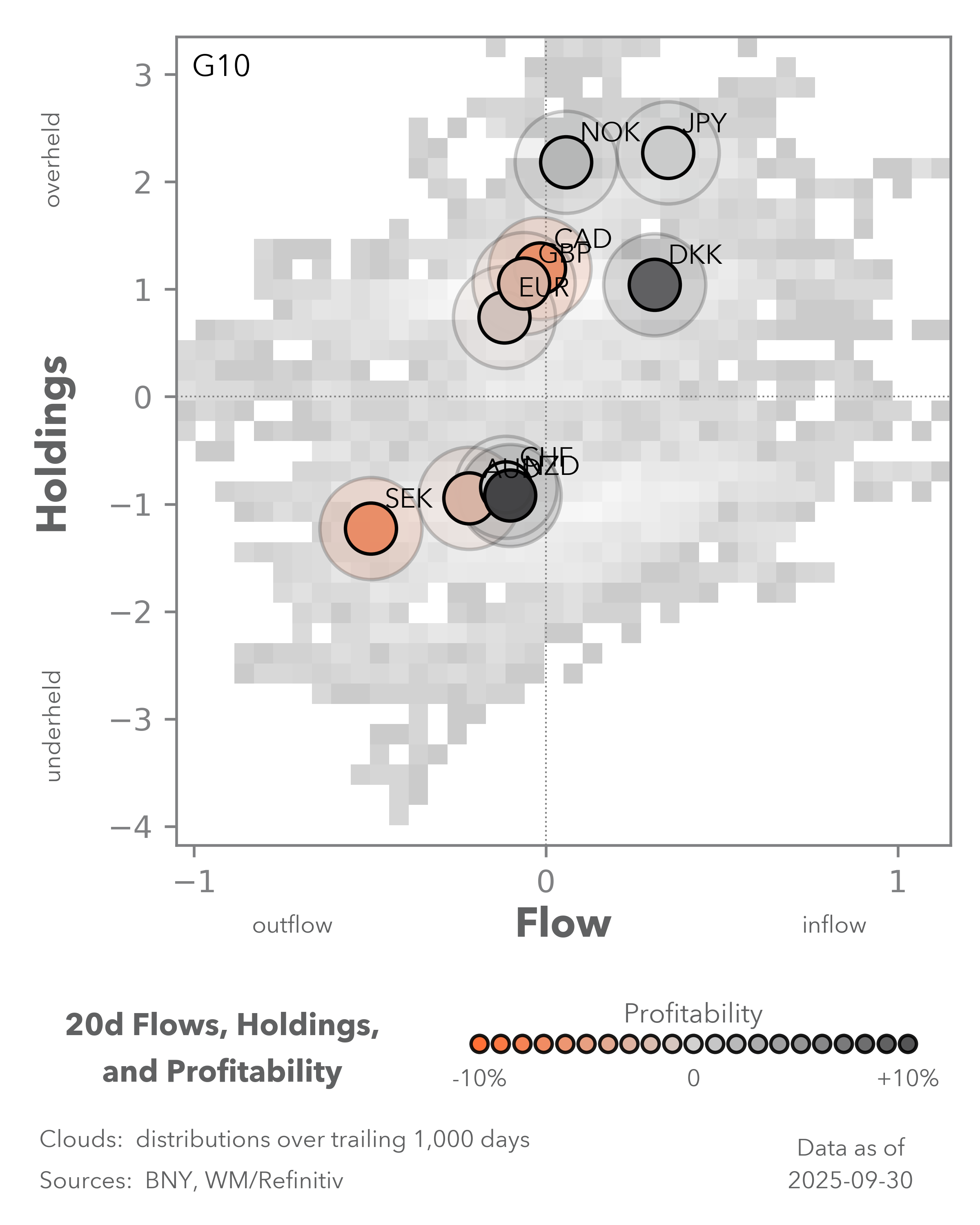

EXHIBIT #1: JAPAN NOMINAL VS. REAL WAGES SINCE END OF JUNICHIRO KOIZUMI’S PREMIERSHIP

Source: BNY

Our take

Japan’s ruling Liberal Democratic Party (LDP) will hold its leadership election this weekend and opinion polling remains split on the result. Irrespective of the composition of the next administration, the Bank of Japan’s current communication suggests that the base case remains further hikes – a path which we fully endorse. The recent Upper House elections exposed new faultiness not dissimilar to what has been observed across much of the developed world, especially in the cost of living. We can see how this led to significant distortions in Japan when a new price cycle commenced in 2022 as global inflation surged: inflation expectations shifted aggressively, and this led to a significant change in nominal wages – close to 20% since the end of Prime Minister Junichiro Koizumi’s tenure in September 2006. His son, Shintaro Koizumi, is currently leading opinion polls amongst LDP lawmakers (rather than supporters), and is seen as more of a continuity candidate when it comes to economic policy. Even so, continuity is not viable as real wages continue to struggle, with pass-through inflation having eaten up much of the real value of wage gains (Exhibit #1).

Forward look

We acknowledge that the export outlook remains challenging but the global trade environment from Koizumi Sr’s time – China joined the World Trade Organization during his tenure – will not return. Asia-Pacific economies with long-standing trade surpluses need to let adjustment take place through real effective exchange rate (REER) appreciation. It is telling that with these levels of nominal wage gains, the JPY’s REER is more than 30% weaker over the past two decades, underscoring the extent of nominal depreciation which has inhibited more active adjustment. Rate hikes precipitating JPY strength through keeping surpluses onshore can help optimize the distribution of real effective exchange rate growth more evenly between the exchange rate and inflation, and ultimately we expect both leading candidates to support the BoJ’s current approach.

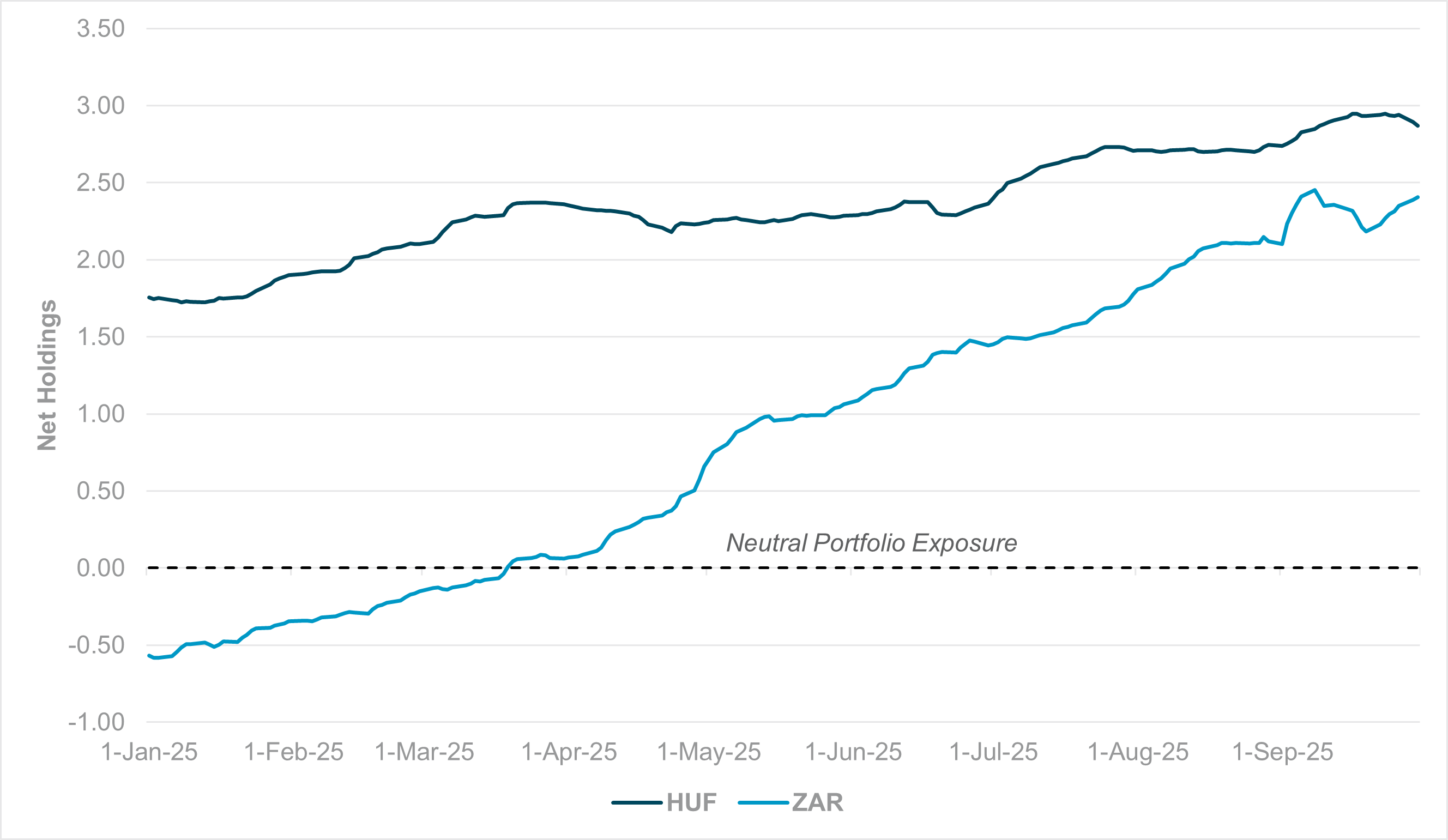

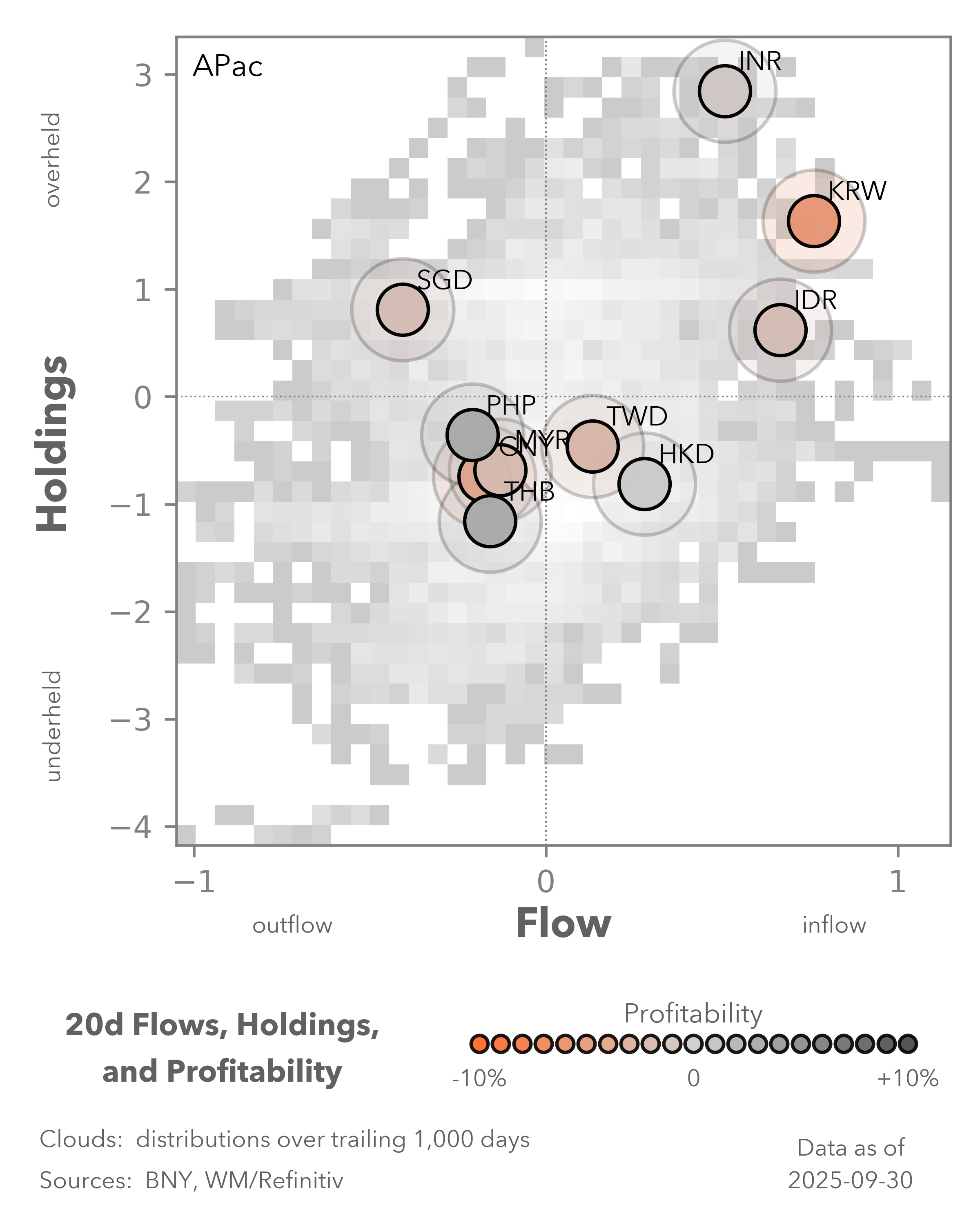

EXHIBIT #2: HUNGARY AND SOUTH AFRICA NET PORTFOLIO EXPOSURE (ASSUMING 60/40 RATIO OF FIXED INCOME TO EQUITIES)

Source: BNY

Our take

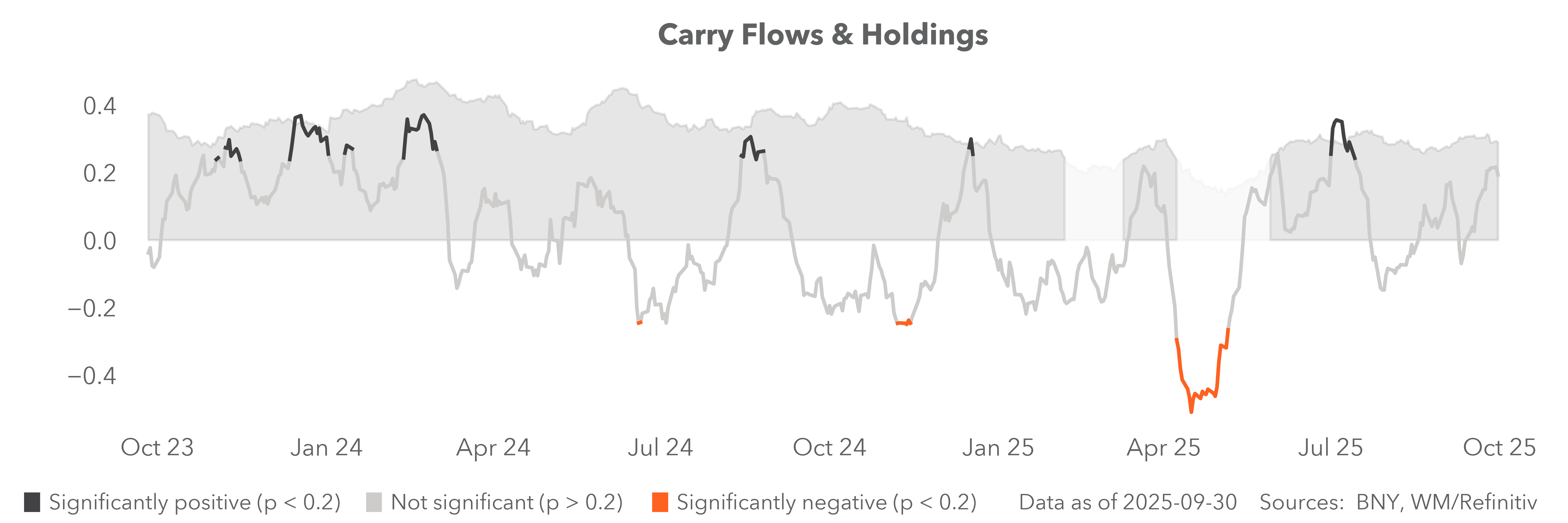

Unsurprisingly, in the wake of the September Fed cut, our iFlow Carry indicator attempted another move into positive statistical significance but was ultimately not successful. If September did indeed mark the point of “maximum dovishness” by the Fed (subject to shutdown-related developments), the risk is for rate differentials against the dollar to continue declining across the board, especially as easing cycles across EM have not ended yet. If carry now shifts back into neutral or even reverses, we believe the markets with “total portfolio exposures” will face the biggest hedging risk, to the dollar’s benefit. EMEA is now the main area with such prospects, and we believe Hungary and South Africa are particularly exposed, even though fundamentals are generally resilient. These two markets have heavy ownership levels in equities and fixed income markets, complemented by overheld positions in FX (Exhibit #2). This stands in contrast to APAC markets, for example, where broadly underheld FX positions hedge against asset exposures. In passive terms, these underheld positions will deepen commensurate to improvements in asset holdings.

Forward look

Hungary has been in a strong “total portfolio exposure” position for the entire year but gains now look exhausted. Last week we stressed that solid real rates and a strong growth narrative continue to underpin asset gains; manufacturing PMI for the country in September surprised strongly to the upside at 51.2 and was a clear outlier in Europe, including Eurozone economies. Nonetheless, the cost of hedging vs. the EUR and the USD is lower relative to ZAR, and the latter also has additional secular support in the form of gold and general commodity exposure.

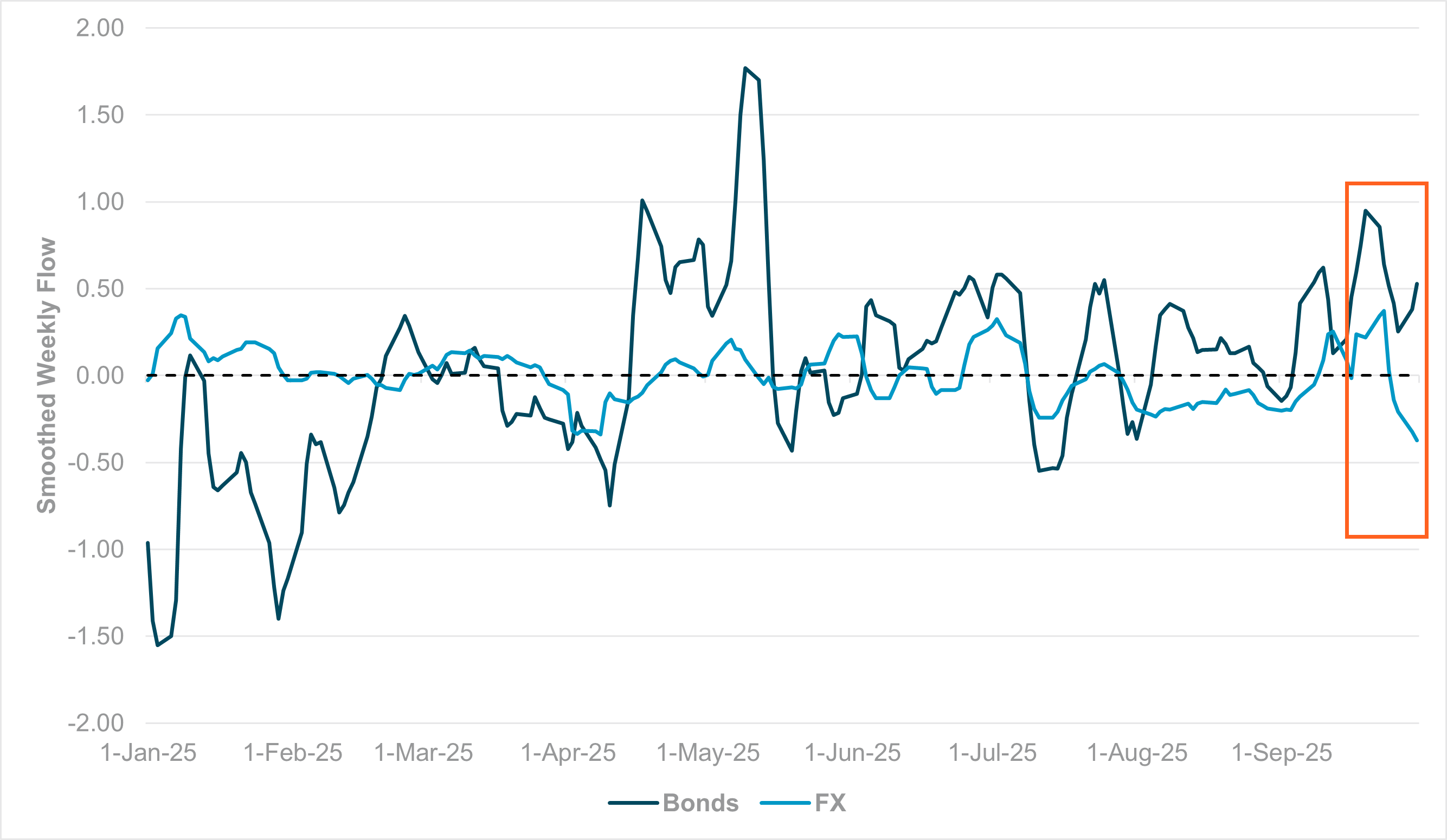

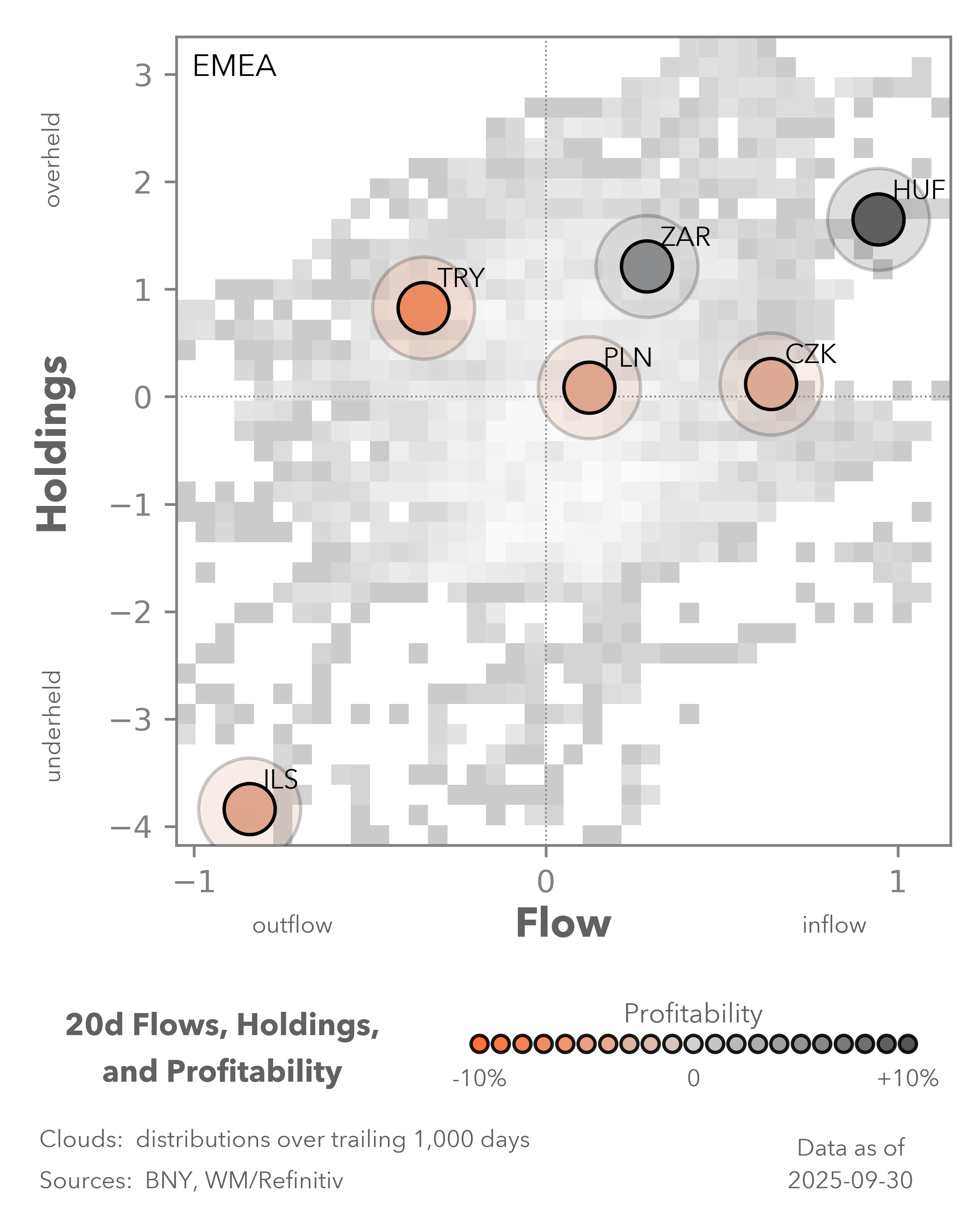

EXHIBIT #3: WEEKLY SMOOTHED FLOW, LATIN AMERICAN BONDS AND FX

Source: BNY, Bloomberg

Our take

Another indication of weakness in carry is the failure of Latin American currencies to make any meaningful gains after the Fed decision. Although there weren’t any policy surprises by the region’s central banks, we can see that on a weekly smoothed basis, the region’s currency performance recently hit their lowest levels year-to-date. Rather than add to new carry trades, hedging is taking place in a region which has been driving carry holdings over the past two years. Given the region’s rate profile is much stronger compared to EMEA, it is striking that the selling is proving more pronounced. Furthermore, we can see this is taking place amid another strong period of flow improvement in sovereign bonds, so the FX sales could indicate that these new positions are being conducted with higher hedge ratios. Even if the flows are largely being driven by Argentina, these would be hard currency bonds with similar FX profiles. U.S. support for Argentina financially is likely to be sui generis and not result in any “stopping in” of external funds more broadly. The entire region’s bonds remain net bought on a quarterly and monthly basis but momentum is on the wane.

Forward look

In contrast to EMEA exposures, the trade relationship between Latin America and the U.S. is also more complex and there is little sign of meaningful progress being made with Brazil, Mexico and Colombia – and there are signs of clear deterioration in the latter. For now, FX sales remain concentrated in the “minor” names in the region and the general asset allocation profiles for MXN and BRL remain highly positive. Nonetheless, as we said about the situation in EMEA, this probably represents the maximum point of divergence in policy expectations. Although central banks will react forcefully to dollar strength due to pass-through risks, domestic growth and external demand will likely soften toward year-end. This remains a supportive environment for duration but we believe the recent shift in LatAm FX flow direction could mark the beginning of more comprehensive risk reduction in one of the best-performing FX regions in the last six months.