Carry Recovery Easier Said Than Done

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

FX: G10 & EM, published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

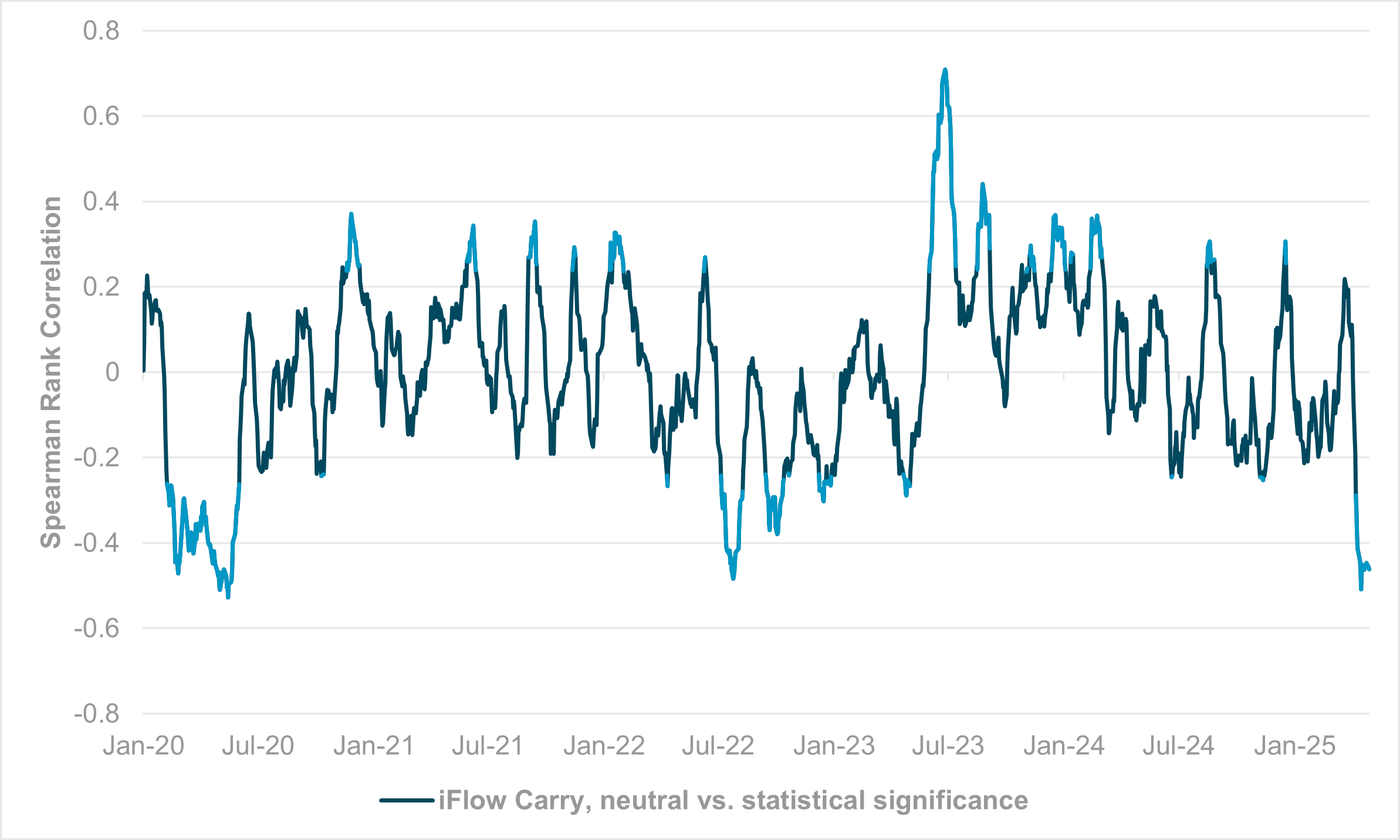

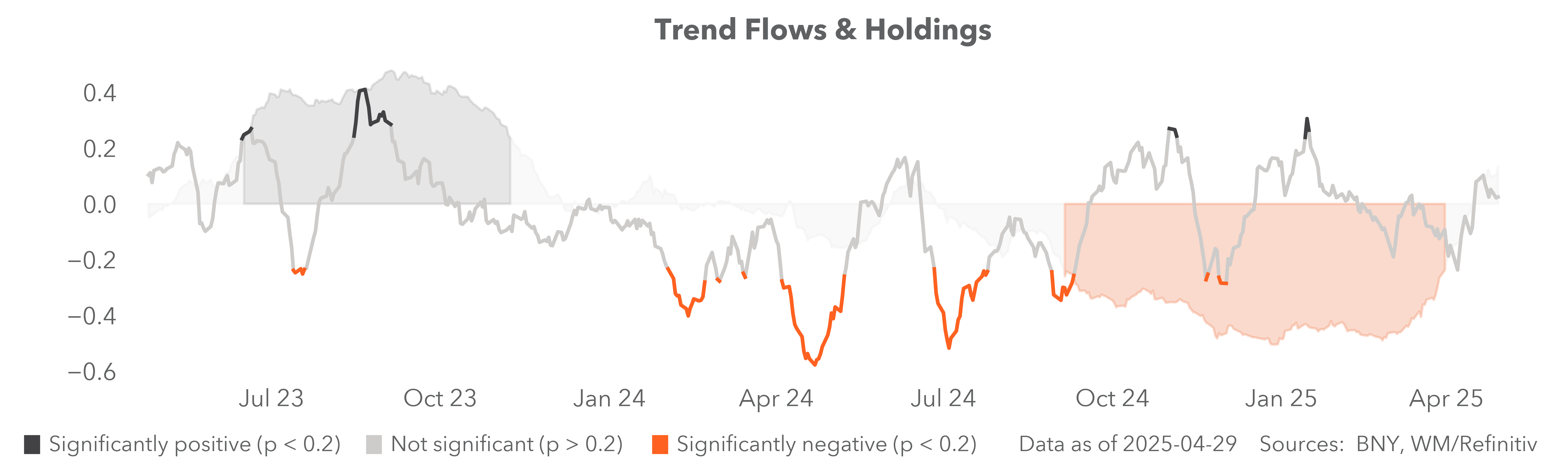

EXHIBIT #1: IFLOW CARRY REMAINS CLOSE TO MULTI-YEAR LOWS AND IS NOT RECOVERING

Source: BNY Markets, iFlow, Bloomberg

Our take

iFlow Carry had reached the lowest levels of statistical significance in close to five years. This indicated that there was significant inverse alignment between the strength of flow in a currency and its underlying yields. For example, over the past four weeks, the Swiss franc was the best-bought currency, whereas the Turkish lira ranked at the bottom. Normally, we would identify such extremes as presenting opportunities for mean reversion, as in the past when such extremes are hit, there tends to be a swift reversal as carry interest rebounds in a manner consistent with recovery in risk appetite. However, this has not been the case.

Forward look

Our assessment that positioning against carry trades had reached extremes remains accurate. iFlow Carry has not hit new historical lows (Exhibit #1), which would indicate even stronger sales of high-yielders concurrent with purchases of low-yielders. However, there is very little sign of a sharp recovery, similar to the one we observed in 2020 and 2022 – the last two rounds of extreme stress in carry trades. We believe the key reason is that investors do not see any recovery in yields, while the global risk environment remains subdued due to ongoing volatility in U.S. trade policy. The latter is dampening global growth, which data out of the U.S. and China yesterday broadly confirmed. Along with stagnation in our iFlow Mood index, there is cross-asset confirmation that sentiment is not recovering, despite lower volatility.

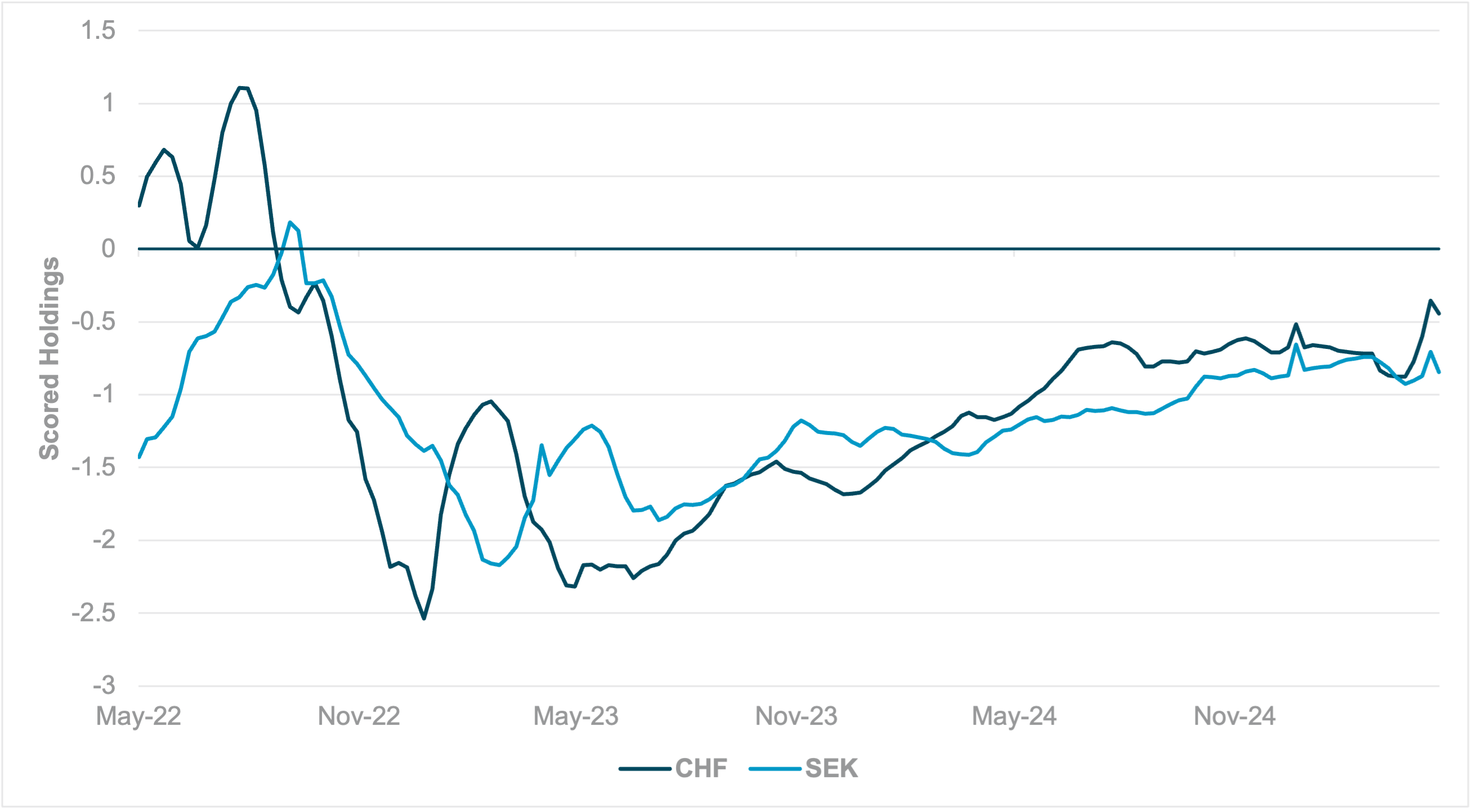

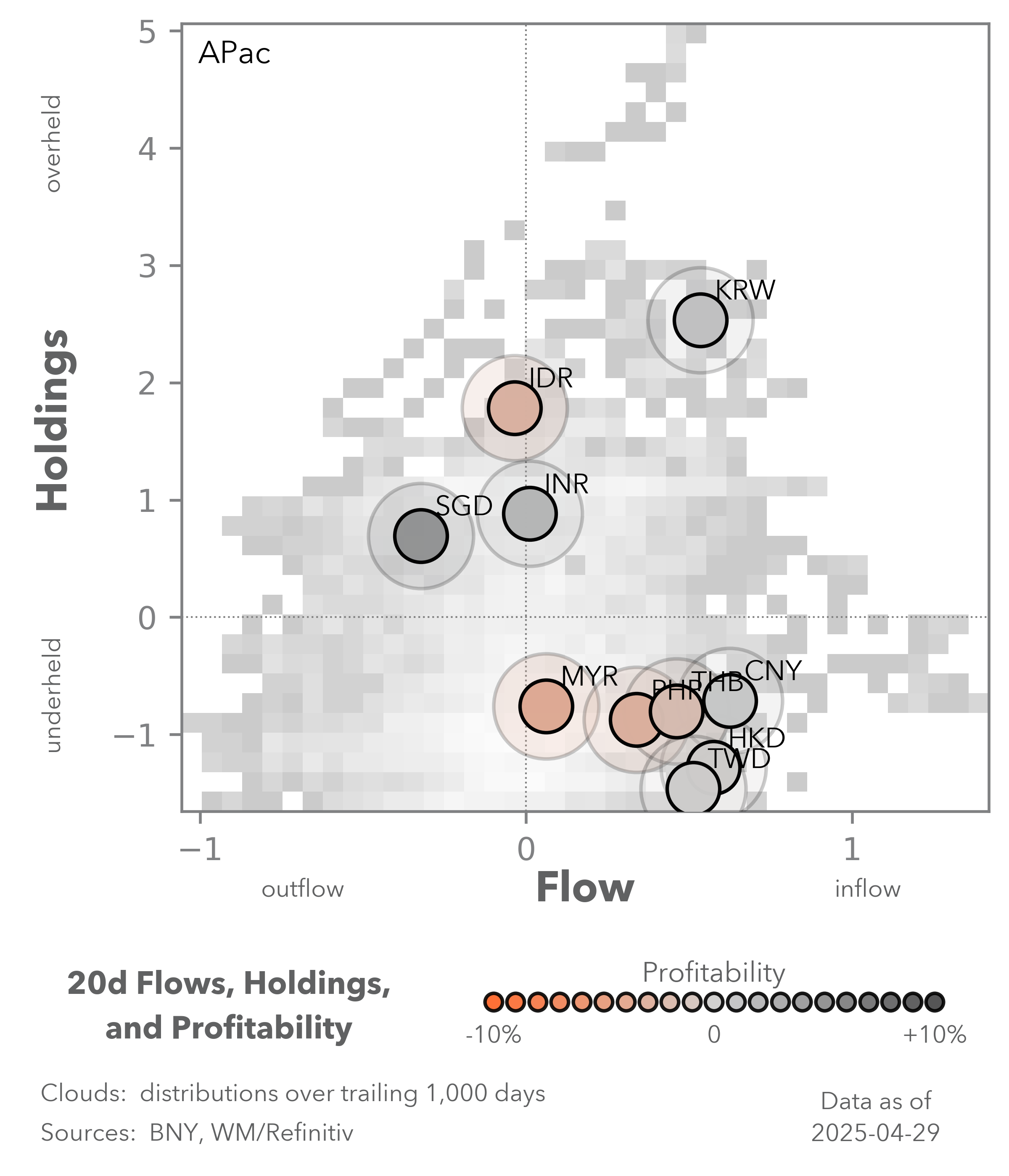

EXHIBIT #2: CHF AND SEK NOW BEST POSITIONED SINCE 2022 HIKING CYCLE

Source: BNY Markets, iFlow

Our take

For carry trades to recover, high-yielders need to be bought, and low-yielders need to be sold. We appreciate the disappointment in the former, but the strength of flow in low-yielders comes as a surprise. The JPY is once again finding bids ahead of the BoJ decision later this week, even though we expect the central bank to indicate material downside risk to their economic outlook, which could impact their view on rate hikes which hitherto had supported and justified JPY flow and positioning. In addition, strong flows into CHF and SEK (Exhibit #2) have now pushed both currencies to their best positioning levels since Q3 2022, when both the Swiss National Bank (SNB) and the Riksbank were ahead of the curve in moving away from negative rates. Indeed, we expect the SNB to return to negative rates at their Q3 meeting, but this is no deterrent to inflows.

Forward look

The performance of the JPY, SEK and CHF indicates that traditional drivers of carry trades – in both directions – have collapsed in the current environment. Although we believe talk of the dollar’s loss of its reserve status is very premature, economies with strong surpluses are anticipating material changes in their balance of payments. For example, SNB President Schlegel stated that the country would “feel tariff fallout more than others.” Fundamentally, this means lower surpluses to recycle into other currencies, and greater home bias as domestic investment is required to offset external risks. While yields for these currencies remain low and could even fall further, the global policy and trade environment has significantly changed the balance of flow. The lack of sellers of low yielders will make it difficult for the carry trade to make a strong comeback.

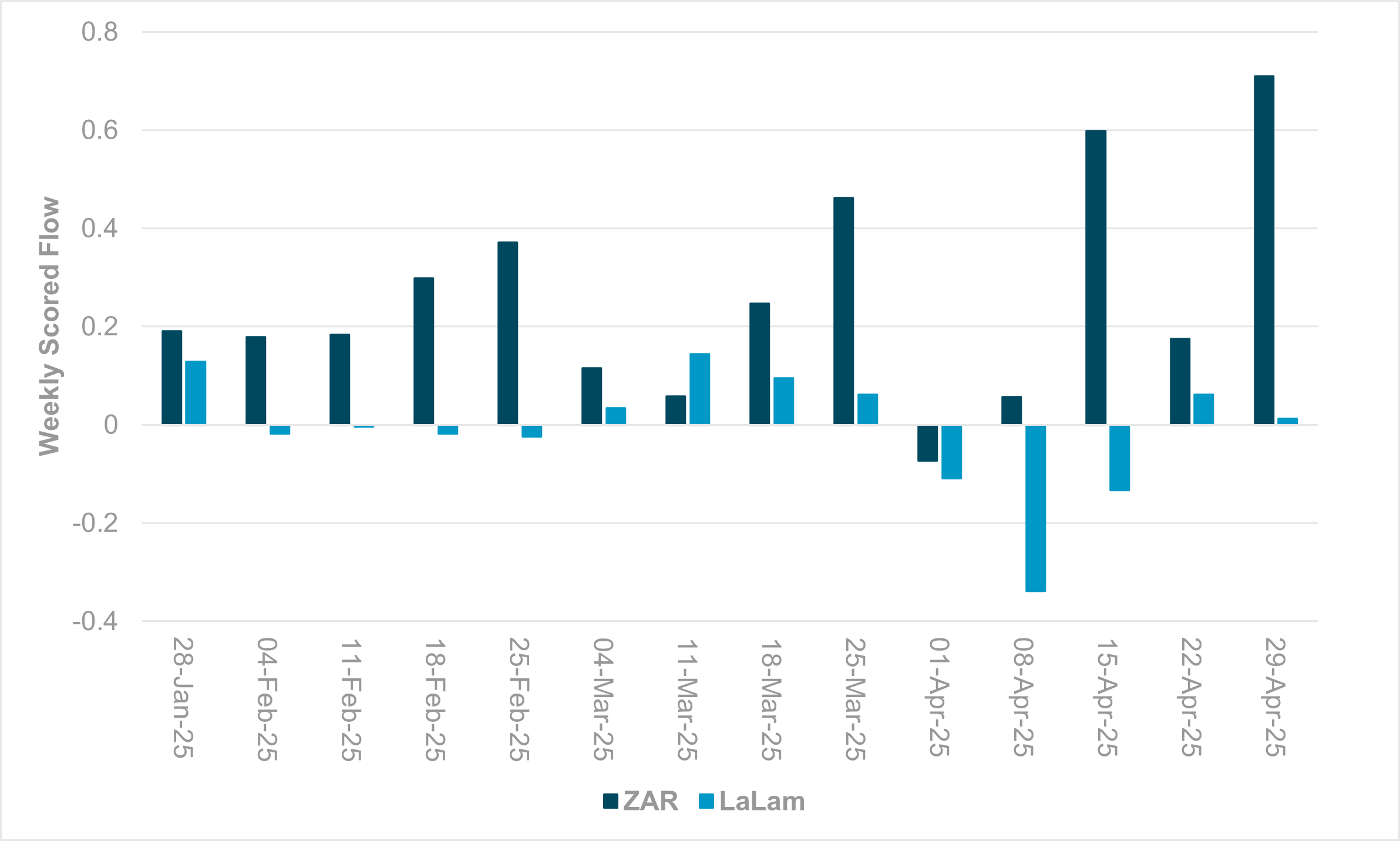

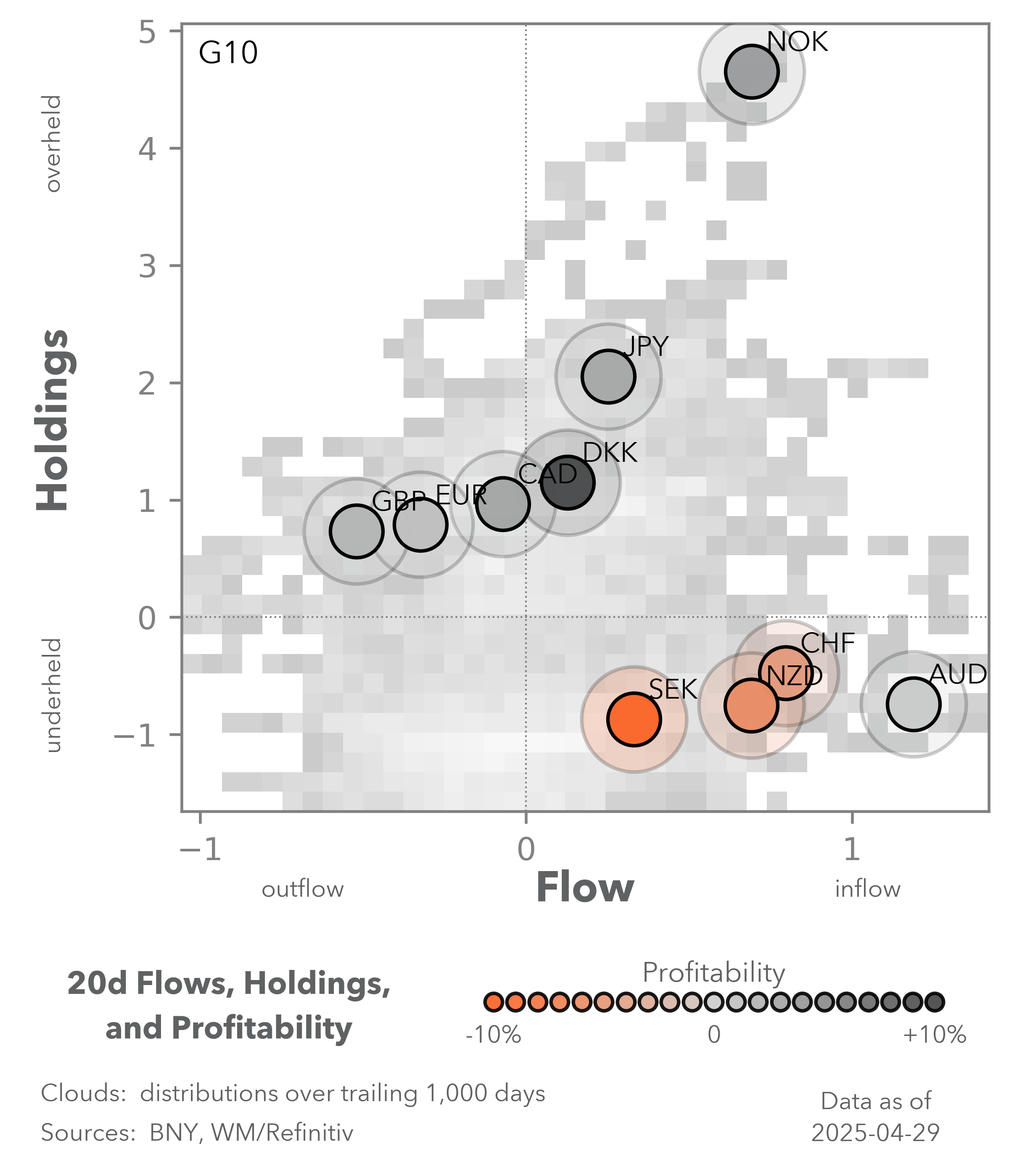

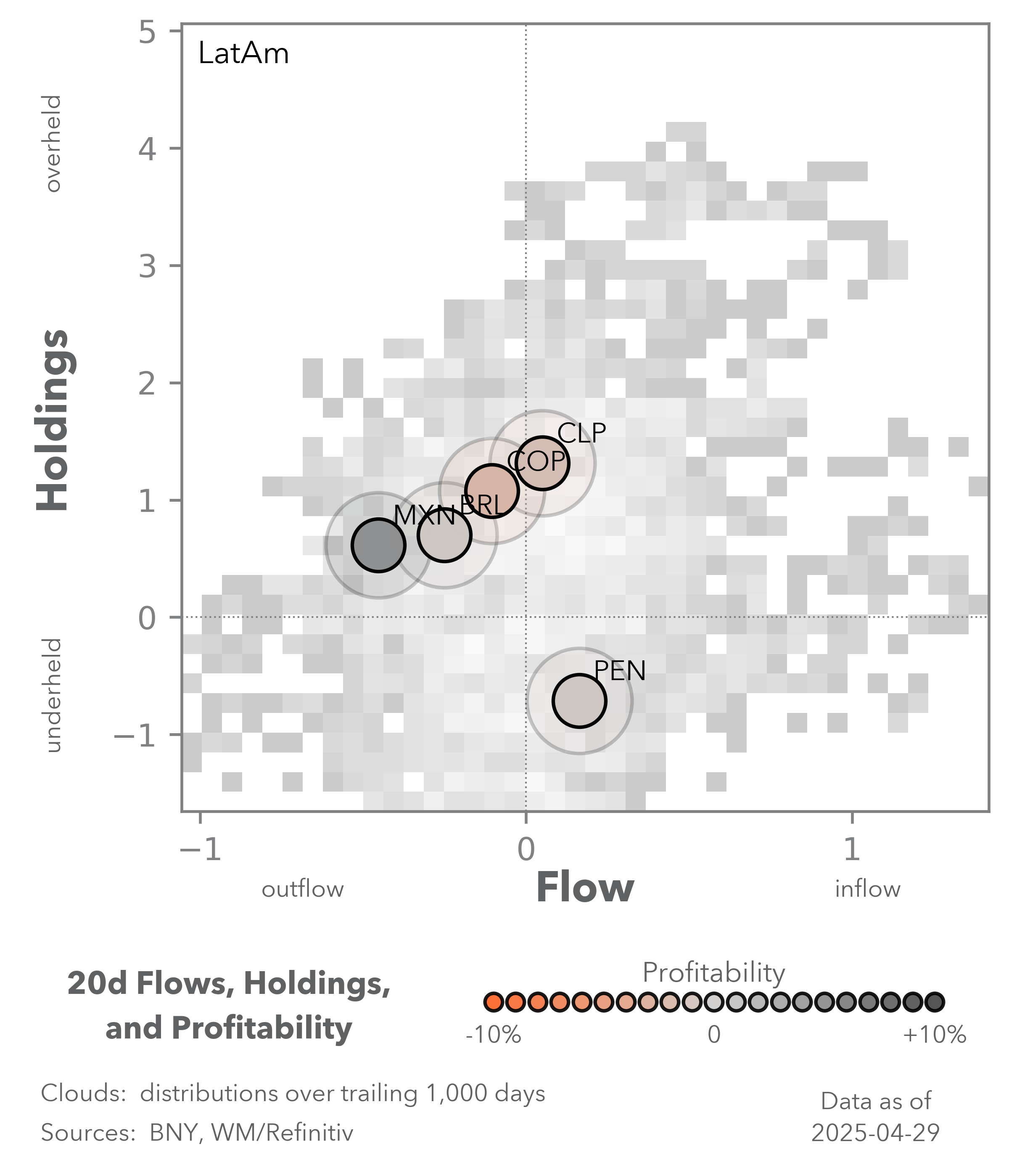

EXHIBIT #3: SOUTH AFRICA OUTPERFORMING LATIN AMERICA DUE TO FISCAL DIVERGENCE

Source: Bloomberg, BNY

Our take

Ongoing support for low-yielders aside, our original view on high-yielders finding support is also being challenged. The current drop in oil prices has already lead to EM headline inflation falling faster than expected, which means real yields – crucial for FX and fixed income flow – will continue to perform well, while headline policy rates in EM are also holding well: there were no interest rate cuts by major EM central banks outside of APAC this month. However, we did not anticipate fiscal pressures to return, especially in Latin America as the region was considered one of the paragons of fiscal responsibility during the pandemic, especially relative to G10 economies. The IMF’s suspension of the flexibility credit line with Colombia – one of the best-held markets by cross-border investors in iFlow – has added to risk premia in the region. Meanwhile, fiscal pressures are building in Chile and according to the Brazilian central bank, “domestic behaviour” (which would entail a strong fiscal component) is contributing to inflation expectations being “unanchored.”

Forward look

In contrast to Latin American economies, in Africa the fiscal outperformer – though somewhat against expectations – is South Africa. While fiscal pressures remain, the recent resolution of disputes within the Government of National Unity (GNU) has caught markets off guard and sharply reduced risk premia. Coupled with the South African Reserve Bank’s moves toward pursuing an even lower inflation target, fiscal and monetary policy credibility is a standout. This much is also evident in FX flows: last week saw the strongest inflow into ZAR on a weekly basis this year, whereas Latin American currencies are struggling for momentum (Exhibit #3). Consequently, we continue to see strong potential in EM debt up ahead, which will help fund the necessary stimulus to support economies facing tariff shocks.

Based on the risk appetite barometers in iFlow, sentiment has stabilized but at relatively subdued levels. The global growth and inflation environment at present differs vastly from 2020 and 2022. The absence of a general tightening cycle means lower market volatility and near-zero yields in funding currencies are insufficient catalysts for economies with higher yields to attract inflows. Meanwhile, fiscal credibility is becoming increasingly important for asset allocation. After all, more questions over debt sustainability are being asked about the U.S. and the Treasury market, so there is no reason for higher-yielders to expect any different. Parallels with the U.S. may also be drawn with respect to political intervention in monetary policy: yesterday Prime Minister Tusk of Poland called upon the National Bank of Poland to cut rates. In such an environment, asset managers will be more willing to hold on to well-financed lower yields until the growth cycle turns, both lifting external yields and alleviating fiscal burdens.