U.S. Rates and Rotations

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 6 minutes

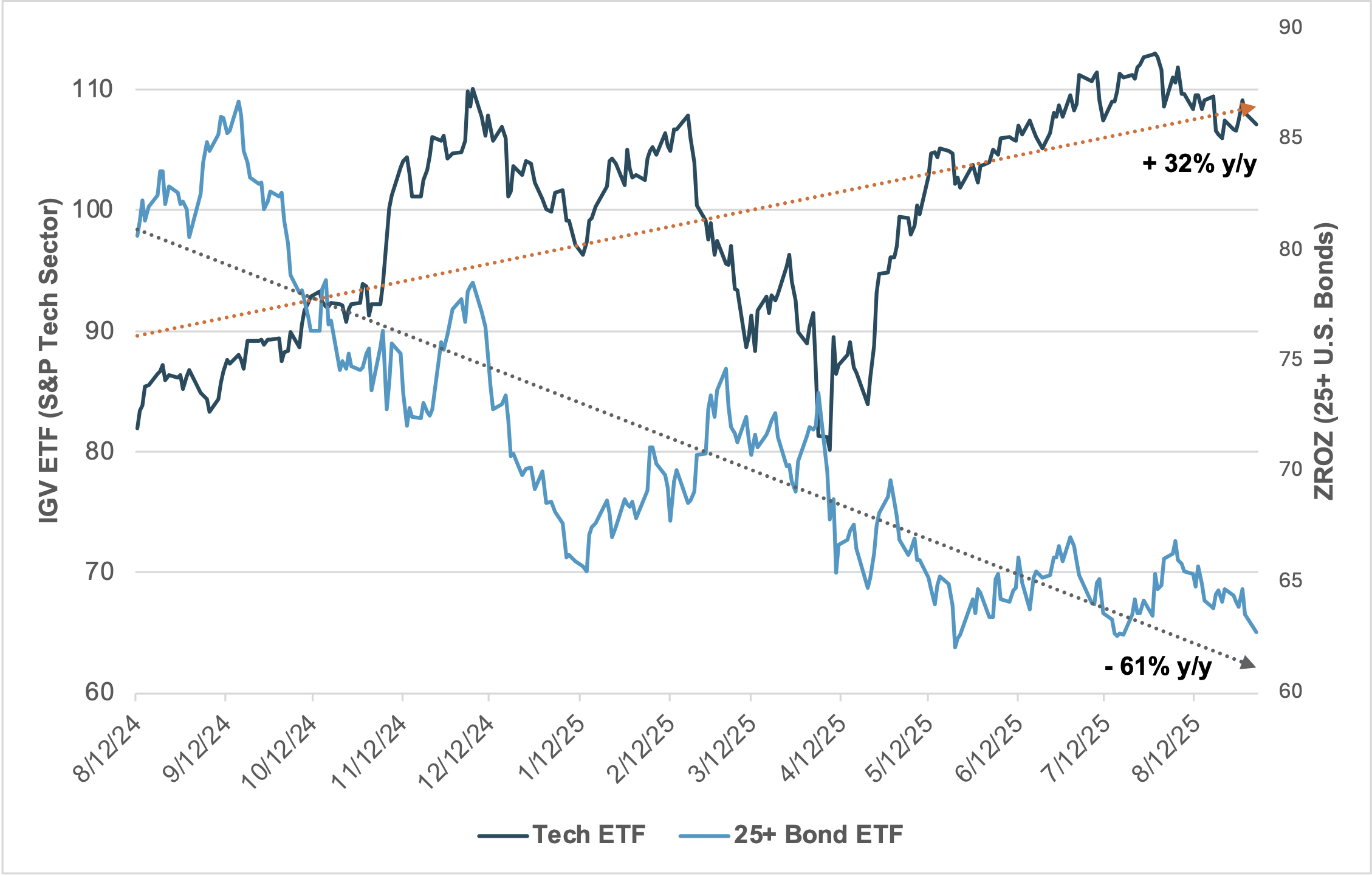

EXHIBIT #1: U.S. IT SECTOR PERFORMANCE AGAINST LONG-END U.S. BONDS

Source: BNY, Bloomberg

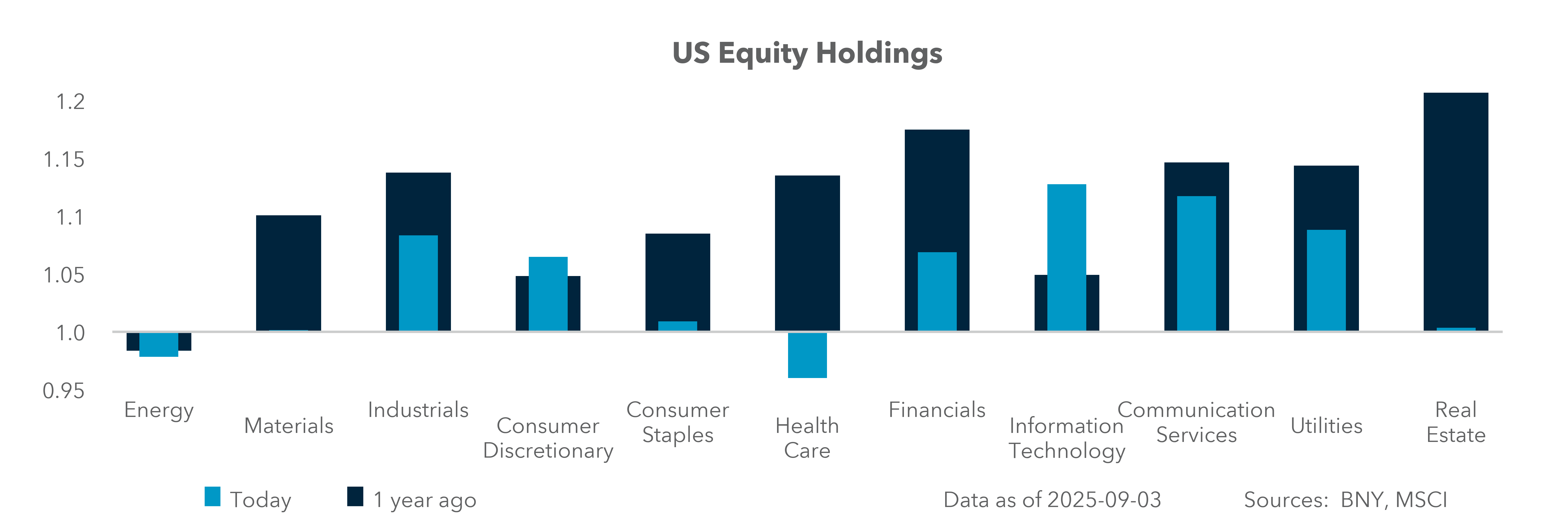

U.S. equity markets continue to lag behind the rest of the world in USD terms, and FX and rates are more important for equities rebalancing risks than during previous turning points. The first few weeks of September are usually the best, in seasonal terms, for performance ahead of the Q3 earnings “confession” period and following the release of the U.S. labor report. The risk now is that a September rate cut by the Fed will lead to expectations of a soft landing in the U.S. However, noise from tariffs and persistent inflation concerns continue to present headwinds for companies as they plan investments, while investors seek greater certainty on margins and the one-off tariff pass-through to consumers. Current rate cut expectations helped broaden the rally up in equities over the summer, but the same logic is now driving a more cautious rotational trade between rate-sensitive sectors and value. Fears of a policy misstep are driving yield curve steepening as well as duration sensitivity in shares. The correlation of rates to stocks is everchanging and dependent on the cycle, with a notable shift occurring from 2010–2020 to the post-Covid period. Potential Fed easing is creating another inflection point, given the narrow landing strip of growth and profits. The main market view is that the Fed has room to ease and prevent a recession. Whether this bears out depends on the economy and the room for policy efficacy in a politically uncertain time for the Fed. The only sector in the U.S. with holdings above last year is IT. Valuation and AI bubble concerns are a key part of the duration story, making the next few weeks critical for S&P 500 performance.

Our take

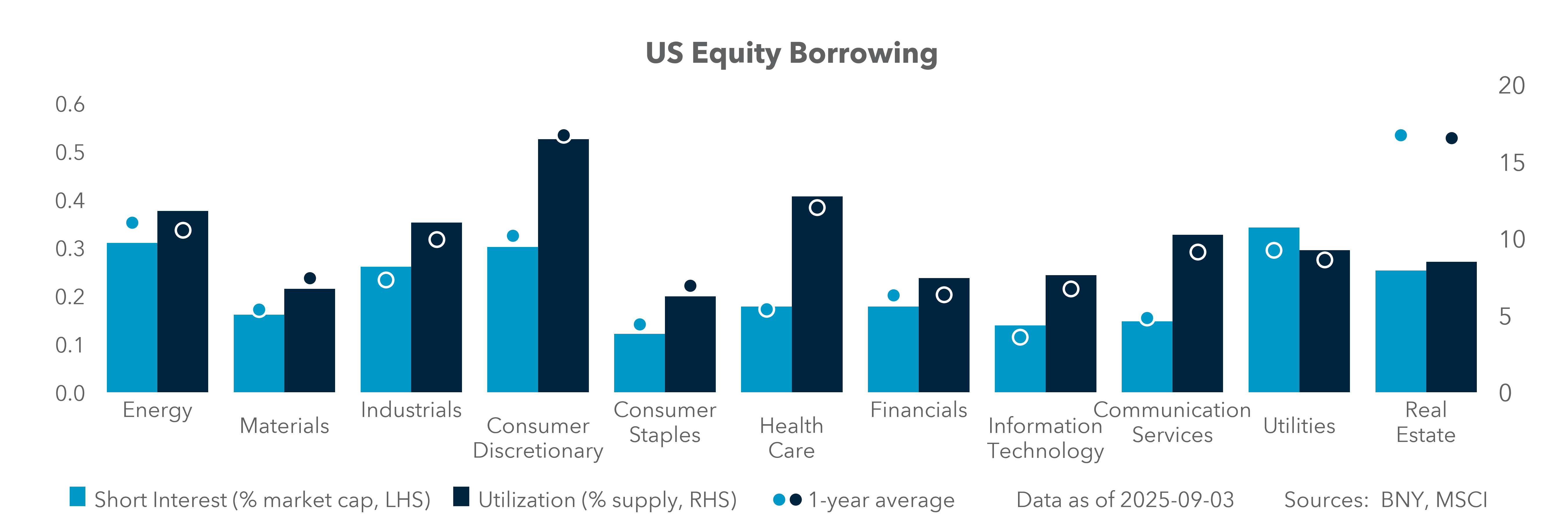

The tech sector has experienced a notable outperformance since equities bottomed out in April following the pause on tariffs. Lackluster bond market performance since then has put the relationship of bonds to stocks and duration into focus for asset allocation. Looking at our flows, the last quarter shows IT gained despite holdings, suggesting a doubling down on positioning. Looking at iFlow equity shorts, IT and Consumer Staples are the least shorted sectors, implying further dependence on Fed rate cuts. In contrast, negative flows in U.S. short-end rate-sensitive sectors stands out, particularly for Utilities, Real Estate and Financials. Some of this appears to be defensive as holdings of Financials and Utilities are 5% over the long-term average.

Forward look

Asset allocation pressure to own more bonds is linked to demographics as baby boomers enter retirement. A recent analysis by the CAIA suggests that stocks with higher interest rate sensitivity tend to lag when rates rise, while lower-duration sectors offer relative outperformance. The bond market, meanwhile, has seen mixed flows. Short-duration bonds have attracted inflows as investors seek to mitigate duration risk, while longer-duration bonds have been choppy. This shows up in the retail space in the form of increasing demand for fixed income in August ETF flows. The role of duration buying also has a level dependency, with this week’s test of 5% 30y bond yields showing significant demand. Nor is this just a U.S. story, as long-end gilts are seeing demand from cross-border investors rise as yields move sharply higher. Markets are showing price reflexivity – with demand rising along with risk premiums. This link breaks down even before fears about equities and bonds come into play. Economic data surprises, which can change views of recession and future rate cuts, pose a risk for markets.

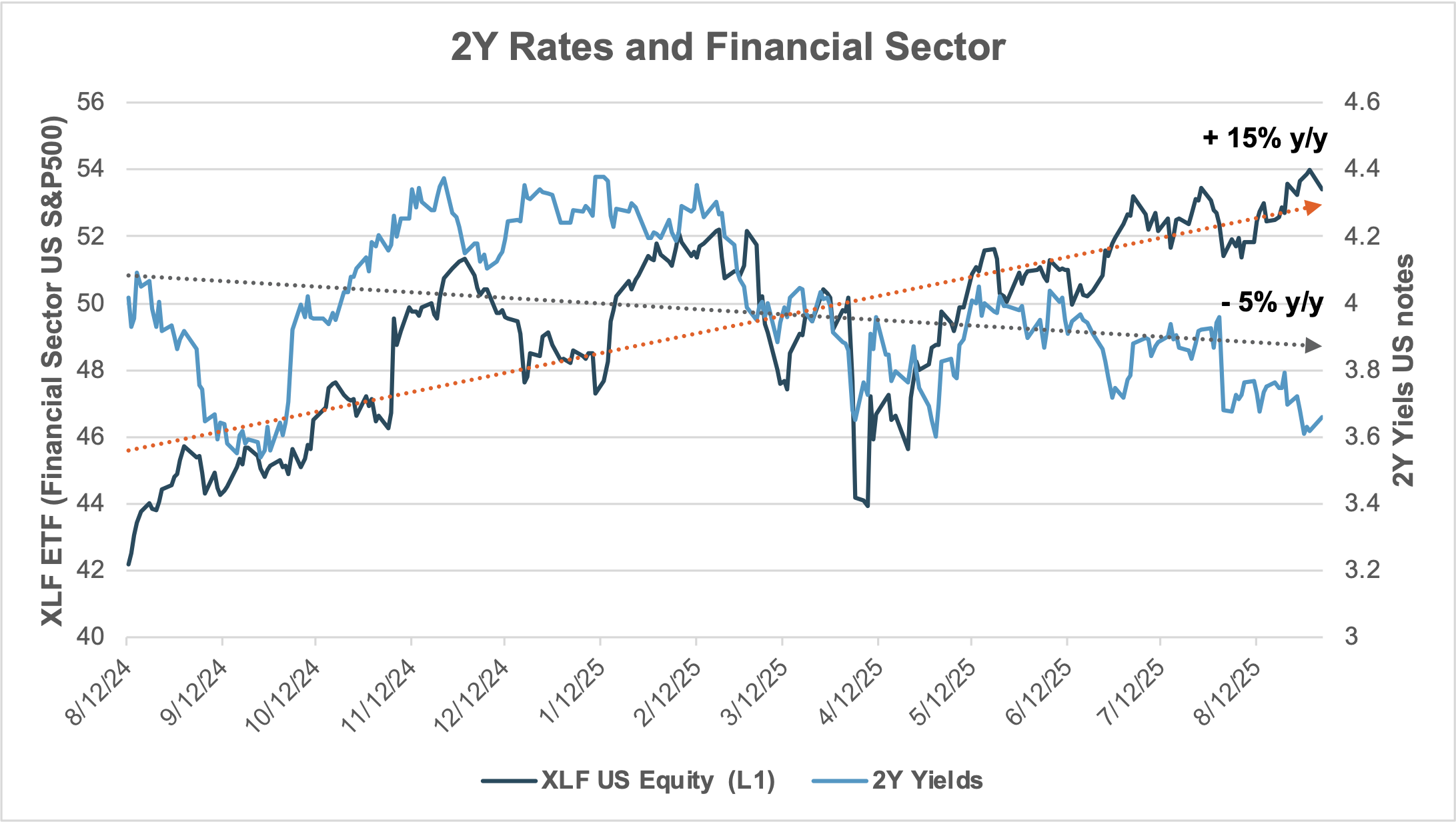

EXHIBIT #2: U.S. 2Y RATES AGAINST THE S&P 500 FINANCIAL SECTOR AND THE CORRELATION ANALYSIS

Source: BNY, Bloomberg

Our take

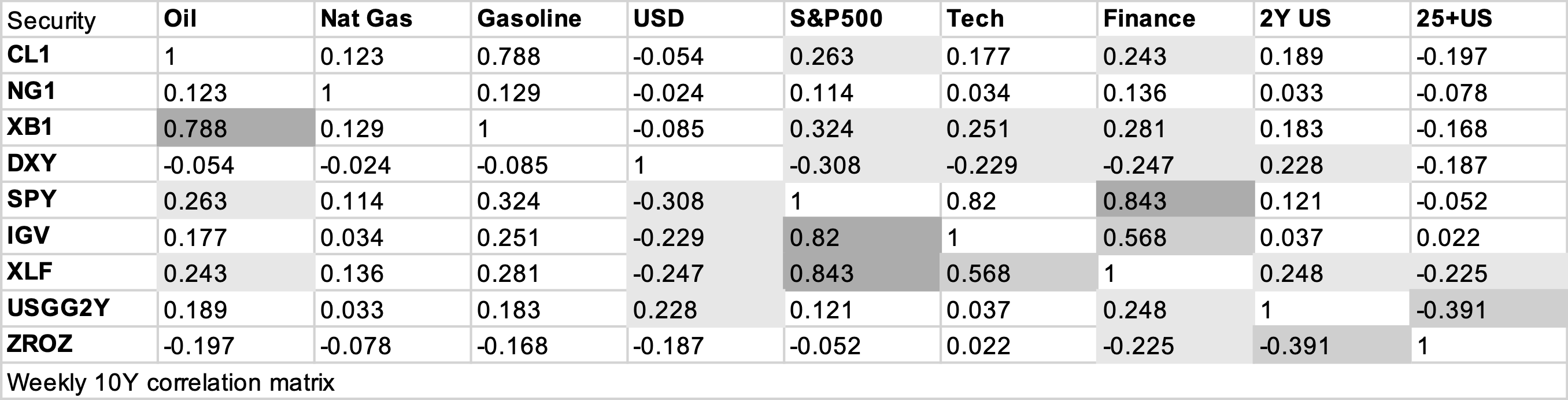

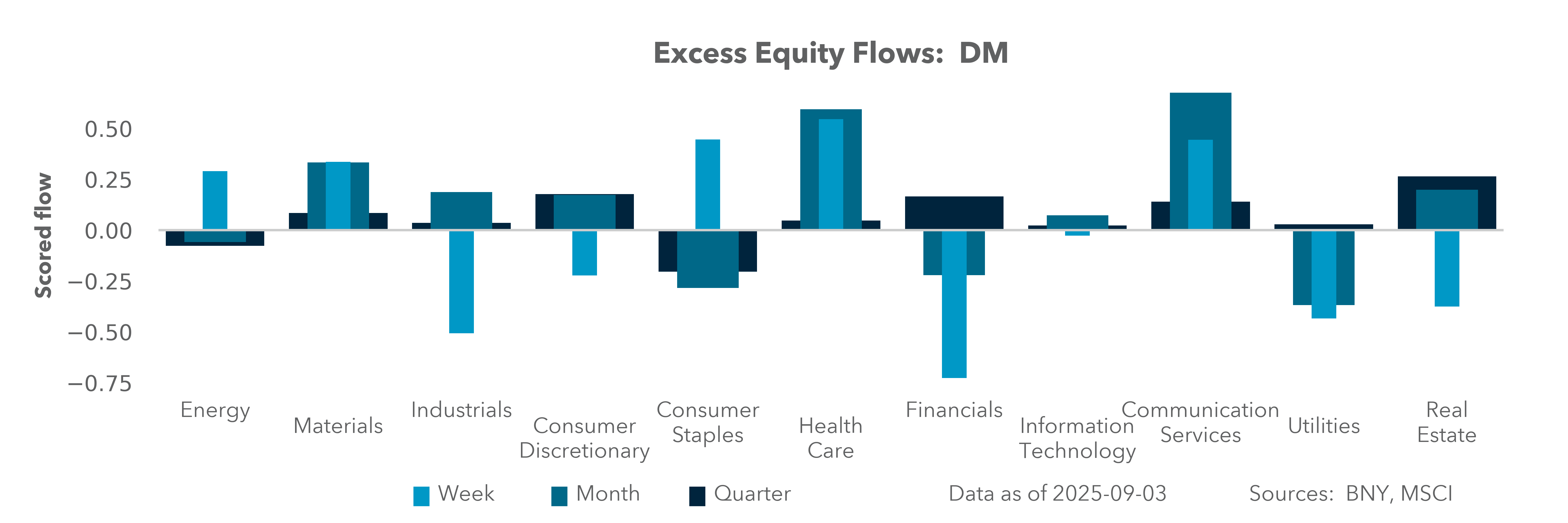

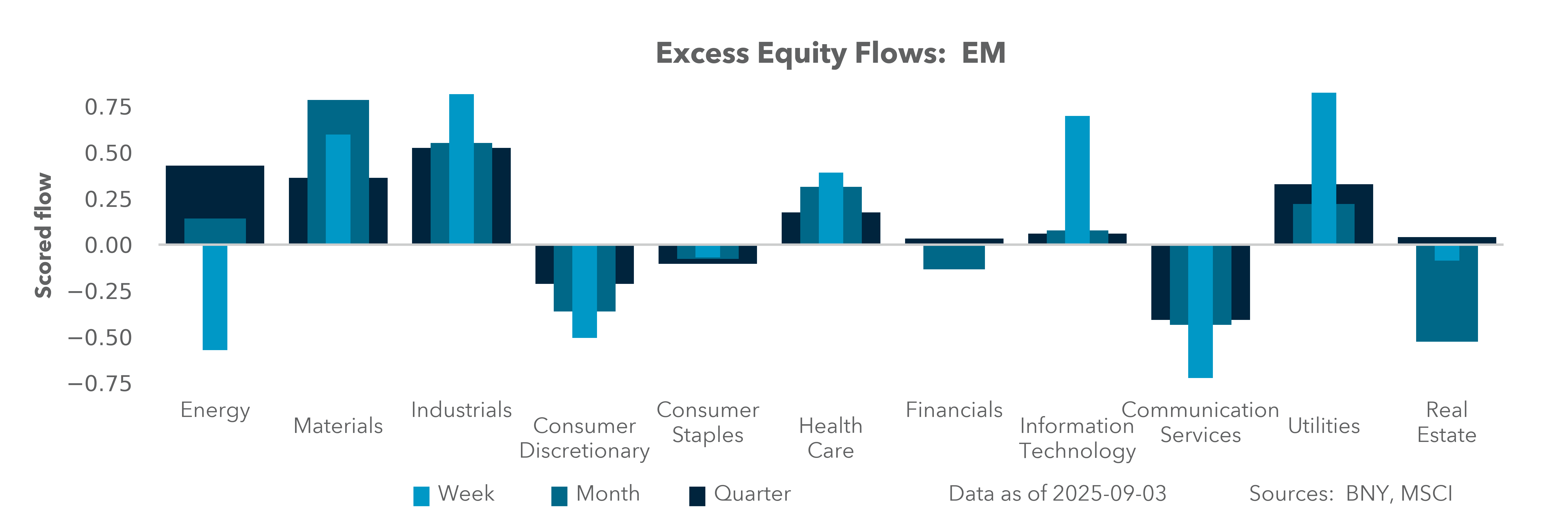

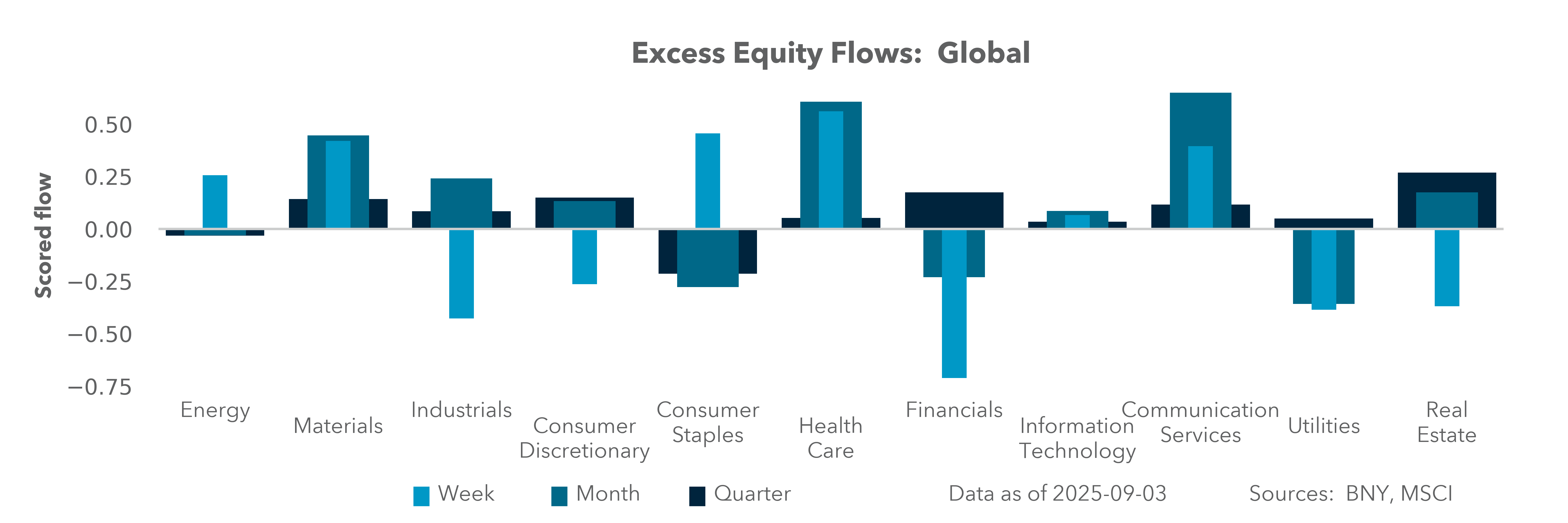

The correlation between 2y rates and the USD and Financials is more significant than the correlation between long-end (25y+) bonds and IT, in particular. In fact, the dollar is more important for the performance of both the tech and finance sectors than U.S. rates. Energy is important, too, as AI and data centers drive costs. From a flow perspective, iFlow shows a sector rotation tracking classic rate-sensitive patterns, with banks, industrials and materials negative on flows despite stable or even rising holdings (reflecting buying outside of real money investors). The pattern of equity and cross-border flows – plus concurrent Treasury duration flows – suggests institutional investors are increasingly positioning U.S. equities as “duration assets,” especially in Utilities and Real Estate. This mirrors 10y+ bonds, with active avoidance of the sectors most at risk from either sticky inflation (Financials, Energy) or a slowing economy (Industrials).

Forward look

The correlation between stocks and bonds has always been a source of debate and anxiety for investors. The difference now is that current expectations of a rate cut by the Fed and higher long-end rates clash with the consensus view of sticky inflation. Survey data suggests that inflation is a real concern for consumers and business. However, analysts do not share this concern. According to FactSet, despite market concerns about inflation and tariffs, analysts have not lowered their EPS estimates more than normal for S&P 500 companies for the third quarter. In July and August, analysts increased EPS estimates slightly for the third quarter. The Q3 bottom-up EPS estimate (which is an aggregation of the median EPS estimates for Q3 for all the companies in the index) increased by 0.5% (to $67.66 from $67.32) from June 30 to August 28. The third quarter marks the first time analysts have increased aggregate EPS estimates in the first two months of a quarter since Q2 2024 (+0.3%). The bottom-up EPS estimate for calendar year 2025 was increased for seven sectors between June 30 and August 28, led by Communication Services (+4.0%), Financials (+3.3%), and Consumer Discretionary (+3.0%). The latter two are considered highly interest rate-sensitive.

Investors have faced conflicting signals over the last two weeks, with lower interest rates but sticky inflation. In response, they have sold bonds and bought stocks. Growth stocks, which have a duration of 25+ years, have underperformed value stocks, with a duration closer to 12 years. Investors are recalibrating portfolios, with many trimming their exposure to rate-sensitive sectors in favor of more defensive, lower-duration names. U.S. equity mood scores have been persistently negative since late June and remain below zero, pointing to a sustained risk-off stance among institutional investors. The iFlow equity-specific flow index remained in negative territory throughout August, consistent with heightened correction risk and reduced risk appetite. Sector flows confirm that rotation risk is real, and not just hypothetical. Since July, flows have rotated out of Technology and Financials (persistent negative flows) and into Consumer Staples, Utilities and Real Estate. Holdings data further supports the persistence of this rotation, as Information Technology holdings (relative index) have drifted slightly lower since July; Consumer Staples and Utilities holdings indices have steadily risen, indicating asset allocation changes rather than transient flows. While the summer delivered historic index highs, the components were less robust. As research shows, understanding the nuanced relationship between rates and stock returns – particularly across different sectors and styles – will be crucial for navigating the coming months. Looking ahead, correction risk and rotation risk are not just potential worries – they are being priced and acted on by institutional flows, according to iFlow and leading options data. Expect elevated volatility around labor data and a potential acceleration in the coming weeks.