The Impact of Tariffs on Shipping and Risk

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

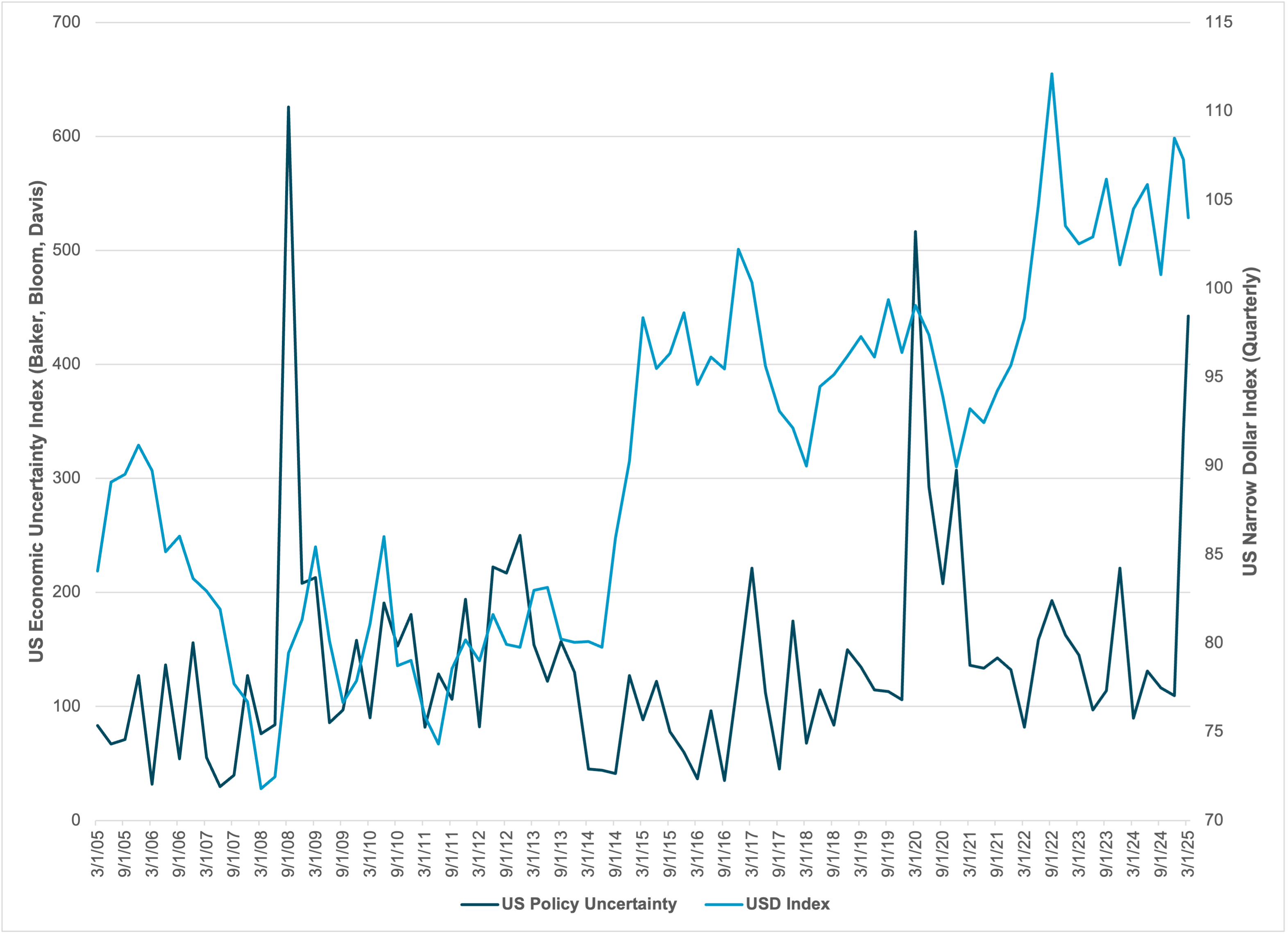

EXHIBIT #1: US ECONOMIC POLICY UNCERTAINTY VS USD INDEX

Source: Bloomberg, BNY

The US dollar fell from 109.50 to 105.00 on the Fed index, highlighting the flow of money out of the US into Europe and elsewhere. This rotation has been driven by the US’ reversal on the Ukraine war and, potentially, its role in NATO, leading to calls for increased European defense spending. According to quantitative trading models, the rotation represents an unwinding of carry trades. The downside for the EU may be the lack of a peace dividend.

Our take

The USD reaction to tariffs so far this year has been counterintuitive, with the USD index off 2.5% and big moves by JPY, EUR and some EM currencies, led by BRL. Economic uncertainty about US policy has made USD less of a safe haven, a surprising turnaround from 2024.

Fixed income moves have been the most pronounced, with tariffs leading to a sharply lower outlook for US rates. Futures have shifted from the one rate cut that was expected as recently as January to three or more in early March. Yields on 2y bonds fell from 4.4% to 3.9%, while the 10y yield rose from 4.8% to 4.10%. These trends are most evident in February ETF flows, with fixed income recording the largest flows since July 2024 and equities the smallest since August.

Forward look

Declines in USD and US equity risk are now positively correlated. The downward USD trend is a problem for stocks that investors need to keep an eye on. Asset allocation will be a key theme for US equities going forward. The flow of money out of US long holdings into European defense shares and Chinese tech companies continued in March, with the addition of a rotational trade into slowing economic sectors. US ETF fixed income inflows highlight that the allocation shift out of stocks into fixed income isn’t just institutional story, but also a retail one. The role of a USD correlation breakdown to US equity buying adds to uncertainty. Higher volatility in all asset classes means less risk taking and less liquidity. Investors will need to pay greater attention to market fragility going forward and plan asset allocation accordingly.

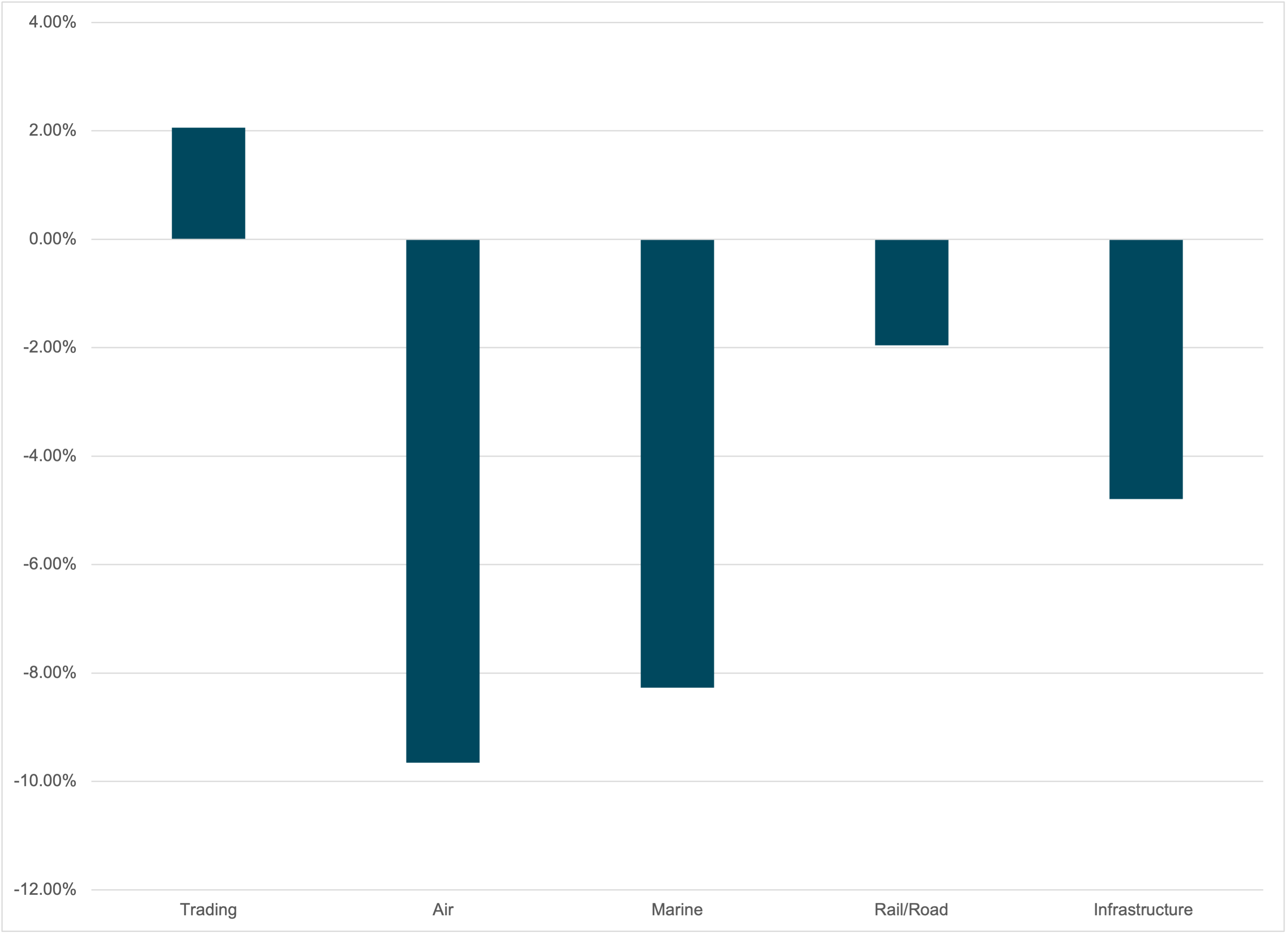

EXHIBIT #2: US EQUITY HOLDING IN TRADE INDUSTRIES VS 3Y AVERAGE

Source: Bloomberg, BNY

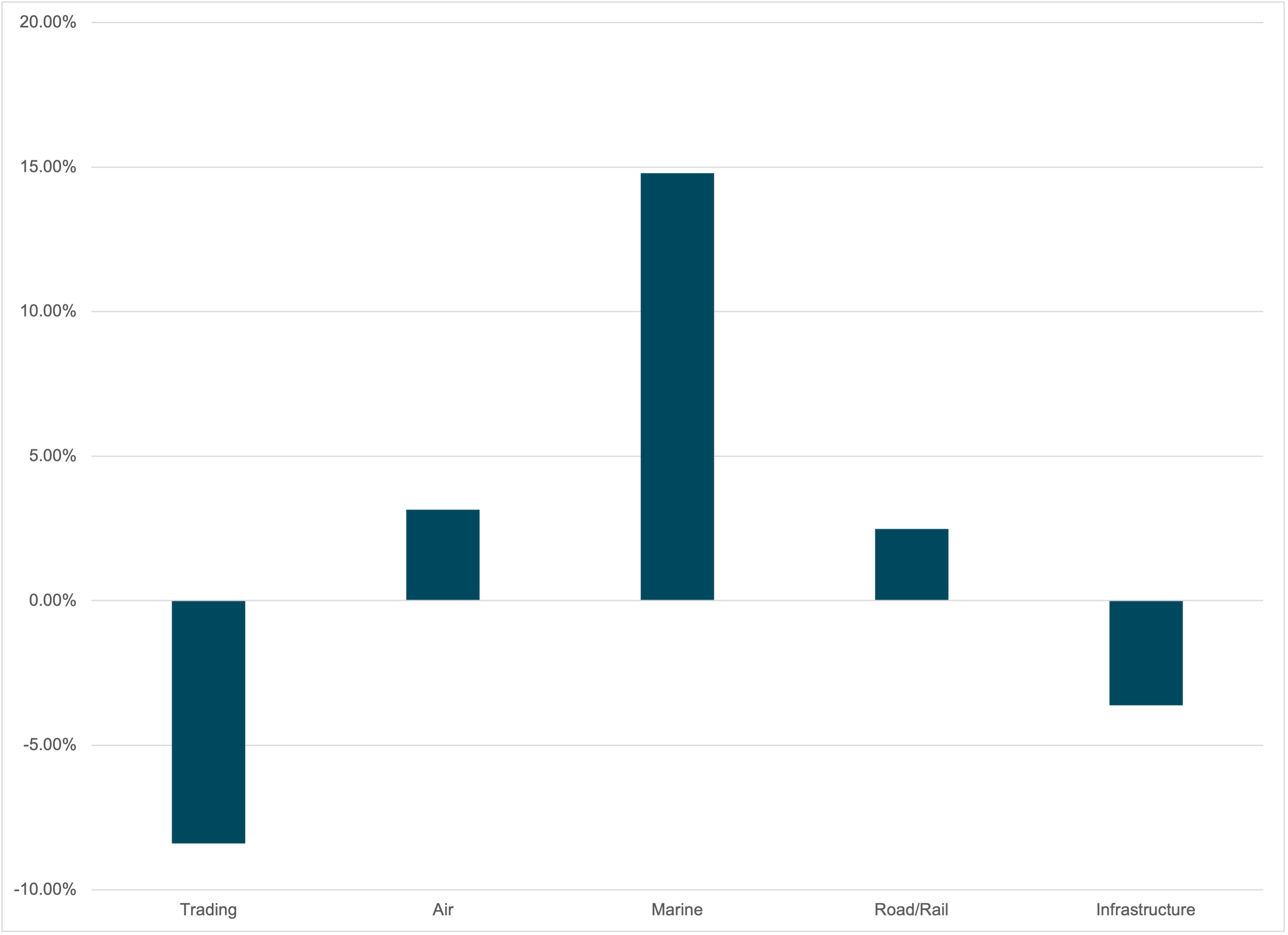

EXHIBIT #3: GLOBAL TRADE INDUSTRIES HELD VS. 3Y AVERAGE

Source: Bloomberg, BNY

Two forces have been at play in equity markets. The first is a rotational shift, with a distinction between domestic and foreign revenues in US markets. This is in anticipation of the response to tariffs and a slowdown linked to supply uncertainty. There has also been a growth factor shift on concerns about a possible US recession as well as tariffs and other policy shifts like less stimulus (as the US government reduces spending and reduces its workforce). The pricing of a recession economy can be seen in stock sector rotations.

The second force shows up in credit markets, as spreads have started to widen after months of tightening on no-landing or soft-landing economic scenarios and further FOMC cuts. Higher borrowing costs surprised many investors this week, led by the surge in EU rates.

Our take

Trade industries – including air freight, marine and rail companies – are seeing a notable downward shift in US holdings, while there has been a major increase in global shipping and investments. This makes any slowing of US shipping demand important for global investment risks. The cost of shipping and the flow of shipping share purchases is normally correlated, but this correlation collapsed in 2024.

Forward look

Over the next month, investors face risks from industrial investment flows, particularly shipping, as US actions begin to take effect. The risk to ship builders, retail companies dependent on Chinese shipping and the port infrastructure that supports the supply chain will unwind as a new equilibrium devoid of US flows is established. Expect selling in global transportation and buying US transportation.

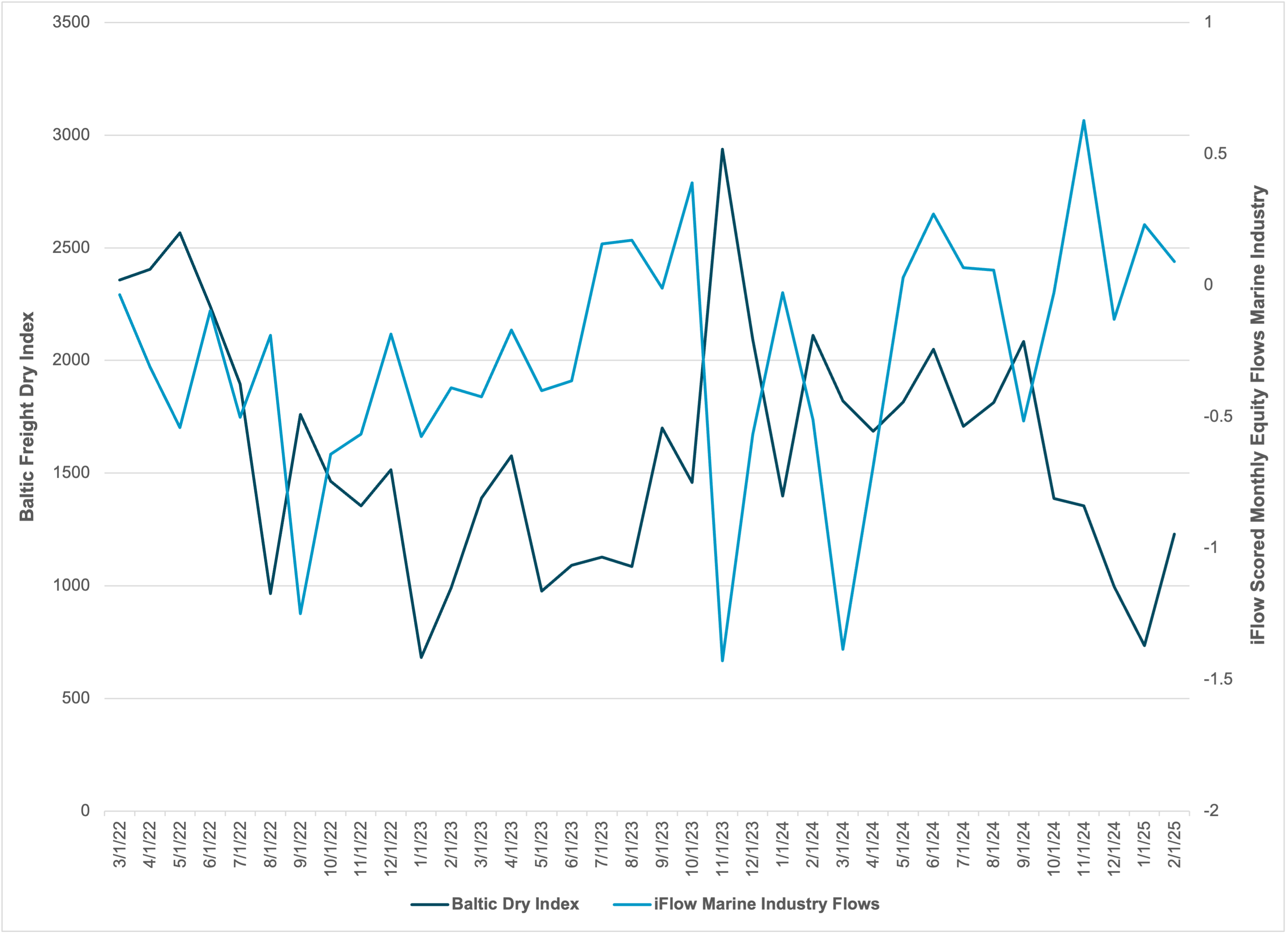

EXHIBIT #4: BALTIC FREIGHT VS. iFLOW MARINE FLOWS

Source: Bloomberg, BNY

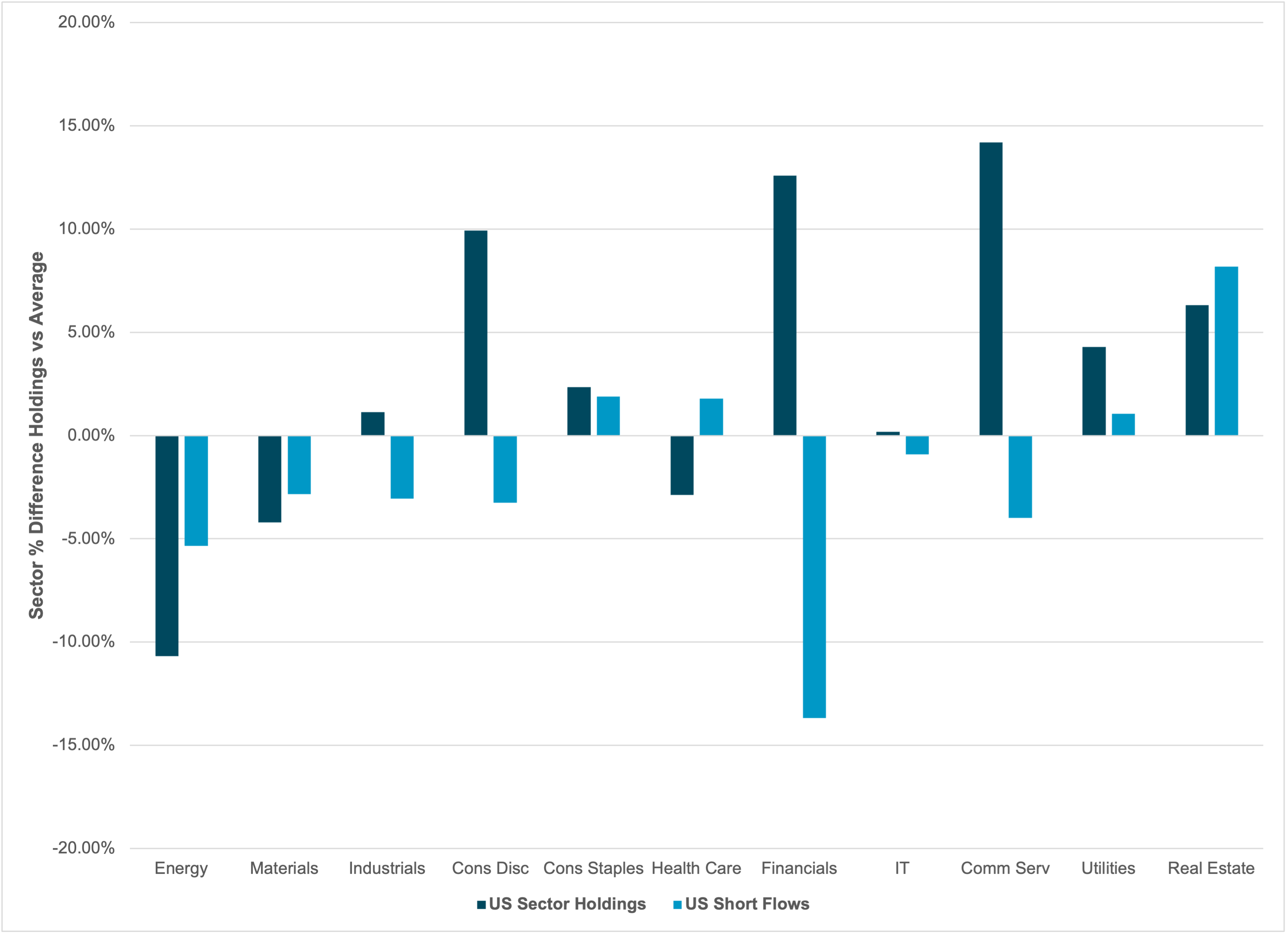

EXHIBIT #5: US SECTOR HOLDINGS AND SHORTS

Source: Bloomberg, BNY

The Trump administration has proposed fees on Chinese commercial ships to counter Chinese maritime dominance. The proposal outlines fees on Chinese-built ships that transport traded goods as well as a requirement that a portion of US products be moved on US vessels. Global merchant shipbuilding is dominated by three Asian countries – China, South Korea and Japan – which together account for over 90% of commercial shipbuilding. The USTR study reports that China’s market share has grown from less than 5% of global tonnage in 1999 to more than 50% in 2023. China owned 19% of the commercial world fleet as of January last year, and it controls production of 95% of shipping containers. The US ranks 19th in the world for commercial shipbuilding. The US builds five ships a year to China’s 1,700. The USTR proposes a $1mn levy on Chinese-built vessels entering US ports and further remedies under Section 301 of the 1974 Trade Act.

Our take

While shipping may be the most vulnerable part of tariffs in the months ahead, US sector holds and the shorts around them may be a better place to watch for a larger risk reversal in March. Equity markets are shifting from US exceptionalism to a US slowdown and a global growth shock. Our holding data, which represent slow-moving unlevered investors against faster, more levered investors using our security lending service, reveals a more specific set of sector risks. The Financial sector has shown an overweight, while short positions hedge that risk, while Utilities, Consumer Staples, Retail Sales, and Communication Services saw inflows.

Forward look

Tariffs take time to make their effects felt – first inventories run down, then domestics replacement goods are found and used, and finally, those items that can’t be found are bought with efforts to pass along the costs. IT, Health Care and Industrials are near flat and have upside potential as the US domestics basket should benefit over the next 6–9 months.

Flows are shifting away from US international champions to domestic ones and from shipping and transport to more service-focused plays such as Consumer Staples and Utilities that endure in weaker economic environments. We see equities at the front lines of a larger global rotation away from US exceptionalism to US isolationism.