Slow but notable progress against involution

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Geoff Yu

Time to Read: 5 minutes

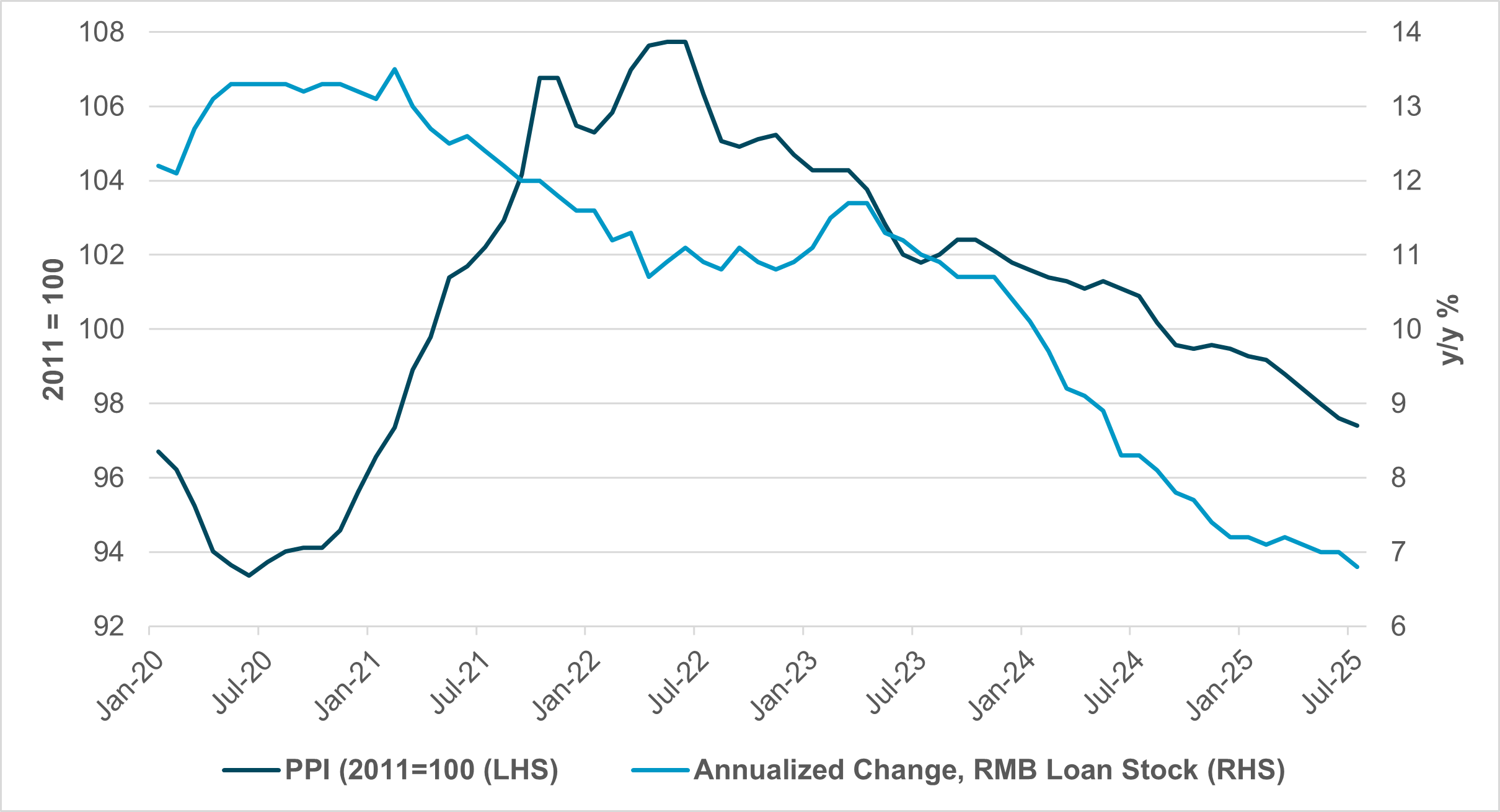

EXHIBIT #1: NEW CNY LOANS VS. CHINA PPI

Source: BNY, Macrobond

Our take

Long before the U.S. moved on tariffs, China’s main trading partners had made strong representations regarding the country’s industrial policy. Capacity generation and supply expansion at scale were difficult for the rest of the world to compete with. Efforts are still being made to manage trade, but clearly some introspection has taken place and Beijing has been vocal domestically in calling on companies across all sectors to end “involutionary” competition. Expanding capacity at the cost of margins and profit growth – which is ultimately feeding through into weak household income and price expectations – is clearly no longer serving the country’s interests, and eliciting a strong reaction globally. “Quality over quantity” is the latest mantra, even if it means companies ceasing production, such as the recent case with a major battery manufacturer’s lithium mine. The campaign has been in place for around a quarter now but there is little sign of change: changing supply dynamics are no guarantee that final demand will adjust in kind. The total social financing report for July showed the biggest contraction in new loans on record. Over the past five years, the halving of loan growth has moved in tandem with falling output prices (Exhibit #1). For borrowers and lenders, it is difficult to make a case for credit growth, even at the lowest possible borrowing rates, when prices ae only expected fall.

Forward look

In an immediate reaction to the July credit figures, the PBoC stressed that it was important to avoid “overhyping” the credit figures. The central bank once again highlighted the recent principle of “quality over quantity,” noting the shift from “involutionary competition” amongst corporates would have a clear knock-on effect on the credit cycle, as “banks are changing their approach – from focusing on size and growth speed to emphasizing quality of service and precision. This transformation leads to a “purifying” effect in overall financial data, as artificially inflated loans are removed.” While we would give this interpretation the benefit of doubt, it is an implicit acknowledgement that previous credit cycles, especially when outright growth figures were high, were lacking in quality. Breaking the link between the credit cycle and corporate profitability has arguably not been attempted over the past two decades. The goals are exactly what China needs but it is important to ensure that, like changes in prices, the process of removing inflated loans doesn’t lead to a self-fulfilling and contractionary credit cycle.

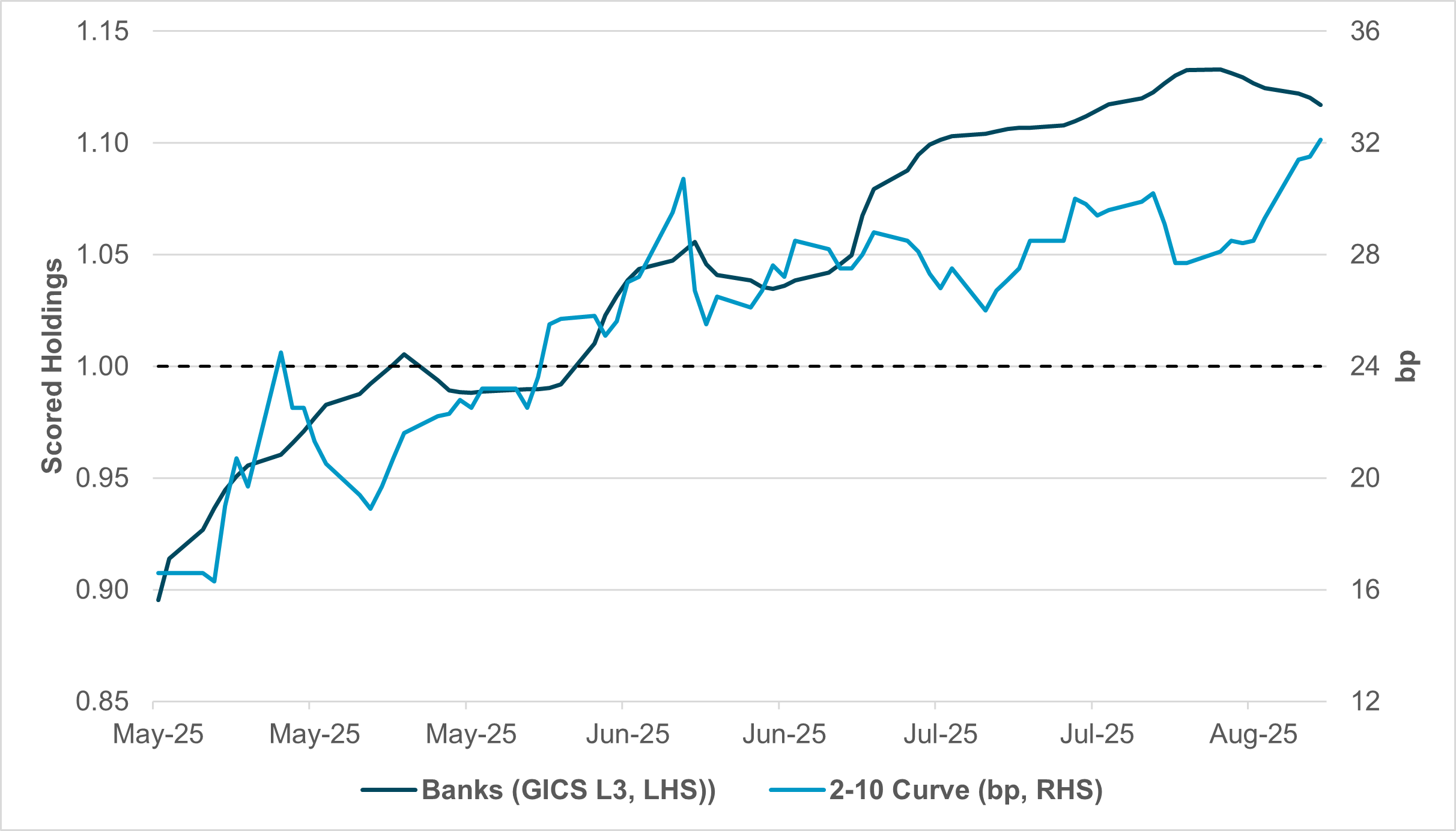

EXHIBIT #2: EM APAC BANK (GICS LEVEL 2) HOLDINGS VS. CHINA 10Y YIELDS (OR CURVE)

Source: BNY, Bloomberg

Our take

Another test of improved quality will be bank profitability, especially in sectors outside of real estate or investment-intensive industries. Incentives are already in place to shift balance exposures, as indicated by the consumer loan subsidy scheme announced this week. The credit figures noted above show that financing costs have not been the main issue compared to lack of demand, as manifested in price expectations and outcomes. However, with the release of the recent core inflation figures, which appear to be moving to sustainably positive levels, yield curves have finally started to shift, which will be crucial for banks’ profitability up ahead. Meanwhile, markets are taking notice as well: after spending much of the year in the doldrums, there has been a sharp pick-up in banking sector holdings in EM APAC (Exhibit #2), with Chinese names dominating, even without any discernible pick-up in growth. However, yield curves are starting to move, which bodes well for future profitability, assuming credit growth can stabilize.

Forward look

It is difficult to make an extraordinarily bullish case for financials based on the steepness curve alone, especially with loan books contracting. Furthermore, the defensive aspect of financials in emerging markets – many of which have explicit or implicit state support – is likely attracting interest as general diversification away from highly-valued developed market sectors is a growing theme. For cross-border investors, such names are often the easiest to access. Nonetheless, we believe asset allocation will also increase the “risk” that China’s involution efforts will prove more sustainable and support “high-quality” credit impulse further down the line. The recent turnaround in government bond yields suggests that initial guidance on price outcomes for corporates is bearing fruit. Net interest margins for Chinese banks have fallen sharply over the last decade, declining from more than 2.5% to 1.4% as of Q1 2025. The base is very low for improvement, but the onus is now on policy execution.

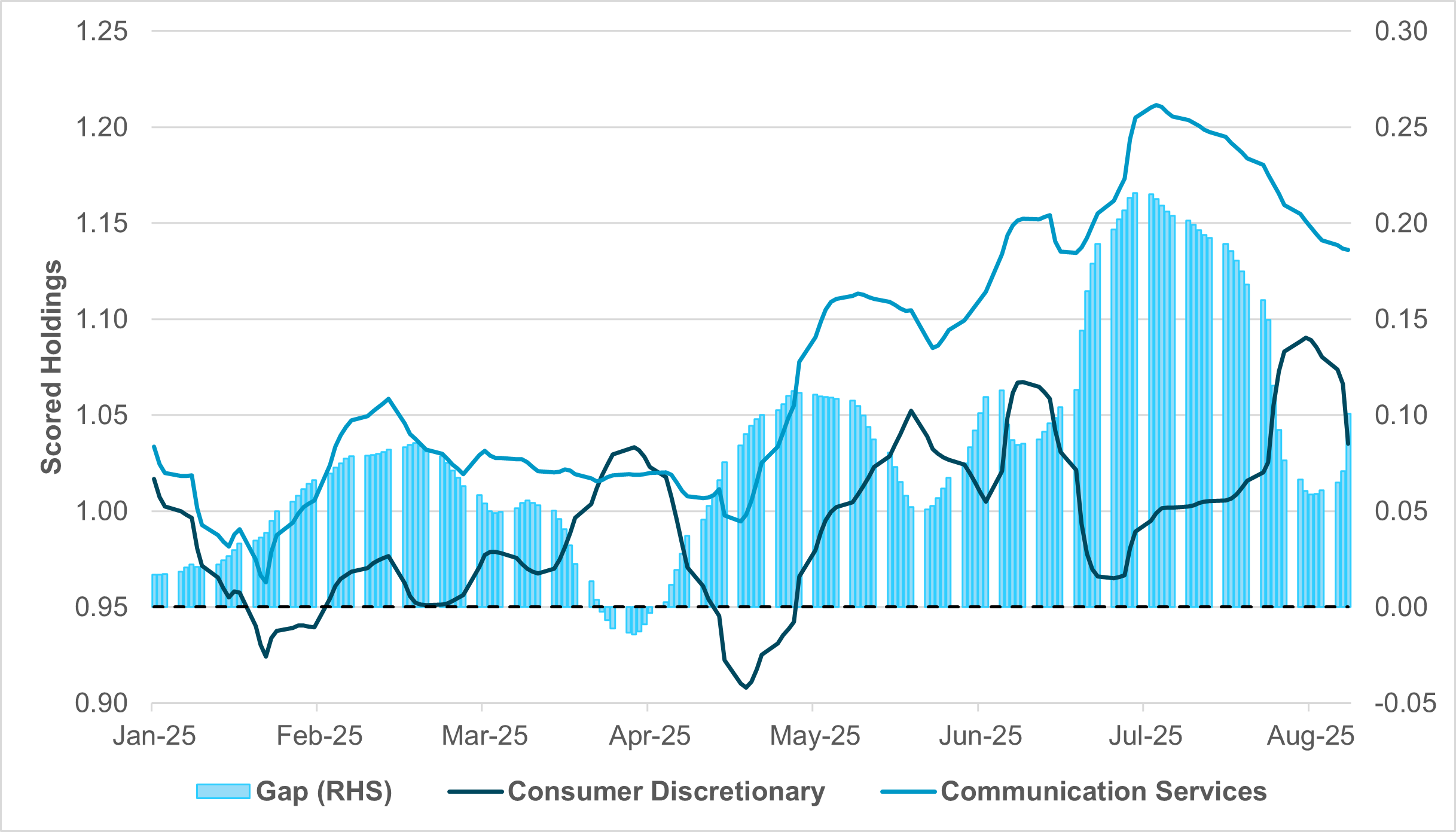

EXHIBIT #3: EM APAC EQUITY HOLDINGS, CONSUMER DISCRETIONARY VS. COMMUNICATION SERVICES

Source: BNY

Our take

After fading into the background for several years, “dual circulation” is making its way back to the forefront of policy statements, led by domestic circulation, i.e. domestic demand. Traditional, public investment-driven demand such as infrastructure will remain in place, but household consumption is moving to the fore. Beijing’s recent launch of a childcare subsidy – called the largest direct household subsidy in the country’s history – is a clear sign that the government is no longer averse to direct injections. As many central banks and finance ministries have noted in the past, the struggle lies more on the spending side, and measures are needed to ensure that disbursements are not simply saved. More support may come, and we still do not rule out tax relief along the lines of the 2019 round of direct household fiscal stimulus, but asset allocators remain very hesitant to take a structurally positive view of the consumer side across EM APAC due to so many false dawns. Recent policy efforts have clearly triggered a reaction in August, but the gap against the most favored EM APAC sector – communication services – remains wide.

Forward look

As global equity positions continue to favor AI and tech, given the well-established prowess of Chinese firms in these sectors, a natural rotation toward communication services is understandable. Yet, the key issue is whether “rotation” itself is the right strategy, as if there is sufficient investment and productivity growth contribution from these sectors into the broader economy, household real incomes can benefit and support consumer-exposed sectors as well. Governments across the world have acknowledged that translating current advances across industries, especially technology, into better employment growth is a major challenge. Nonetheless, Beijing is in a better position to optimize the distribution of gains and losses, so the holdings gap between household-related and tech-based sectors should not be particularly wide. In the near term, however, holdings in EM APAC in general appear to be stagnating, suggesting cross-border investors are skeptical of fresh earnings catalysts.

The change in mindset for industrial policy in China is very real and will help stabilize expectations over time. Over the years, the term “involution” has evolved from household nomenclature into the corporate scene to describe diminishing returns from competition. However, the hope is that ultimate outcomes will reverberate positively back into household expectations, and we would expect the phrase “quality over quantity” to be used much more often up ahead, and not just in the context of data outcomes. In the short term, asset allocators will unlikely see immediate results in earnings or macro data. Nonetheless, key sectoral beneficiaries are clear and we anticipate continued improvement in flow and holdings, especially from domestic investors, over the medium term.