Retail doesn’t always win

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

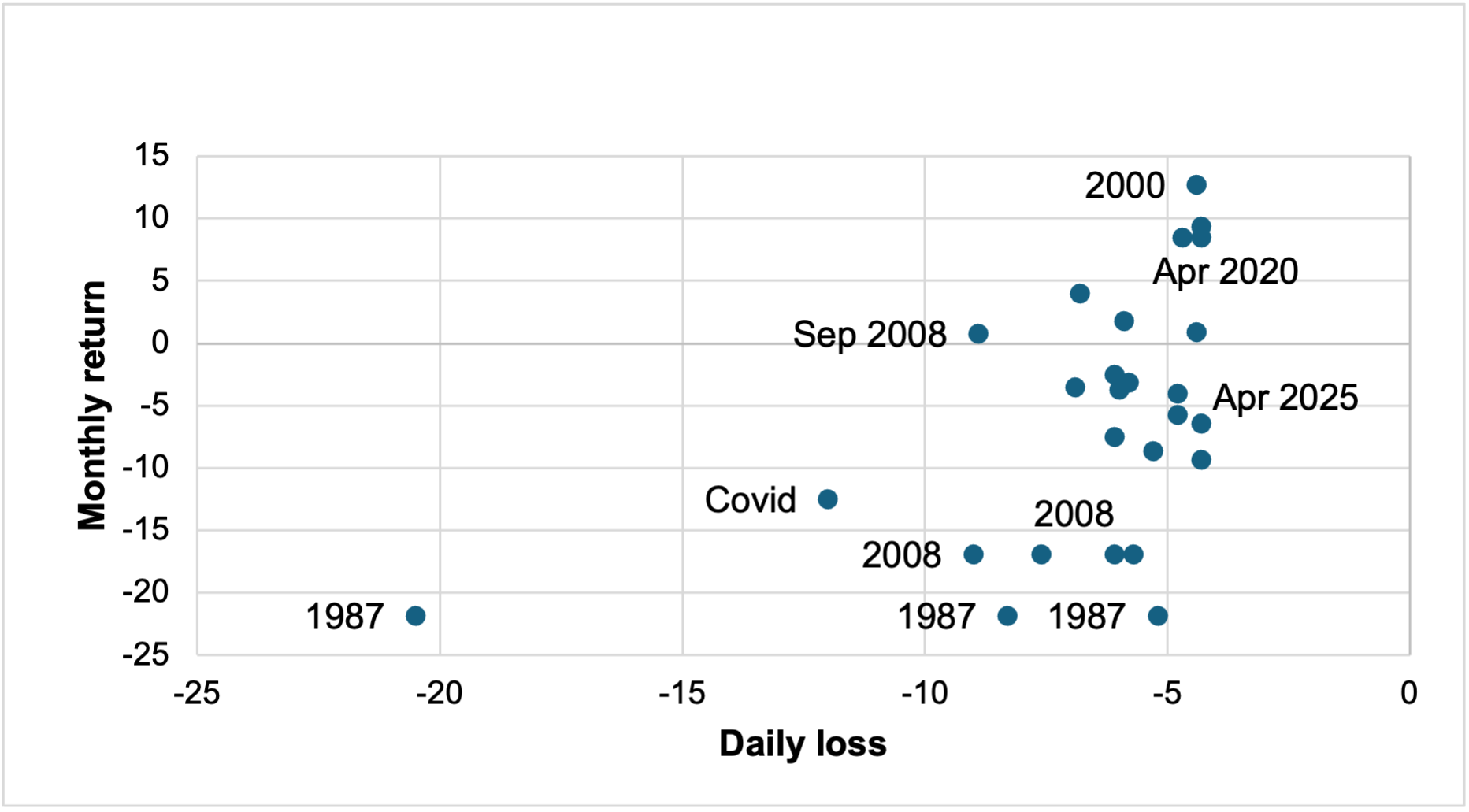

EXHIBIT #1: TOP 25 S&P500 DRAWDOWNS

Source: BNY, Bloomberg

The focus on retail over institutional money flows has been a long-standing tradition. Compared to larger institutional flows, retail has smaller tickets, trades less frequently and has a higher correlation to trend. However, in times of stress, retail buyers can help define tops and bottoms for markets via the animal spirits they unleash. There is a Wall Street adage learned during Covid and Meme stock eras saying to “never to fade retail flows”. Buying a 2% dip in the S&P500 makes money, but some analysts argue this is a sample error from the last 5 years. Many of the current U.S. retail traders in stocks have less than 10 years of experience, meaning they missed the pains of 1987, 1997, 1998, 2001, 2007 and 2008. The bigger question is whether there is a signal that can help differentiate when retail is proven wrong.

Our take

The last 5 years have had a 10% return using a straightforward process: buy-the-dip when the S&P500 moves more than 2%, hold for 1 month, then sell. This method has worked 75% of the time. The holding period could be longer, but that increases risk and volatility versus reward. The notable lesson post-Covid has been that markets are orderly and protected by policy expectation shifts. Retail investors have learned this lesson and were key drivers for overall market shifts in sentiment. The problem arises when drawdowns in equity markets are larger than 2%. The last 75 years of the S&P500 show that buying the dip doesn’t work, and instead loses 75% about 7% of the time. Buying during a bigger drop in stocks is only successful when the Fed eases. The bounce back last week was due to the pause on tariffs causing policy shifts, not monetary policies. Trade talk will prove if these changes are sufficient.

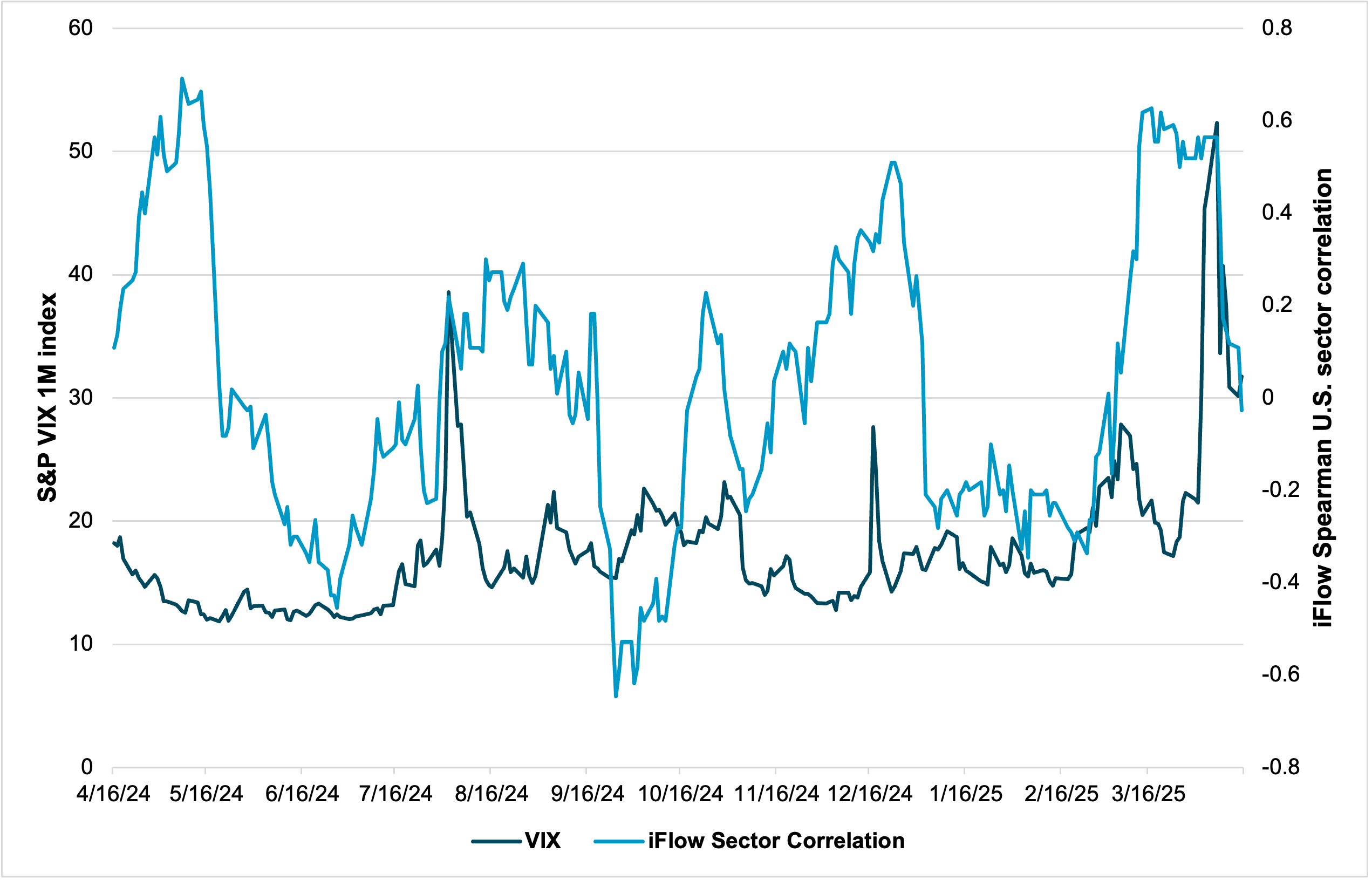

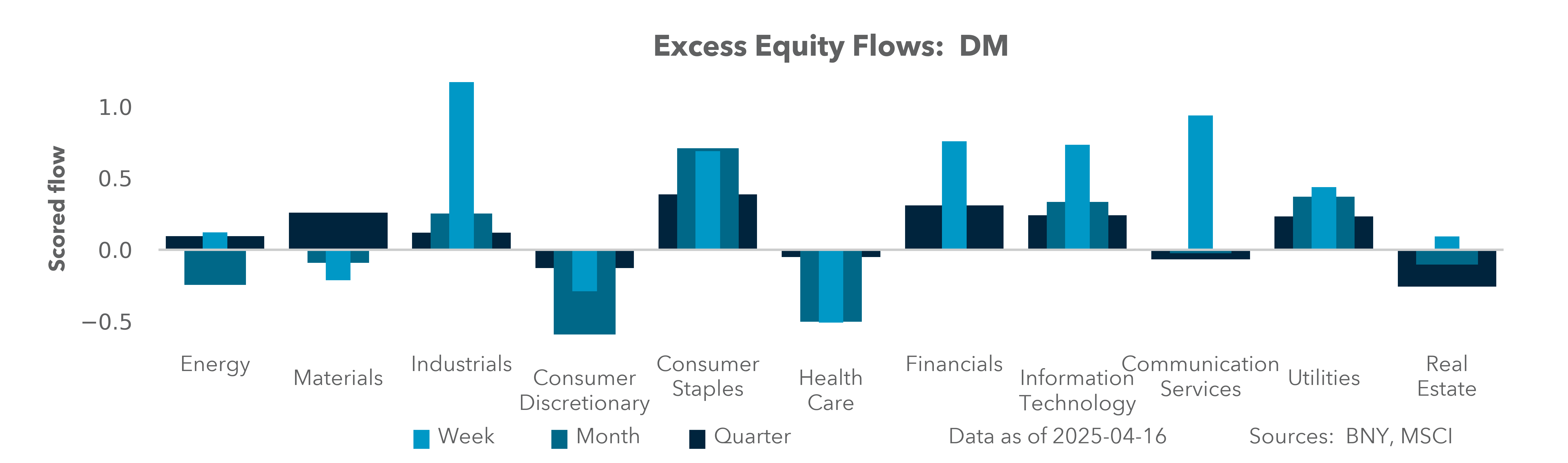

EXHIBIT #2 : IFLOW U.S. SECTOR CORRELATION VS. VIX

Source: BNY, Bloomberg

Our view

In the last 3 weeks of trading, investors saw a sharp rise in the VIX index, suggesting volatility was overwhelming returns. Our data suggests that institutional investors cut back risks in an orderly outflow. These changes can all been linked to uncertainty around U.S. tariffs and policies. Notably, in March and April our flow showed less stock picking and broader stock indices trading. This is where institutional flows and retail flows interact. Buying U.S. shares on the biggest outflows were mostly in ETFs linked to the S&P500 and the NASDAQ 100. The Magnificent 7 also played a role but little else was bought otherwise. The correlation between sectors for our institutional flows peaked last week and has since fallen from 0.55% correlation. This suggests a broad market deleveraging, rather than any one sector or set of stocks being sold. The April 3 and April 4 retail buying against ongoing volatility peaking stands out in our flows, showing “retail” interest at 2-3 times the normal amount for the month.

Forward look

The key component for equity market instability is how stocks trade as a market or a diversified bottom-up set of equity names, albeit at elevated volatility. Some of this information shows up cyclically in earnings seasons. Micro meets macro over the next 3 weeks while retail takes a pause and waits for institutional flows to lead. We see a high correlation of trading ETFs to retail dominance over institutional uncertainty.

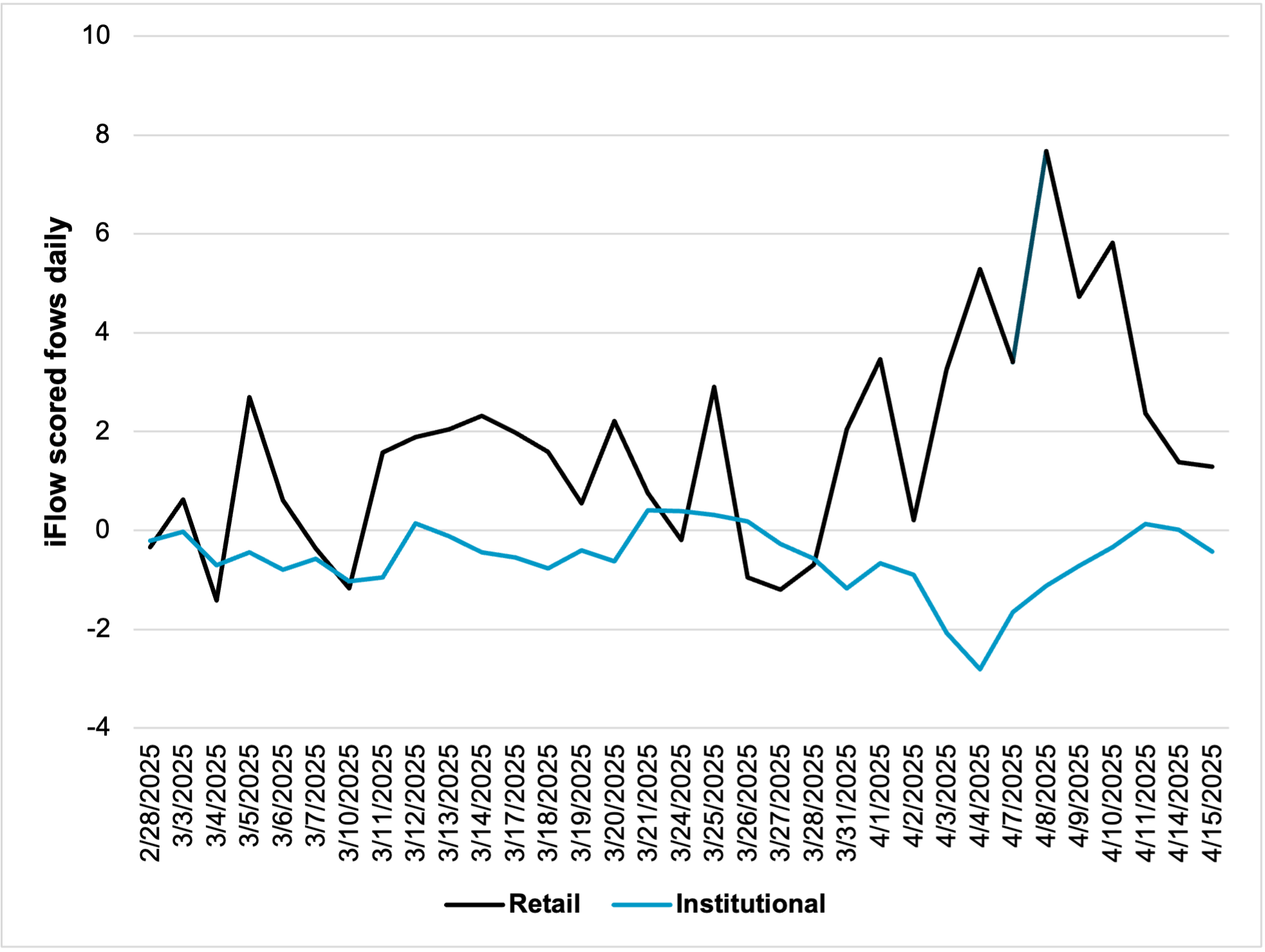

EXHIBIT #3 : INSTITUTIONAL VS. RETAIL FLOW FOR U.S. EQUITIES

Source: BNY

On April 3 and 4 our data was dominated by retail flows volume spiking to 2-3 times the normal amount. Buying the SPY and VOO ETFs (S&P500) accounted for most of the flows, supported by some Magnificent 7 names. The lack of retail buying in fixed income ETFs over the last month started to switch this week but remains lower than January or February levels.

The role of “buying the dip” relates to the view of how long markets can last in a volatile and negative return state. The problem for investors simply following the retail buyer - or just buying every big dip in markets - is that this method can fail. The start of Q2 equity market trading has been notable for its volatility and persistence. Historically, the top 25 biggest S&P500 drawdowns show that only 25% have positive returns. This is a warning shot for April 2025, and I bought this dip. Outsized moves down have a tipping point linked to volatility and the state of the economy. The shocks of 1987 and 2008 were memorable, but still less painful than post-March 2020. The risk for the rest of April rests on how the FOMC reacts to financial conditions. The history of 2008 trading suggests you need bigger policy turn to get the dip to work.