Q3 Rebalancing and Risk

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

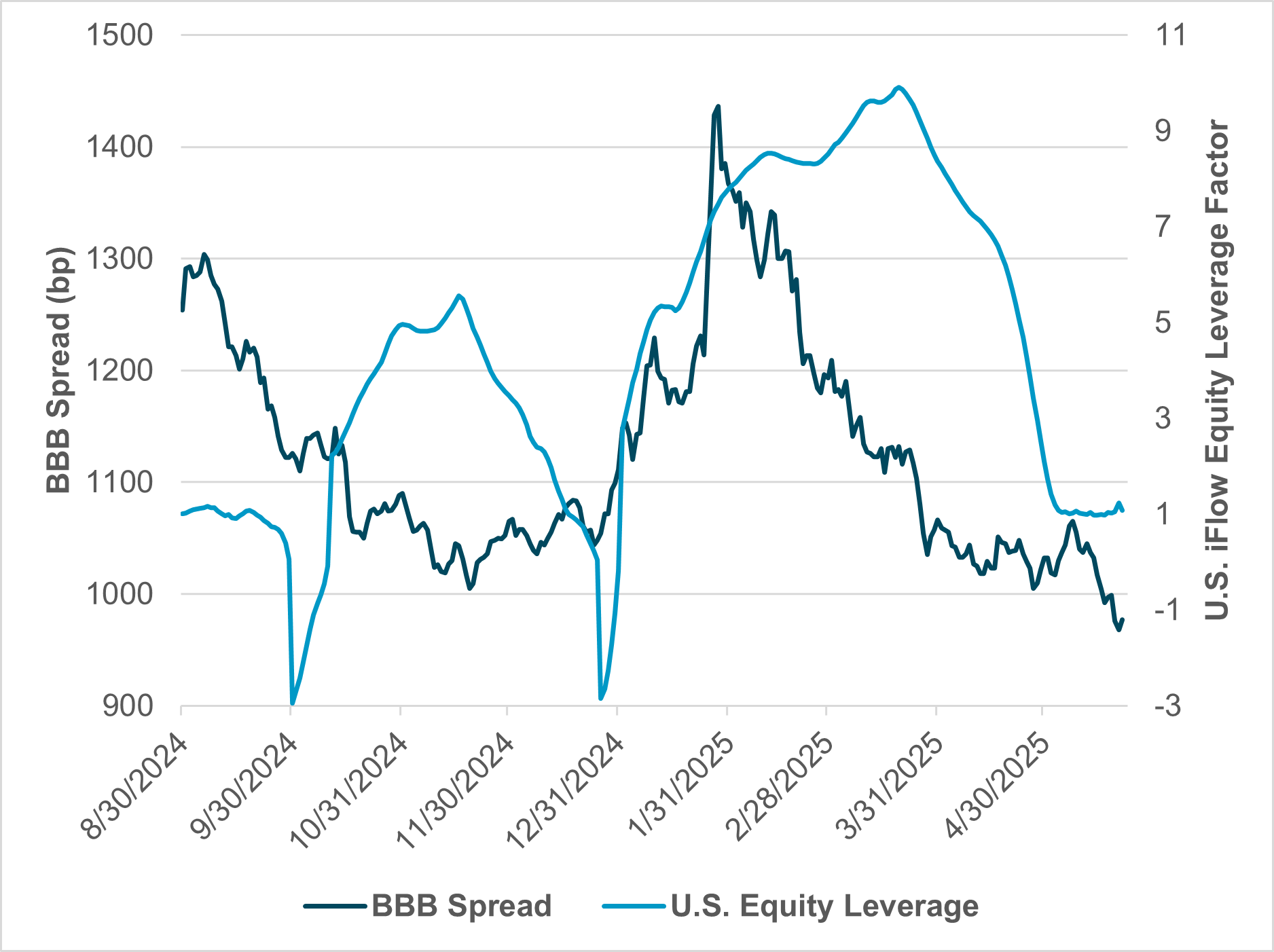

EXHIBIT #1: U.S. BBB SPREAD VS. IFLOW EQUITY LEVERAGE FACTOR

Source: BNY, Bloomberg

Our take

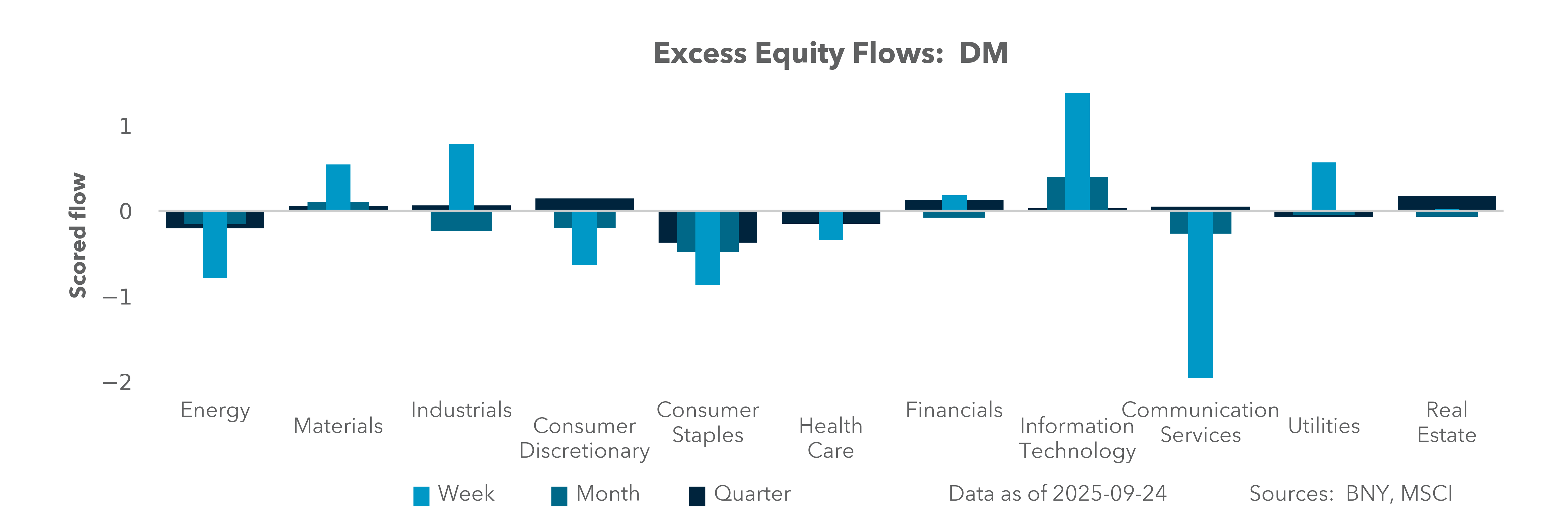

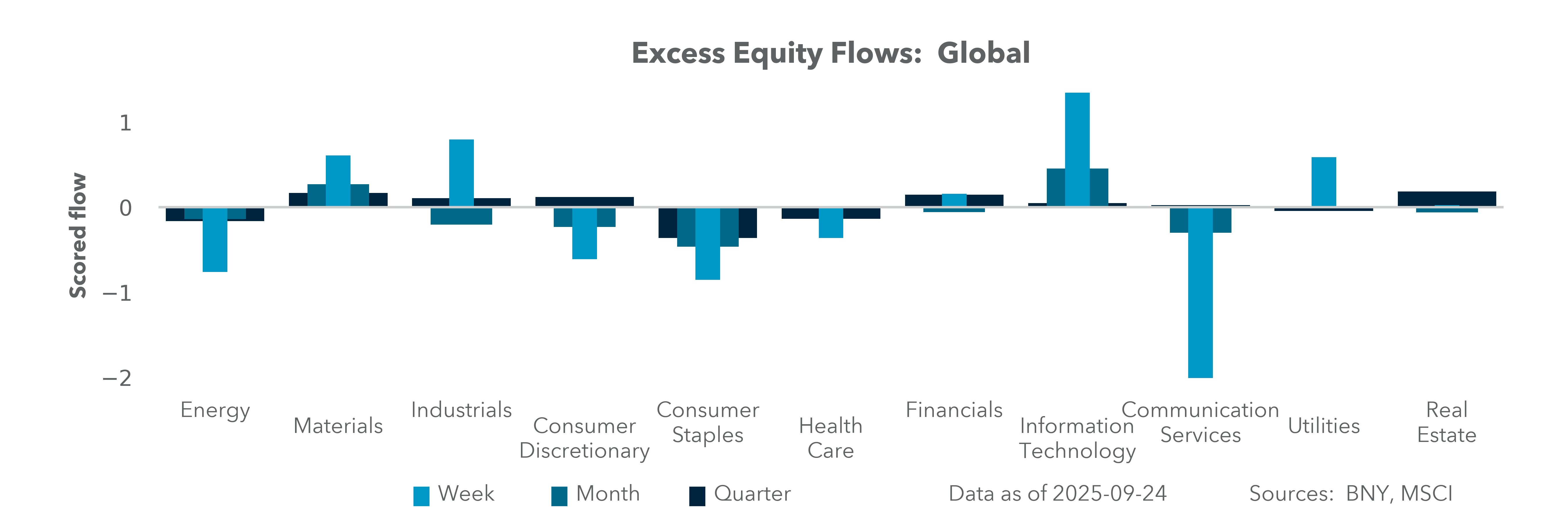

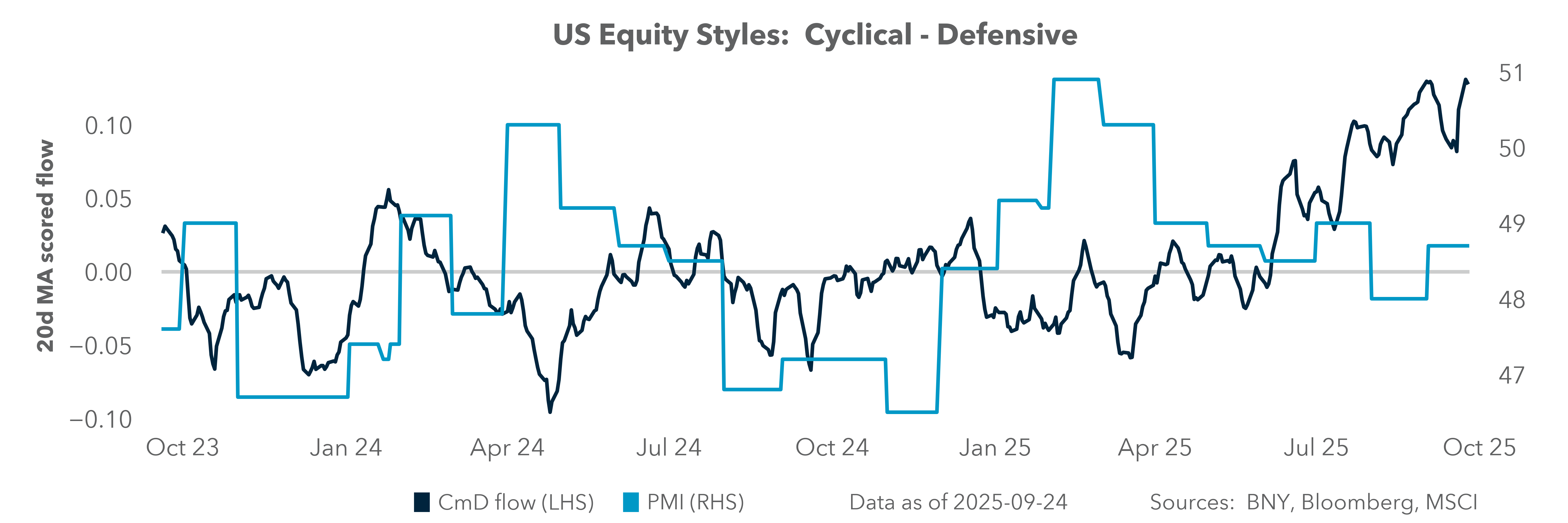

After posting new highs on Monday, U.S. equity markets sold off this week. iFlow shows clear defensive sector rotational moves by clients. Selling overheld Nasdaq shares into underheld Russell 2000 stocks has been a notable trade for the quarter and the month, with small companies that are interest rate-sensitive beating out higher valuation shares. Our institutional holdings fell 9% for both the IT and Communications sectors, but Consumer Discretionary and Financials were also sold – sometimes as proxies for the Russell 2000 – albeit selling from a lower base of holdings. Outside of our flows, the equity option markets also show more interest in the downside rather than in rotational trading. The set-up for fast money is not a Russell 2000 rally, but rather a reduction in overall risk, given the tail risk of a recession over a soft landing. The biggest divergence in our iFlow signals shows up in trend factors, which are positive against the 0.8% w/w drop in QQQ and IWM, even as the price of these two ETFs remains over the 200-day averages.

Forward look

The lack of credit spreads has led to concerns about the correct risk/reward balance in leveraged accounts. We have seen a notable drop in leverage as a factor even though the FOMC has restarted its easing cycle. Recession fears in July 2024 spurred the Fed to cut rates in September 2024, but this is not the same price action we are seeing now. Real money investors are set up defensively, with spreads narrowing, adding to the logic that risk premiums do not justify overweight positioning into Q4. The upside to the Russell 2000 is the greater growth potential as a result of the policy shift to deregulation under the Trump administration as well as depreciation tax reform along with the potential for AI to boost productivity as the technology allows smaller companies to see faster benefits. The extension of the credit cycle for the Russell 2000 rests on economic data for the U.S. being “just right” for Fed cuts without inflation eroding margins. Investors are likely to wait until the next Fed meeting at the end of October before fully embracing the rate cut rotational trade of the Russell 2000 vs. the Nasdaq 100.

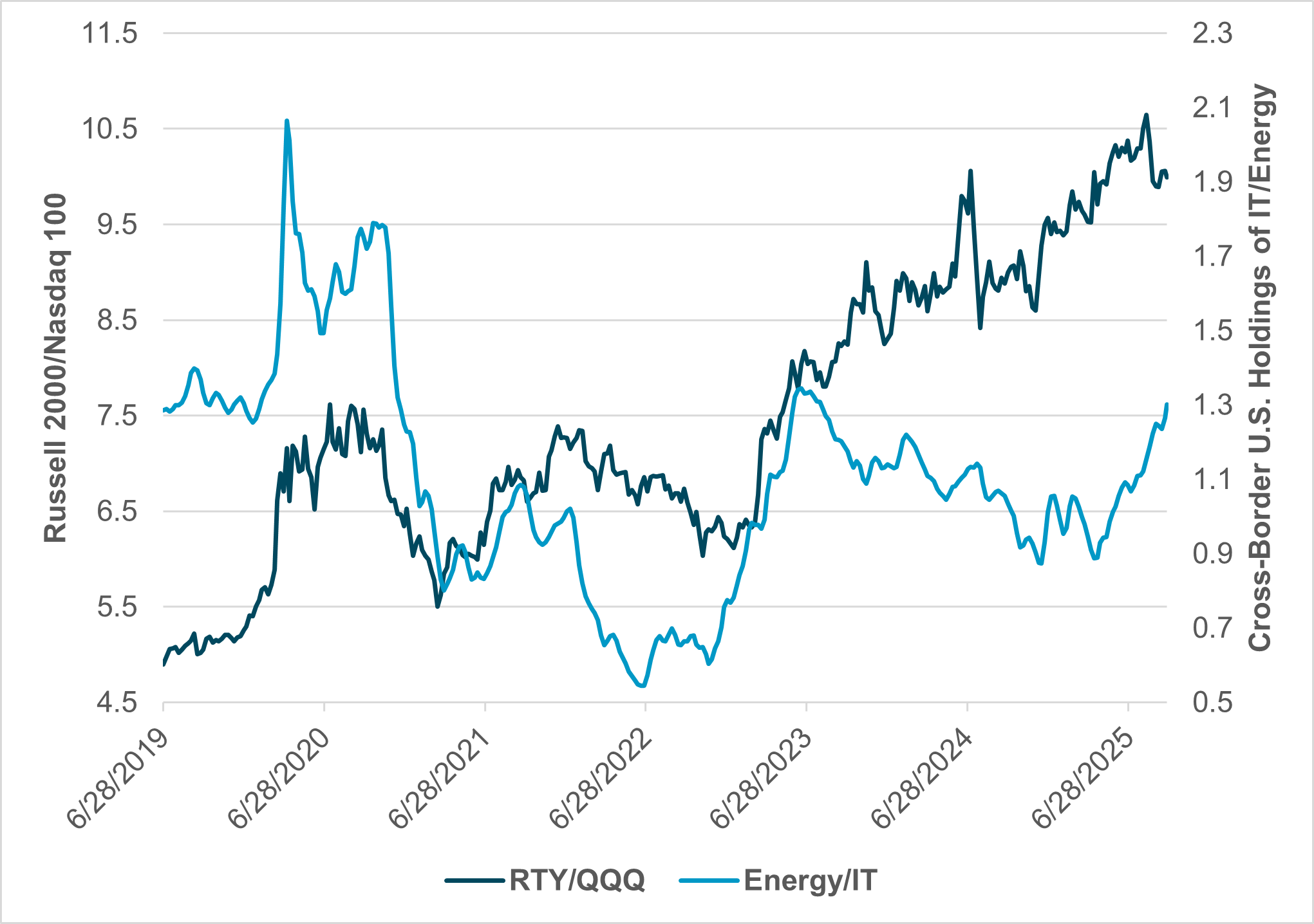

EXHIBIT #2: NASDAQ 100/RUSSELL 2000 VS. CROSS-BORDER U.S. HOLDINGS OF IT/ENERGY

Source: BNY, Bloomberg

Our take

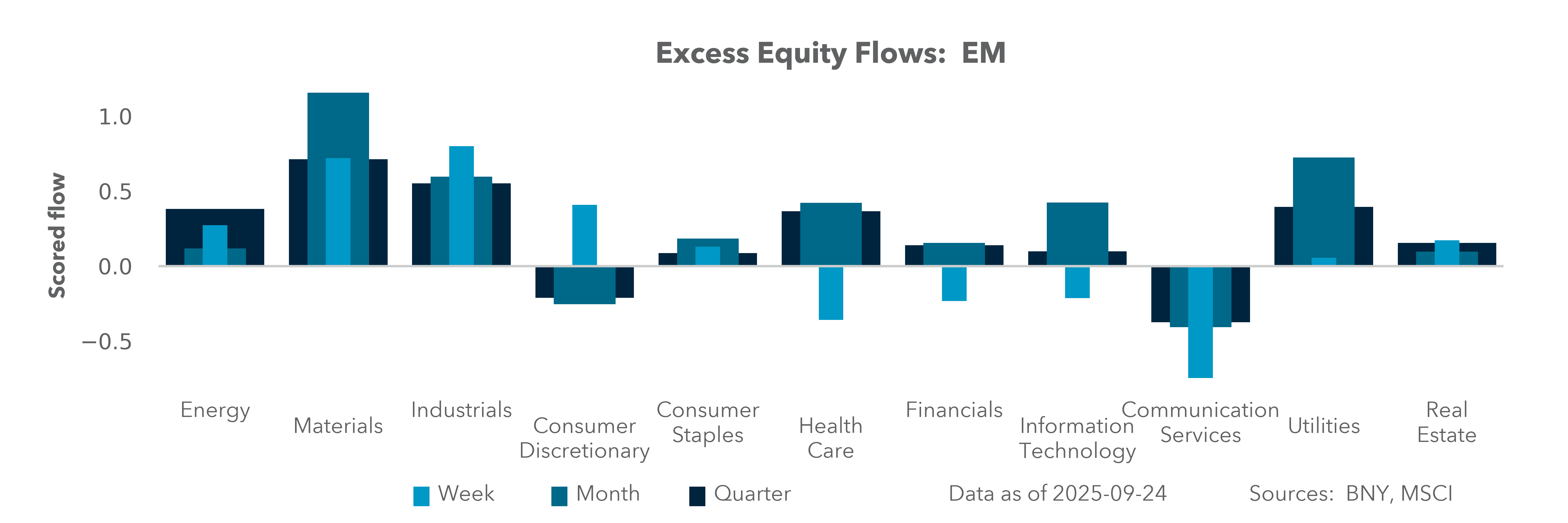

The Nasdaq outperformance from 2022 to now has been led by AI. Large tech names have led the rally, but there have been moments of volatility, and for many this week was a testing one given pressure to reweigh portfolios into the end of Q3. The week’s interesting flows are in the rejection of thematic ETFs for more stable large caps, which suggests a shift from growth to value, with recession fears offset by rate cut hopes. Our data suggests that critical flows for a larger SME rotation trade will depend on demand by cross-border investors. We see the dynamic tension between IT and Energy investments as a good proxy for the current uncertainty. For investors, an extension of U.S. equity market exceptionalism will require more cross-border buying of IT over defensive plays in Energy, Health Care or housing. There is room for this trade, but it clashes with the U.S. rotational trades that are in play this week.

Forward look

Tech valuation concerns this week are related to credit, with the Oracle $18bn bond issue being one example of demand finding a limit. The other valuation risk is vendor financing concerns. The Nvidia investment in OpenAI raised such concerns for some analysts. However, such arrangements can help scale the ecosystem for AI and add to the hopes for SME adoption for better growth and productivity into 2026. When financing becomes widespread, large-scale and dependent on optimistic assumptions, then previous credit bubbles become more pertinent to current valuations. The downside risks for markets both IT and SME are that rate cuts will be insufficient to prevent a larger U.S. slowdown. The negative headlines about Tricolor and credit standards add to views that we are approaching extra innings for the U.S. economy baseball game. Our data suggests that this risk has been part of the playbook for both domestic and foreign investors most of the year. What is not priced is the risk of fewer rate cuts ahead, driving concerns about leverage and debt, with curve steepening the duration limit for investors that feeds back into stocks.

As we move into Q4, portfolio positioning remains defined by defensive rotations, narrow credit spreads and a cautious read on Fed policy. The balance between equity upside and credit risk looks increasingly asymmetric, with IG issuance near record highs and vendor financing dynamics raising questions about leverage sustainability in both IT and SMEs. While Russell 2000 valuations appear attractive on a relative basis – supported by deregulation, tax incentives and potential AI-driven productivity gains – the trade still requires confirmation from cross-border flows and steadier macro data. Narrowing spreads and reduced leverage suggest real money investors are prioritizing risk management over chasing incremental upside. With rate cut expectations now the key pivot, markets are likely to wait for October’s FOMC before committing to a broader rotation. Until then, equity managers should assume that credit is the constraint and volatility the risk premium, even as long-term growth narratives remain intact.