Q3 Earnings Primer: Good, Not Great

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

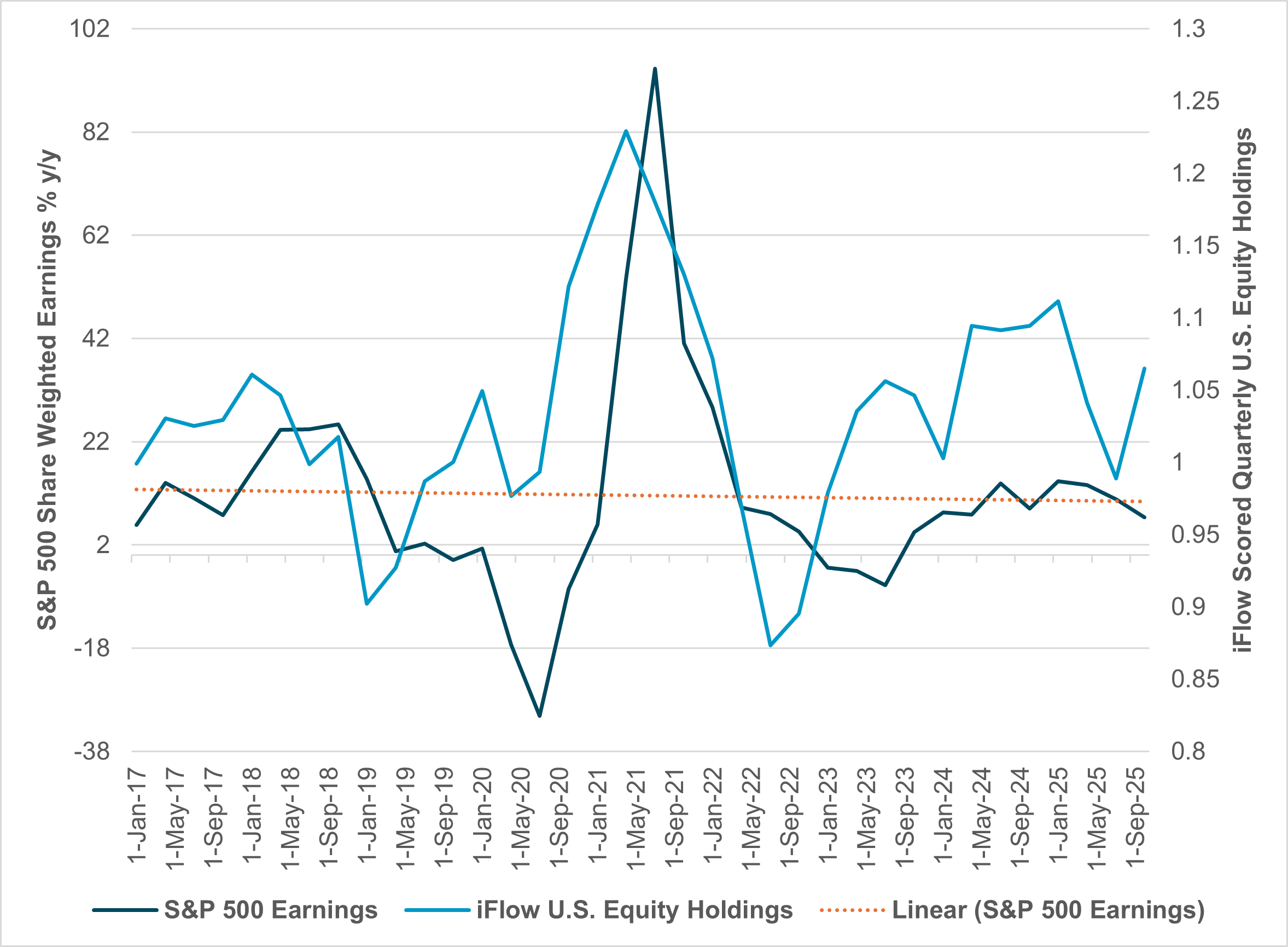

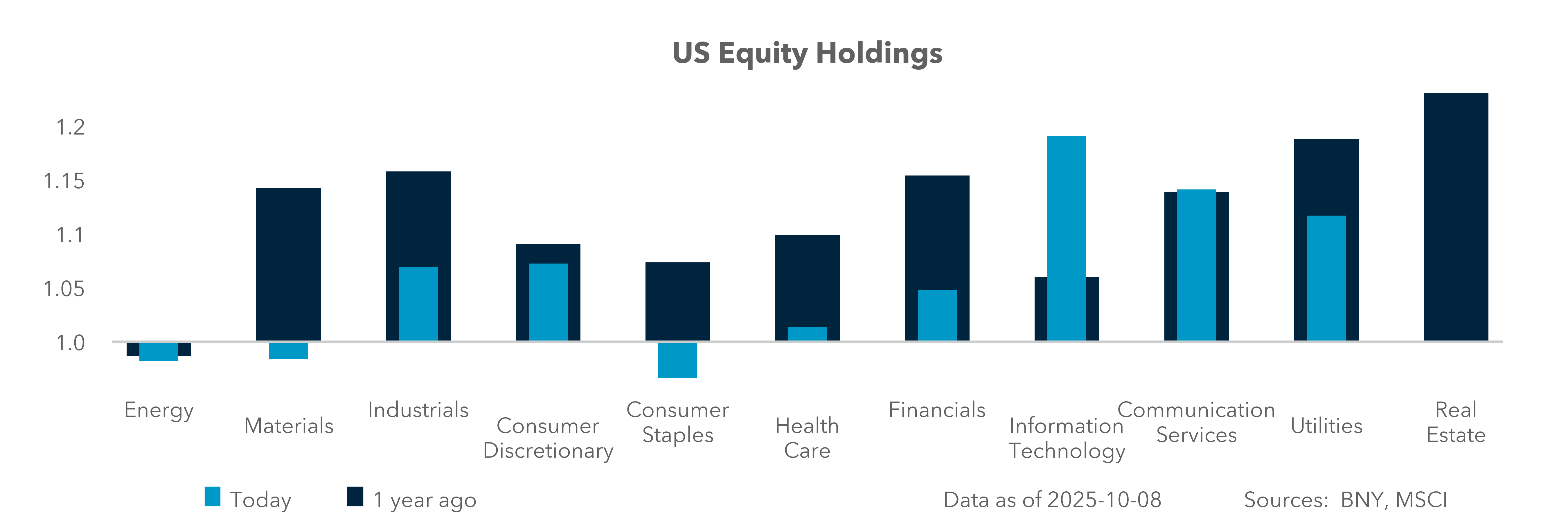

EXHIBIT #1: U.S. EQUITY HOLDINGS VS. SHARE-WEIGHTED EARNINGS

Source: BNY, Bloomberg

As Q3 earnings season gets underway, the key question for investors is: Are markets priced for them? Consensus calls are for Q3 earnings of 8% y/y, with whispers of 10%. If this is indeed the case, it would be the ninth consecutive quarter of gains, albeit lower than the 13.8% we saw in Q2. This is good, not great, contrasting with the price gains for U.S. markets we have seen in the past. The sector EPS growth consensus is also balanced: Industrials and Materials had significant gains of 30%, Technology posted an increase of 20%, and there were also solid gains in Consumer Discretionary and Health Care. The one sector expected to see a decline in earnings is Utilities.

The list of concerns expressed on CEO conference calls is long and includes tariffs and supply chains, margin squeezes and cost pressures, credit risks from sub-prime consumers and global growth. The main concern revolves around valuation and the breadth and strength of earnings against the expectations of more Fed rate cuts and a stable economy. Market risk is acutely concentrated in mega-cap tech and AI stocks, making the index highly vulnerable to downside surprises. However, this is not a new fear and is offset by the outperformance of earnings.

Our take

Overall, the biggest risk for Q3 earnings may be the lack of negative guidance, with the ratio of 1.4 to 1 near the historic low end, suggesting less fear about the economy and earnings ahead. However, investors are not set up for the usual post-earnings rally. There is a defensive posture to holdings, albeit one that is not prepared for tail risks of a recession or ongoing melt-ups. We see significant concentration risk from both domestic and foreign investors in U.S. tech wrapped around the AI theme but little faith in the usual rate sensitive sectors recovery. S&P 500 options confirm the defensive posture. SPY Strikes 668–672 dominate both calls and puts, with the put/call ratio at 1.32 and put open interest nearly triple that of calls – reflecting an institutional bias to maintain downside hedges, not a directional conviction.

Forward look

There is a significant correlation between equity holdings and actual earnings. While not a perfect indicator, the bounce in holdings after June 30 suggests investors are prepared for better earnings across the S&P 500. The normalization and broadening of returns beyond the Magnificent Seven basket of Big Tech companies is important for how the risk of a correction bears out. The current earnings season will be scrutinized for a bounce-back to the 8% y/y trend. While this has been priced, our holdings suggest investors expect more. Big Tech, with earnings in excess of 20% for each of the past four quarters, plays a leading role but is unlikely to sustain these numbers. However, this concern will subside if the U.S. cuts rate and recovery from concerns about less trade shows up in margins and profits. Whether we experience a correction or not will depend not just on Big Tech, but rather on all overheld positions in the U.S.

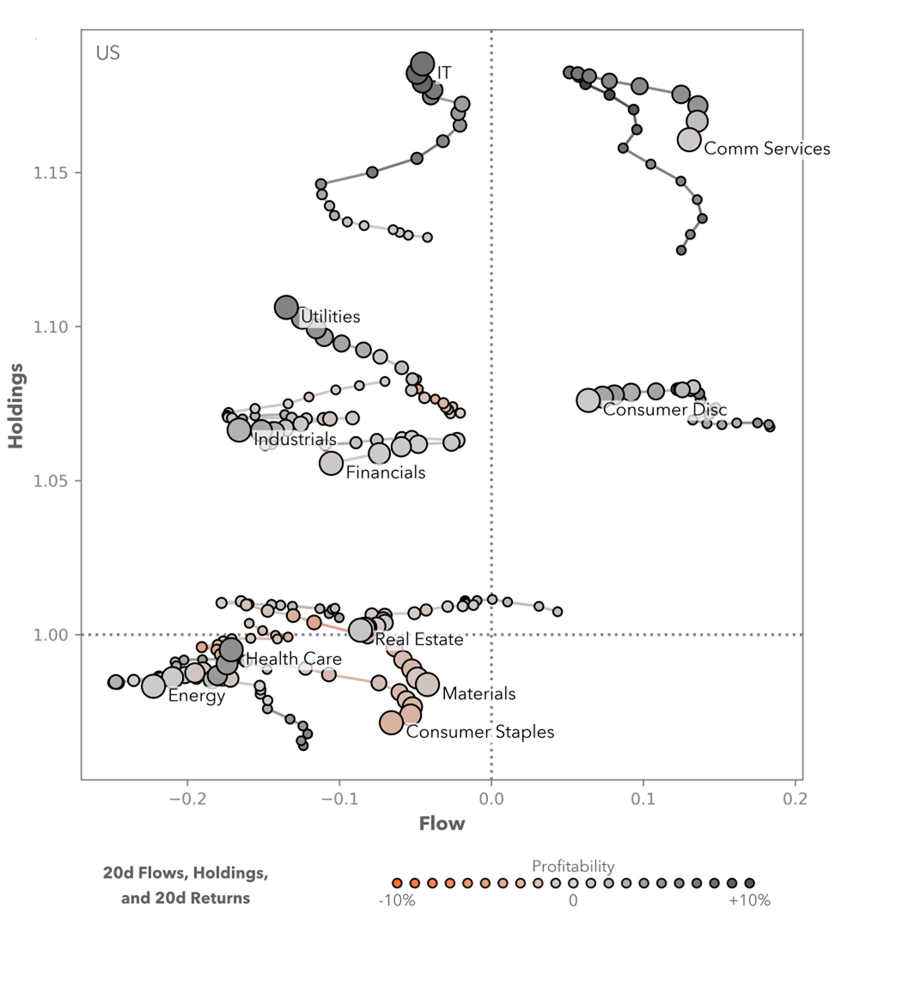

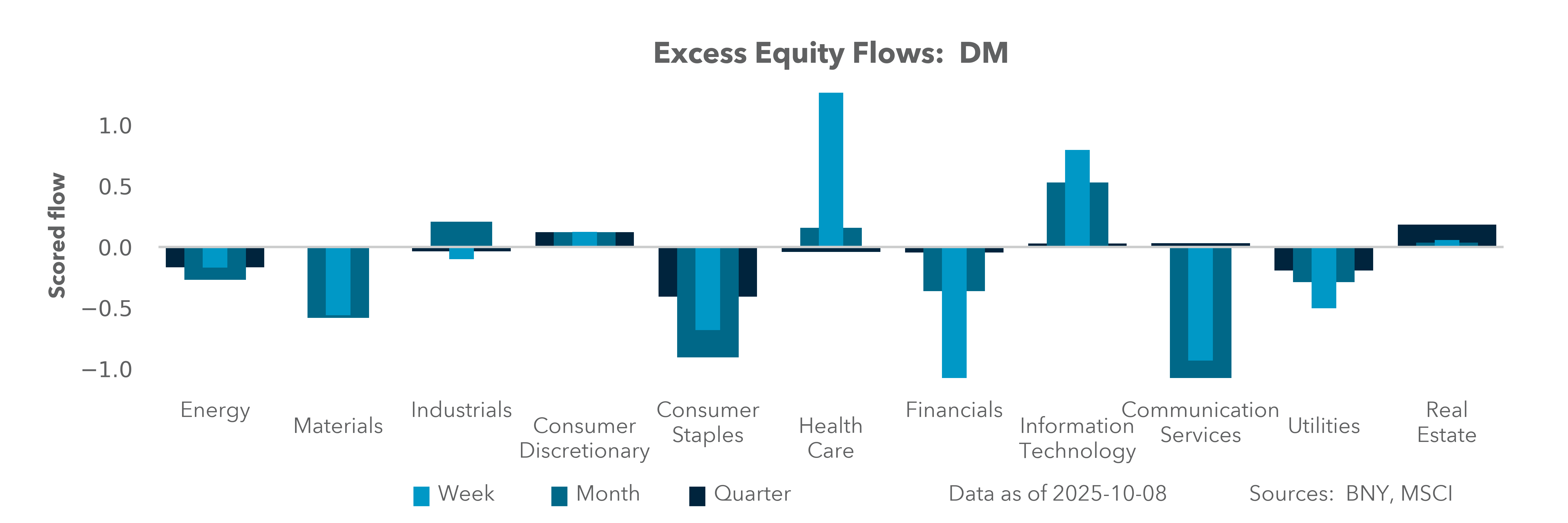

EXHIBIT #2: U.S. HOLDINGS AND FLOWS IN WITH 20-DAY TRACKING OF S&P 500 SECTOR SHIFTS

Source: BNY, MSCI

Our take

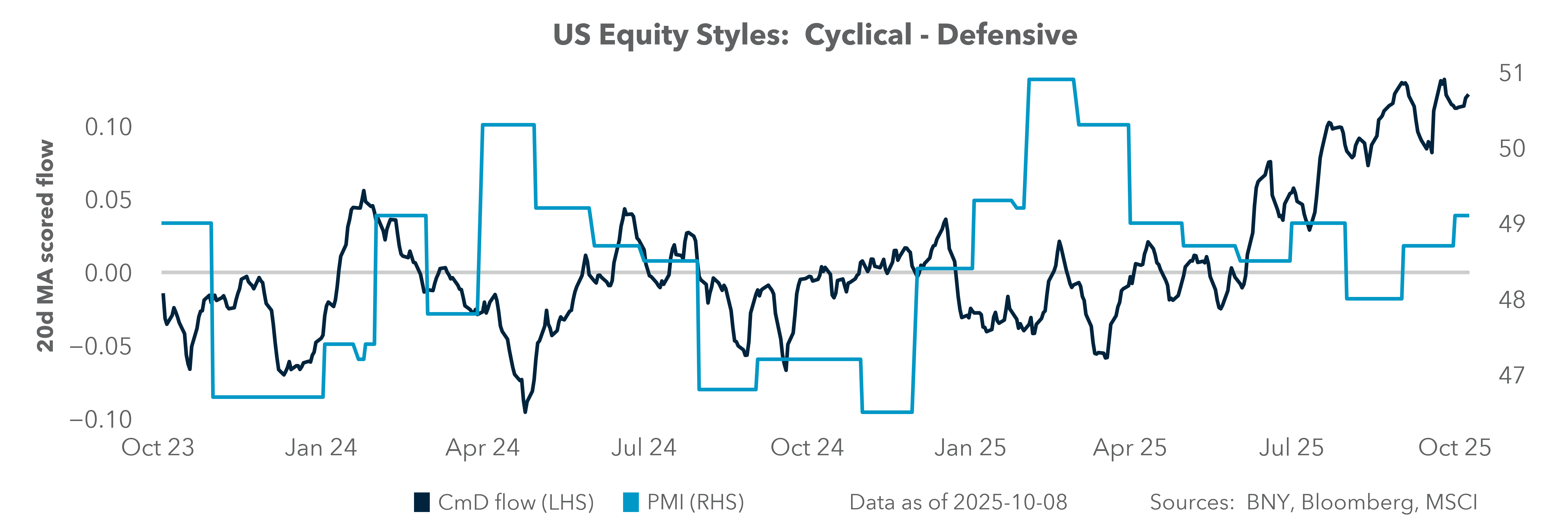

Risk trading as we head into Q3 earnings season has been defensive. The only two sectors seeing new inflows against long holdings are Consumer Discretionary and Communication Services. Against that we are seeing short holdings and further selling of Real Estate, Health Care, Energy, Materials and Consumer Staples. In addition, holdings of IT, Industrials and Financials have seen outflows, although holdings are still higher than average. Exhibit #2 shows the direction of travel of flows and holdings, with the vertical lines suggesting trend-chasing, and the horizonal ones suggesting indifference. This indicates that the only two sectors where trend-chasing shows up are favorites IT and Communications Services.

Forward look

U.S. holdings are not set up for a bounce-back in earnings but rather a marginally weaker outcome. We are priced for good, but not great overall results, as holdings suggest that investors expect an ongoing bifurcation of earnings between the technology and communications sectors and all other sectors. The lack of aggressive positioning suggests that the risk for Q3 results is a gradual and grinding melt-up in equities. The bar to clear is low. Actual U.S. Q3 economic growth looks to be closer to 2.0–2.5% rather than the blue chip consensus of 1.5%. How that growth shows up in Q3 earnings will be watched closely, with a focus on supply chains, inflation pass-throughs and margins.

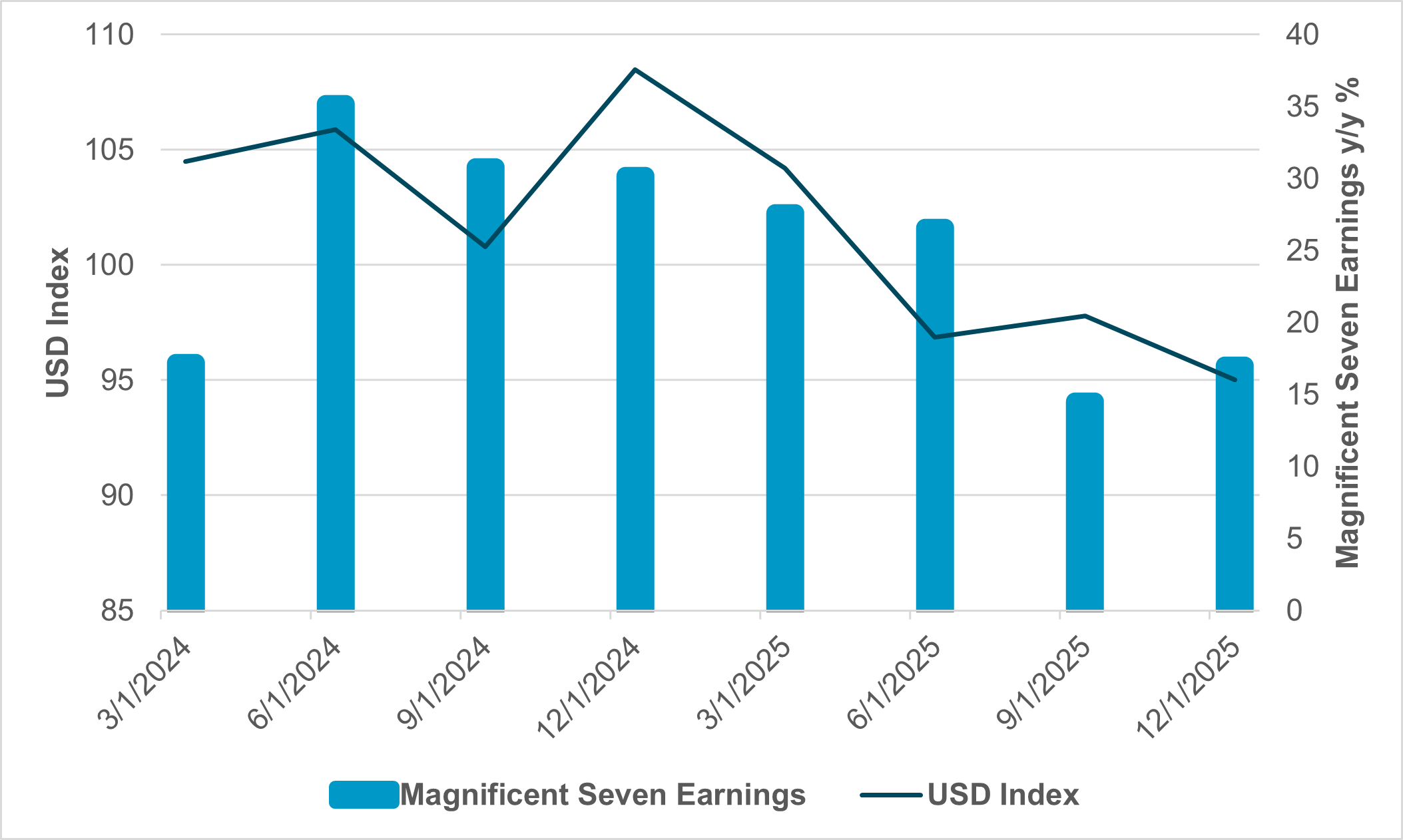

EXHIBIT #3: U.S. DOLLAR INDEX AND MAGNIFICENT SEVEN EARNINGS S&P 500 SECTOR SHIFTS

Source: BNY, Bloomberg

Our take

The role of the USD in stocks has become a relevant focus again, as the USD rally in 2021–2022 hit Magnificent Seven returns significantly. The USD jumped over 12% during that period of U.S. economic growth and recovery. The dollar fell 8% in 2025 before steadying in Q3 and it is now up 1% on the year. As the Magnificent Seven earn about half their revenues abroad, the 1% jump in USD during the period will matter but not significantly.

Forward look

The forecast for USD weakness into Q4 is also important for how markets trade Q3 earnings into Q4 expectations. Given the current uncertainty over USD hedging from abroad vs. U.S. growth and U.S. rates, it is likely that the USD as a key factor in earnings will be less important than others in 2026. However, for global investors hedged positions in other places may be worth watching as a key driver of diversification. The Nikkei rally following the LDP leadership election, and the JPY move from 148 to 153 highlights how currency trends and interest rate differentials matter. The long Nikkei and long USD trade may be factors to consider in U.S. markets to drive sector rotations and interest rate-sensitive trades in 2026.

As the Q3 earnings season begins, investors face a delicately balanced environment: earnings expectations remain positive but modest, with a consensus of around 8–10% growth. For some analysts, equity markets appear priced for perfection after months of resilience. Defensive positioning across portfolios – evident in high put/call ratios and subdued inflows – suggests limited confidence in a sustained rally. Sector dispersion continues to define performance, with Technology and Communications leading while Real Estate, Health Care and Energy face headwinds. The concentration in mega-cap Tech names introduces fragility, but broadening earnings across other sectors could cushion potential volatility. Looking forward, much depends on how profit margins absorb cost pressures and whether easing financial conditions offset slowing global trade. A stable macro backdrop, coupled with further potential Fed rate cuts, could extend equity gains, but the margin for error is thin. The next quarter will test whether “good” earnings remain good enough to sustain current valuations.