Misses, Beats and Bubbles

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 6 minutes

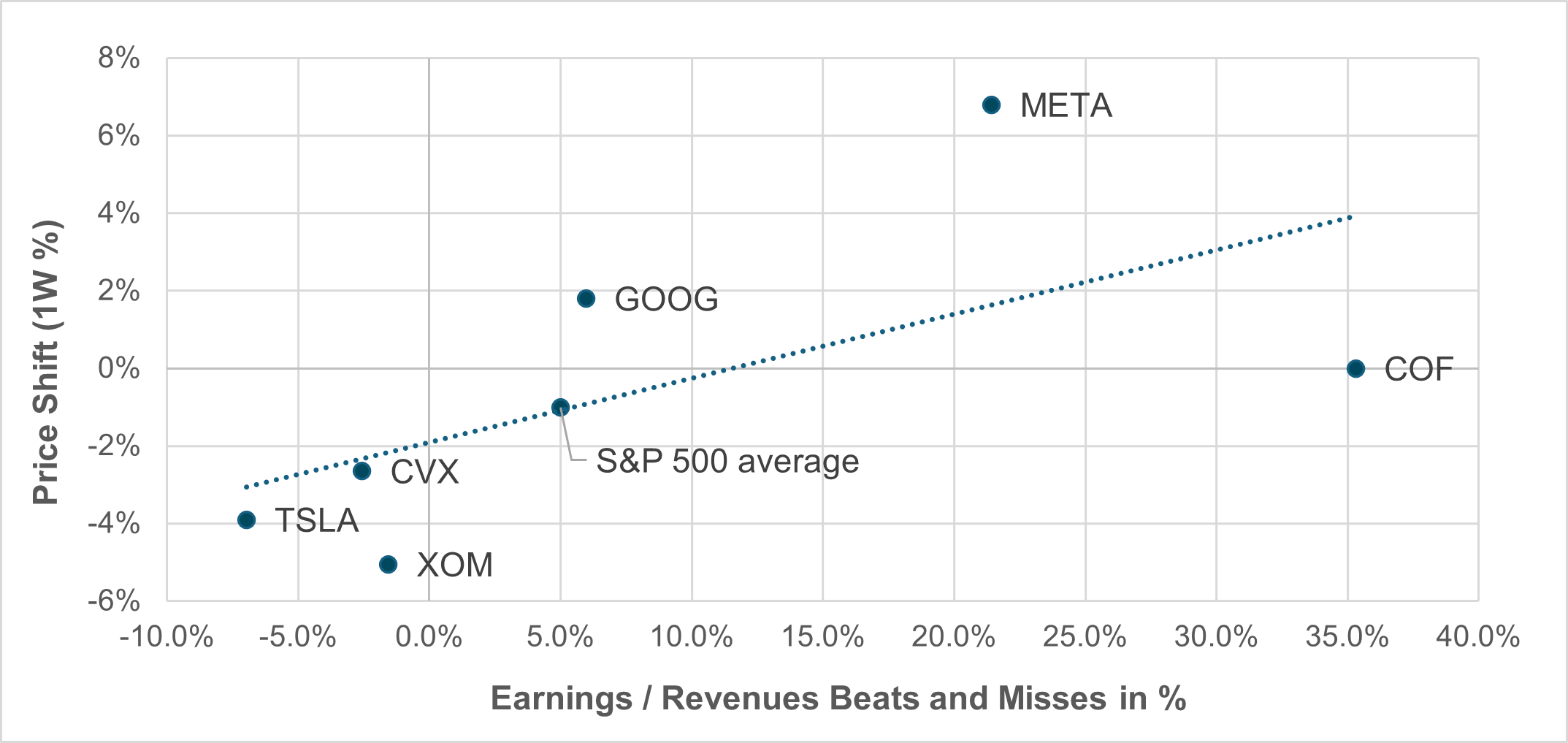

EXHIBIT #1: S&P 500 TOP 3 BEATS/TOP 3 MISSES AND PRICE SHIFTS

Source: BNY, Bloomberg

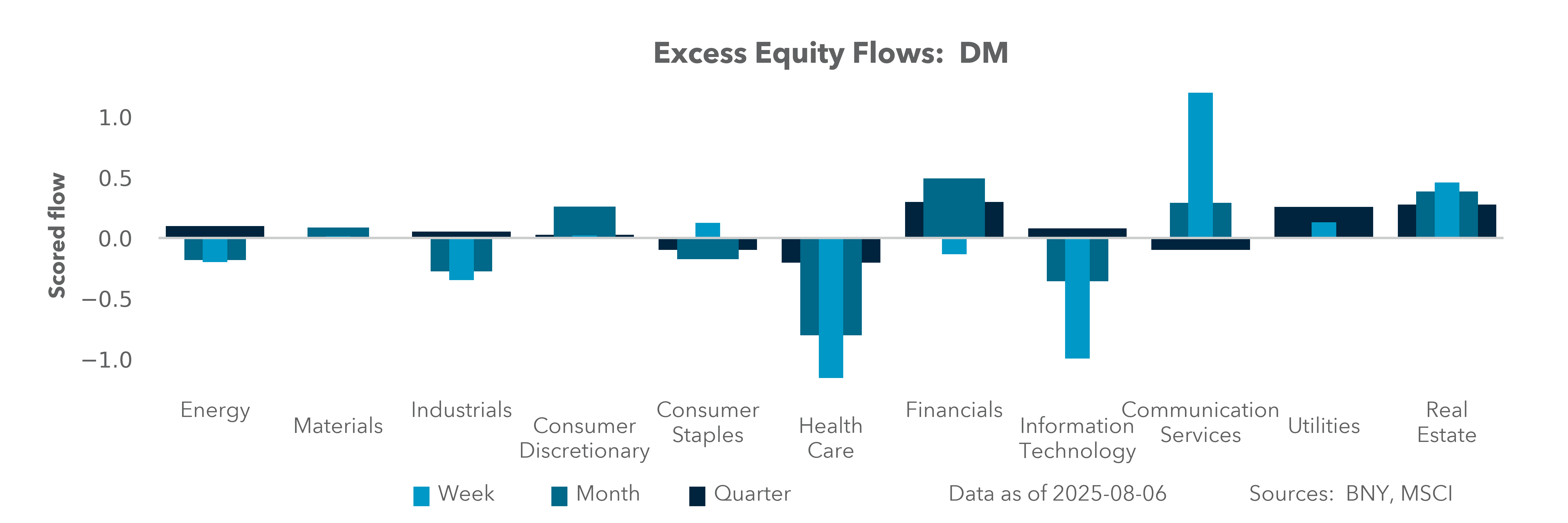

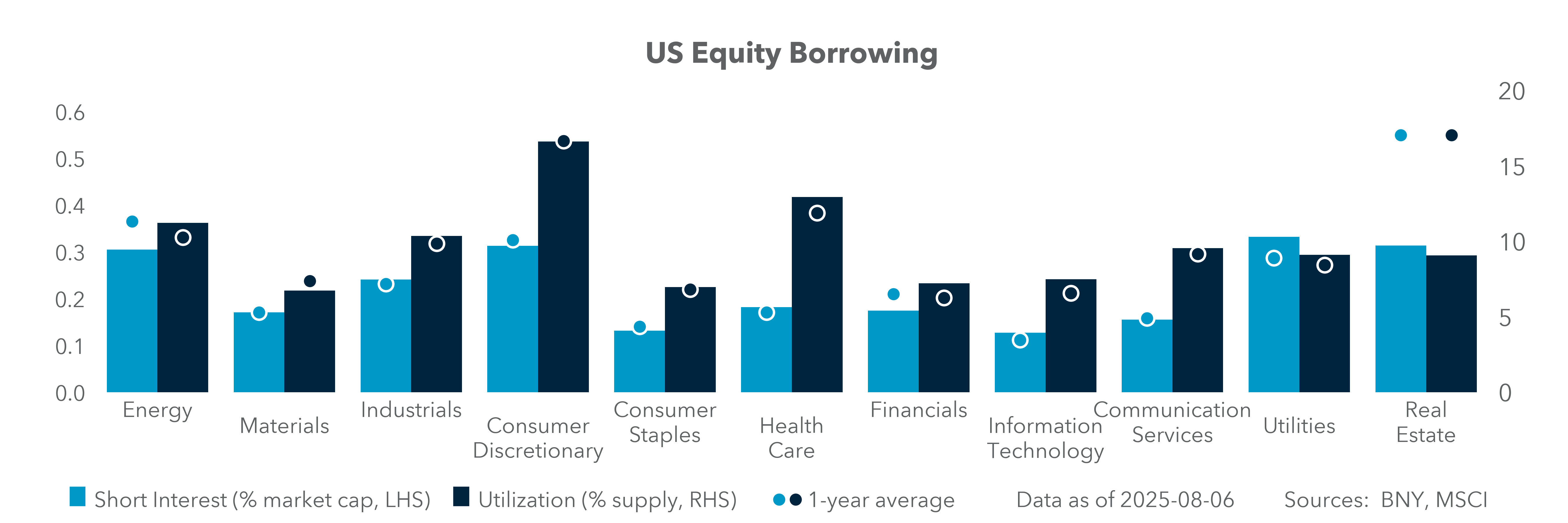

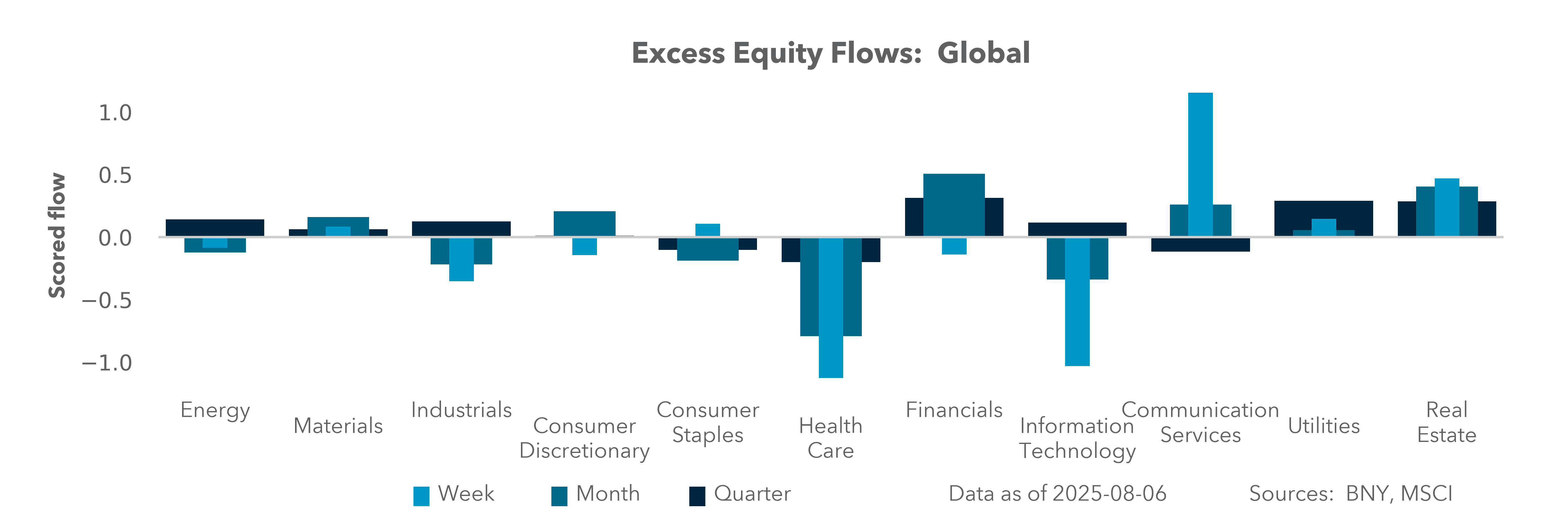

U.S. equities recorded their largest “buy-the-dip” session since May on August 4, following weaker payrolls print and a soft manufacturing ISM, increasing the implied probability of a Fed policy rate cut from below 50% in July to above 90% now. This “bad news is good” narrative is new, and contrasts with last month’s complacency. July ETF data showed strong inflows into equities and alternative products, while small caps lagged, suggesting retail investors have returned to buying following May’s catch-up moves. Three-quarters of S&P 500 companies have reported Q2 earnings, with 82% beating EPS forecasts and 79% topping revenue estimates. Blended EPS growth is 10.3% (June 30: 4.9%) and revenue growth is 6.0% (June 30: 4.2%). Health Care, Consumer Discretionary, IT and Communication Services delivered the strongest surprises, yet dispersion is acute: Meta, Alphabet and Capital One dominate the beat league-table, while Exxon, Chevron and Tesla headline the misses. Hedge funds are scaling back IT and growth exposure, redirecting capital toward Consumer Staples and international names. This shows up in our short utilization data. iFlow also confirms continued tech outflows, further buying of Utilities and short covering in Real Estate.

Our take

About three-quarters of S&P 500 companies have reported their Q2 earnings, with 82% reporting EPS above expectations and 79% beating on revenue. Both of these figures are well above historical averages, with the EPS blended average at 10.3%, up from 4.9% on June 30, and revenues climbing 6%, up from estimates of 4.2%. The strongest contributions to the revenue surprise came from Health Care, Consumer Discretionary, Information Technology and Communication Services. The notable story for U.S. flows in the last week was the bounce-back in buying on August 4 following unwelcome news of a weaker U.S. jobs report and a weaker manufacturing ISM showing higher prices and lower growth, driving hopes for a FOMC rate cut. The odds of a Fed cut rose from under 50% in July to over 90%. The rise in shares also reflects earnings beats, as we discussed in July. The biggest issue for U.S. markets is the skew caused by IT dominance linked to AI investments, which are driving up valuations. The beats are mostly driven by IT and Financials (with the top three being Meta, Alphabet and Capital One), while the misses are in Energy, Materials and Industrials (with Exxon, Chevron and Tesla representing the bottom three). During the week, hedge funds were seen driving tech outflows and Consumer Staples inflows, while our iFlow data showed further inflows into Utilities and short covering of Real Estate given Fed cut hopes.

Forward look

We are nearing the end of Q2 earnings reporting season, and surprises will continue to drive market shifts. The biggest factor affecting U.S. equities is the ability of the FOMC to avert a hard landing, with rising fears of stagflation leaving faster money looking for defensive alternatives. The CPI report August 12 will be a key risk for equities in the U.S., given the connection between growth hopes, stable prices and a Fed cut. The other micro risk ahead is how the rest of the world compares to U.S. stock values. Revenue and earnings growth clearly supported U.S. markets in July, but hard economic data will be needed if this is to continue in Q3. Investors are most concerned about tariff-induced growth risks slowing consumer demand and corporate investments. Retail sales figures due out on August 15 will be an important barometer of U.S. consumer demand in a month with better financial conditions and lower market volatility. The burden of proof is shifting in equities from earnings and AI investments to consumers and the real economy, with risks for higher volatility ahead.

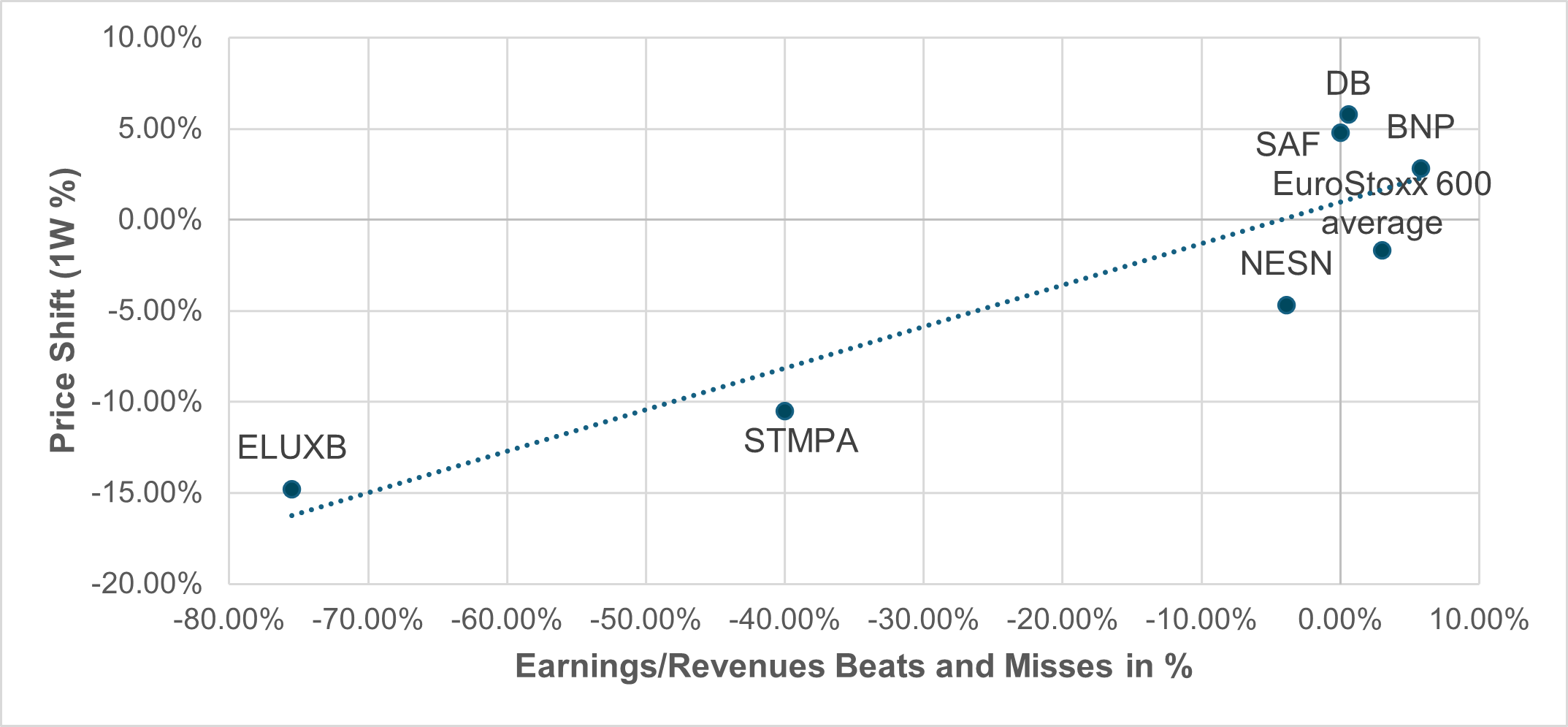

EXHIBIT #2: EUROSTOXX 600 TOP 3/BOTTOM 3 AND EPS & REVENUE SUPRISES AND PRICE SHIFTS

Source: BNY, Bloomberg

Our take

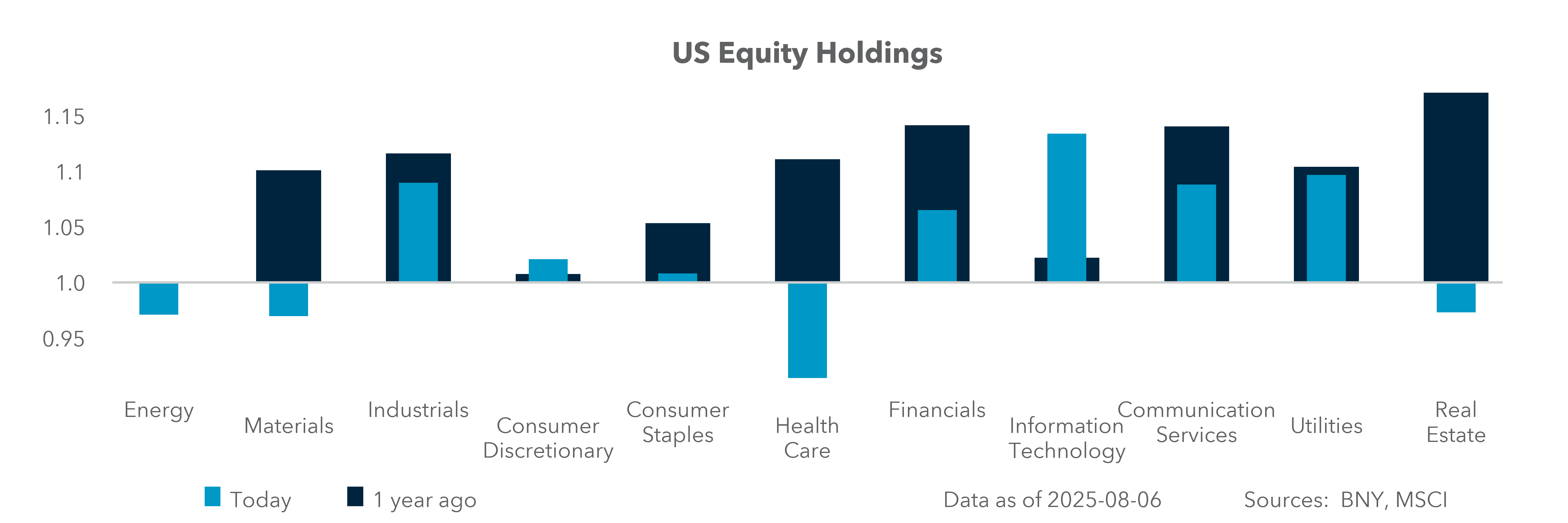

Based on the EuroStoxx 600 index, overall EU earnings have been better than expected, moving from –0.5% EPS to +3%. The role of tariffs in skewing earnings reactions shows up in a number of industries, with pharmaceuticals being one of the prime examples. Take GSK (Glaxo Smith Kline), where a 4% earnings beat still resulted in a 5% price decline. At the sector level, European profit growth is outpacing expectations, though earnings misses – especially in Materials, Consumer Staples and Utilities – are triggering sharper downside stock reactions than for U.S. peers. The contrast of long-tail misses in Europe to the long-tail beats in the U.S. goes a long way toward explaining the current price action, with the S&P 500 up on the week and the EuroStoxx 600 down. iFlow data also support the price movements and reactions to earnings as investors are overweight European shares – particularly in Financials and Industrials – while they are near average holdings in the U.S., with the exception of IT and Communications.

Forward look:

The headwinds for EMEA investors come from comparison to U.S. earnings, which are once again in double digits (for the fifth quarter in a row), the risk of tariffs dragging down EU exports and growth, and the ECB being 1–2 rate cuts away from its terminal rate for the cycle. Downside surprises this week in Europe hurt more than positive surprises helped. Rising concerns about a weaker U.S. economy can be seen in international flows. The focus into next week will continue to be on earnings beats, and sentiment barometers like German’s ZEW will shine a light on how the bloc’s tariff deal shows up with investors. The other variable for investors is the EUR. A move over 1.17 may be seen as a headwind against Q3 outlooks and earnings growth.

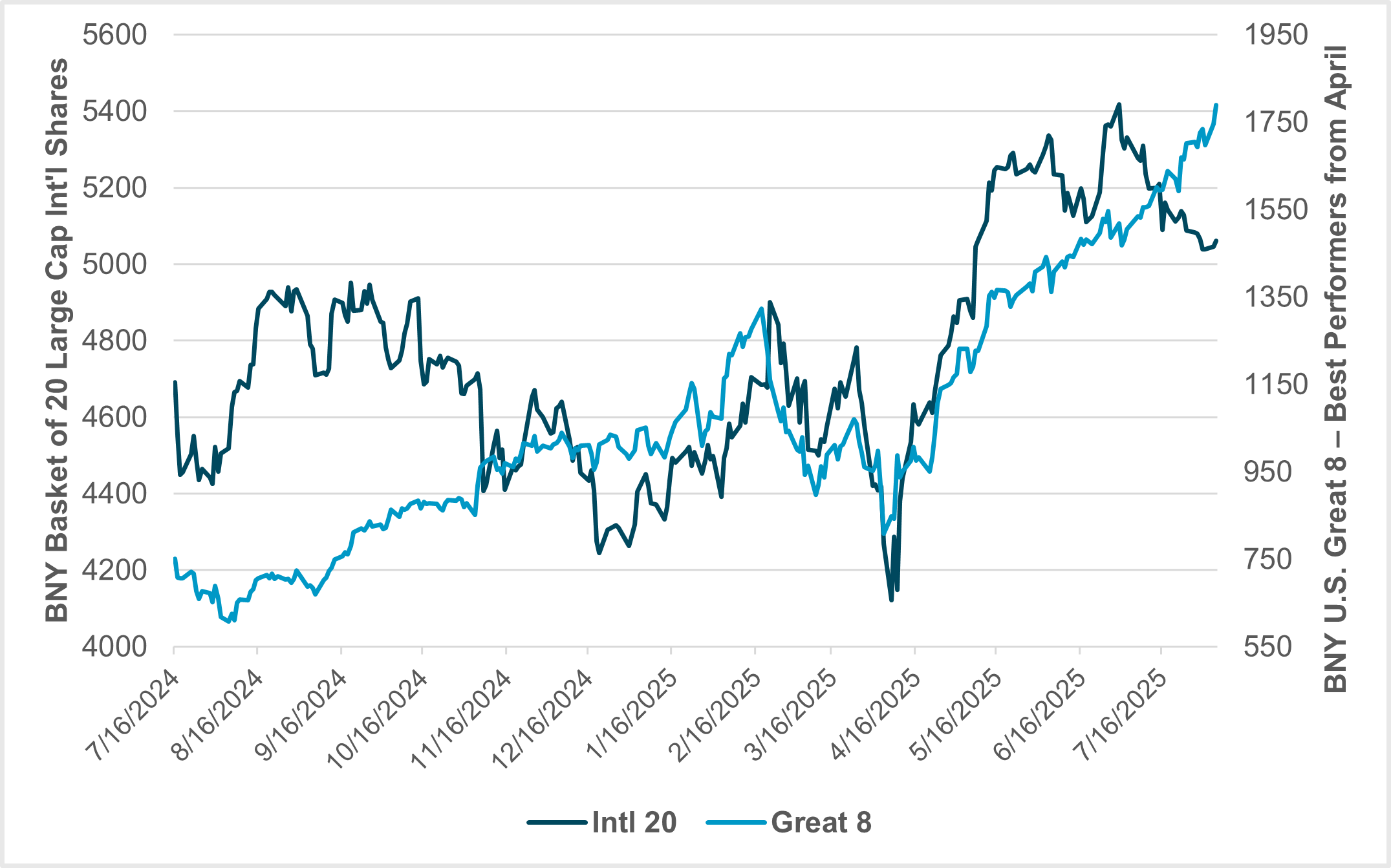

EXHIBIT #3: PRICE DIVERGENCE BETWEEN THE U.S. "GREAT 8" AND THE "INTERNATIONAL 20"

Source: BNY, Bloomberg

U.S. Great 8 basket = CEG, DELL, GEV, MCHP, NRG, PLTR, STX, WDC (best performers from April lows to July)

International 20 = TAQA, SHEL, SAP, RO, RJHI, Reliance, Petrobas, NOVOB, MLB1, LVMH, HSBA, ENR, ASML, ARAMCO, SAMSUNG, BYD, ICBC, TSMC, Tencent, Toyota

Our take

Starting in June, investors began pushing back from international diversification and re-embraced U.S. IT, particularly the “Magnificent 7.” Momentum buying from April lows showed a brief outperformance for international shares, linked in part to the weakness of the USD. The role of the dollar in driving flows in 2025 stands out. Diversification away from U.S. is not a new story, but one that was evident until the FOMC cut rates in September 2024 – a turning point for the U.S. equity market. The July moves lower in international shares reflects the return of tariff uncertainty in global growth and revenues along with the bounce-back in the USD.

Forward look

U.S. investor positioning, which had been pushing money into Europe, stalled in June and July. The outlook for August is less clear, as the Q2 earnings narrative slows, and economic growth becomes the key story for risk. The problem for international shares is the combination of the dollar’s variability and its role in translating earnings. Markets have looked through tariffs, dampening demand and complicating all cross-border profitability as well as creating price uncertainty. A larger problem for the rest of the month is the correlation of all equities in a broader risk-off environment driven by weaker economic data everywhere. Global growth expectations were resilient in Q2 but will be more fragile in Q3 given the fear of bubble-like valuations in various sectors – particularly finance and IT.

The push for international diversification, which saw a brief outperformance of the “International 20” over the “U.S. Great 8,” stalled in June and July as the USD rebound and renewed tariff uncertainty led investors to retreat from international shares. The market’s focus is now shifting from Q2 earnings to economic growth, with the burden of proof on the real economy. Key barometers will be the U.S. CPI report on August 12 and retail sales figures due out on August 15. Headwinds for European investors include the comparison to double-digit earnings in the U.S., the risk of tariffs dragging down exports and the ECB being 1–2 cuts from its terminal rate, with a EUR/USD move over 1.17 seen as a further obstacle. This transition carries risks of higher volatility, as fears of U.S. stagflation challenge a fragile global growth outlook.