Market of Stocks?

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

The correlation of sector flows is high, suggesting a market focused on macro risks rather than micro stories – something that usually flips in April Q1 earnings season.

The key market uncertainty has been US tariffs and the expectation of a global slowdown hitting the US most – with surveys pointing to a sharp drop in activity.

The level of volatility has been good for risk parity programs as bonds have become more important in asset allocation; we have seen ETF flows supporting this.

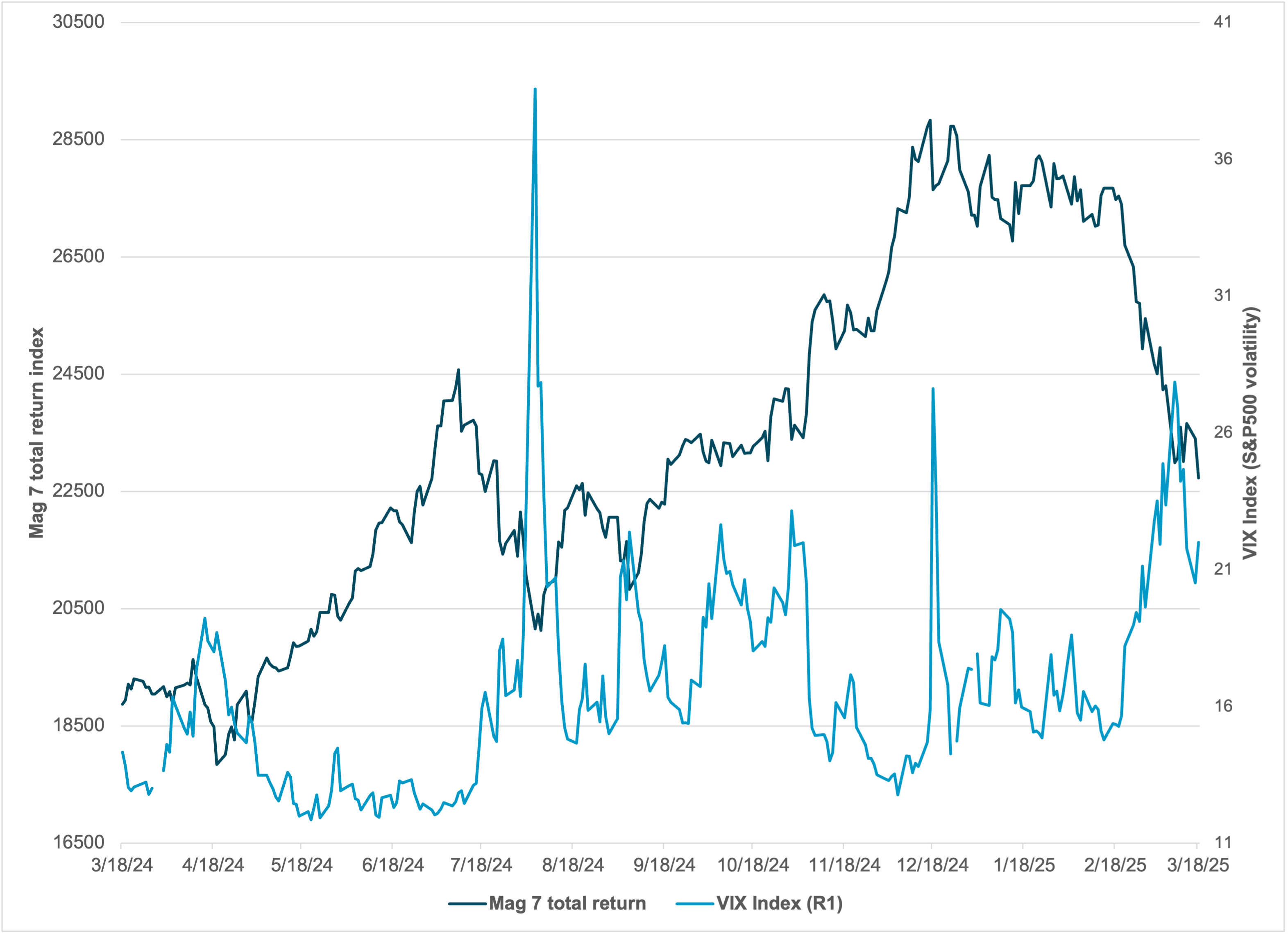

EXHIBIT #1: THE S&P 500 AND THE MAGNIFICENT SEVEN

Source: Bloomberg, BNY

We continue to see ongoing weakness in US shares in March, but volatility expectations slowed this week. There has also been a notable slowing in volumes – fundamentally linked to multiple central bank decisions this week – as well as three idiosyncratic drops in emerging market shares. In Indonesia this decline was led by tech, in Turkey by political worries, and in Hong Kong by regulators limiting retail leverage. Position washouts were followed by lower volumes, which traditionally results in some retrenchment trading of ranges.

Concerns about tariffs did not alter most central bank policy decisions, with rates in the UK, Sweden, Indonesia, Taiwan and the US all remaining on hold. The focus of the US “dot plot” Summary of Economic Projections confirmed market expectations of two rate cuts in 2025, with tails risks of more cuts looming as downside growth concerns dominate global economic outlooks. The OECD cut its global growth forecasts this week, and the FOMC did the same for the US growth outlook. The role of position washout in the volatility this week as well as over the month and the first quarter stands out. The Magnificent Seven are sharply lower on the year, with more than 10% of investors unwinding their overheld positioning, according to our data. The correlation of market volatility to tech unwinds worked well in January and February but slowed in March. And the drivers of volatility are changing.

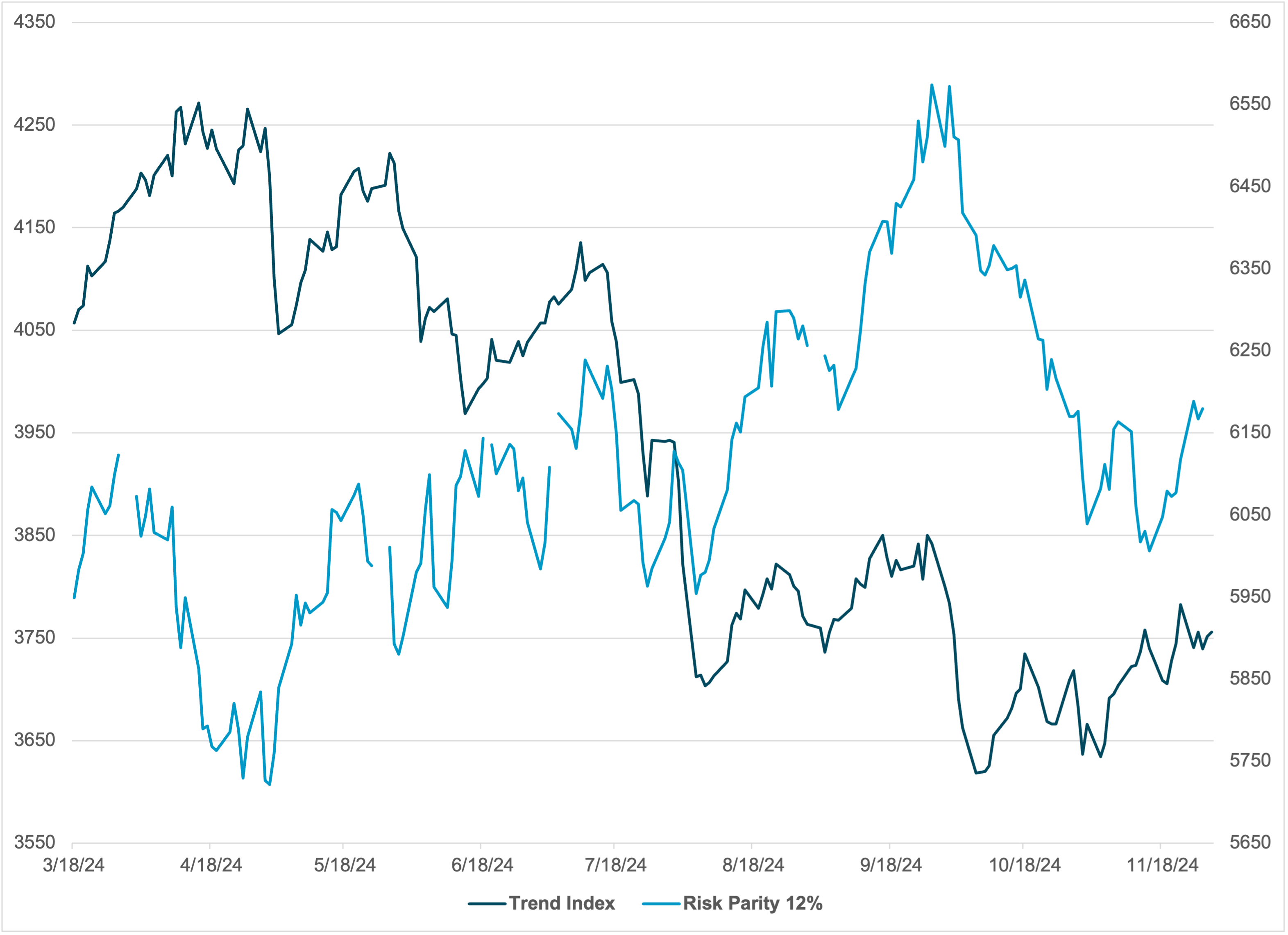

EXHIBIT #2 : RISK PARITY AND TREND PERFORMANCE - DIVERSIFICATION MEETS VOLATILITY

Source: Bloomberg, BNY

Our take

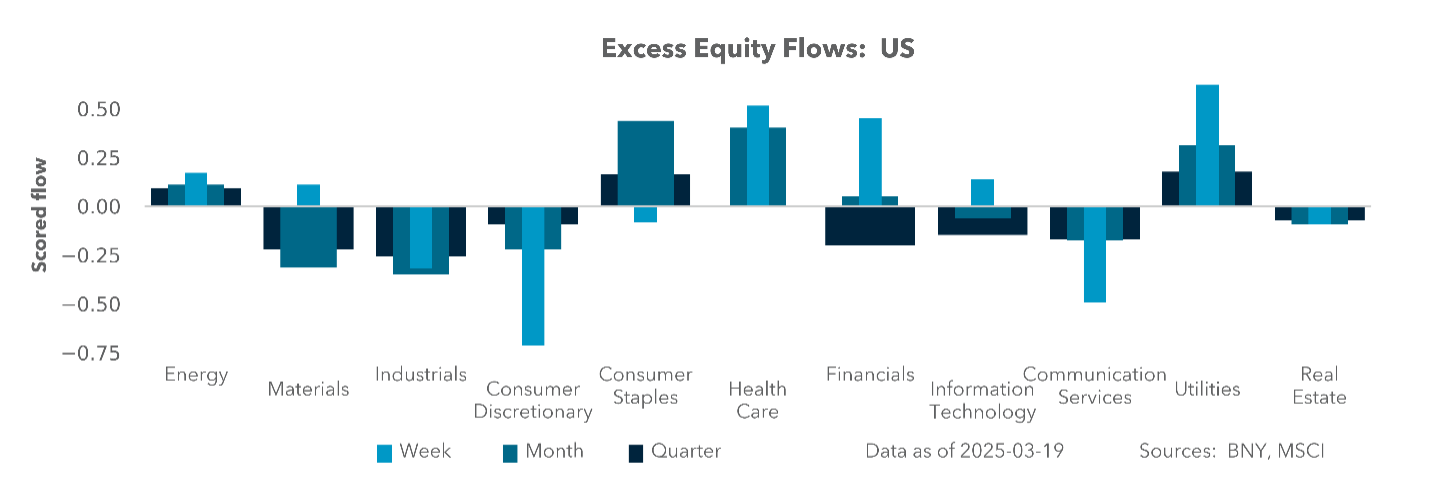

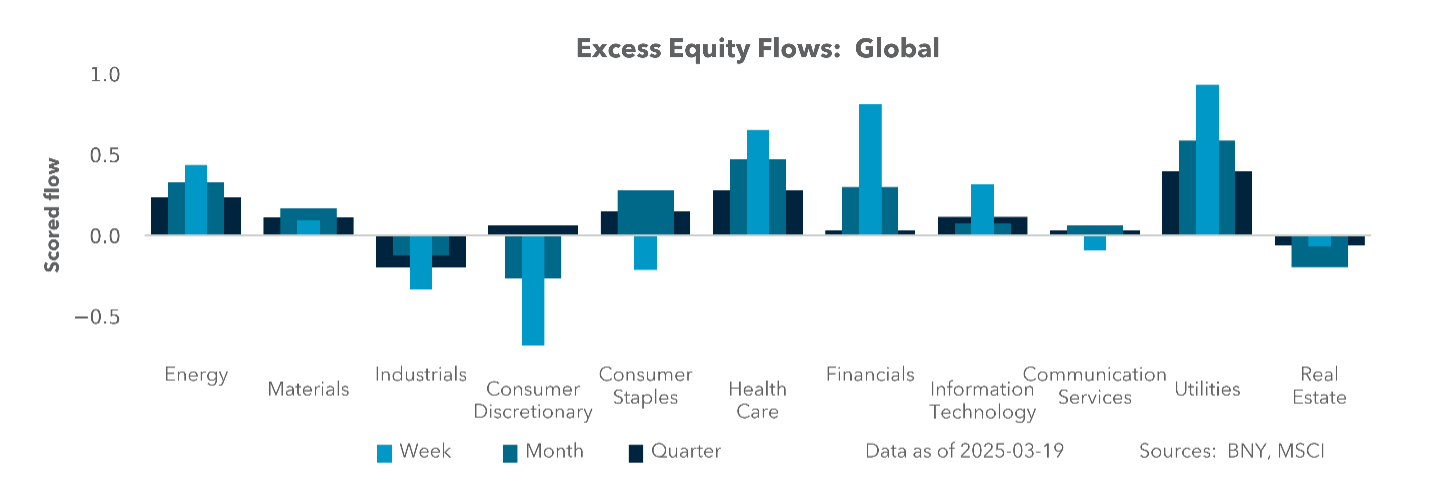

Trend chasing fails as positions wash out. The biggest problem for equity markets in March has been the on-and-off trading for risk. Higher uncertainty forces risk reduction everywhere. Volatility has remained above the long-term average, with the VIX index over 20% most of the month. Global gains also reached limits and despite a better week, the returns for March are mostly negative in Europe and the US, while they are up in APAC. The iFlow holdings show ongoing defensive trading in US shares with the soft-landing expectations dropping back to October lows. The push from soft landing to recession fears in the US and the bounce back in EU and China shares failed this week as sectors proved highly correlated to each other – the most in three years, according to our flows.

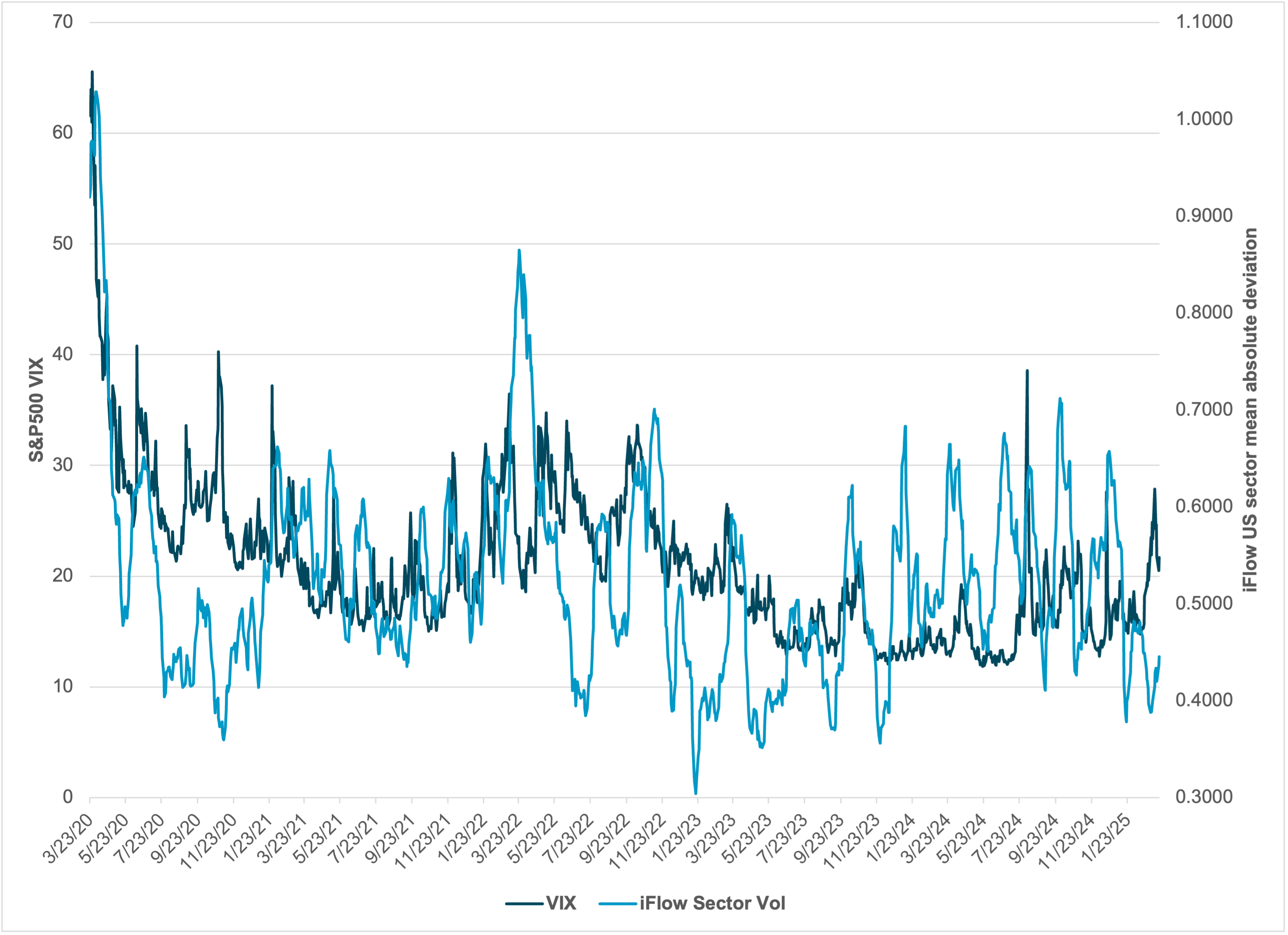

Forward look

We expect sector rotation rather than position washouts to drive short-term risk-taking. Our iFlow sector flows, when put against the S&P 500 VIX index, suggests we are in a range but one that remains over the 5- and 20-year averages. In the long term, investors use diversification to offset market risks. The problem is that multi-strategy hedge funds failed to produce positive returns in Q1. Combined with a lack of clear global trade, this left volatility as a key factor for trading anything. The S&P 500 concentration risk was a worry in 2024 and that has corrected in 2025, but the market continues to sell shares in the US more than rotate from one sector to another. The lack of a trend in stocks, bonds and FX stands out in the last month – with the blame for this being placed on Trump trade policy, DOGE federal layoffs and Congressional budget debates. The offset of EU defense spending and China AI also proved insufficient this week. Global uncertainty will not stop until there is more evidence of US corporate earnings holding and US economic growth bouncing.

EXHIBIT #3 : VIX AGAINST THE IFLOW MONTHLY SECTOR MEAN STANDARD ABSOLUTE DEVIATION

Source: Bloomberg, BNY