Linking BoJ policy, JPY and Japanese equities

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

EXHIBIT #1: TAYLOR RULE ESTIMATE FOR JAPAN VS. FIXED INCOME AND EQUITY HOLDINGS

Source: BNY, Bloomberg

Investors will face another political test in Japan in the coming days, as the LDP minority puts Sanae Takaichi forward for election as prime minister. The LDP is enjoying its highest level of public support since the days of former Prime Minister Shinzo Abe, with its poll numbers rising to 28%. However, there are clouds on the horizon, with Komeito breaking away from the ruling coalition and negative headlines about Takaichi’s fiscal plans.

Japanese shares rose sharply this week while the yen fell. JPY hedges are once again an important factor for carry trades by cross-border investors in Japanese equities. U.S.-based investors can now hedge long positions in the Nikkei or Topix indexes with a JPYUSD forward and add 3% to their annual returns. While this is not a new trade for many investors, it reflects interest in the new government’s fiscal spending plans, the risk of higher inflation and a weaker yen. The keys to this trade are higher growth and a weaker Japanese currency. The same carry can work for investors outside the U.S., but there are limits to its effectiveness. The Bank of Japan (BoJ) plays a role in limiting JPY weakness, as does the government, with the Ministry of Finance warning it may intervene as the yen approaches 155.

Our take

Inflation unleashed by the COVID-19 pandemic reshaped Japan’s economy and made it harder for the BoJ to normalize policy and ensure stability. During the recent stock rally, investors bet on a shift to higher rates. But when the BoJ surprised markets at the 2023 inflation peak, shares dropped and bond yields bottomed out. Since then, flows and holdings in Japan have been driven more by BoJ policy than by government initiatives – and the noise now around the Liberal Democratic Party is largely viewed as temporary. The more important issues are growth under the new U.S.–Japan trade deal and the path of inflation. The forthcoming wage negotiations in Q1 2026 will be pivotal for both investors and the BoJ’s next policy move.

Forward look

There has been a clear trend in Japan, with investors buying equities and selling bonds. Other factors are less clear. Tariffs will play a role as will politics, which have not derailed moves that have been occurring for years. Equities and the view of Japan by global investors are unlikely to be swayed by domestic politics as much as they are by the BoJ. The BoJ has plenty of room to raise rates while remaining accommodative. The yen will continue to be a positive factor through year-end, making Japanese shares even more attractive.

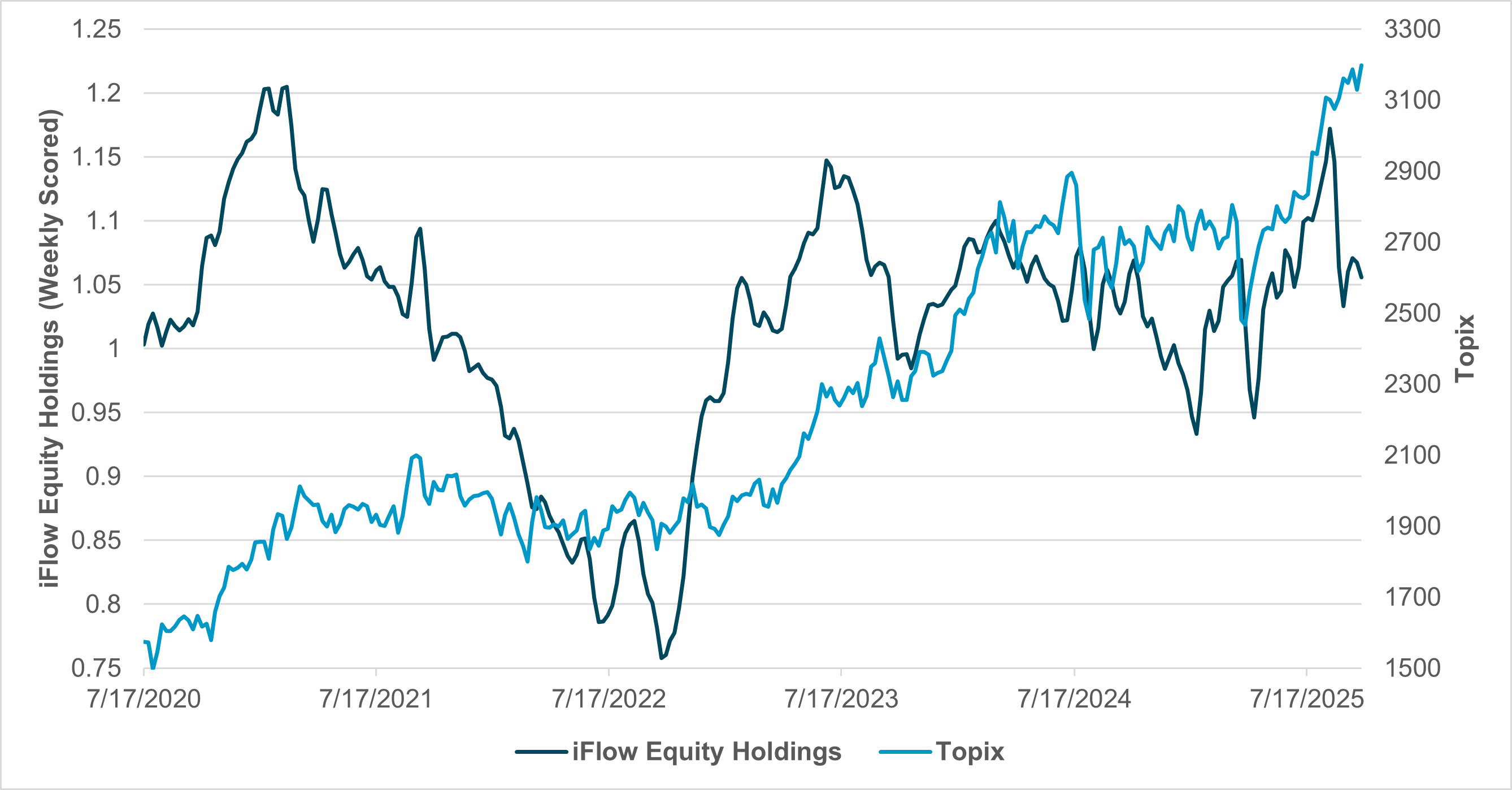

EXHIBIT #2: TOPIX VS. IFLOW EQUITY HOLDINGS

Source: BNY, Bloomberg

Our take

The most interesting point about the recent price action in Japan shares is that holdings have drifted lower since July. Markets rose sharply following Takaichi’s victory in the LDP leadership race, but the rally wasn’t sustained and higher shares and holdings remaining near their five-year average suggests there is no clear consensus on future growth or the potential of Japanese shares.

Forward look

The most important factor for investing in Japan is the yen. If the currency touches 150, it could test 155 and possibly even 160 if growth and inflation remain mixed enough to prevent a clear policy path for the BoJ. The final hurdle to 155 is the expectation that the BoJ will refrain from a rate increase at its October meeting. Japan’s central bank is behind the inflation curve, and waiting until December to hike will hurt the JPY as much as it will keep JGB yields at the longer end of the curve.

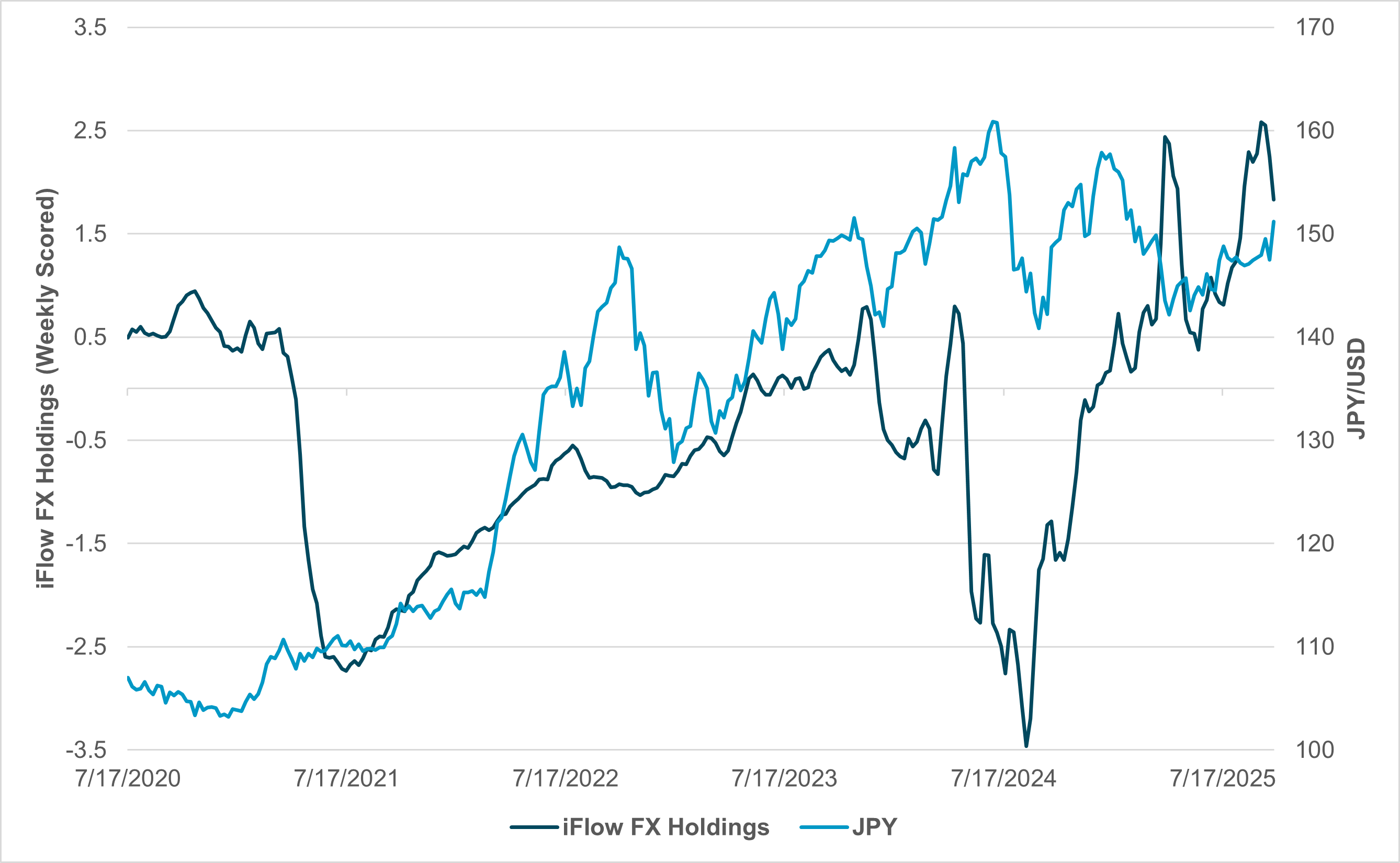

EXHIBIT #3: JPY AND IFLOW FX HOLDINGS

Source: BNY, Bloomberg

Our take

The biggest factor driving JPY isn’t positioning but the need to hedge. The most important factor for understanding Nikkei and JPY risk as we head into year-end may be how Japanese investors view U.S. bonds and stocks and how they see their hedge ratios now compared to the beginning of the year. Our JPY holdings have dropped back but remain over the 5-year average, with the risk of another washout of JPY longs if the BoJ holds rates steady. The political uncertainty in the week ahead may add to JPY position risks, and the market seems set up for another test of 155.

Forward look

If JPY moves, so will KRW and to some extent CNY. As an anchor for APAC FX, JPY could trigger a policy reaction by the U.S. Allowing JPY to weaken beyond 155 would require a signal that U.S. growth and tariff revenue are in line with the U.S. Treasury. The biggest risk for Nikkei shares may be JPY intervention at 155 because of political pressure from other countries in the region as well as the U.S. as the Japanese authorities try to hold a line on financial stability.

Looking ahead, the correlation between the JPY and the Nikkei is poised to remain sensitive to the Bank of Japan’s (BoJ) policy trajectory rather than short-term political shifts. The new LDP leadership under Takaichi may offer a fiscal impulse, but the larger determinant of investor sentiment will be how the BoJ balances controlling inflation control and supporting growth. As long as yield differentials remain wide and U.S. policy stays restrictive, JPY weakness should continue to bolster equity performance through renewed carry demand. Yet, intervention threats near 155 – and possible coordination with the Ministry of Finance – could temper speculative flows. For global investors, Japan’s appeal remains grounded in improving corporate governance, structural wage growth and a stable policy backdrop. The coming quarters will test whether Japan can sustain equity momentum without undermining currency credibility – a key factor for determining whether foreign capital will deepen its commitment or retreat in search of higher real returns elsewhere.