Japan and the Art of the Deal

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

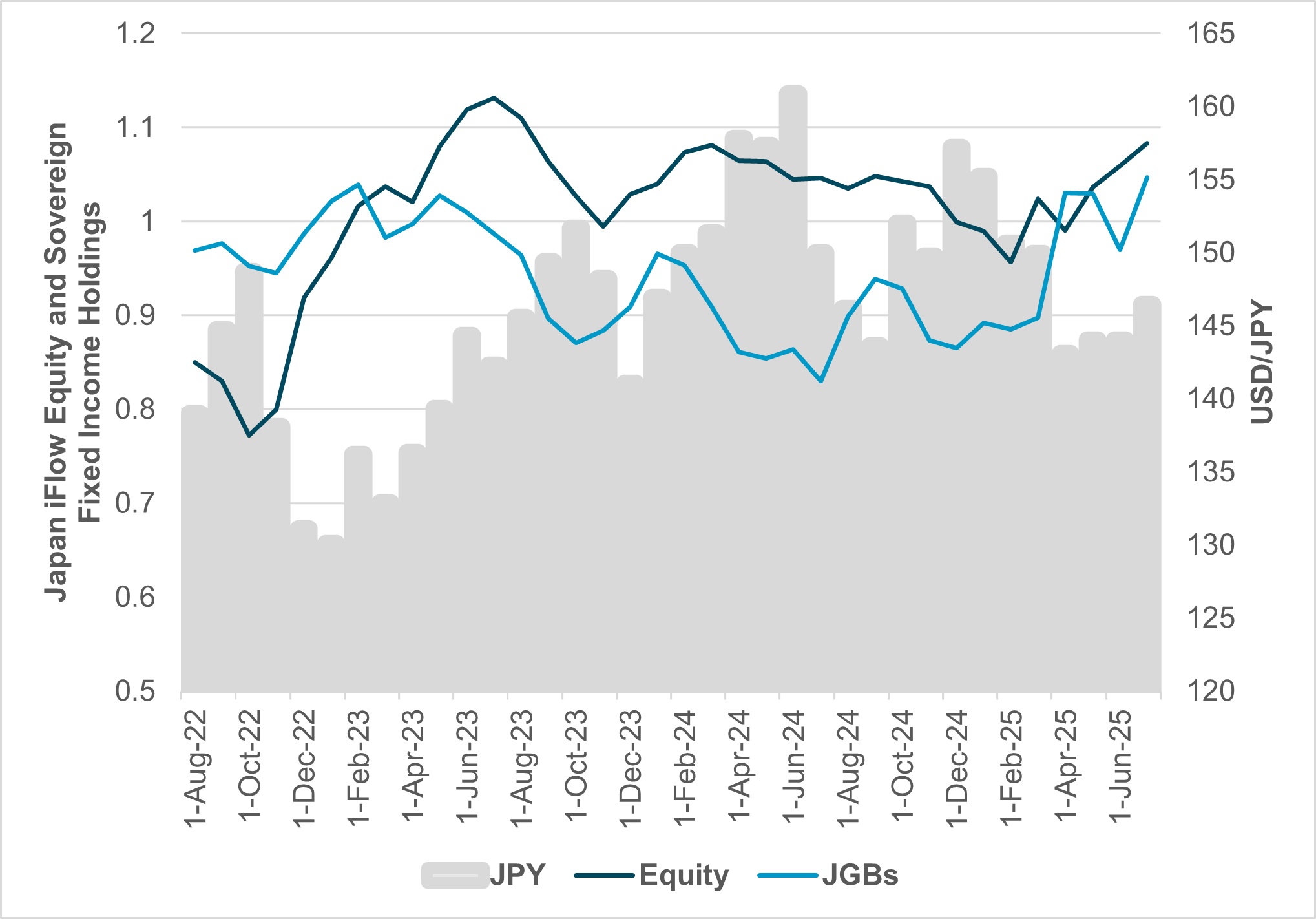

EXHIBIT #1: JAPAN HOLDINGS FOR EQUITIES AND BONDS AGAINST USD/JPY

Source: BNY, Bloomberg

The Japan–U.S. trade deal catalyzed a 5%+ relief rally in Japanese equities this week, establishing a 15% tariff baseline – significantly below threatened levels – while preserving agricultural protections despite maintaining 50% steel and aluminum levies. With Japan's 2024 trade surplus with the U.S. near $150bn, this implies $22.50bn in future U.S. Treasury revenues. Our iFlow data indicate a near two standard deviation inflow into Japan shares over the past month, suggesting substantial catch-up momentum can continue given year-to-date returns are the lowest among developed markets. The JPY–Nikkei correlation has moderated to 2022 levels, with the rally from 2023 originating from a short holdings position, while the current upswing stems from a slightly overheld one. Notably, JGBs are now attracting investors, whereas during the previous rally rates remained well below international levels. July’s Tokyo CPI exceeded the 2% target, strengthening the case for BoJ action in September rather than July. Industry earnings show notable divergence, with July’s flash PMI retreating to 48.8 from 50.1, though real retail sales remain positive for the 38th consecutive month (+2.2% y/y). With TOPIX volatility significantly below China and U.S. markets by 3–5%, Japanese equities could gain an additional 5–10% as political and trade uncertainties diminish.

Our take

Prices are near historic highs again following this week’s TOPIX and Nikkei 225 rally, but year-to-date returns in Japan remain the lowest among developed markets. Our iFlow data have been consistent with a near two standard deviation inflow over the last month into Japanese shares. As such, there is a catch-up momentum factor to consider in the weeks ahead. For equities, the correlation of a weaker JPY and stronger Nikkei peaked in 2024, and we are back to 2022 levels, with the dollar important, but not dominating flows. Is the “new” Japan story, based on structural corporate improvements, powerful enough to forge a secular bull market on its own, or is the rally vulnerable to the dollar’s usual carry dynamics? We can see from our holdings in Japanese equities that the 2023 rally into Japan was from a short position, while the current upswing is from a slightly overheld one. We can also see that JGBs are attracting investors now, whereas rates were still well below international interest levels during the previous rally. The Bank of Japan’s role in equities is clearly a potential risk, but for now higher rates in Japan and lower valuations in equities are garnering cross-border flows.

Forward look

The ability of bonds and stocks to attract international investment flows cannot be sustained. The Tokyo CPI July data showed inflation still well over the 2% target – adding to the case for BoJ action. While the meeting at the end of July is not expected to deliver a rate hike, it may telegraph action for September. Investors are watching margins and earnings in Japan, which will be critical for keeping the headwinds of rates and a stronger JPY from hurting momentum back into equities. The role of the government and further fiscal stimulus will be a significant factor in any BoJ outlook. The election result was slightly better than expected for the already weak Prime Minister Ishiba, but the full effect of the vote is still in motion. The success of striking a deal with President Trump also helps support the status quo. The key will be whether sustained momentum leads to effective reforms that spur stronger economic growth – an outcome we expect but that is not yet reflected equity market prices.

EXHIBIT #2: MONTHLY CASH EARNINGS IN JAPAN BY INDUSTRY

Source: BNY, Macrobond

EXHIBIT #3: NIKKEI PERFORMANCE AGAINST 12-MONTH FORWARD EPS CONSENSUS ESTIMATES

Source: BNY, Bloomberg

(The BNY large cap index includes: TAQA, Al Raji Bank, ASML, Boyd Gaming, HSBC, ICBC, LVMH, Mercado Libre, Novo Nordisk, Petrobras, Reliance, Roche, Samsung, SAP, Saudi Aramco, Shell, Siemens, TSMC, Tencent and Toyota.)

Our take

There is a notable divergence in the sectoral performance of Japanese equities, making the current TOPIX and Nikkei rally all the more interesting. Utilities, banking and education stocks are underperforming, but this is more reflective of a stabilization of the yen and demographics than restrictive rates. If the trade deal is to drive a relief rally in manufacturing shares, the sector must offer better returns. However, there is plenty of room for growth, with the current flash Japan PMI highlighting the upside as the outlook fell following the election and trade agreement from 50.1 to 48.8. Services industries are clearly underperforming, which plays a significant role in the political landscape, as government actions on inflation continue to be a key factor influencing consumer behavior.

Forward look

EPS estimates for Japan need to catch up with prices, which should come with further clarity on government policy plans following the upper house election and the rate path. The BoJ balancing act on JGBs against the undervalued JPY and inflation comes through in earnings by industry. Nevertheless, real retail sales are up 2.2% y/y – positive for the 38th consecutive month – and that trajectory alone makes the overall picture for shares positive, which the EPS consensus reflects. Decades of zero rates and “zombie companies” have ended in Japan and the last three years bear this shift out. Beyond the normalization of rates and the relief for the auto sector, which anchors the optimism in equities, there is also room for technology to recover, with robotics and IT underappreciated by global investors. IT holdings in the entire region ex-China are below the 10-year average. The other factor supporting TOPIX is the index’s modest volatility, which at 3–5% is well below China and the U.S., even though compound growth is only 2% below China and 4% below the S&P 500. With risks from the upper house election removed and the good will from the trade agreement with the U.S., Japan may have a further 5–10% to gain in equities to normalize volatility against the region and the G10.

The details of the trade agreement for individual sectors will be important for global trade and equities, with reports that the EU is hoping for a similar deal and pushback against the agreement by U.S. industries. Japanese industry and machinery robotics are important to the U.S. re-industrialization narrative and will result in more JV efforts with U.S. importers to negotiate in-market assembly. Semiconductors and other electronic parts from Japan will be interesting as well given the promise of $550bn in investments in the U.S., with some in the chip manufacturing arena. Taken together, the tariff deal in the context of higher Japanese inflation, the impact of the upper house election on the Ishiba government, ongoing JPY weakness, and the BoJ decision at the end of July give investors plenty of other reasons to pause before adding to Japan exposure.

Despite a historically strong connection between a weaker JPY and a stronger Nikkei, the price action begs for a new explanation given that we are near record highs and the JPY is 12% stronger this year. The Japan corporate upgrade narrative appears more influential now than in 2024. There is also a clear sector rotation in play: dispersion remains wide – utilities, banks and education lag on demographics and a steadier JPY, whereas machinery, semiconductors and robotics are riding the re-industrialization theme and prospective $550bn in U.S.-bound capex. With regional IT allocations still below the decade average and TOPIX volatility 3–5 ppts under U.S. and China benchmarks, normalization could lift equities a further 5–10% provided margins weather higher domestic yields and any strengthening of JPY contains inflation more than it destroys margins. The key question is whether structural reform – governance overhaul and the fading “zombie” legacy – can seed a secular bull market or if momentum will revert to carry dynamics once BoJ tightening and tariff effects percolate.