Finding a Bottom

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 4 minutes

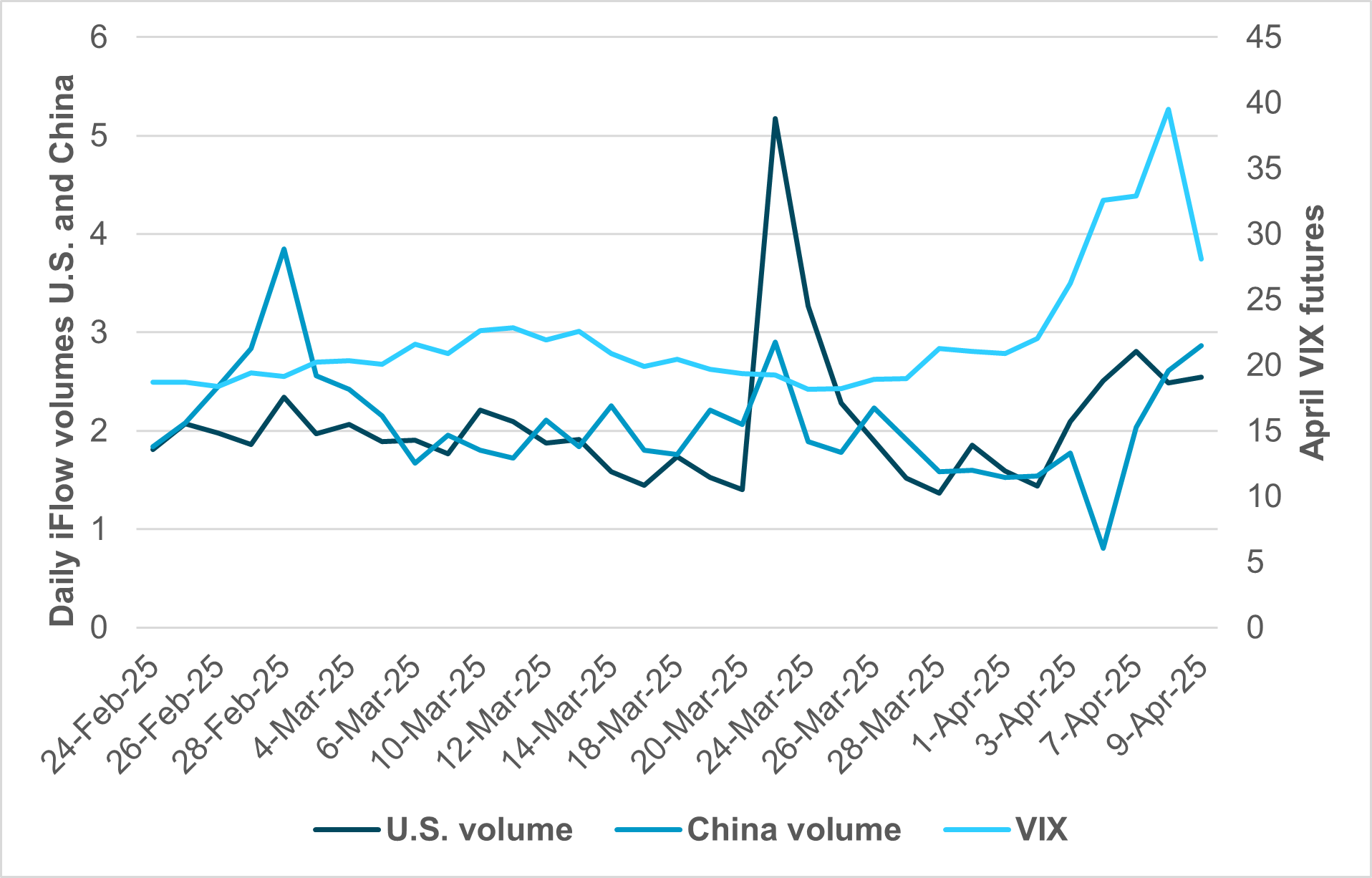

EXHIBIT #1: U.S. AND CHINA EQUITY VOLUMES VS. VIX

Source: BNY iFlow, CBOE VIX

All market disruptions involve a cycle of events that lead to a bottom. Risk aversion results in liquidation of positions, forcing leveraged holders out, driving up cash demands and raising volatility. This drives more liquidation as risk models require a further reduction in positions. Eventually, markets burn out and a bottom is found based on growth and value factors. The first requirement for finding a bottom is lower volatility and this is connected to volumes. In the last week, markets saw these factors at play as President Trump’s tariffs were paused for 90 days and replaced with a universal rate of 10% except for China, which will still be subject to a rate of 145%. The problem for investors is that the drop in volatility is insufficient to sustain a higher bounce back in equity prices.

Our take

The spike in the S&P 500 VIX is notable in that the rise over 40% held for multiple days – something not seen since 2008. The correlation with higher volume buying by our institutional clients over the last week is modest. This means the rebound was led by retail and faster money traders. Flows from ETFs on the recovery are important to consider. We saw inflows in technology, financials, consumer discretionary, and communications with a focus on SMH, XLF, XLY and XLC. Outflows in health care with redemptions were less than 10% of inflows with a focus on XBI.

Risk off forces have left investors stressed and wary of any position. The liquidation of positions is ongoing but countered by intervention by many central bankers and governments. This includes the U.S. administration as they cited the moves on bonds and stocks in their decision to pause tariffs. The size of the required liquidity depends on the broader math of $10trn in market capitalization eroded – or 10% of global GDP – an amount that will take time to recoup. The leverage from this loss has pockets of pain beyond equities. The counterintuitive consideration is that intervention slows the position clearing and price discovery needed to find value. Liquidity factors and market function drive this action globally – with the focus shifting from equities to fixed income this week. Earnings will be a critical factor in helping to stabilize markets, both through the actual results of Q1 and the outlooks for Q2 and beyond.

Forward look

Beyond the cyclical reactions, other factors, like finding value in a crisis, will continue to play out and likely make this an extended process given the risks of tariff policy, with negotiations and additional tariffs both likely to change current interest rates and therefore value calculations for growth and value. Another issue is the role of the dollar in markets as de-dollarization rises as a theme in response to U.S. policy. This changes the plumbing of the financial markets has consequences for global investors as they try to compare value and growth ahead. Our iFlow data show a clear divergence in equity growth expectations globally.

EXHIBIT #2 : EARNINGS EXPECTATIONS AND VALUE ARE CONNECTED TO BROADER ECONOMIC GROWTH OUTLOOKS

The risk of Q1 earnings disappointing is lower, but there is still a risk that companies will use tariffs as an excuse for any weakness in performance. The lesson of previous market washouts shows that companies will push out any distressed parts of their business at such times as a way of cleaning their balance sheet as all competitors suffer and the impact of doing so is less consequential than in an upturn.

Our take

A larger issue for markets and the cycle is that the use of equities as a corporate currency to buy out competitors and hire talent shifts down. Furthermore, the markets have bought into the mixed signals of Fed easing and tariff pausing driving growth hopes back up over recession fears. The M&A outlook for 2025 was expected to be robust because of deregulation and now maybe lessened by the 20% bear market test and uncertain bounce. The current price action has destroyed companies’ growth potential by shifting the focus from market cap power to free cash flow. The first value driver will be cash, then margins and finally growth potential.

Forward look

The most interesting outcome of U.S. tariffs is the break in the traditional cyclical sector models. Consumer staples fail when they are dependent on foreign supply for their margins. The growth of uncertainty in the present environment makes any equity value model suspect – and unlikely to inspire investor confidence. If 10-year U.S. bond yields can move 70bp in a week, then how do you know what the long-term neutral rate is? Until we can get a stable view of rates, equities will be uncertain. Therefore, the earnings season ahead may stop some of the selling out of risk positions, but it will not solve the volatility problem preventing value factors from returning as the key driver for finding a market bottom.

The pressure for investors to put money to work starts with the cyclical pressures for creating a market bottom. The two events that could build out such a story for the second quarter rest on Q1 earnings and corporate outlooks with tariffs. The role of growth and inflation factors driving Fed policy and the bond markets also anchor the 10-year yields and are important for any value metric. Volatility and volumes from our data and ETF flows from our franchise do not indicate that we have found a bottom for markets.