Fed Cuts and Risk

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

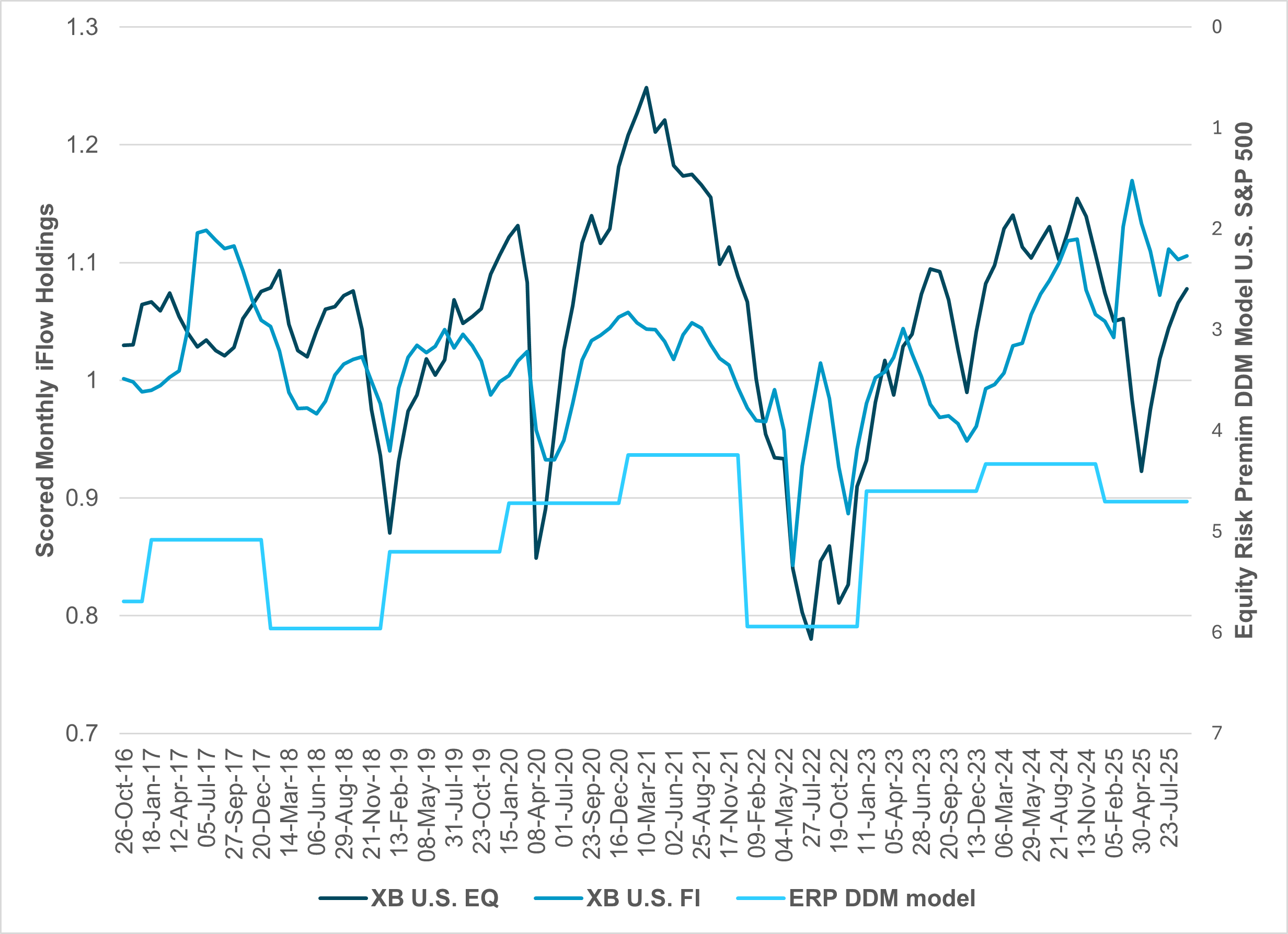

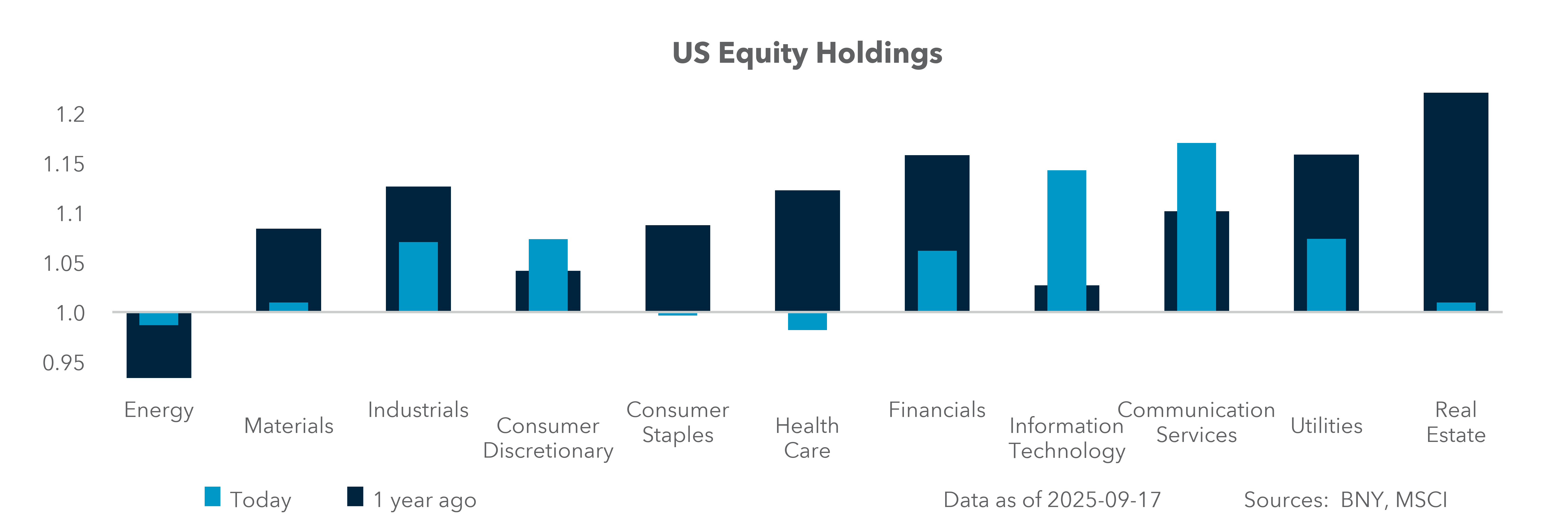

EXHIBIT #1: CROSS-BORDER HOLDINGS OF U.S. EQUITIES AND FIXED INCOME VS. U.S. EQUITY RISK PREMIUM

Source: BNY

At the FOMC press conference this week, Chair Powell described the 25bp rate reduction as “a risk management cut” given concern about growing labor market weakness, leaving room to move from restrictive to a more neutral policy. The Fed’s bias to ease 2–3 more times this year changes the equation for risk in equities. The key point to keep in mind is that this is considered “insurance” easing, not an emergency action. There are historical parallels to previous easing cycles in 1998 and 2001. The Fed’s current economic projections call for higher growth, slightly higher inflation and stable jobs. As a result, investors expect corporate earnings to improve, fueling the conviction that the stock market rebound will continue. The equity risk model now reflects current bond yields, future expectations of earnings growth for shares, including dividends and buybacks, and tax changes. The U.S. has room to rally, with holdings below the levels of EMEA and APAC in portfolios.

Our take

Over, the past ten years, iFlow cross-border holdings of fixed income and equities for the U.S. market have usually shown a negative correlation with risk during times of economic stress. Equity holdings for foreigners recently dipped well below the long-term average before recovering after April. Equity holdings are now near their average while fixed income is 2–3% above average, with most below the 5y duration. The dividend discount model for implied equity risk premiums is shown in Exhibit #1 using expected earnings growth and dividends. The higher the risk premium, the better the future expected returns. By this value measure, markets have room to move higher.

Forward look

The current underheld position in U.S. shares relative to the rest of the world and the divergent monetary easing cycle suggest we are approaching a turning point for U.S. equity outperformance into year-end. Markets are likely to focus more on equities than bonds through the rest of the year as equity risk premiums are in the middle of the range of the last 10 years vs. bond risk premiums, which are just off their August highs of around 60bp.

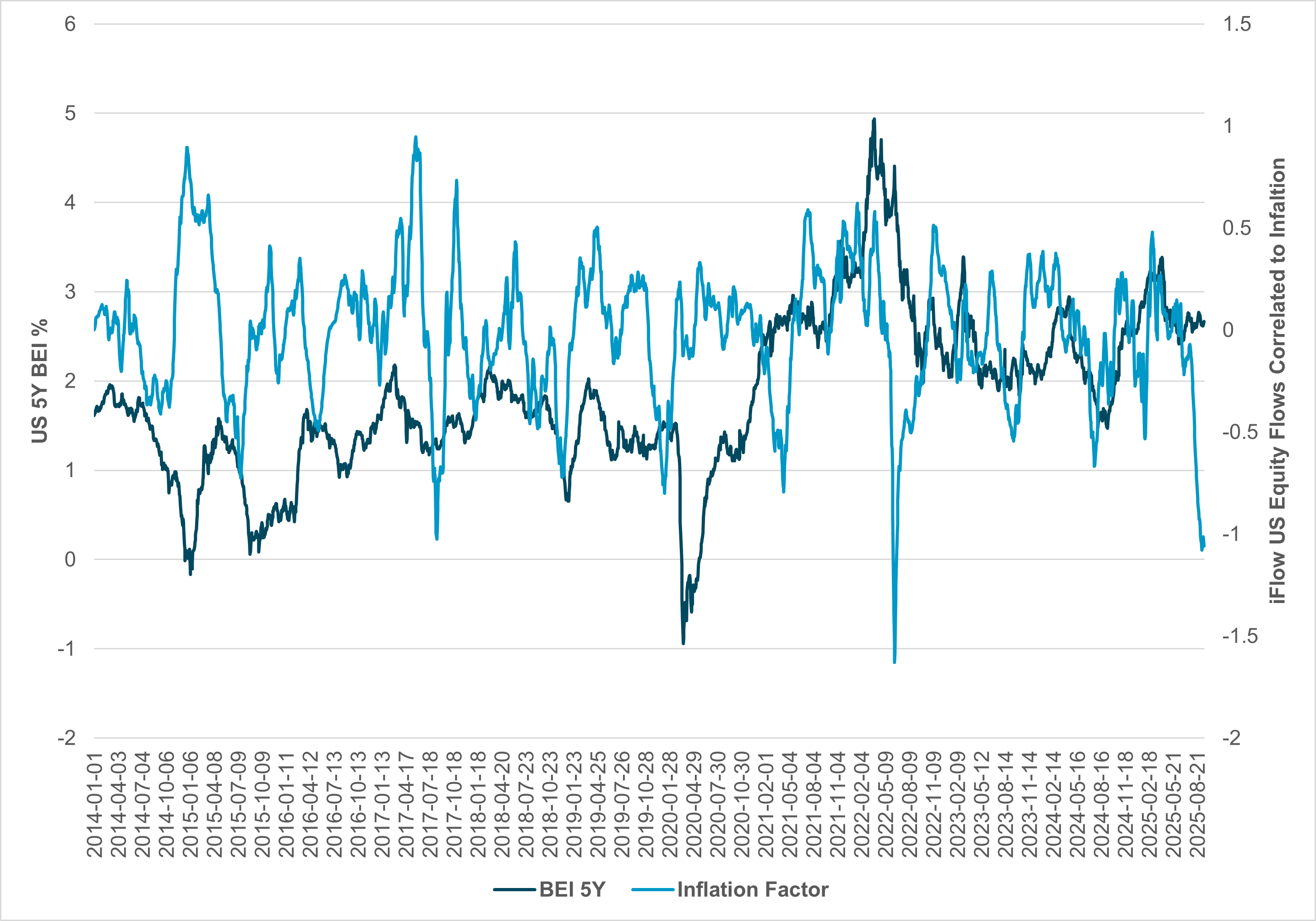

EXHIBIT #2: EQUITY INFLATION FACTOR FLOWS VS. 5Y BREAKEVEN INFLATION SWAPS

Source: BNY, Bloomberg

Our take

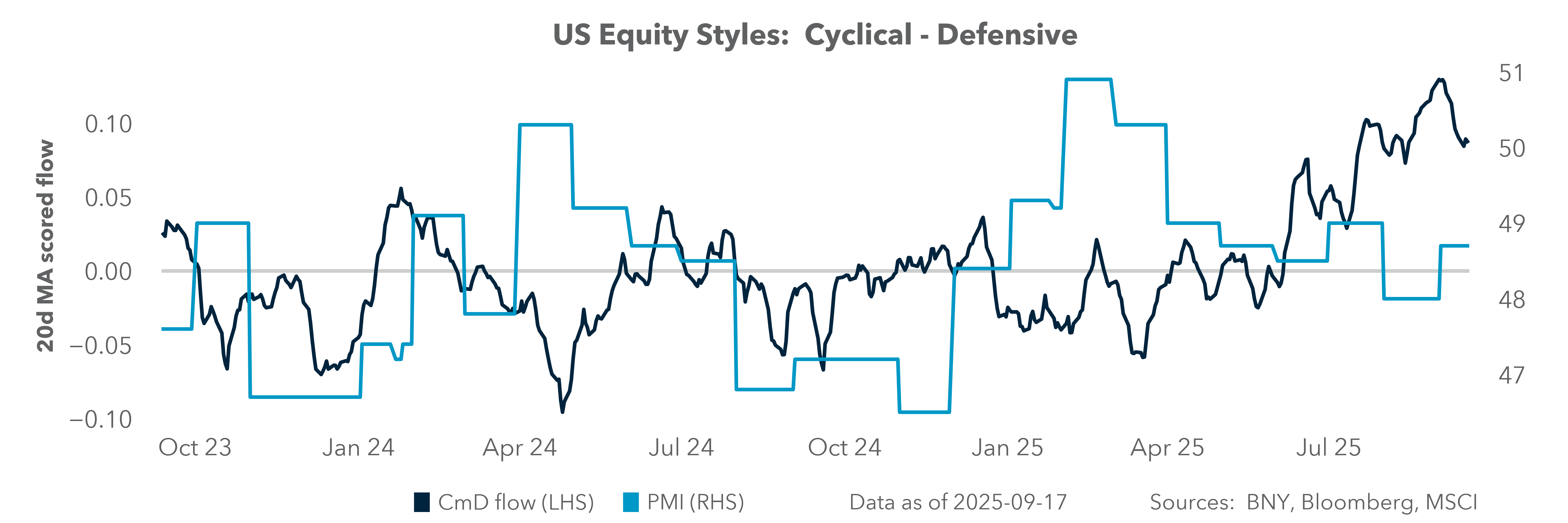

The U.S. markets are more concerned about growth than inflation. The rate cut and projections from the Fed added to “inflation lower”-related flows in equities. Exhibit #2 tracks our domestic and cross-border flows in U.S. shares and how they correlate to industry sectors by inflation. The result of tariff policy for investors is less about inflation and more about growth concerns. The drop in inflation worries reflects the FOMC focus on jobs and the lower wages seen across some key service sectors. AI investment themes and productivity are also clearly in the mix.

Forward look

There may be less disconnect between U.S. bonds and stocks than analysts believe given the dramatic decline in inflation concerns in U.S. equity flows. The flows we have seen in equities since April reflect more rotational plays than trend chasing. IT and communications sector holdings are the most overheld, but this is led by cross-border rather than domestic investors. The risks for inflation surprising to the upside could be the key catalyst for larger equity selling in industries not yet fully affected by tariff turmoil.

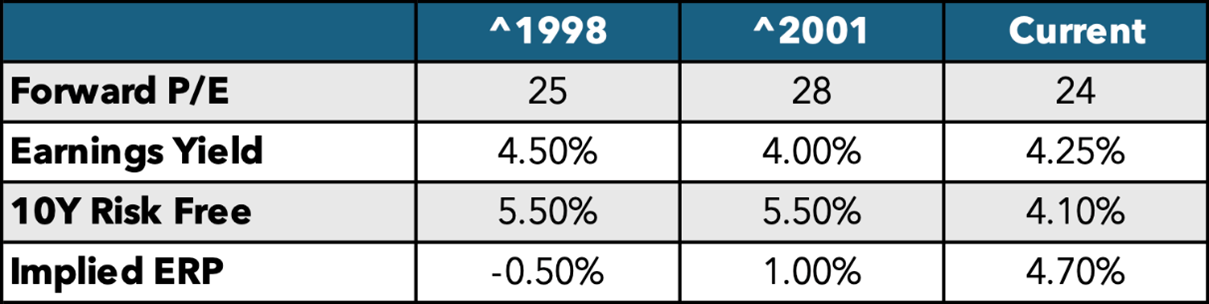

EXHIBIT #3: TABLE OF EQUITY METRICS FOR 1998, 2001 AND 2025

Source: BNY, Bloomberg, NYU Stern

Our take

The Fed cut rates in 1998 as an insurance policy against the risk of an economic slowdown following the collapse of LTCM and the financial crises that hit Asia and Russia that year. Given the turmoil in global banking, the central bank placed a premium on financial stability. The Fed cut rates again in 2001 in response to the fallout from the bursting of the Nasdaq bubble in March 2000, after having increased rates to 6.50% in May 2000. It made an emergency cut of 50bp in January 2001 following the financial fallout of the revaluation and its impact on consumers, and then eased to 4.75% as the economy slowed that year. In this case, the Fed was responding to a cyclical slowdown and the risk of a recession. Current conditions are closer to the ones that prevailed in 1998 than those of 2001.

Forward look

It is important to consider the historical context because markets are looking for a valuation crack in the current rally since April. This fear is misplaced. The risk of higher rates is now more about rate curve views linked to inflation concerns and central bank credibility. U.S. markets are positioned much more defensively for the next four months than the headlines about record-high indices suggest. The October 3 jobs report and the start of Q3 earnings on October 13 will set the tone for how inflation and growth drive rotational risks in U.S. shares, with a sharp focus on the connection between AI investments and rate cuts and margins.

The Fed’s recent 25bp cut is best understood as an “insurance” move – more akin to 1998 than 2001 – that is intended to manage labor market risks rather than counteract a deep recession. U.S. equities are seen as under-owned relative to the rest of the world, leaving room for catch-up, with equity risk premiums modest but not stretched to dangerous lows. Forward valuations look healthier compared to past cycles, with an implied ERP (approx. 4.7%) that is significantly stronger than the compressed levels of 1998 or 2001. Risks ahead revolve less around a growth collapse and more around unexpected inflation pressures, the credibility of central banks and investor positioning. In the near term, earnings season and key jobs data are expected to define the sustainability of the rally, particularly given heavy cross-border allocations to IT and communications stocks. The odds of a recession are not zero, and any outside shock will drive significant volatility. Whether the U.S. cuts ahead are sufficient to offset any such risks are relative to the rest of the world where values more diffuse but positioning more concentrated.