Equity flows not expecting a hawkish Jackson Hole

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

iFlow > Equities

An in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Geoff Yu

Time to Read: 5 minutes

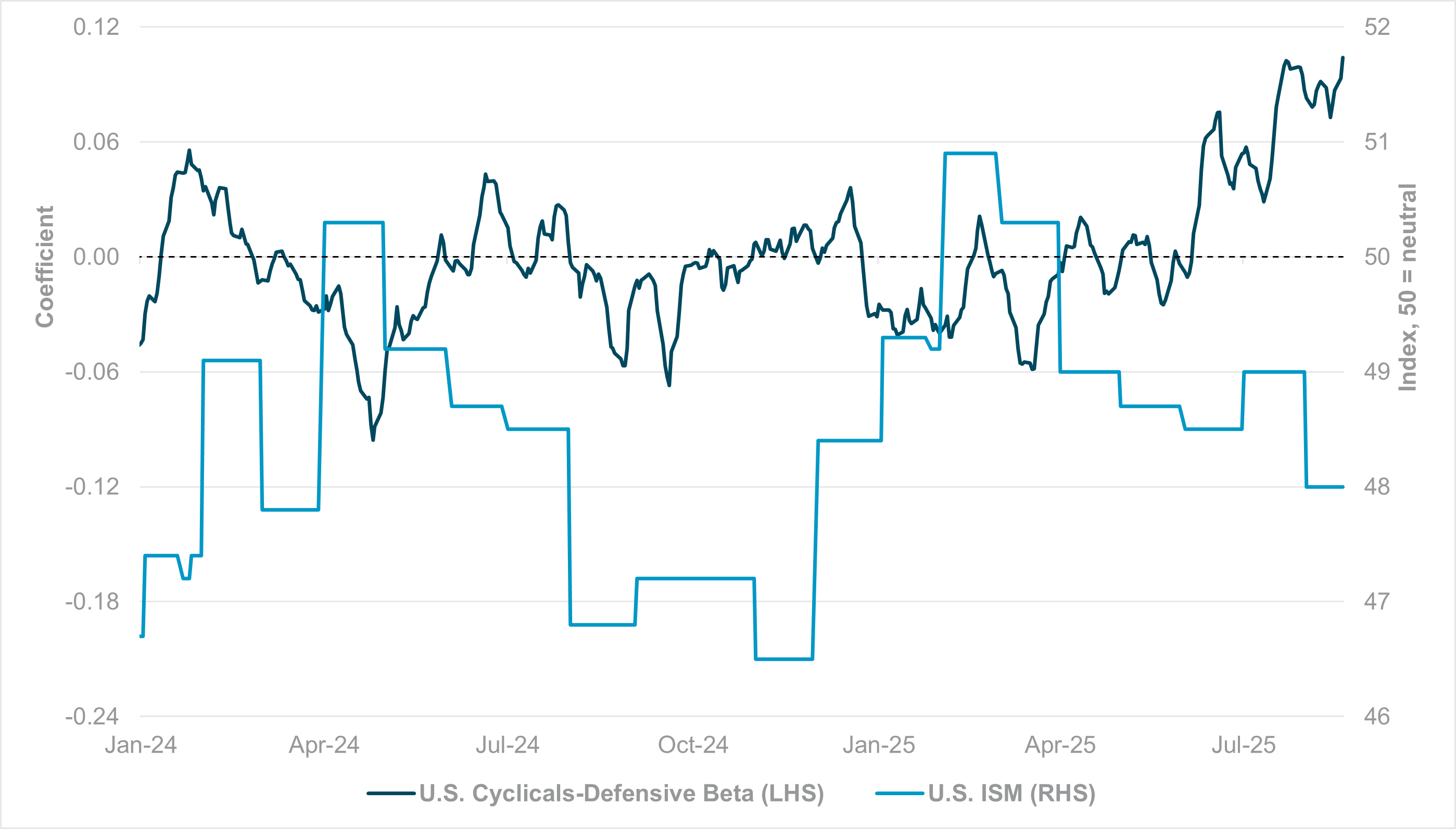

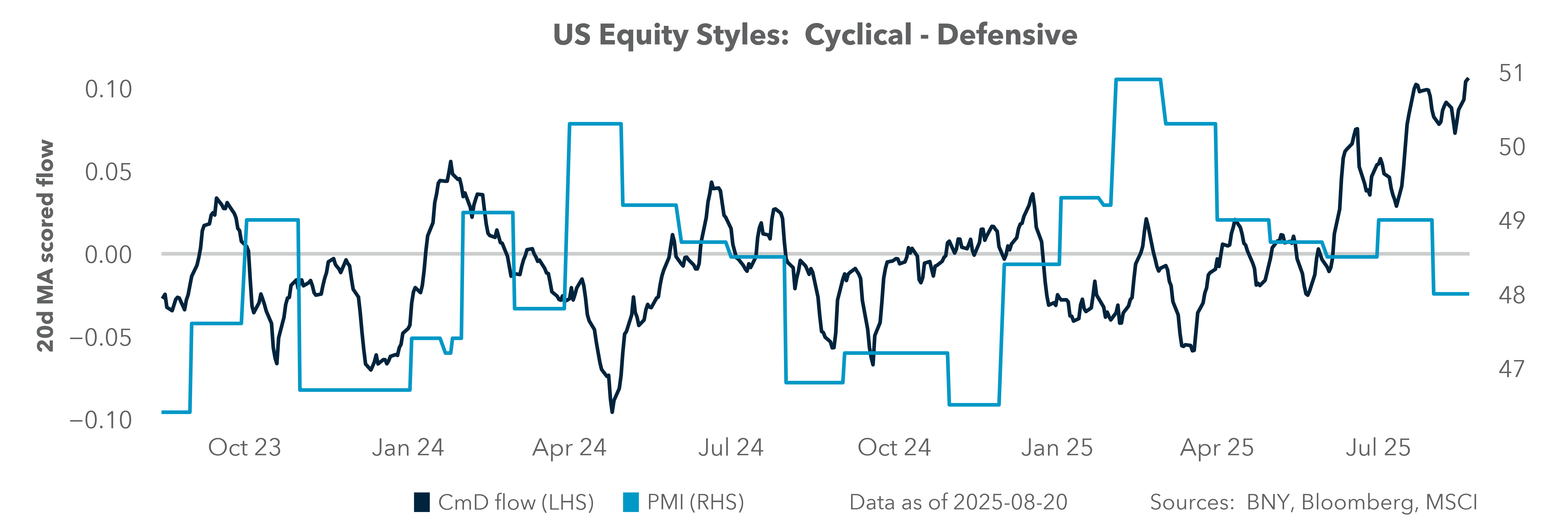

EXHIBIT #1: U.S. CYCLICALS VS. DEFENSIVES RELATIVE PERFORMANCE BETA VS. MANUFACTURING ISM

Source: BNY, Bloomberg; the difference between the first principal component of flows (rolling 65-day sum) into 16 cyclical industry groups and the same for flows into eight defensive groups, compared to manufacturing ISM index.

Our take

Balancing the risks between a weakening labor market but without commensurate easing in wage growth and inflation will likely feature prominently in Fed Chairman Powell’s Jackson Hole speech today, accompanied by forceful defense of central bank independence by all participants around the world. The net result of both factors is that restrictive conditions will linger. The poor performance in equity markets in the run-up to the symposium suggests some concern that a less dovish tone will be set for the September FOMC meeting, but we believe investors should take a closer look at their current flows and positioning, which are looking increasingly misaligned with the economic cycle. The short-term narrative may point to greater preference for defensive stocks, but our data show the opposite is true: the conventional relationship between the behavior of flows, in which cyclicals outperform defensive flows based a cyclical indicator such as manufacturing ISM, has not just been absent but inverted since the beginning of the year (Exhibit #1).

Forward look

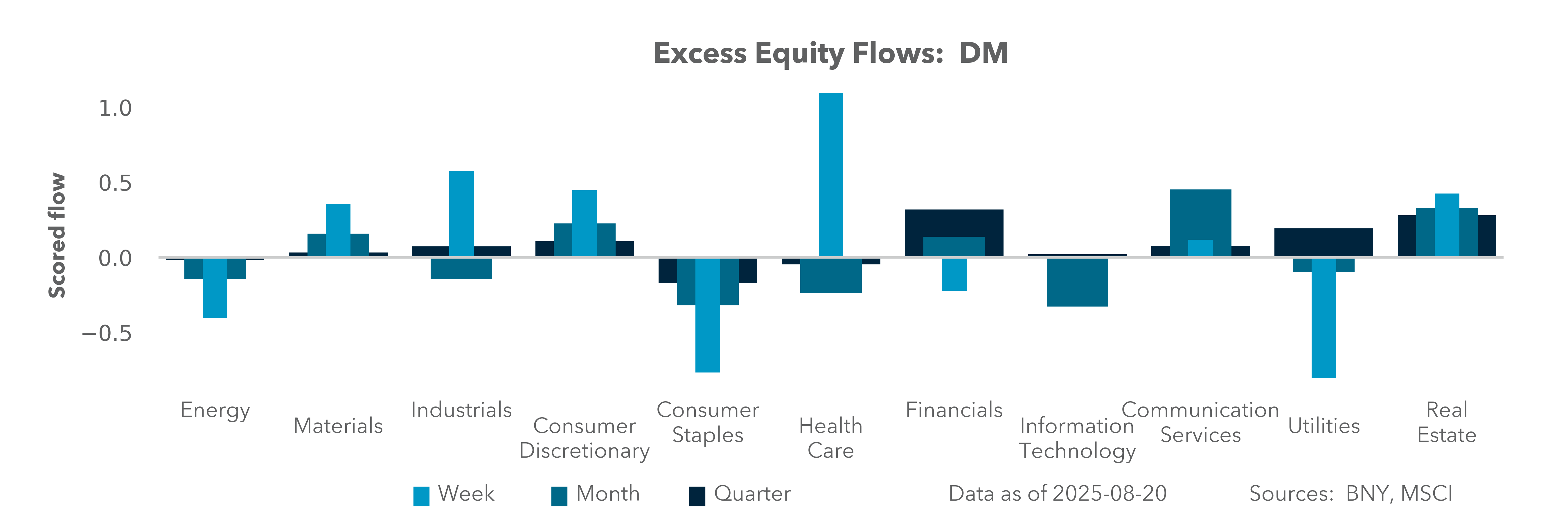

The current strength of cyclical flows is being supported by the likes of information technology and communication services, but we have observed similarly robust interest in sectors such as materials and industrials, which at present do not have secular investment themes in place which can defy contractionary outlooks from survey data. We acknowledge that earnings weakness in energy and healthcare – with the latter currently weighed down by idiosyncratic factors – is also generating exceptional weakness in defensive sectors. Consequently, reversion to data and policy will require a shift in performance for both styles, but we expect cyclical rotation to dominate the process.

EXHIBIT #2: EXCESS MONTHLY FLOWS INTO SOUTH KOREAN AND TAIWANESE EQUITIES

Source: BNY, Bloomberg

Our take

If current cyclical flows in the U.S. adjust lower, there will be material implications for some well-held and high-performing markets which are highly integrated with realized investment themes in the U.S. Geopolitics may have been the focus for the White House this week, but sector-specific tariffs still loom large and supply chain partners in the Asia-Pacific region are sounding the alarm over outcomes. For example, yesterday the Philippines’ Economic Secretary Arsenio Baliscan warned that the 300% semiconductor tariffs floated by President Trump earlier in the month “would kill global trade.” Our data indicate that on an excess flow basis (i.e., daily flows with the mean 1-year flow removed), flows into Taiwanese and South Korean equities have remained firm for all or parts of the last three months. With cyclical flows already under pressure, a further price-based demand hit would be highly destabilizing to a very concentrated question in Asia.

Forward look

We doubt that some of the larger tariff numbers involved will be realized, but the risk alone underscores the multitude of risks facing global tech. Yet, there are often attempts at mitigation as well, with the latest being potential U.S. government investment in critical semiconductor companies. This may not even be limited to the U.S. as Taiwanese authorities have indicated that proposals have been made surrounding U.S. government investment in local chipmakers as well. Such plans will likely face geopolitical hurdles, but we also fear the market may be looking for an “AI put” for the global tech industry due to strategic needs, thereby keeping valuations elevated despite the clear need for cyclical adjustment.

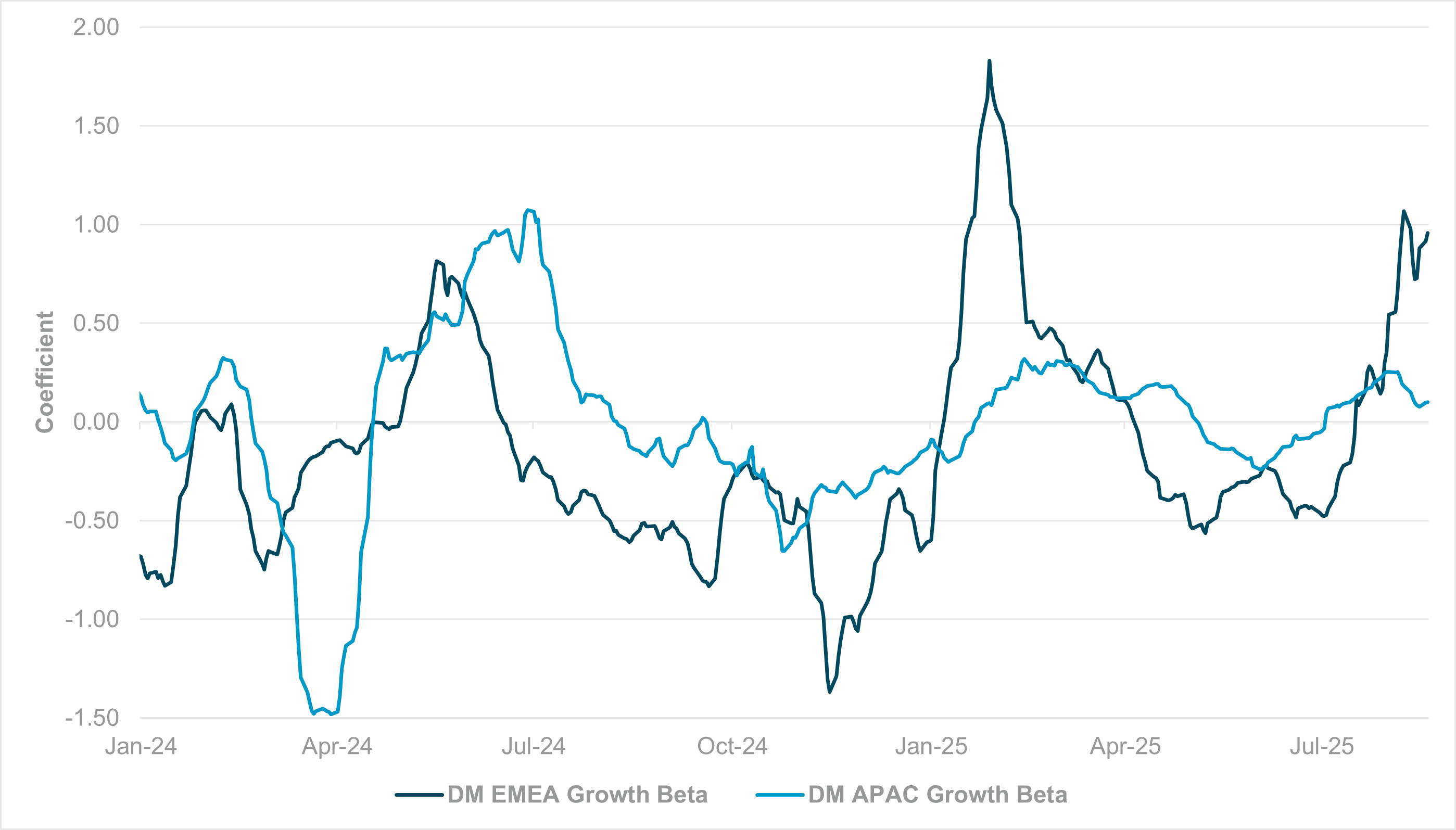

EXHIBIT #3: REGRESSION COEFFICIENT OF IFLOW SURGE FLOWS VS. SECTOR P/B RATIOS, DM EMEA VS. DM APAC

Source: BNY, Bloomberg LP; regression coefficient of daily surge flows by iFlow sector’s scored flows vs. standardized price-to-book ratios of the respective sectors.

Our take

Although not as extreme as U.S. equity flows at present, we believe pursuit of growth and concentration risk in European equities is also approaching extremes. ECB President Lagarde will also be at Jackson Hole; from where she stands stagflation risk may not be as big a problem for now, and the realization of an EU-U.S. trade deal has provided a good level of certainty for local firms. Nonetheless, trend improvement in both soft and hard data, especially in manufacturing, is starting to look exhausted, but equities are still pushing for new highs. In contrast, Bank of England Governor Bailey, who will also be in Wyoming, might need to offer a cautionary tale on the risks of cutting policy rates into rising stagflation. We doubt financial conditions through the interest rate channel in developed Europe can ease much further, as between the ECB and the BoE, there’s probably scope for only one more cut by the former for the rest of the year. Yet, the “growth beta” for developed Europe’s equity flows are now hitting their highest levels since the beginning of the year, and above any point in 2024. This means that equity flows into developed Europe are moving into “expensive” industry groups and out of “cheap” ones. In contrast, flows into developed APAC are neutral, indicating no particular style preference.

Forward look

Compared to the U.S., perhaps the low absolute level of rates and greater capacity for fiscal impulse is supportive of a higher growth narrative for Europe. However, the same reasons were put forth earlier this year and led to a fundamental rotation in asset allocation preferences away from deep value-seeking at the end of 2024 toward growth. For Europe, it is less about financial conditions but more about end-demand, especially from the private sector. There is a strong case for public sector investment to “crowd-in” private sector demand, ultimately being channeled back into household real incomes, but we struggle to see any marginal information in the EU, let alone the U.K., to support an extension of this style’s performance beyond current levels. In contrast, the lack of a high growth beta in equity flows in developed APAC, both now and historically, perhaps underscores the lack of fiscal impulse in the region. Unfortunately, we believe this will remain the status quo. Even in the face of strong external headwinds from U.S. tariffs and pledges of fiscal support for domestic rebalancing, caution in government expenditure remains the norm. Without a demand catalyst, efforts to improve margins are unlikely to be impactful.

Markets will likely wait until after Chair Powell’s speech later today before deciding whether to extend this week’s dour performance in technology- and growth-related sectors and stocks. However, simply to attribute performance in either direction to the Fed’s capacity to ease (or not) is far too reductive. Stagflation concerns hanging over the U.S. and global economy are not new, and financial conditions in non-monetary factors such as the shape of the curve and corporate spreads have not loosened at all this year. However, thematic growth flows in the U.S., and to a lesser extent in Europe, were based on secular shifts but now look overextended relative to company fundamentals. A “friendly” Jackson Hole speech will help avoid accelerated selloffs, but there is a clear need for growth-based equity exposures to realign with the global cycle, especially demand factors.