Don’t Sell in May and Don’t Go Away

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Equities provides an in-depth look each Friday at the factors shaping equities markets in developed and emerging economies around the world.

Bob Savage

Time to Read: 5 minutes

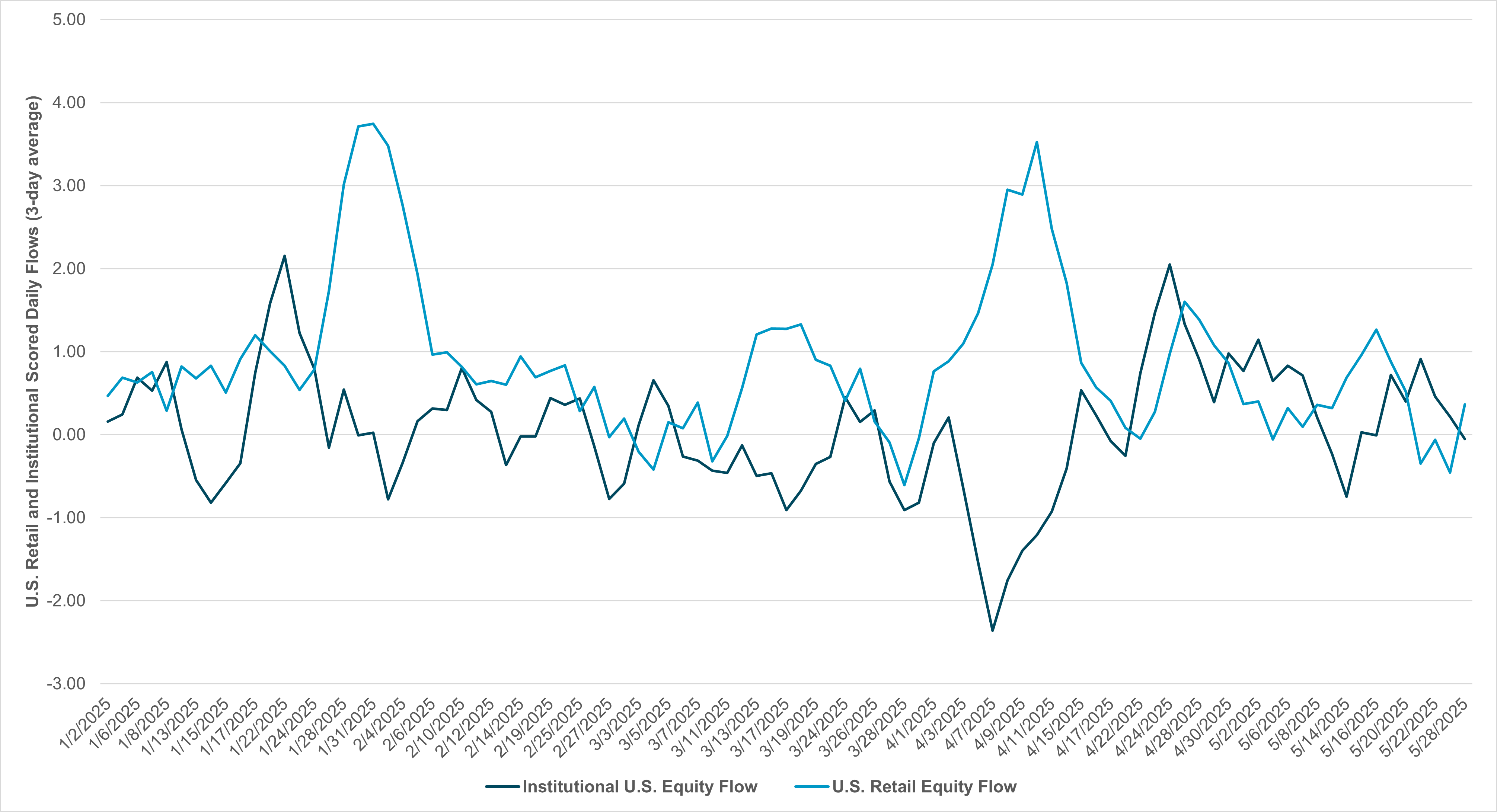

EXHIBIT #1: RETAIL VS. INSTITUTIONAL FLOWS – SELLING THE RALLY AND BUYING THE DIP

Source: BNY

April taught investors to buy the dip, but May’s lesson is less clear, as institutional flows caught up with retail flows even as retail investors sold the rally. The key question as we head into June then is, does this rally have legs or will it lead to regrets by midsummer? History suggests that July rallies tend to result in lighter summer markets with less investor concern. This year could be different, however, with a number of important risk events up ahead. Markets will find themselves at a crossroads next month, setting up the possibility of a summer of discontent as tariffs, taxes and policy risks loom in the months ahead.

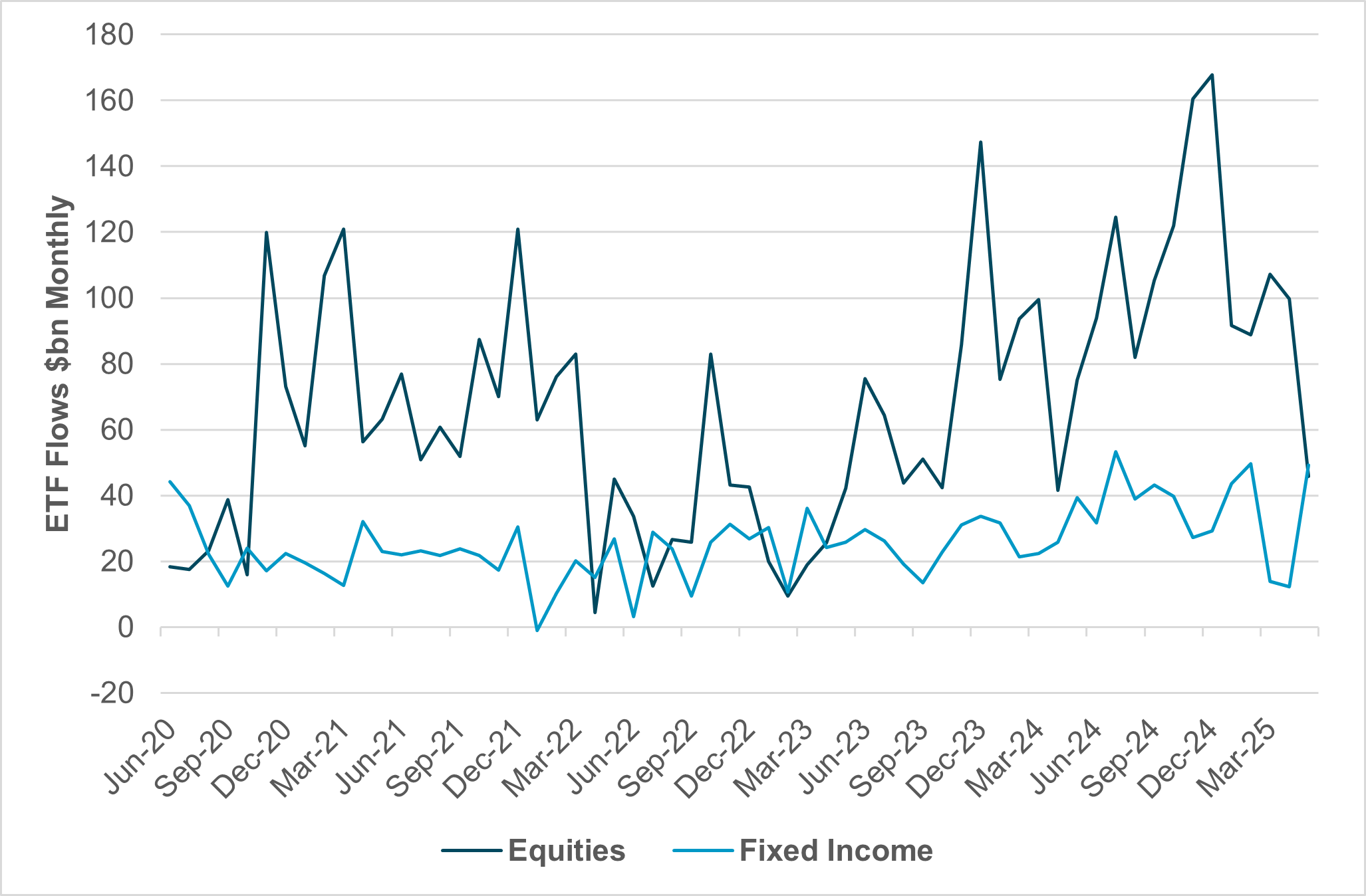

EXHIBIT #2: ETF FLOWS SHOW MORE BOND BUYING THAN EQUITY BUYING

Source: BNY, Bloomberg

The buy-the-dip action of ETF flows that we saw in March and April has reversed in May. Fixed income, by contrast, saw flows spike back to their February levels, with retail investors and passive funds leading the price action. Also notable this month has been the moderate volumes in U.S. shares. Higher yields in May will be a key factor to consider when making equity allocations.

Our take

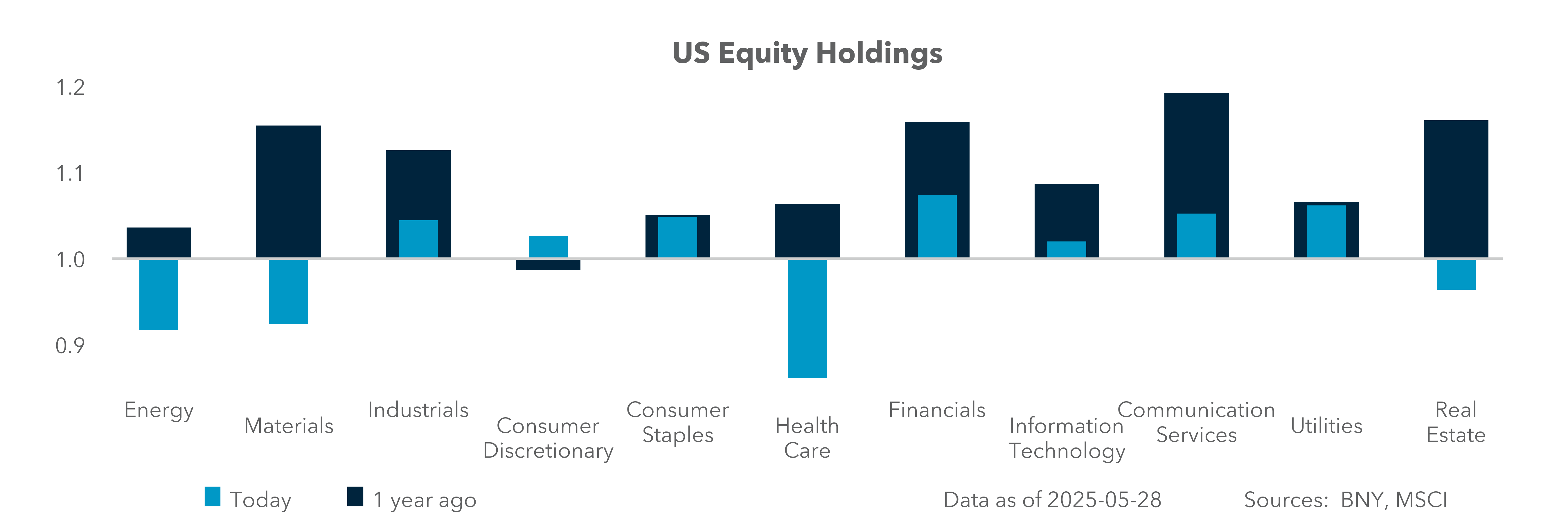

We have seen ongoing cash holdings and duration buying in fixed income while momentum buying dominated equities in the U.S. iFlow holdings show the U.S. is at its 10-year average of around 1.01, while EMEA developed markets are at 4%, led by Italy and moderated by selling of German equities. APAC has also seen inflows, dominated by the Chinese tech sector, with Hong Kong leading the region. The financial and industrials sectors have been at the forefront of the global rally, while IT and communications saw outflows. ETF flows have reflected more of a wait-and-see attitude compared to the tape, which has returned to a slightly positive stance, with the iFlow Mood Index back to positive.

Forward look

Market narratives suggest flows are consolidating following a relief rally, and further directional conviction will require new macro or policy catalysts. Whether we continue to see this into June depends on whether the data support a narrow soft-landing view for U.S. growth along with continued hope for a Fed rate cut in late summer. Investors will be watching for signals about Q2 earnings, and the confessional period ahead will be a key factor in how Q2 rebalancing pressures play out, with many seeing USD weakness as supportive of U.S. equities.

EXHIBIT #3: IFLOW HOLDING CHANGE AGAINST S& P500 SEASONAL RETURNS

Source: BNY

Our take

Over the past 10 years, May and June have been the best months for equity risk, but the last 20 years point to July and November as the best months. Comparing these results against changes in iFlow holdings over a 10-year seasonal basis, we see that February and May dominate investor inflows. There is significant debate about seasonality and whether it matters to markets. The strategy of selling in May and going away failed in 2025, but we have seen a seasonality factor at play in our flows linked to non-market factors like taxes, half-year-end strategy shifts and elections.

Forward look

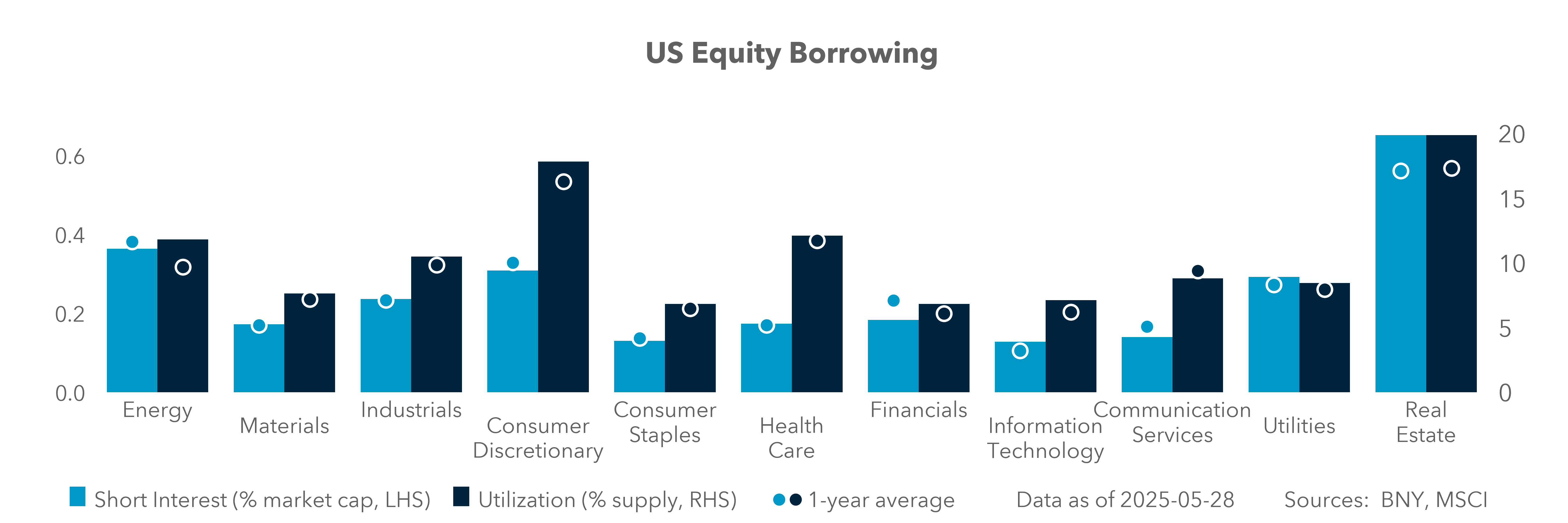

The biggest risks in July stem from the long list of major events, including the end of the pause of tariffs, Q2 earnings, meetings of the FOMC and BoJ, and elections for Japan’s upper house of parliament. The bias to own equities in July and the current sanguine mood about ongoing uncertainty have added to analysts’ predictions of a summer of discontent. We see the lack of significant long positioning and the ongoing rise in VIX for July as evidence that investors are aware of the risks ahead. Our own flows for borrowing in the U.S. show that sector shorts are near historical yearly highs with energy, consumer discretionary, IT and real estate seeing the biggest utilization of short positions. The one factor that stands out for a sell-off risk in July is the lack of skew in the VIX. The global reversal risks in Europe and Asia could be significant if the U.S. data hold and if Trump’s tariffs prove less scary given the new phase of legal challenges to reciprocal and emergency actions.

Looking ahead, market narratives suggest there will be a period of consolidation following the relief rally, with further directional conviction dependent on new macro or policy catalysts. Investors will closely monitor Q2 earnings and the confessional period, with USD weakness potentially supporting U.S. equities. The debate over the impact of seasonality’ on markets continues, with May and July historically strong for equity risk. However, the 2025 “sell-in-May” strategy failed, highlighting seasonality’s link to non-market factors like taxes and elections. July’s risk calendar, including the end of the tariff pause, Q2 earnings, and key central bank meetings, suggests heightened awareness of upcoming risks. Sector shorts in the U.S., particularly in energy, consumer discretionary, IT and real estate, are near historic highs, with the absence of VIX skew posing a sell-off risk. Global reversal risks in Europe and Asia could be significant if the U.S. data hold and Trump’s tariffs face further legal challenges.