Reassembly Revisited: The Path to Central Clearing

What the U.S. Treasury clearing rule means for market participants

What the U.S. Treasury clearing rule means for market participants

Nate Wuerffel

Time to Read: 12 minutes

The United States Treasury market isn’t just another asset class — it is arguably the heart of the global financial system. With close to $29 trillion outstanding,1 the U.S. Treasury market is the largest bond market in the world, and it serves as a port in the storm for global investors in times of market stress, providing safety and liquidity to investors around the world. As Treasury market transactions shift to central clearing, a Fixed Income Clearing Corporation (FICC) survey estimates over $4 trillion dollars in daily transactions across cash and repo trading will shift from bilateral markets into centrally cleared markets,2 a major change that requires significant preparation from market participants.

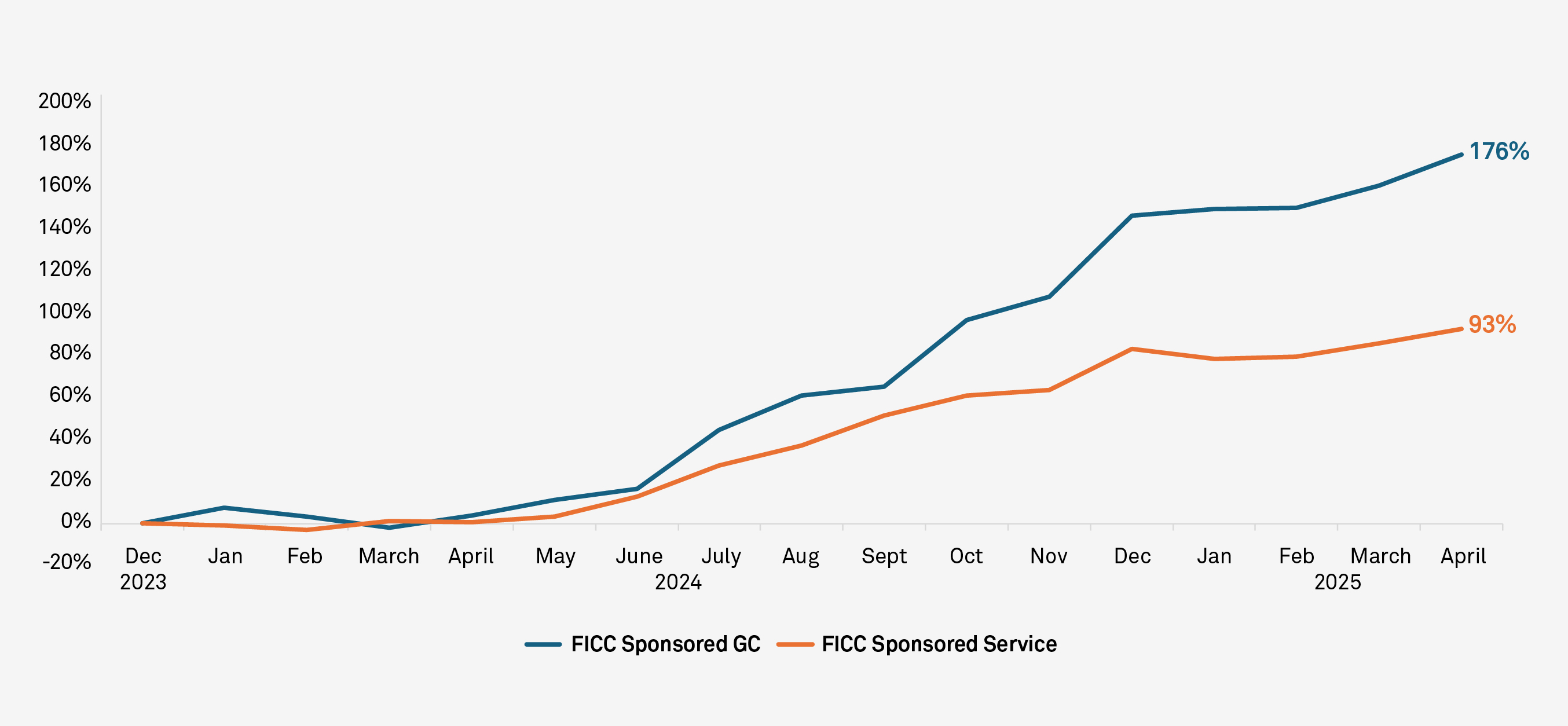

In February, the SEC extended the deadline for compliance with the central clearing rule, providing the market essential time for implementation. The central clearing rule will effectively reassemble the U.S. Treasury market, and while market participants are still preparing, market behavior has already begun to shift as market participants have increased their centrally cleared activity. (Figure 1)

FIGURE 1: FICC-SPONSORED REPO SERVICE GROWTH

Source: DTCC, June 2025

The rule requires members of a U.S. Treasury central counterparty (CCP) to centrally clear a large portion of their cash and repo trades, and given the breadth of participation in the market, it will impact a wide swath of market participants globally, including banks, broker-dealers, hedge funds, asset managers and asset owners.

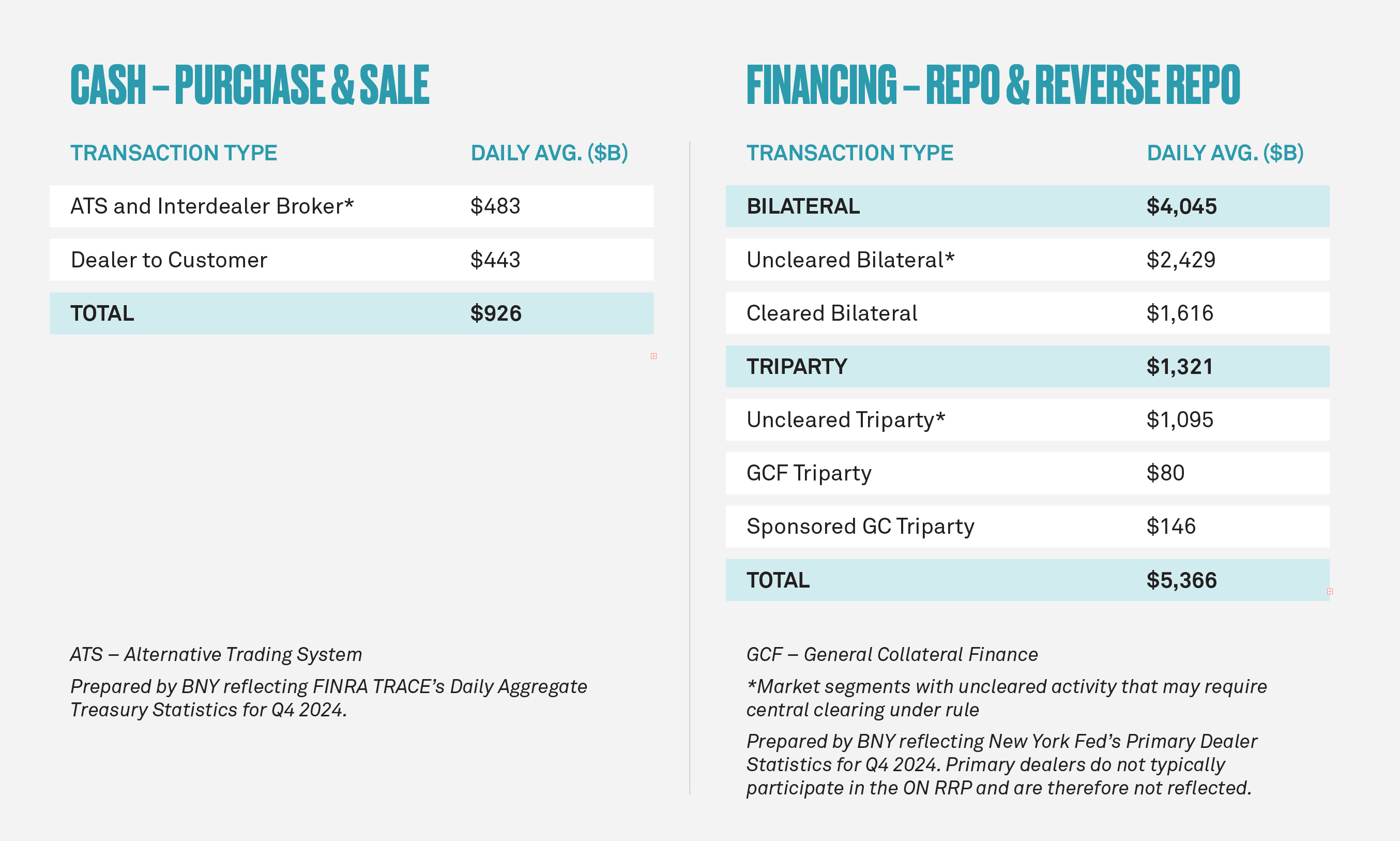

FIGURE 2:

Safety and liquidity are the core tenets of the U.S. Treasury market and are central to its deep participation. Central clearing can help bolster the safety and liquidity of the market if implemented effectively, and the SEC’s extension of compliance dates for the rule was aimed at supporting a smooth implementation. The extension gives the industry time to adequately prepare for the changes to come, and to work with regulators to address open issues around the scope.

Although there has been significant work by the industry to prepare for central clearing since the rule was adopted in December of 2023, market participants are at varying levels of readiness. Some market participants are further along in the process and have already begun conducting a significant amount of their activity in centrally cleared trades. Centrally cleared repo activity has grown substantially on a voluntary basis since the mandate was adopted, with FICC-sponsored repo and reverse repo volumes growing by more than 90% since December 2023. (Figure 1) Centrally cleared triparty repo activity has grown as well, with FICC-sponsored GC volumes growing by more than 170% over the same time period.3

But even for those familiar with central clearing, the implementation of the rule is highly complex and will require further changes to enter into or expand centrally cleared repo. These changes span several key areas, including legal, operations and systems. The magnitude of these changes, combined with the scope of the mandate and key implementation items, prompted a collection of industry groups, including the Securities Industry and Financial Markets Association (SIFMA), the Futures Industry Association (FIA), the Managed Funds Association (MFA) and the International Swaps and Derivatives Association (ISDA), to request in January that the implementation dates be pushed back by a minimum of 12 months.

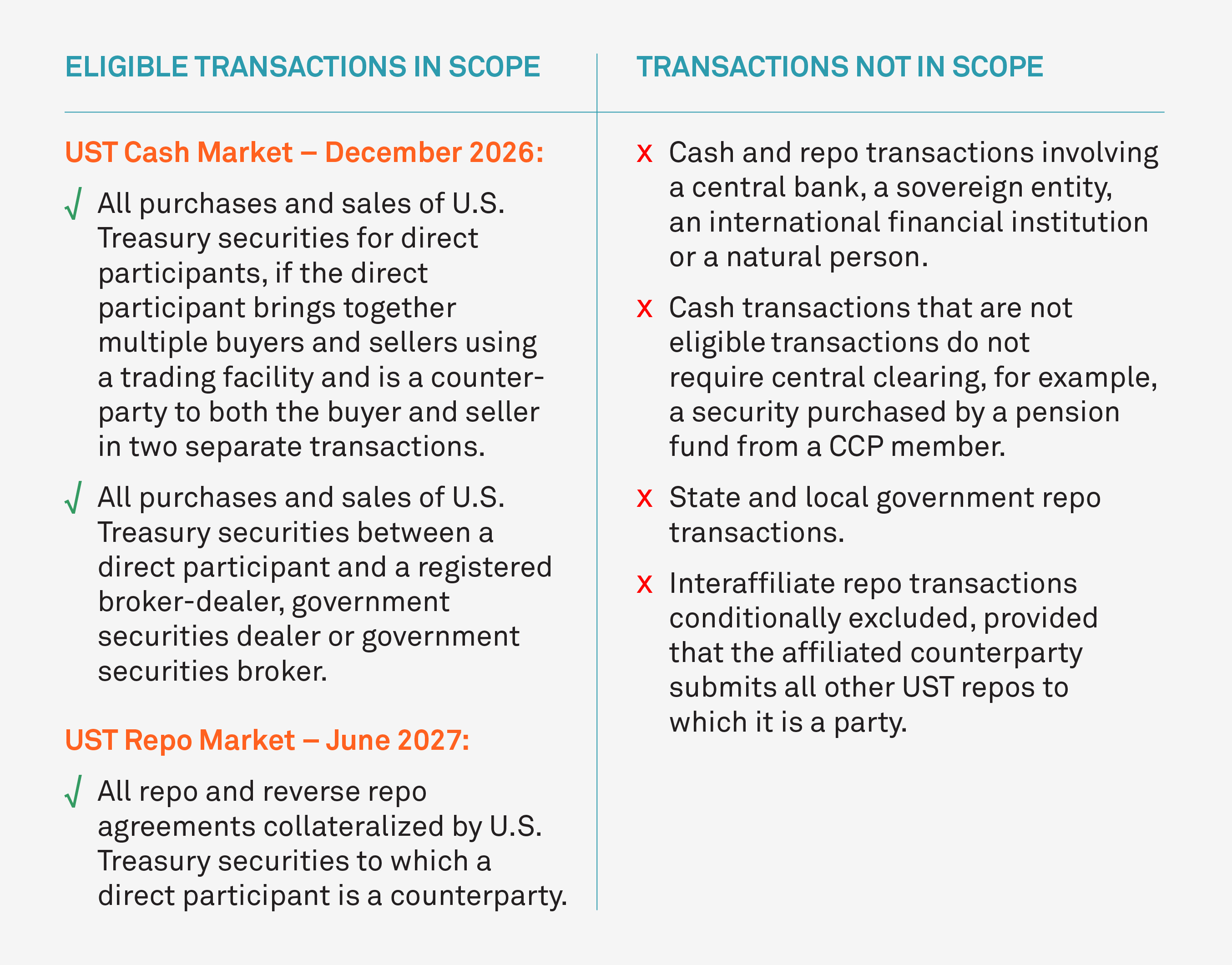

FIGURE 3:

In February, the SEC announced a 1-year extension to the compliance dates for the rule, with cash clearing now required at the end of 2026 and repo clearing required at the end of June 2027. (Figure 3) The SEC also issued a temporary exemption for firms to meet the original March 2025 deadline, extending it to September 2025, in order to separate house and client activity.4 After considering the industry associations’ request, the SEC agreed that an extension in the compliance dates would allow for further engagement on compliance, operational and interpretive questions related to the rule. Given the extension, the industry is now focused on a number of key scoping issues that remain outstanding, as well as key implementation challenges.

There are several scoping issues where the industry is seeking clarification from the SEC to help with a successful implementation of central clearing. These include requests from market participants to refine the scope of the rule associated with mixed collateral triparty repo transactions and interaffiliate repo transactions, among others. Both items, if not addressed, add complexity to the implementation of the mandate, and bring a large number of additional transaction volumes into scope for central clearing.

Market participants have raised concerns around the potential impact the central clearing rule could have on interaffiliate transactions, which are within the scope of the rule. Interaffiliate repos play an important role in allowing global firms to manage their liquidity and risk efficiently across the various legal entities that constitute the larger firm. For example, interaffiliate repos are often used to move Treasury securities so they can be posted as margin by an affiliate, or so that an affiliate can meet capital or liquidity requirements.

The SEC initially required that interaffiliate repos be subject to clearing to avoid evasion; the concern being that a FICC member could shift their in-scope client repo activity to an affiliate that was not a FICC member and thus be able to avoid the requirement to clear transactions. To provide some flexibility under the rule, the SEC — in response to industry feedback — has since included a conditional exemption that exempts clearing members from centrally clearing interaffiliate repos, provided that the affiliate submits all their other eligible repos for central clearing.5

For example, if an FICC member wanted to exempt the interaffiliate repos that they conduct with their European bank affiliate, all the client-eligible repos that the European bank affiliate conducts would then need to be centrally cleared. SIFMA and other market participants have asked for further flexibility under the conditional exemption. First, they have asked that the definition of an affiliated counterparty be broadened, as it currently only applies to affiliates that are a bank, broker-dealer, or futures commission merchant (FCM). Additionally, they have asked that a small share of client-facing repo be allowed to remain outside of clearing, even if the interaffiliate repos are exempt.

Based on current language in the central clearing rule, most market participants judge that mixed — or general collateral (GC) — repo transactions in triparty that contain Treasurys will be required to be centrally cleared. General collateral repos are a transaction where funding is provided against a general basket of security types; the specific securities that will be provided as collateral are not known at the time of the trade. In that transaction, the cash investor agrees to accept any specific collateral delivered by the seller, provided that it is eligible under the types of general collateral agreed to under the terms of the trade. The rate on the transaction reflects the range of general collateral that could be delivered, with higher funding rates applied to GC repos backed by general collateral with higher risk. For example, agency, corporate or equity GC repos are usually funded at higher rates than Treasury GC repos.

In most GC transactions, shortfalls in higher-risk collateral can be met by substituting lower-risk, higher-quality securities — like U.S. Treasurys — that are eligible under the terms of the trade. In this way, GC transactions are useful in funding markets because they provide flexibility in collateralizing repo transactions, including in times when the availability or market value of collateral changes, for example due to delivery failures or market volatility.

Treasurys play a particularly important role in GC repo trades. Because they are widely considered the safest, most liquid collateral, they are almost always eligible collateral in GC transactions and are often delivered to fill shortfalls in GC transactions including agency, equity, corporate and other types of repo. For example, across BNY’s collateral platform, close to 20% of the collateral backing agency GC triparty trades (in which agency mortgage-backed securities (MBS), agency debt and Treasurys are eligible collateral) are Treasurys.6 At the individual transaction level, over 40% of the agency GC transactions in triparty are collateralized by at least some amount of U.S. Treasurys as collateral, and nearly 10% of transactions are fully collateralized by Treasury securities.7

Treasury securities are used more often in times of market volatility, as we saw during market volatility in April 2025. As the market value of equity collateral declined, market participants substituted Treasury securities as collateral in non-Treasury GC transactions in order to remain fully collateralized. Despite the important role of GC repo transactions, regulators were concerned that they could be used by market participants to avoid complying with the central clearing mandate by entering into non-Treasury GC repo transactions in order to finance their Treasury securities. To address this, the SEC rule requires that all GC repos that contain Treasurys at the outset of the transaction must be centrally cleared. In practice, because all agency GC repo allows for Treasury securities to be delivered, the language in the rule would have the effect of pulling all FICC-eligible GC trades into clearing. This would have a particularly large impact on the agency GC triparty repo market, which is FICC-eligible. Requiring central clearing of agency GC repo transactions could raise the cost of funding these assets, which could in turn flow through to mortgage pricing.

Industry participants and associations have called on the SEC to take a more targeted approach in the rule. They argue that because agency GC trades are financed at a higher rate, there is an economic disincentive to financing Treasury securities through agency GC repo solely for the purpose of avoiding clearing. Moreover, regularly financing an unusually large share of Treasury securities through agency GC repo could be easily monitored through the compliance regime that is required as part of the rule.

In addition to allowing for the open scoping issues to be addressed, the extended timeline will provide more room for market participants to address key implementation issues with the rule, including the rollout of new access models that are more capital and margin efficient, the evaluation of additional CCP clearing options, and how best to clear transactions globally.

Many market participants continue to grapple with the implication of the additional margin requirements associated with central clearing. Under FICC rules, clearing members post margin when called upon by the CCP. However, there is no requirement that the members collect that margin from their clients. Margin practices between the member and their client are typically negotiated terms based on the risk and cost of the transaction.

Today, most non-centrally cleared bilateral repo transactions do not have haircuts or margin applied. As those trades move into central clearing, the cost to clearing members is likely to rise as they fund margin payments. How and whether that is passed along to clients will depend on counterparty risk management practices, the price of providing clearing services, and the ability or willingness of clients to post margin.

With respect to risk management practices, several public/private efforts have highlighted the importance of effective risk management practices for repo trades. These include the Treasury Market Practices Group (TMPG), a group of senior Treasury market professionals sponsored by the Federal Reserve Bank of New York, which recently published a set of best practices on U.S. Treasury repo risk management. These efforts, along with others, were also highlighted in recent testimony before the United States House Financial Services Committee Task Force on Monetary Policy, Treasury Market Resilience, and Economic Prosperity.

Repo transactions between dealers and money market mutual funds face a different margining challenge under the central clearing rule. Under current SEC rules, it is typical for money market funds to require dealers to overcollateralize trades with 102% of the value of the cash provided. In centrally cleared repos, dealers typically continue to overcollateralize their transactions with money funds, but also separately must post margin to the CCP. This “double margining” leads to higher margin and capital costs for repo trades between dealers and money market mutual funds.

Two potential solutions in development are the FICC-sponsored GC “Collateral-in-Lieu” model and the FICC Agent Clearing Service, both of which aim to offer direct participants significant savings on margin and/or capital costs. These solutions could play a crucial role in lowering the cost of implementing the clearing rule across the industry.

The FICC is currently the only approved U.S. Treasury market CCP. However, additional entities, including the Chicago Mercantile Exchange (CME) and the Intercontinental Exchange (ICE), have announced that they intend to enter the market. Both CME and ICE announced their intention to apply to become Treasury CCPs in 2024 and have been working to develop their new access models. CME filed an application with the SEC in January 2025 and public comments were due in March 2025. ICE has yet to officially file its application.

The extended timeline should allow market participants a window to evaluate these new clearing approaches. A recent study by the Treasury Borrowing Advisory Committee (TBAC) examined the possible outcomes of having multiple CCPs supporting the Treasury market. The Committee report notes that a multi-CCP market could lead to increased innovation and more efficient ways to access central clearing. However, there is potential for added complexity and less balance sheet netting. The extension of implementation dates will allow additional time for market participants to fully weigh the considerations of a multi-CCP market.

Many market participants have highlighted the legal and operational costs needed to transition to central clearing, and the potential for a “done-away” clearing model to help address them.

In order to centrally clear transactions, CCP members and their clients enter into clearing agreements that often result in complex and lengthy negotiations. SIFMA and other market participants are working to develop standardized documentation to counter this problem. While standardization would mark important progress, it does not address challenges market participants face in building their operational infrastructure to meet the mandate.

Currently, most centrally cleared transactions are conducted on a “done-with” basis, meaning that the CCP member that executes a trade with a client also serves as the clearing agent for the client, guaranteeing the client transaction to the CCP and operationally supporting its clearing. By contrast, in a done-away transaction, a client would conduct a trade with an executing dealer, but a separate third-party clearing agent that is “away” from the trade would be responsible for submitting the trade to the CCP.

The separation of execution and clearing agent responsibilities is common in derivatives markets, where trades between dealers and their clients are given up to third party agents to submit into clearing.

Many market participants believe done-away clearing would help address issues around legal documentation, operational scalability and clearing costs in the following ways.

These solutions are currently being developed by market participants for a variety of access models, but certain elements will need to be worked out ahead of the implementation dates, including the documentation, fee structure and the capital treatment, among others.

The impact of the rule on global markets is significant, owing both to its design and to the large scale and broad diversity of participants in the U.S. Treasury market.

The rule requires that members of CCPs clear eligible transactions, regardless of where those transactions are conducted around the world. As such, the mandate was designed to ensure eligible transactions in the Treasury market are treated consistently. Rather than being seen as extraterritorial, the rule is best seen as focused on Treasury securities transactions, as an asset class rather than focusing on the location of participants.

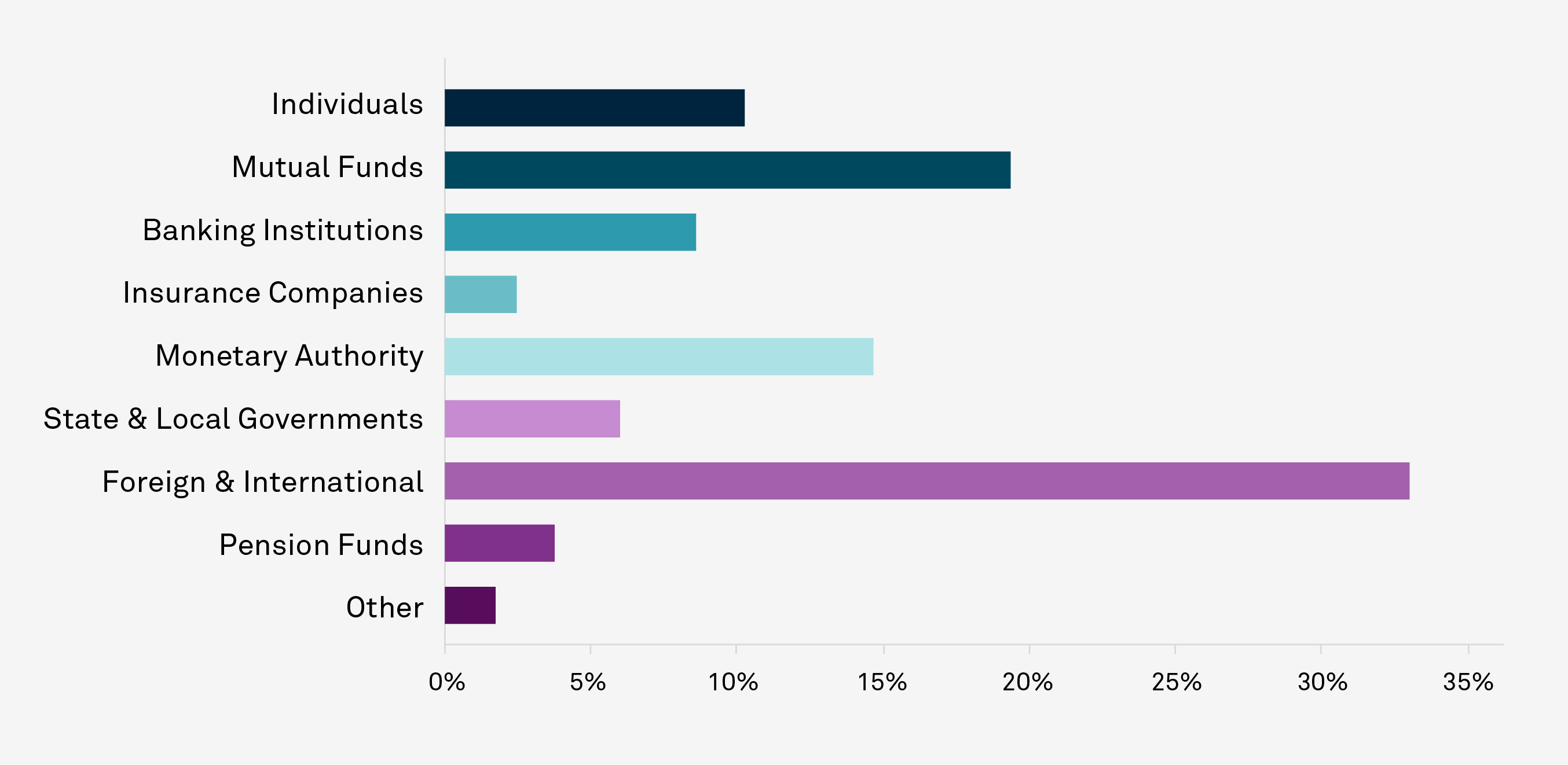

Indeed, participation in the Treasury market is broad. U.S. Treasury securities hold a unique position in global markets, acting as a safe haven for global investors during periods of market volatility and providing a risk-free benchmark for many financial products. This unique role is reflected in the diversity of holders of Treasury securities, with foreign and international institutions holding roughly a third of all outstanding Treasury securities. (Figure 4) International market participants also face unique challenges in adapting to the rule, as the effects of time zone differences and jurisdictional challenges can introduce added complexity to the compliance requirements. Continued industry efforts will be important to help facilitate consistent clearing of global Treasury transactions, including transactions conducted on various collateral platforms, between affiliates and banks and their branches.

FIGURE 4: HOLDERS OF OUTSTANDING U.S. TREASURYS

Source: As of Q4 2024; BNY calculation based on SIFMA data, exclusive of discrepancy representing accumulated valuation difference between issuance and holdings.

The extension in the implementation of the SEC’s central clearing rule will provide additional time for important scoping and implementation issues to be resolved, but the additional time doesn’t mean market participants should take a wait-and-see approach. All participants must continue to prepare for the mandate because the changes to the market will be significant across all dimensions — clearing, collateral, margin and access. The private sector will continue to play an important role in helping to ensure the rule is successfully implemented and partnering with the public sector on this transition will be critical in helping maintain the safety and liquidity of the U.S. Treasury market.

Nate Wuerffel is Head of Market Structure and Product Leader for BNY's Global Collateral Platform

Conor Sari, VP Global Collateral contributed to this article.

1 "Debt to the Penny,” FiscalData, U.S. Treasury Department, June 3, 2025, https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny

2 “Sponsored Membership,” DTCC.com, DTCC, June 2025, https://www.dtcc.com/charts/membership

3 Ibid.

4 “SEC Extends Compliance Dates and Provides Temporary Exemption for Rule Related to Clearing of U.S. Treasury Securities,” U.S. Securities and Exchange Commission, February 25, 2025, https://www.sec.gov/newsroom/press-releases/2025-43

5 “Standards for Covered Clearing Agencies for U.S. Treasury Securities and Application of the Broker-Dealer Customer Protection Rule with Respect to U.S. Treasury Securities,” Sec.gov, Securities and Exchange Commission, December 13, 2023, https://www.sec.gov/files/rules/final/2023/34-99149.pdf

6 BNY triparty data, avg. as of 2H 2024

7 Ibid.

With U.S. Treasury market changes afoot and effective liquidity management more essential than ever, BNY outlines how market participants can leverage these changes to better position themselves for growth.

Understand the growing liquidity challenges in the U.S. Treasury market, the impact of fiscal and monetary policies, and BNY’s role in fostering stability.

The Securities and Exchange Commission's proposal for central clearing will reshape the U.S. Treasury market. Read more about its impact on liquidity and the Treasury market's future dynamics.

Victor O’Laughlen, Executive Platform Owner at BNY Global Clearing, discusses in-house versus outsourcing, and how 2025 will bring about the next step in the industry’s evolution.