Market Movers: More Time, Please

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 9 minutes

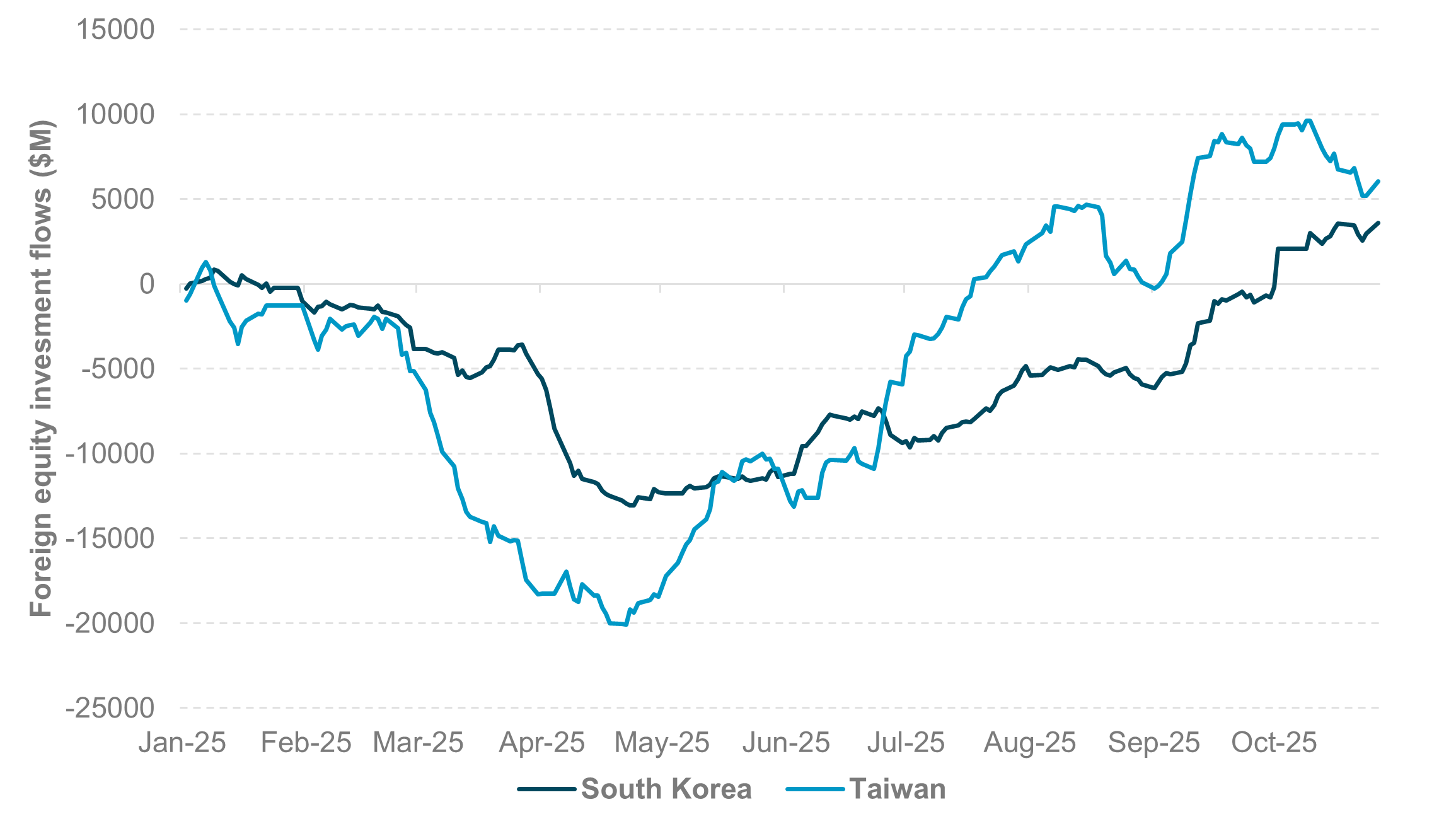

Foreign Equity Investments into South Korea and Taiwan

Source: BNY

Optimism on technology and artificial intelligence had been one of the key supportive factors for APAC equities, especially in South Korea and Taiwan. South Korea’s equity market made a remarkable comeback in 2025, rising over 60% year to date after a nearly 10% sell-off in 2024. The semiconductor sector, which suffered from high-inventory levels in 2024, helped lead the rebound. Foreign investors’ interests in KOSPI had been relatively cautious for most of the year. The recovery in equity flow after the liberation day-triggered sell-off was slow in Korea compared to Taiwan, with KOSPI net year-to-date flows turning positive only in early October, compared to mid-July for Taiwan equities. Interestingly, the recovery of equity flows and prices, along with a less-dovish Bank of Korea, has not benefited the Korean won. The upward move of USDKRW since mid-September has been more than implied by the rebound of the USD, pressured by near-term trade-related uncertainties, particularly surrounding the implementation of Seoul’s $350B investment pledge in the U.S., as well as the on-going concern of high levels of household indebtedness and elevated housing prices, especially in Seoul. We are hopeful that a middle ground will be reached between U.S. and South Korea. This, along with the upward growth momentum, as demonstrated by the stronger than expected Q3 GDP growth of 1.2% q/q, 1.7% y/y, is positive for Korean won. USDKRW is hovering just below 1440 technical levels as we write this.

The Tuesday turnaround in equities requires more time to take hold, as commodities, led by energy and gold, drop on mixed signals about global growth. Risk sentiment wobbled overnight as investors braced for central bank decisions, fretted over Q3 earnings, and watched for new signs of a U.S.-China trade détente. The FOMC is widely expected to cut 25bp on Wednesday, but forward guidance will be key, as easy financial conditions mixed with sticky inflation cloud the 2026 outlook. The European Central Bank and Bank of Japan are both expected to hawkishly hold rates. Job losses remain a significant concern in the U.S., but the lack of harder employment data leaves investors like the Fed flying blind. Big tech earnings in the U.S. tomorrow and Thursday are expected to drive volatility, with Amazon job-cut plans an example. Finally, hopes for a larger trade deal with China remain in focus, but other agreements matter too: Mexico trade discussions face delays, Canada’s new tariffs remain unclear with no new talks set. For the day ahead, the U.S. markets face another set of regional Fed surveys, a $44B 7y coupon sale, and another heavy slate of Q3 earnings. Focus overnight is on USD weakness, which failed to support equities and or lift gold, with prices breaking below $3,900 per ounce. The unwinding, rotational nature of risk trading reflects the heavy month-end pressure to reassess winners across markets. More time may be needed to test the buy-the-dip reaction function into the certainty of rate decisions.

South Korea’s Q3 GDP rebounded sharply to 1.2% q/q, 1.7% y/y from 0.7% q/q, 0.6% y/y in Q2 2025. Private consumption increased 1.3% q/q, driven by higher spending on goods (motor vehicles, communication equipment) and services (restaurants, health). Government consumption also rose 1.2% q/q, mainly due to goods and healthcare benefits. Construction investment slightly declined by 0.1% q/q, while facilities investment surged 2.4%, led by machinery such as semiconductor manufacturing equipment. Exports grew 1.5% q/q, supported by semiconductors and motor vehicles, while imports increased 1.3%, mainly in machinery, equipment and motor vehicles. KOSPI –0.802% to 4042.83, USDKRW +0.423% to 1433.15, 10y KTB –0.2bp to 2.91%.

The Bank of Korea plans to consider additional gold purchases from medium- to long-term perspectives. The last time the bank added to its gold reserves was 2013. Elsewhere, the Philippine central bank will sell some of its “excessive” gold holdings with the precious metal set to retreat further from record highs as safe-haven demand eases. Gold accounts for about 13% of the Bangko Sentral ng Pilipinas’ gross international reserves compared with between 8%–12% of the central bank’s reserves, which stood at about $109B as of September 2025, the most in almost a year.

U.S. August FHFA House Price Index is expected at -0.1% m/m, its fifth monthly decline.

U.S. October Richmond Fed Manufacturing survey is forecast to improve to –10 from –17.

U.S. October Conference Board consumer confidence is forecast to ease to 93.3 from 94.2.

U.S. Treasury sells $95B in 6-week bills, $50B 52-week bills and $44B 7-year notes.

Mood: iFlow Mood continued to normalize with selling pressure in equities equalizing core sovereign bonds. Improving market sentiment may push iFlow Mood to flat and then to positive territory. iFlow Mood is at -0.024.

FX: USD, EUR and GBP posted light outflows against inflows in the rest of the G10. Elsewhere, notable flows were COP and PHP outflows and PEN inflows.

FI: Notable flows were buying in U.S. Treasurys, U.K. gilts and Polish government bonds against selling in Chile and Indonesia government bonds.

Equities: G10 equities were significantly sold, led by Sweden, Eurozone, Australia and the U.S., except for Japanese equities. Equities flow in LatAm and EMEA were mixed, while better outflows pressure was seen in APAC, especially in Korean equities.

“Time is what we want most, but what we use worst.” — William Penn

“Time is the most valuable thing a man can spend.” — Theophrastus

Euro area firms’ median inflation expectations remained at 2.5% for the one-year horizon and at 3% for the three- and five-year horizons. Across size classes, large firms increased their median one-year-ahead inflation expectations to 2.4%, from 2.2% in the previous survey, while small- and medium-sized enterprises (SMEs) continued to report a figure of 2.9%. For the three-year horizon, SMEs did not revise their expectations (stable at 3.1%), while large firms slightly decreased their expectations (to 2.5%, down from 2.6% in the previous survey). SMEs raised their inflation expectations to 3.8% (from 3.2%) for the five-year horizon, while large firms decreased (to 2.7%, down from 2.9%). The balance of risks around their long-term inflation outlook is similar to the previous round. In total, 53% of firms perceived upside risks to their own inflation outlook five years ahead (up from 52%), while 33% perceived risks to be balanced and 14% saw risks to the downside. For both large firms and SMEs, risks remain clearly tilted to the upside. Eurostoxx 50 -0.301% to 5692.06, EURUSD +0.026% to 1.163, BBG AGG Euro Government High Grade EUR –286.2bp to 0%.

Germany’s November GfK consumer confidence dropped from –22.5 to –24.1. The Consumer Climate continues its downward trend, due to German consumers' significantly dampened income expectations in October. In contrast, both economic expectations and the willingness to buy are rising slightly. And, as in the previous month, there is currently almost no change in the willingness to save. In October, income expectations fell by just under 13 points to 2.3 points. This has been the lowest value since March of this year, when –3.1 points were measured. The ongoing tense geopolitical situation, increasing fears of inflation, and again growing concerns about jobs are destroying hopes for a short-term recovery in Consumer Climate. DAX +0.186% to 24284.92, EURUSD +0.026% to 1.163, 10y Bund +0.6bp to 2.632%.

The U.K. October BRC shop price index unexpectedly slowed to 1.0% y/y from 1.4% y/y below the 3-month average of 1.1%. On the month, BRC shop price index was down –0.3% m/m, the first drop since March with a significant monthly decrease in food prices. The annual rate of food price inflation decreased to 3.7% from 4.2% in September. There was a 0.4% monthly drop in food prices, the largest since December 2020. Non-food prices saw a smaller year-on-year decline in September compared to August, indicating a potential end to the drop. Note that the BRC attributed rising prices to factors like global issues and higher costs for retailers, such as National Insurance contributions. FTSE 100 +0.065% to 9642.33, GBPUSD +0.128% to 1.3328, 10y Gilt +0.6bp to 4.438%/.

Italy’s October consumer confidence increased from 96.8 to 97.6. All components improved: future climate (92.6 to 94.1), personal climate (96.0 to 97.0), economic climate (98.8 to 99.3), and current climate (99.9 to 100.2). Business confidence also rose from 93.7 to 94.3. Manufacturing confidence improved from 87.4 to 88.3, supported by better order book assessments (from –19.7 to –19.2) and production expectations (from –0.1 to 1.9), despite a slight decrease in inventory levels (2.7 to 2.3). Construction confidence increased from 101.6 to 103.3, driven by higher order book volume (–3.7 to –2.3) and stronger future employment expectations (7.0 to 9.0). Conversely, market service confidence declined slightly from 95.6 to 95.0, with optimism on future order books (6.2 to 7.1) offset by concerns over business trend (0.2 to –1.2) and order book levels (–0.2 to –1.6). Retail trade confidence rose notably from 101.8 to 105.0, reflecting increased expected sales volume (27.3 to 28.3), improved current business trend (8.1 to 14.5), and reduced stock levels (9.5 to 6.8). FTSEMIB +0.573% to 42730, EURUSD +0.026% to 1.163, 10y BTP –0.5bp to 3.411%.

South Korea's consumer sentiment fell for the second consecutive month in October amid concerns over prolonged negotiations with the U.S. on its new tariff scheme and renewed tensions in Sino-U.S. trade relations. The Composite Consumer Sentiment Index (CCSI) for October 2025 stood at 109.8, 0.3 points lower than that in September. Consumer sentiment regarding living standards and their future outlook were unchanged at 96 and 100, respectively. Consumer sentiment related to future household income and future household spending were both unchanged, at 102 and 110, respectively. Consumer sentiment concerning current domestic economic conditions was unchanged at 91, and that concerning future domestic economic conditions was 94, three points lower than that in September. The expected inflation rate for the upcoming year, the three-year ahead rate and the five-year ahead rate were all the same, at 2.6%. KOSPI –0.802% to 4042.83, USDKRW +0.423% to 1433.15, 10y KTB –0.2bp to 2.91%.

South Korea’s Q3 GDP rebounded sharply to 1.2% q/q, 1.7% y/y from 0.7% q/q, 0.6% y/y in Q2 2025. Private consumption increased 1.3% q/q, driven by higher spending on goods (motor vehicles, communication equipment) and services (restaurants, health). Government consumption also rose 1.2% q/q, mainly due to goods and healthcare benefits. Construction investment slightly declined by 0.1% q/q, while facilities investment surged 2.4%, led by machinery such as semiconductor manufacturing equipment. Exports grew 1.5% q/q, supported by semiconductors and motor vehicles, while imports increased 1.3%, mainly in machinery, equipment and motor vehicles. By sector, manufacturing expanded 1.2% q/q, electricity, gas & water supply rose 5.6%, and services grew 1.3%, led by wholesale & retail trade, accommodation & food services, and finance & insurance. Agriculture contracted 4.8%. On a y/y basis, real GDP increased by 1.7% in Q3 (0.6% in Q2). Exports of goods and services rose 6.0% y/y, with goods exports up 5.0% and services exports up 11.2%. Construction remained weak, down 8.1% y/y. This advance estimate reflects a broad-based recovery in domestic demand and exports, despite ongoing challenges in agriculture and construction sectors. KOSPI –0.802% to 4042.83, USDKRW +0.423% to 1433.15, 10y KTB –0.2bp to 2.91%.

New Zealand’s September adjusted filled jobs rose 0.3% m/m, the best monthly gains since October 2023. It was primarily driven by gains in services industries (+0.4% m/m or 6737 jobs) and good-producing industries (+0.1% m/m, 549 jobs) against losses in primary industries (-0.5% m/m, -534 jobs). On the year, filled jobs were down -0.5% y/y, with construction, manufacturing and professional, scientific and technical services sectors jobs down -4.5% y/y, -1.7% y/y and -2.6% respectively, while jobs gains in healthcare (+1.8% y/y) and education and training (+2% y/y) sectors. NZX 50 +0.083% to 13391.59, NZDUSD +0.14% to 0.5758, 10y NZGB 0bp to 3.999%.

The cost of living for the average New Zealand household, measured by household living costs price indexes (HLPIs), increased 2.4% y/y in Q3 2025 versus 2.6% y/y in Q2 2025. Meanwhile, inflation, as measured by the consumers price index (CPI), was 3.0% y/y in Q3 2025 versus 2.7% y/y in Q2 2025. Breaking this down, mortgage interest payments decreased 15.4% y/y; electricity increased 11.3% y/y; local authority rates increased 8.8% y/y and rent increased 2.6% y/y for the average household in Q3 2025. NZX 50 +0.083% to 13391.59, NZDUSD +0.14% to 0.5758, 10y NZGB 0bp to 3.999%.

Taiwan’s September monitoring indicator increased 4 points to 35. The trend-adjusted leading index increased by 0.07% in September 2025 to 100.22, rising for two consecutive months. The trend-adjusted coincident index decreased by 0.11% in September 2025 to 105.27, falling for two consecutive months. The trend-adjusted lagging index increased by 0.16% in September 2025 to 97.38, rising for three consecutive months. TAIEX –0.159% to 27993.63, USDTWD +0.313% to 30.719, 10y TGB +0.3bp to 1.245%.