Partial Eclipse

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 12 minutes

There were a number of central bank decisions last week, lifting the USD and stocks, but leaving bonds largely untouched. The correlation between markets reflects a partial eclipse of recession thinking for risk takers, but also highlights what Fed Chair Powell has said repeatedly: Decisions will be data-dependent. The risk of labor market weakness outstrips upside inflation fears for now but will come into play in the week ahead. Why the partial eclipse in recession fears? First, the Fed cut 25bp and more rate cuts are likely, but it disappointed the market with just four cuts instead of the six that were priced. But a higher USD didn’t stop equities from going higher. Bonds, however, are well contained. The risk for markets comes from correlation clashes – USD and equities, equities and bonds and how key economic data like inflation dented the credibility of central bankers. The other driver of volatility in the week ahead will be how FOMC speakers see the risks and where they stand as the breadth of dot-plot diversion between governors will continue to lead the rethink of the terminal rate.

Will growth and leverage factors drive markets in the week ahead?

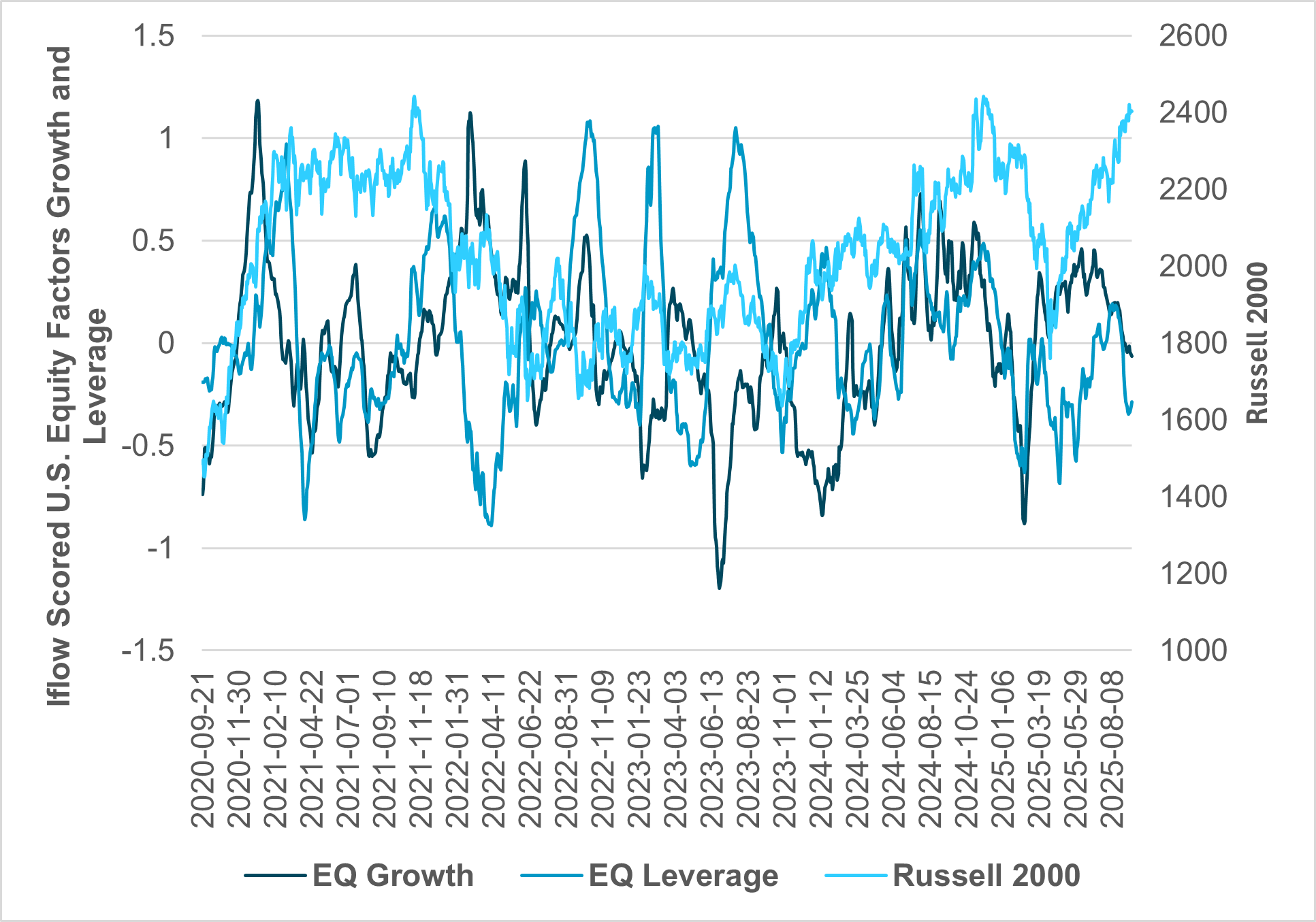

EXHIBIT #1: iFLOW U.S. EQUITY GROWTH AND LEVERAGE FACTORS VS. THE RUSSELL 2000

Source: BNY, Bloomberg

Our take: The Russell 2000 U.S. small cap index reached record highs following the Fed rate hike, suggesting a shift in the investment theme from AI to a broader U.S. recovery. The relationship between our flows and the Russell 2000 reveals negative correlation periods between leverage and peaks in growth. This reflects the business cycle and Fed monetary reactions. We also see a link between low U.S. rates and the Russell 2000 upside.

Forward look: Given the relationship between our flows and Fed easing, there is a bias for rotational trades and more risk-on thinking from investors when it comes to the U.S. This may be counter to the data on jobs and could fall apart if U.S. recession risks come back into focus. At some point the Fed’s insurance cuts may lead to a real claim by consumers for government support as we have seen in other slowdowns that turned into recessions. However, we are not yet at a notable low in our leverage or growth factors, suggesting there is further upside for U.S. equities, particularly in a rotational expansion across sectors and rate-sensitive industries.

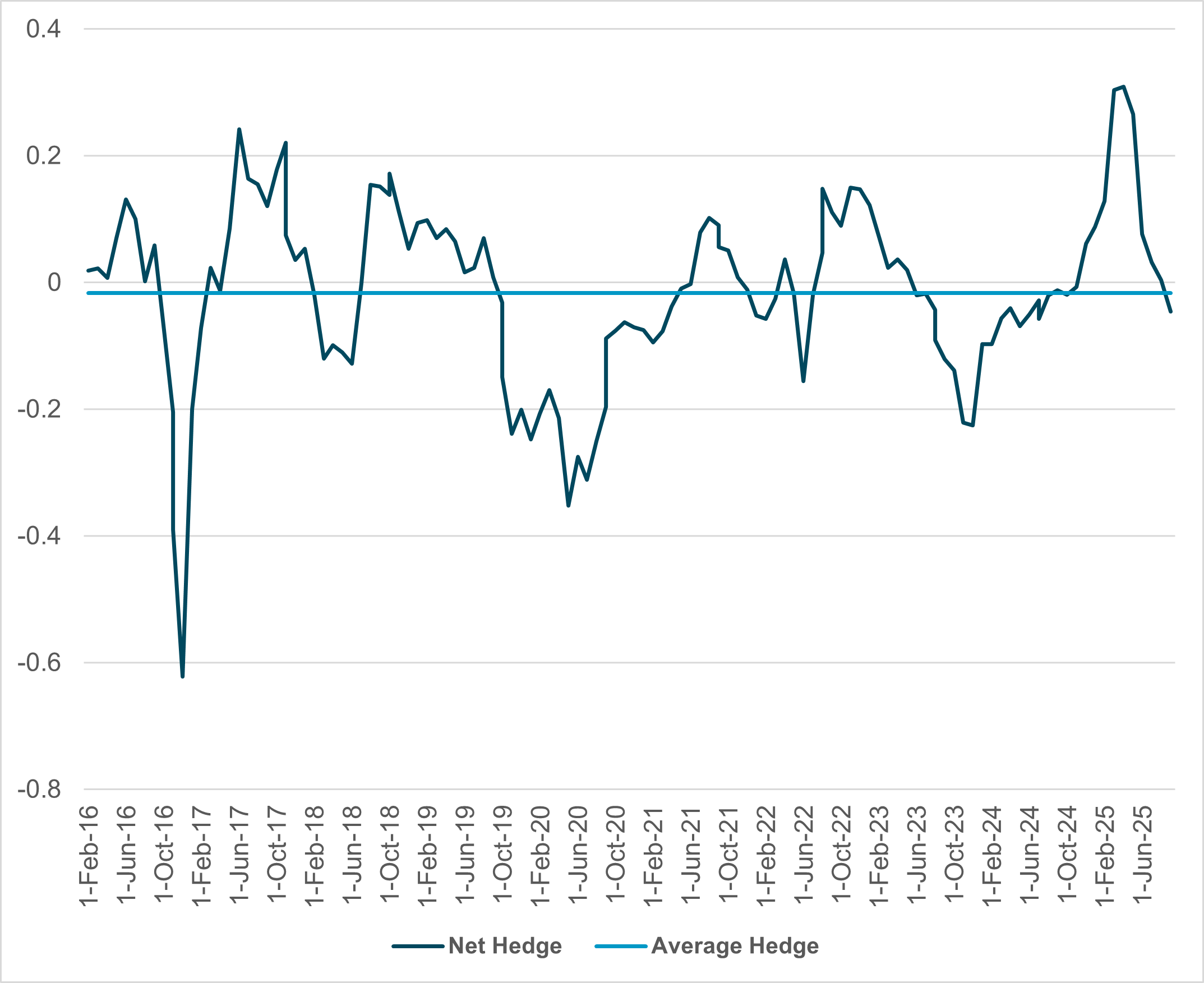

EXHIBIT #2: NET USD HEDGE FOR CROSS-BORDER HOLDINGS OF U.S. ASSETS

Source: BNY

Our take: While USD holdings by foreigners have fallen in 2025, they remain above the 3-year average. The hedging shift for U.S. assets post-“Liberation Day” has been led by fixed income. In Exhibit #2, we refresh our chart on hedging with the key assumption that 80% of U.S. fixed income holdings are the target hedge (based on a 10-year average of our iFlow data) and that equities are 20%. The chart suggests that despite current positions being near the year’s low, there is more room for dollar selling. Adding to this is the price action of the USD after the Fed cuts, with noisy correlations to stocks and bonds.

Forward look: If the cost of hedging is going down and volatility markets are stable, then foreign investors are likely to continue to hedge. The end of Q3 has been a target for investors wanting to catch up on their hedging needs, and the rally in U.S. shares and the outperformance of U.S. bonds should force the issue. The role of growth and leverage in stocks and bonds will be key in the weeks ahead.

U.S. core PCE prices and Fed predictions

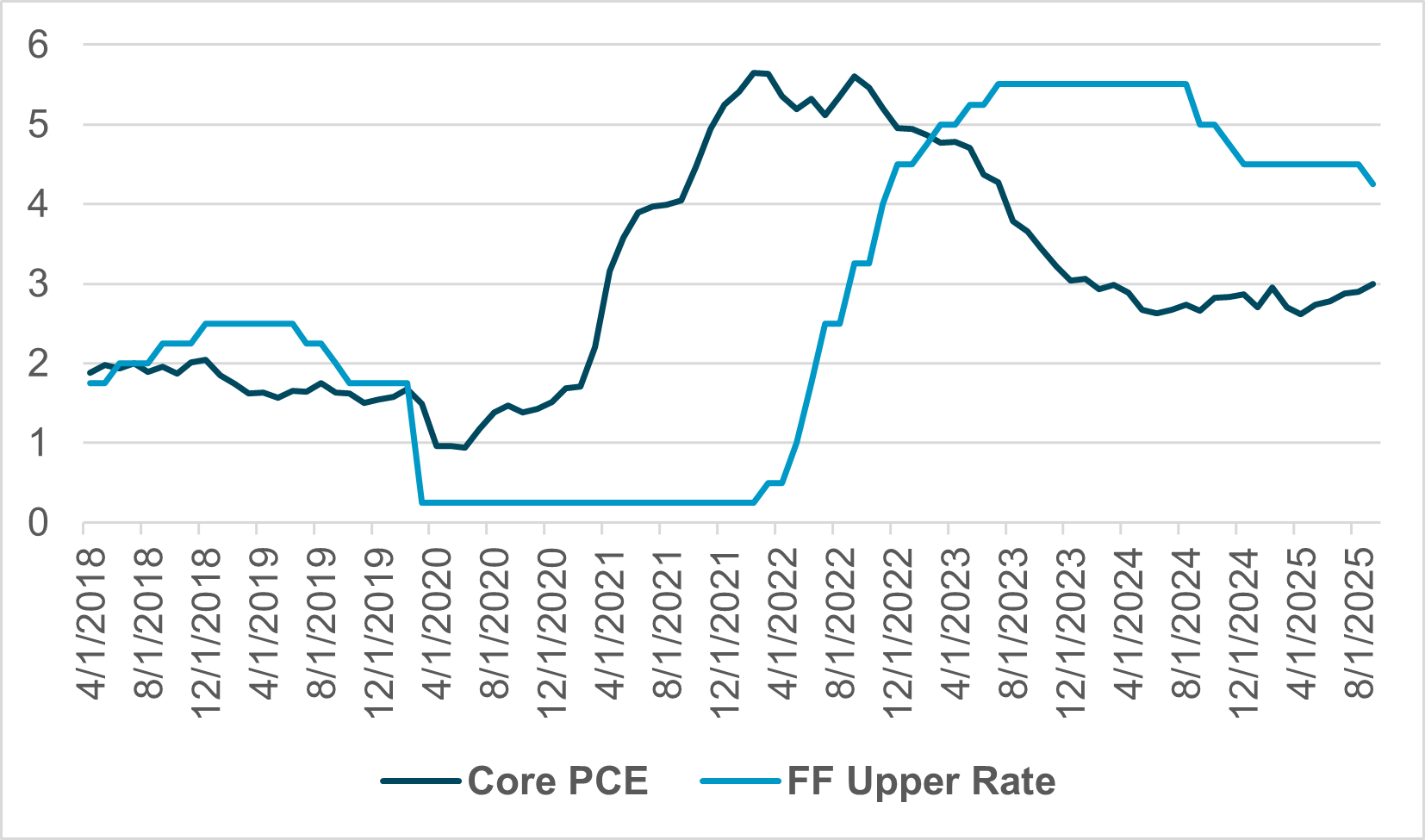

EXHIBIT #3: U.S. CORE PCE INFLATION AND FED RATES

Source: BNY, Bloomberg

Our take: The lack of significant data until Friday’s core PCE inflation release leaves investors open to rethinking Fed rate cuts and the plan ahead. Fedspeakers will be important, with over 18 events planned. Chair Powell speaking Tuesday on the economy is the most important but close attention will also be paid to the Cleveland Fed’s Hammack and the St. Louis Fed’s Musalem given their more hawkish view prior to the September 17 rate cut. The short-end coupon supply will also be a focus for investors given the view that the government will continue to front-load borrowing. The tension of $500bn+ in borrowing from bills to notes next week along with further IG issuance may test demand. Of the economic data that could surprise the U.S. markets, advance trade should be the focus given the risks of larger imports despite tariffs and lower exports despite a weaker USD. Durable goods and new homes sales are important but unlikely to shift growth and inflation thinking.

Forward look: The recession watch risk will continue to make the weekly jobless claims report and any forward-looking surveys important to investors as they balance the path of Fed cuts against the need for further easing against inflation risks. Inflation hurts the bottom 33% of U.S. consumers more than the top 10%. The week ahead should also see a redoubled focus on Q3 earnings outlooks as equity markets reach new highs, and valuations will require higher earnings to maintain momentum. For bonds, the role of mortgages and the housing market may be the next theme as cuts by the Fed may not spark enough new building or buying. Refinancing rose notably in the last two weeks in anticipation of Fed easing, but this trend will require even more cuts and spread narrowing in order to continue. The slowdown in jobs and lower-end wages should force renewed bifurcation on sub-prime risks.

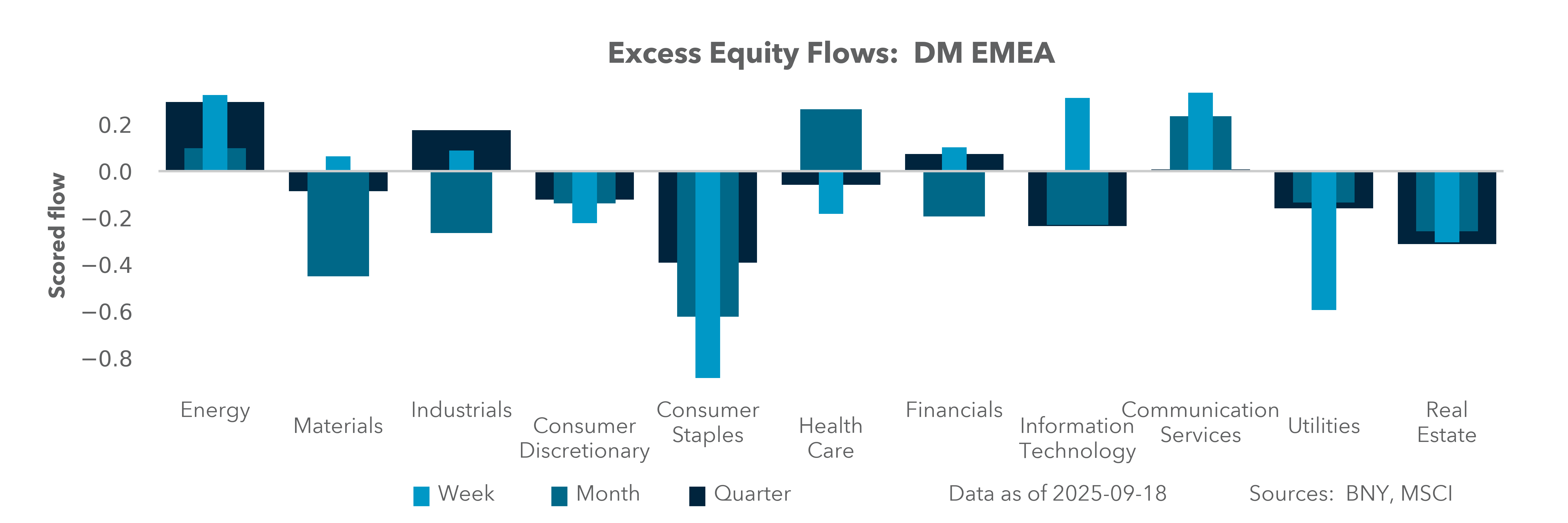

EMEA: SNB and Riksbank seek to hold the line

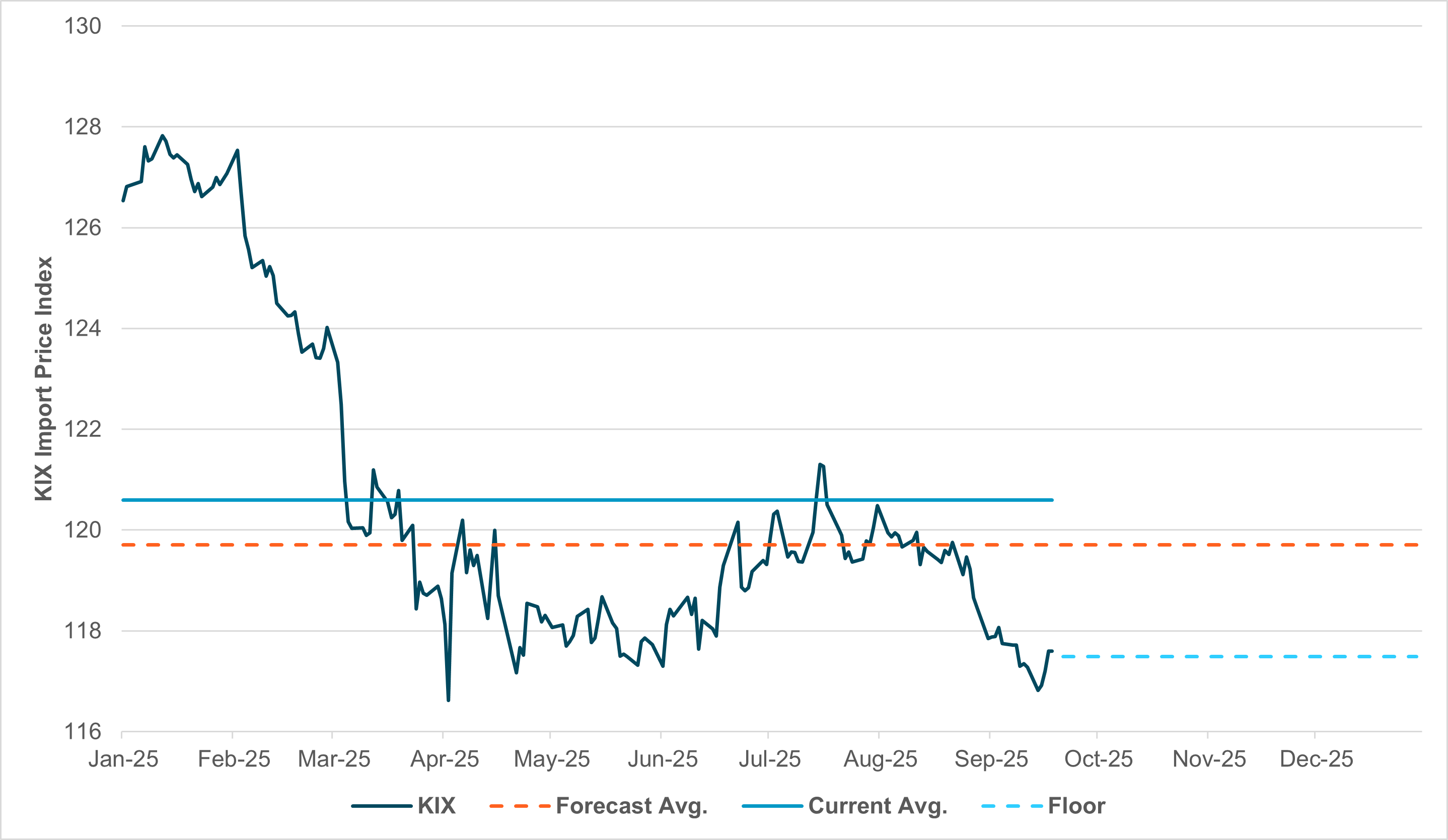

EXHIBIT #4: SWEDEN IMPORT PRICE INDEX (KIX) CLOSE TO RIKSBANK’S FORECAST “FLOOR”

Source: BNY, Sveriges Riksbank

Our take: The Riksbank and SNB decisions in the week ahead will be a test case of how far high-surplus economies in Western Europe can deviate from the ECB. As the euro remains very well-valued and the latest projections indicate tolerance for EURUSD as high as 1.24, arguably there will be enough easing through the exchange rate channel to limit stronger disinflation in the Swiss and Swedish economies. This means that domestic elements can feature strongly, and despite the current challenges we would agree with market pricing that rate cuts are unlikely in both.

Since the surprising breakdown in trade talks between the U.S. and Switzerland and the imposition of 39% tariffs on the latter, Swiss data have shown clear signs of deterioration, and further franc strength would we unwelcome. Nonetheless, the SNB’s relatively narrow inflation mandate is clear and the current leadership is clearly not inclined to move toward unorthodox measures unless data confirm that deflation risks becoming entrenched. The June decision – made before the trade news – did indicate an improvement in inflation outcomes through their forecast horizon. The bottom line is that unless deflation is signaled in the new conditional inflation forecast, there is scope for the SNB to avoid more aggressive moves. The franc’s nominal effective exchange rate is firm, but inflation differentials are moving in the SNB’s favor, i.e., providing enough of an offset to limit deflation risk. Furthermore, although the news flow has been limited, we believe talks are ongoing between the two sides and our base case remains some form of resolution which would help stabilize growth expectations and allow re-acceleration in activity data.

In contrast, the Riksbank’s tolerance for further SEK appreciation may prove more limited and this will be a factor behind the policy outlook for the rest of the year. Core inflation is high enough to limit additional cuts, but the central bank’s own KIX import price (a stronger SEK equates to a lower KIX) index is now at the limits (Exhibit #4) of forecasts provided in the last monetary policy report (MPR). Currently at 117.60, the annual average has now fallen to 120.59, versus the forecast of 119.7 which would result in 2.0% annual average inflation for this year, and 1.7% next year, based on the June MPR. Further SEK appreciation risks pushing the currency below the same 117.60 average expected for 2026, which would almost certainly lead to CPI falling closer to 1.5% y/y, which would constitute a clear break from the mandate. Although there is a case for long-term valuation attractiveness, the pace matters and the Riksbank can ill afford another near 50bp cumulative cut for 2025 and 2026 combined trend price growth forecasts in one quarter.

Forward look: After a summer of considerable hedging interest in the dollar which has extended into the Fed decision, we expect asset allocators to reassess their FX exposures and acknowledge that transatlantic rate differentials may have peaked. The risk to inflation is to the downside via the pass-through channel for the ECB and the Riksbank, while the latest borrowing numbers out of the U.K. mean significant fiscal contraction is needed in Q4, which will affect growth further and may prompt the BoE to act earlier than expected. Comparatively, cross-border investors are more under-hedged in GBP, SEK and CHF, and this is where we see greater risk-reward for tactical dollar consolidation.

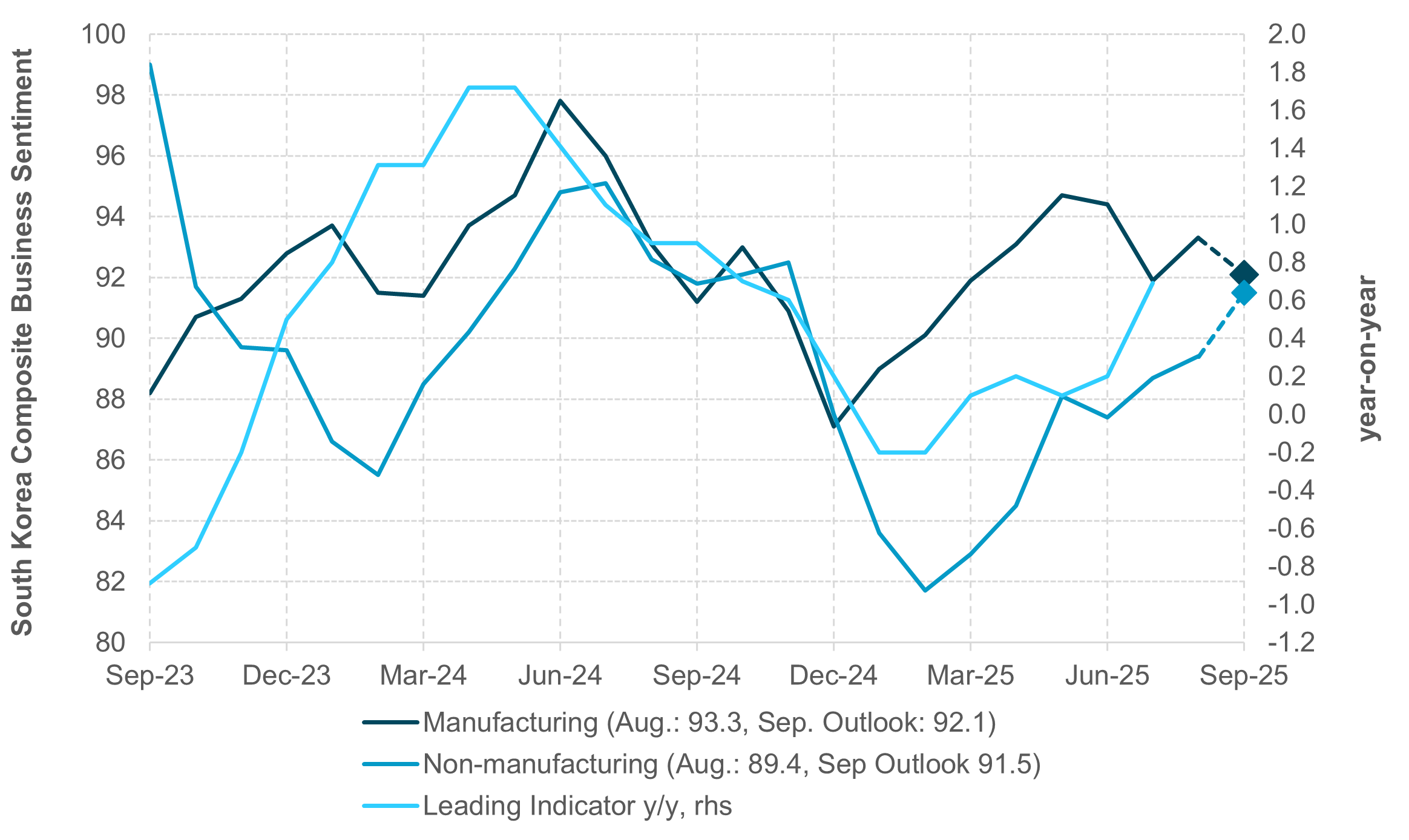

APAC: Growth and inflation in focus

EXHIBIT #5: SOUTH KOREA COMPOSITE BUSINESS SENTIMENT INDEX

Source: BNY, Bloomberg

Our take: In the Asia-Pacific region, this week’s economic data releases will center on sentiment, exports and inflation indicators. Japan, Australia and India are scheduled to publish their September PMI manufacturing figures, while South Korea will release updates on consumer confidence and business sentiment. Additionally, South Korea, Taiwan and Thailand will report their latest export and trade statistics, and inflation data is expected from Tokyo (Japan), Malaysia, Singapore and Australia. China’s data calendar is relatively light, focusing primarily on loan prime rates, which are expected to remain unchanged at 3.0% for the one-year period and 3.5% for the five-year period.

Forward look: Asia's macroeconomic indicators are expected to remain volatile due to ongoing disinflation risks from low crude oil prices and uncertainties around export recovery, aside from consistent performance in the semiconductors and chips sector. Regional downside growth risk appears limited, with support from loosening fiscal policies and monetary policy easing. Regional equities have seen positive movements, driven by AI and technology investment trends, renewed foreign inflows and increased asset allocation from developed to emerging markets, as indicated by iFlow data. The recent market correction occurred as indices reached new highs, which is considered within normal market fluctuations. At this stage, current trends do not indicate technical extremes. There is a noted divergence between economic data and asset prices, warranting continued monitoring of capital flows for any sudden changes in foreign investment patterns. Upcoming factors include India’s Q4 issuance plan (October 2025 to March 2026), potential measures in Thailand to address THB strength, Japan’s LDP leadership election on October 4, 2025, and the 4th plenary session of the 20th Communist Party of China Central Committee in October, which will focus on discussing the next five-year plan.

Global markets are entering a pivotal phase, with central bank decisions, shifting growth expectations and evolving capital flows are colliding. The Fed’s cautious rate-cut path has lifted both the USD and equities, while bonds remain contained, highlighting unusual cross-asset correlations. Equity performance, particularly in small caps, signals a potential broadening beyond AI-led gains, suggesting a more cyclical recovery theme. Meanwhile, foreign investor hedging dynamics and EMEA/Asia central bank positioning will shape FX and fixed income allocations. Looking ahead, sustained monitoring of labor markets, inflation prints and global trade flows will be essential to navigate risks and capture rotational opportunities.

Central bank decisions

Sweden, Riksbank (Tuesday, September 23) – The Riksbank is expected to keep rates on hold at 2.0% as it will focus on anchoring core inflation, which continues to run at relatively high levels, though there are some initial signs of a slowdown in the wake of August’s contraction. Headline prices are also contracting materially but some relief may arise from current EUR valuations in the wake of the latest ECB decision. We still see a high chance of the Riksbank moving independently of the ECB, especially if the KIX continues to weaken (arising from SEK strength). There is no longer any margin for error as this year’s inflation forecast is sitting at 2.0%, while the 2026 outlook is at 1.7% and risks slipping into strong disinflation in short order, especially with the external outlook remaining uncertain. Governor Thedéen indicated at the August decision that it was “appropriate” to signal some probability of a rate cut, and this should remain the case irrespective of the impact of the ECB’s move.

Hungary, MNB (Tuesday, September 23) – The National Bank of Hungary is expected to keep rates unchanged at its upcoming meeting. Inflation held at 4.3% y/y in August, unchanged from July, with consumer prices flat on a monthly basis. Despite progress compared with the double-digit inflation of 2023, the rate remains above the NBH’s 2–4% target band. The base rate stands at 6.5%, where it has been since late 2024, and policymakers recently reiterated that tight conditions must remain until disinflation proves durable. They highlight risks from volatile energy markets, wage growth and food prices, which could reignite price pressures. The NBH has also noted that although growth momentum is weak, premature easing would risk undermining inflation credibility. As such, the central bank is widely expected to hold rates steady through September, with cuts unlikely until inflation shows a clear and sustained return to the tolerance band supported by credible forecasts.

Czechia, CNB (Wednesday, September 24) – The Czech National Bank is expected to keep the two-week repo rate at 3.5% on September 24. August headline inflation eased to 2.5% y/y, while core inflation edged up to 2.8%, and the Bank has described the structure of price pressures – especially food and services – as unfavorable. The CNB’s September communications report that all respondents in its August financial market survey expect an unchanged decision at the next meeting. Recent official messaging has also cautioned against further cuts for now, noting that the prevailing policy stance, together with the exchange rate, is broadly neutral. The central bank has confirmed that all seven Bank Board members will attend the meeting. Overall, the combination of near-target headline inflation, slightly firmer core readings and guidance from the CNB supports expectations for a hold while it gauges progress toward the 2% target.

Switzerland, SNB (Thursday, September 25) – The Swiss National Bank is expected to keep rates on hold despite the significant pick-up in economic headwinds since the June decision. Contrary to expectations, Switzerland failed to reach a trade agreement with the U.S. and now faces the highest level of tariffs, at 39%, among developed markets. Further risks surrounding pharmaceutical and bullion exports are of existential risk to Switzerland’s trade surplus, while the former industry is also a crucial source of economic value-added. Data is showing clear sign of deterioration, and we have calibrated our franc view to some extent, but for now fundamentals are manageable and SNB President Schlegel recent noted that the bar for additional easing is “high.” We believe the SNB will stay on hold for now, barring material downside revisions in the conditional inflation forecast, but if U.S. tariffs are permanent, then a reassessment will be necessary.

Mexico, Banxico (Thursday September 25) – The Bank of Mexico is expected to keep the policy rate at 7.75% at its meeting on September 25. August headline inflation rose slightly to 3.57% y/y, while core inflation was about 4.2%, keeping underlying pressure above the 3% target midpoint. Banxico’s late-August quarterly report noted that inflation projections were revised up for the coming quarters and that convergence to the 3% target is still anticipated around the third quarter of 2026. The Board also emphasized that policy will remain focused on consolidating disinflation and anchoring expectations, with the inflation risk balance still tilted to the upside. iFlow indicates ongoing interest in adding to Latin American FX exposure and Banxico’s real rate buffer is clearly conducive for MXN performance, especially with the updated Fed trajectory. However, we still favor duration as the better expression as the dollar’s soft positioning situation and limits to additional easing in pricing could generate a broader tactical recovery.

Data Calendar

Event Calendar