Wednesday’s September FOMC, 25bp and what else?

Published on Tuesdays, Short Thoughts offers perspectives on U.S. funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

Published on Tuesdays, Short Thoughts offers perspectives on U.S. funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

John Velis

Time to Read: 5 minutes

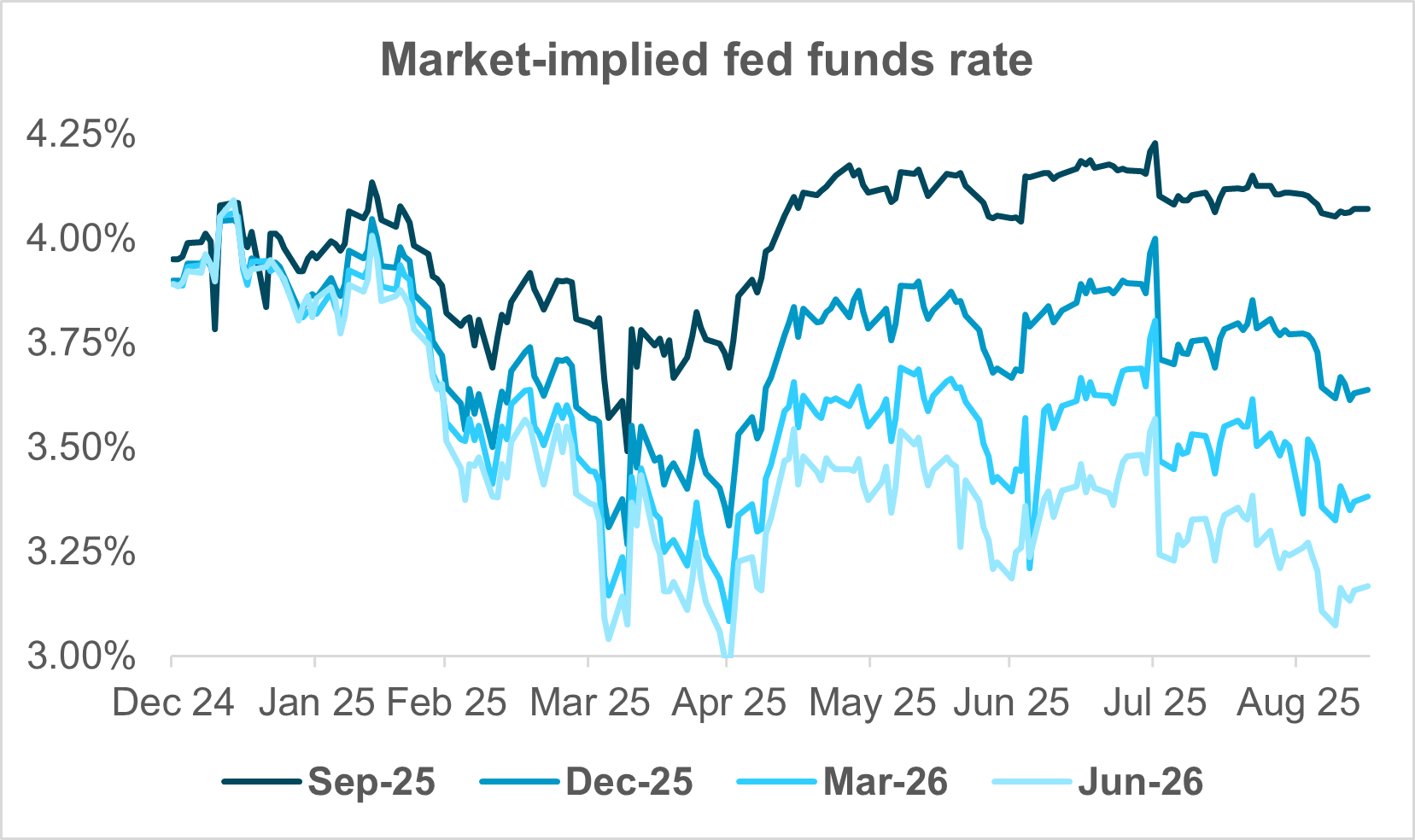

EXHIBIT #1: A SERIES OF RATE CUTS PRICED IN

Source: BNY Markets, Bloomberg

The Fed will cut rates 25bp on Wednesday, and the Summary of Economic Projections will add a third quarter-point rate cut for the end the year (up from the two cuts seen in June’s SEP). We don’t expect a 50bp cut, nor do we expect – despite the dots – the Fed to signal that an October cut is a fait accompli, adding some hawkish undertones to the meeting. As we pointed out in last week’s publication (see here), rate cuts this autumn, starting with this meeting, would have the Fed cutting rates even while inflation is running well over the 2% target. This doesn’t seem to concern the markets, which continue to price in a series of rate cuts well into next year.

Let’s start with the dots. In the June SEP, the median 2025 projection envisioned two rate cuts this year (assuming 25bp for each). It wouldn’t take more than one or two contributors to move their dots lower for this quarter’s SEP to arrive at the three cuts we expect to be signaled. To mitigate against the market keying in on this anticipated change, we expect Chair Powell to point out – as he is wont to do at his press conferences – that the dots don’t represent a plan or a forecast but rather a representation of the collective view of the Committee given the outlook.

We note that these cuts are largely fully priced in the market now, as Exhibit #1 shows. In addition, if the dots are indeed lower for 2025, we would expect that the projections for unemployment will have to rise from June’s 4.5%. Finally, we don’t have a high conviction view on 2026 and would not be surprised if the Committee as a whole feels the same way. In this regard, a wide dispersion of 2026 dots is not unlikely, and we don’t think the market will read too much into next year’s projections.

Turning to the expected rate cut and how it is characterized, we first will look at the statement, which we expect to note the weakening in the labor market. At the July meeting, the statement was changed to assert that economic growth had moderated (from earlier statements asserting that the economy was expanding at a solid pace). How much alarm the Fed expresses about the economy and weakening jobs growth will be interesting, especially given the expected rate cut. However, if it also raises concerns about inflation, which is stubbornly high and potentially still grinding higher in coming months, it would highlight a degree of caution about a locked-in extended cycle. This is something we expect Powell to point out in his press conference, likely softening any overly dovish read of the meeting.

EXHIBIT #2: SHORT-TERM INFLATION EXPECTATIONS REMAIN HIGH

Source: BNY Markets, Bloomberg

We noted last week that inflation expectations were elevated, and we reprise the chart of 1- and 2-year inflation swaps from last week in Exhibit #2. Furthermore, survey data also show higher expectations in both the short and long term. Expect the Chair to point this out, and this to be brought up at the meeting, something we won’t know for sure until the meeting minutes are published in three weeks’ time. But this is where we think the hawkishness, and the lack of an overt pre-commitment to an October cut, will temper a positive market reaction, despite the dots and current market pricing.

The goals of the Fed’s dual mandate are in “tension” (Powell’s word) and are likely to become more so going forward. Add in the growing politicization of the Fed, and things are getting complicated for the central bank. This is likely to lead to rising risk premia in the bond market, and with an extensive cutting cycle currently (already) priced in, we don’t expect yields to fall much across the curve in reaction to Wednesday’s meeting.

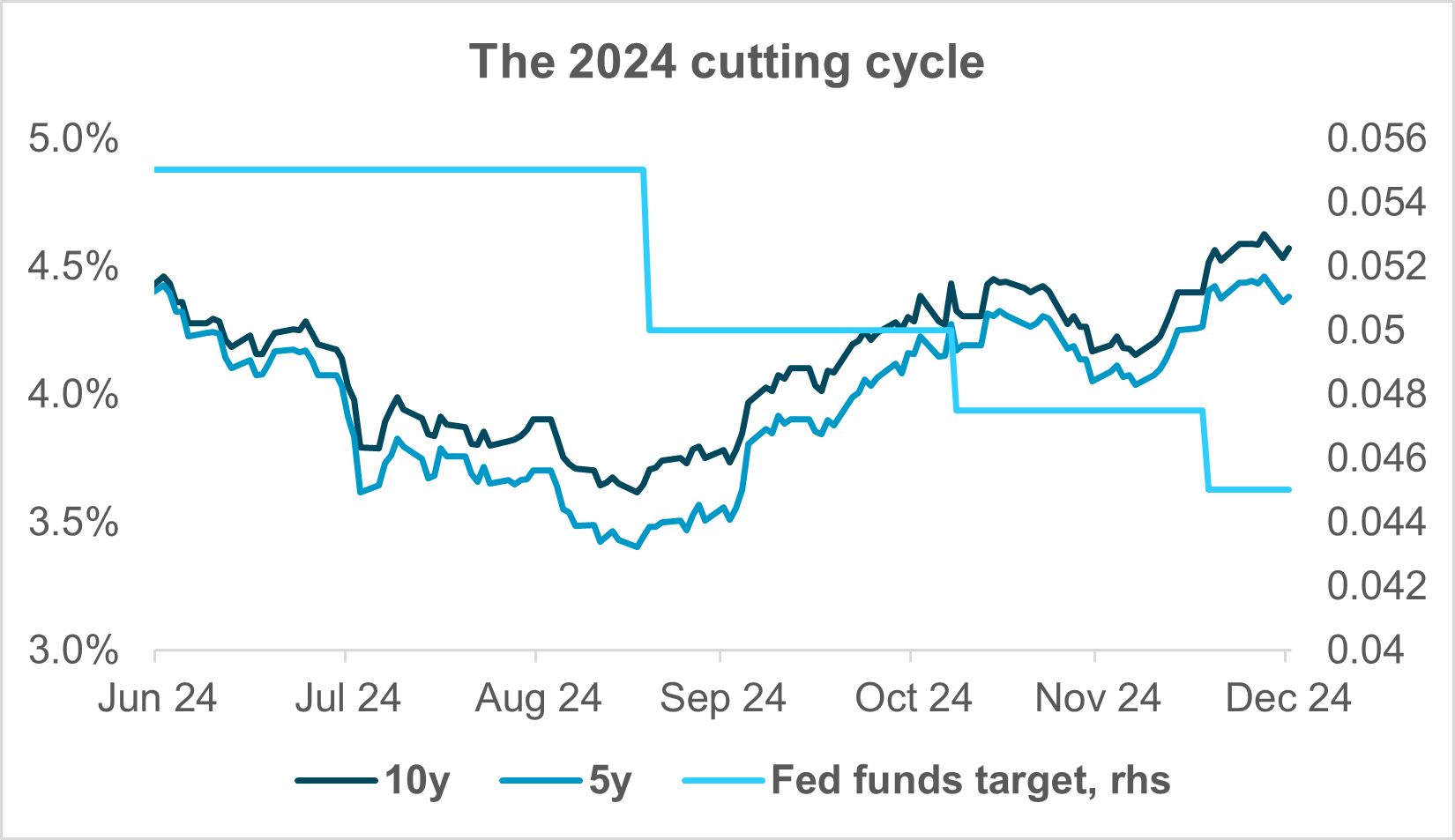

EXHIBIT #3: LAST YEAR’S CUTS DIDN’T LEAD TO LOWER YIELDS

Source: BNY Markets, Bloomberg

On this point, we note in Exhibit #3, that a year ago, after the Fed kicked off its (short) cutting cycle with a 50bp cut, 5y and 10y yields actually rose, and we wouldn’t be surprised if that is case this time as well. If it looks like the Fed is – even just temporarily – allowing inflation to run at or over 3% y/y, the 10y could easily back up from where it is now, although not necessarily on the heels of this particular meeting. Rather, it would be due to a perceived erosion of Fed credibility on inflation, even if the jobs market declines. Stagflation and a central bank in the crosshairs politically would be an effective recipe for rising term premia in rates markets.

Finally, we are keeping an eye out for dissents. If, as we expect, the Fed opts for 25bp rather than 50bp, we wouldn’t be surprised to see dissents in favor of a larger cut. If, as appears likely, current Council of Economic Advisors Chairman Miran is confirmed in time to fill the seat vacated by Adriana Kugler, he would likely dissent in favor of 50bp. There could be others as well. In the other direction, although this year’s committee makeup is rather dovish, we could see a dissent in favor of keeping rates steady as well. This means we could see dissents in different directions, putting further pressure on monetary policy.

This is a crucial meeting and much will be revealed on Wednesday. We’re not sure the market will know what to make of multiple dissents; a dovish statement, but a potentially hawkish press conference; and high inflation with a cooling labor market. This is why we’re not ready to make a pronouncement with high conviction on the future path of policy. For now, however, we think labor market concerns will translate into three cuts this year, with 2026 presenting a much murkier picture.