Could We Be in the Final Days of QT

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

iFlow > Short Thoughts

Published on Tuesdays, Short Thoughts offers perspectives on US funding markets, short-term Treasuries, bank reserves and deposits, and the Federal Reserve's policy and facilities.

John Velis

Time to Read: 4 minutes

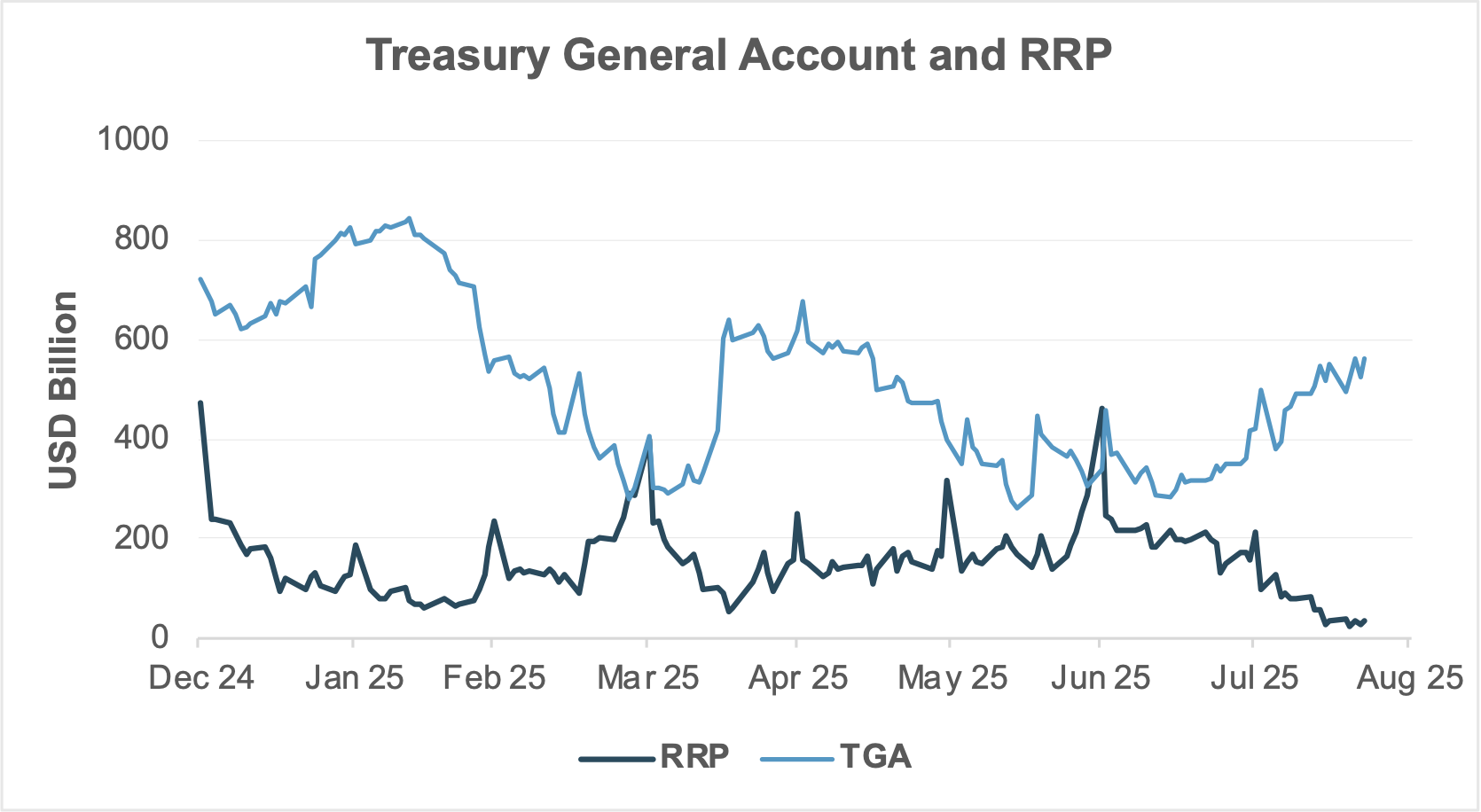

EXHIBIT #1: TGA INCREASES AS RRP DECLINES

Source: BNY Markets, U.S. Department of Treasury, Federal Reserve Bank of New York

Perhaps lost amid the focus on Federal Reserve Chair Powell’s Jackson Hole speech on Aug. 22 and subsequent market reaction was renewed focus by the Federal Open Market Committee (FOMC) on the balance sheet and market liquidity heading into September. The July meeting minutes, published just one and a half days before Powell’s remarks, drew less scrutiny given the timing of the two events. Nevertheless, we think there is a good chance the Fed will soon address the risks of further reserve reduction and explore contingencies, such as suspending its balance sheet runoff.

According to the minutes, the Fed expects that a combination of ongoing quantitative tightening (QT), T-bill issuance tied to rebuilding the Treasury General Account (TGA), and dwindling use of the overnight reverse repurchase agreement (RRP) facility is “likely to bring about a sustained decline in reserves for the first time since portfolio runoff started in June 2022.” We wrote about this recently. Furthermore, the minutes report that on certain days, such as period-end, tax payment dates or large Treasury settlement dates, reserves could “dip temporarily to even lower levels.”

The July FOMC meeting was the first since the Republican budget bill passed and increased the debt limit, allowing the Treasury to resume debt issuance, primarily T-bills. The TGA, which had fallen to about $300bn at the end of June, is slated to return to its desired level of $850bn in September. In addition, RRP facility use remains low as cash is deployed into a T-bill market that is heavy with issuance. With an additional $20bn per month in balance sheet runoff, the Fed justifiably considered this issue in its July meeting and highlighted it in the minutes. Exhibit #1 shows the evolution of the TGA and the RRP this year.

In its discussion of these potential liquidity developments, the Fed didn’t appear alarmed and expressed confidence that any disruptions to liquidity could be addressed with existing tools. Chief among them is the standing repo facility (SRF), which was last used significantly at the end of Q2 when it was tapped for $11bn on June 30. As noted in the minutes, “If such events created pressures in money markets, the Federal Reserve's existing tools would help supply additional reserves and keep the effective federal funds rate within the target range.”

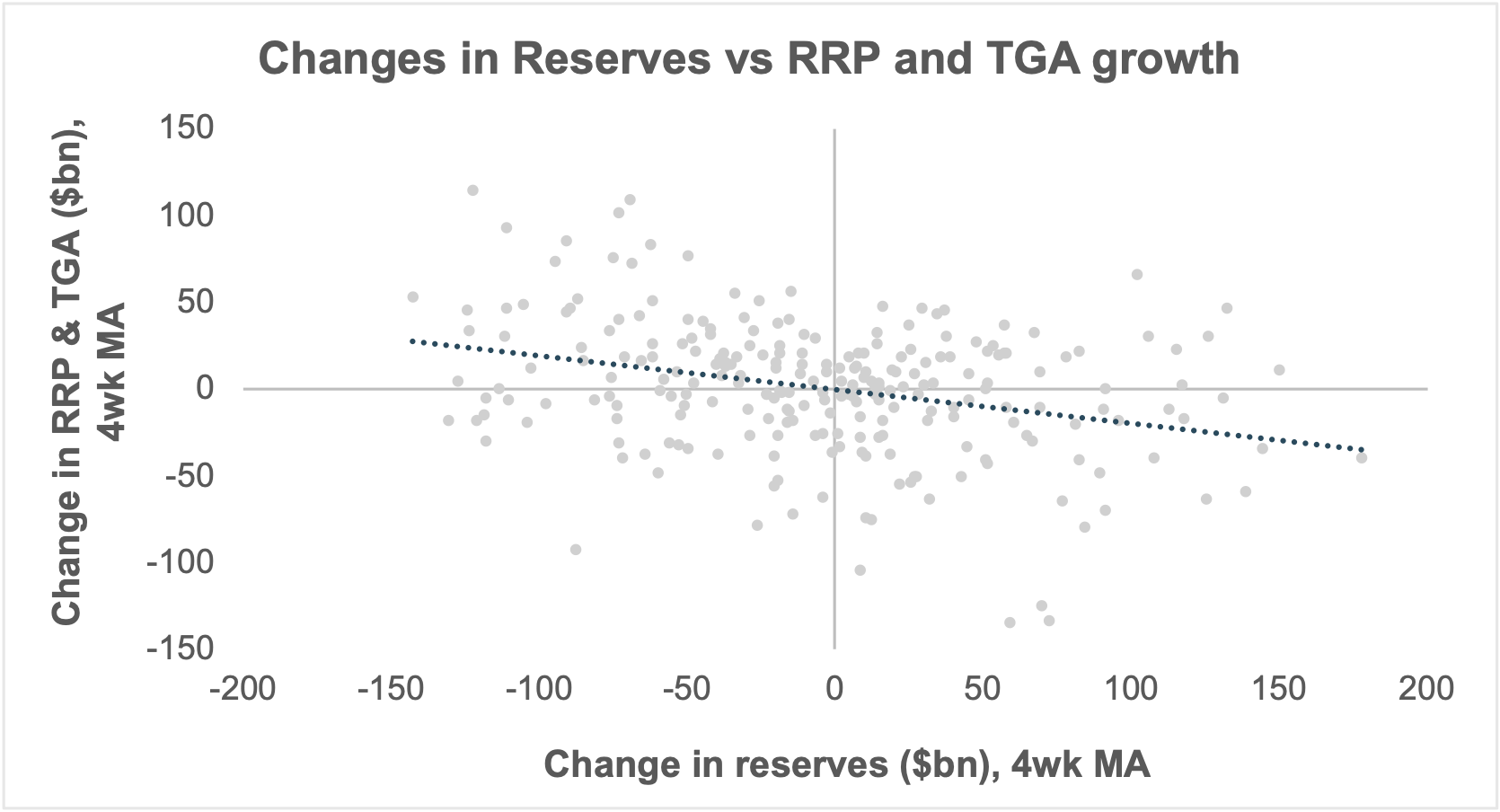

EXHIBIT #2: RESERVES SET TO FALL AS TGA RISES AND RRP DWINDLES

Source: BNY Markets, U.S. Department of the Treasury, Federal Reserve Board of Governors

RRP usage is nearly zero, while bill supply continues to expand. Since mid-July, more than $500bn in T-bills have been net issued, largely snapped up by money market funds (MMFs), which now hold more than $7.5tn in assets. Exhibit #2 shows the combined weekly changes in the TGA and the RRP (four-week moving average) compared with weekly changes of reserves. There is a clear negative relationship between these two series.

The Fed appears alert, though not alarmed, by this risk. Roberto Perli, the New York Fed’s balance sheet manager, noted even before the debt ceiling was addressed that this process was likely to unfold. On May 22, Perli acknowledged that “as the size of the Fed balance sheet continues to decline, however, and as reserves transition from abundant to ample levels, upward pressure on money market rates is likely to increase … it does imply that, in the future, the SRF is likely to be more important for rate control than it has been in the recent past.”

This implication raises the question of when reserves will transition from abundant (as currently characterized) to merely ample. In a recent speech on the same topic, Fed Governor Christopher Waller suggested that $2.7tn in reserves would be the lowest comfortable level, or “roughly ample”. He based this estimate on September 2019, when money market stresses were severe and reserves were only 7% of GDP. Adding a few percentage points as a buffer produced Waller’s estimate, as he describes in the speech.

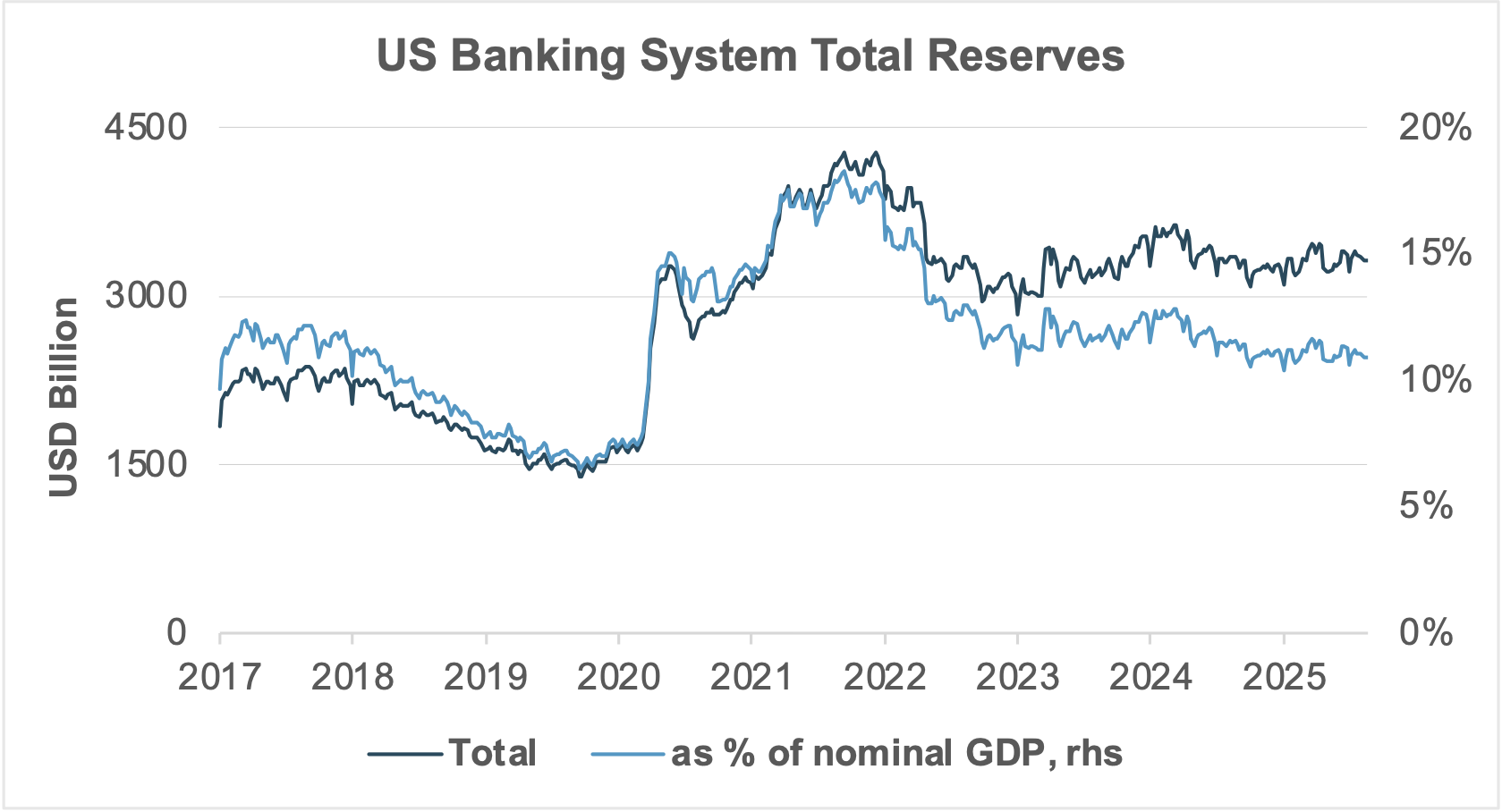

EXHIBIT #3: RESERVES STILL ABOVE SEPTEMBER 2019 LEVELS

Source: BNY Markets, Federal Reserve Board of Governors, Bureau of Economic Analysis

Exhibit #3 shows the level of reserves holding steady at about $3.3tn, or nearly 11% of nominal GDP. Indeed, reserves fell sharply in 2019, prompting the Fed to suspend QT and supply $250bn in liquidity. We can make a comforting argument that we are both well above the 7% level seen during that period, and the SRF can be tapped for up to $500bn, double the amount required in special facilities six years ago.

Forward look

One way to avoid this risk, while also easing policy, would be for the Fed to suspend QT altogether. At its March FOMC meeting, the Fed slowed the runoff of Treasury securities from $25bn per month to $5bn, while keeping the mortgage-backed securities portion of runoff steady at $35bn. The move was intended to “provide meaningful insurance” against the possibility of a funding squeeze. More insurance could be appropriate.