Market Movers: Stall Speed

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

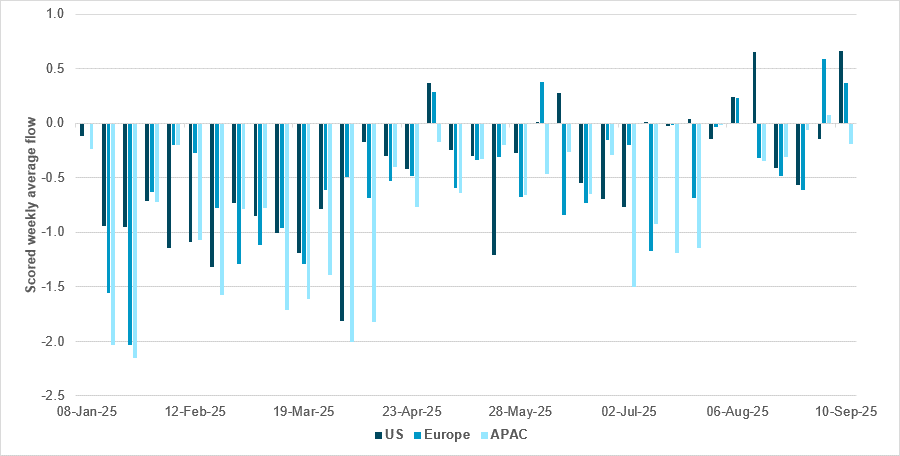

Global credit market flow at 2025 highs

Source: BNY

Global credit markets are now seeing their strongest performance this year. In the run-up to the ECB decision, European junk bond CDSs fell to their lowest level since January 2022, underscoring strong demand for yield as investors move down the risk spectrum. While the ECB is seen holding rates unchanged for the year, the Fed is poised to accelerate easing with three cuts priced in by year-end, fueling robust demand for credit. U.S. corporate bond flows are now at 2025 highs, recovering from a weak Q1 and mixed Q2, though conviction remains soft amid two-way activity. With equity valuations high and inflation sticky, credit has become the fallback option. European inflows remain weaker overall but have improved since July, despite ECB easing being priced out; this highlights the appeal of low absolute yields. Strong equity performance has likely pushed asset allocation into credit, while France’s political volatility has not sparked outflows and sovereign-financial links in the Eurozone remain muted. In APAC, sentiment has improved as weakness in Chinese property fades and equities show gains. The region has just posted its best week of the year, though it still trails the U.S. Low yields across major economies justify sustained flows, while equities support sentiment. However, Japanese corporates remain a risk given front-end hikes and curve steepening, though expectations of policy adjustments under a new government may lend support into year-end.

Markets are ending the week in a conflicted state, with equities and bonds mixed around the world. The worries over slowing growth and higher inflation are hanging over all markets. The U.S. equity market hit new record highs after weaker jobless claims (the worst since 2021) added to Fed easing expectations, even though inflation was back at January’s highs. U.K. GDP for July stalled at 0%, leaving the three-month average at 0.2% q/q; this saw the FTSE down 0.4% and GBP down 0.3%. Overnight, the focus on risk revolved around U.S. calls for the G7 to impose higher tariffs on China and India over their Russian purchases. JPY was not helped by the U.S. and Japan spelling out FX policy; the race to become the next prime minister was instead the main driver, with reports Shinjiro Koizumi plans to run for leadership of the LDP on October 4. French markets lagged on political worries, the performance of health care shares and the Fitch rating decision later today. French OATs are 3-4bp higher, as are U.S. yields. Markets’ stall speed matches views on the global economy. Optimists see a glide path to a soft landing, while pessimists are worried about a more difficult landing. For the day ahead, the University of Michigan Sentiment Survey is expected to reflect a focus on the U.S. consumer and the headwinds of prices against the tailwinds of policy shifts. Few see this changing sufficiently to shake out positions ahead of next week’s FOMC meeting. The bar-belled approached to risk is about to change, as cash loses its yield. This will put emerging markets center stage in relation to how investors see Fed easing. Indian CPI data today and Jair Bolsonaro’s conviction in Brazil yesterday highlight the divergent risks, as the two countries’ yield premiums face their own stalling out, with global commodities and domestic demand central to how we end the week.

The U.S. and India are nearing agreement on a trade deal, according to Sergio Gor, President Trump’s nominee for ambassador, though tensions over India’s Russian oil purchases persist. Trump imposed 50% tariffs on India in August, half as a penalty for energy imports seen as financing Russia’s war in Ukraine. Washington is pressing New Delhi to halt these purchases, with Commerce Secretary Howard Lutnick linking a deal to that condition, while India insists it will continue buying oil. Despite the friction, trade talks are ongoing, with Indian negotiators set to meet U.S. trade representative Jamieson Greer. Gor called India a top priority and highlighted strong defense ties, while also reaffirming U.S. commitment to the Quad alliance. SENSEX +0.486% to 81945.15, USDINR -0.143% to 88.3138, 10y INGB -0.9bp to 6.458%.

ECB officials presented diverging views on interest rate policy following the central bank’s decision to leave rates unchanged for a second meeting. Bank of France Governor Francois Villeroy de Galhau stressed that another rate cut cannot be ruled out, citing downside inflation risks. By contrast, Cyprus’s Christodoulos Patsalides said current rates are appropriate and no further easing is needed unless significant developments occur, even noting the possibility of rate increases if warranted. Latvia’s Mārtiņš Kazāks and Lithuania’s Gediminas Šimkus urged maintaining flexibility, citing persistent uncertainty and risks to inflation from global trade tensions, geopolitical factors, currency strength and energy regime changes. While the decision itself was unanimous, post-meeting remarks revealed a broad spectrum of views within the Governing Council, reflecting an uncertain economic outlook. Euro Stoxx 50 -0.312% to 5369.99, EURUSD -0.052% to 1.1728, BBG AGG Euro Government High Grade EUR -2.7bp to 2.911%.

Germany’s August inflation rate was confirmed at 2.2% y/y, slightly higher than July and June’s 2.0%. The harmonized index stood at 2.1% y/y. On a monthly basis, both indices rose 0.1%. Energy prices fell y/y for a fourth consecutive months (-2.4%), with substantial drops in light heating oil (-5.2%), firewood and pellets (-3.5%) and electricity (-1.7%), though natural gas was up 0.7%. Food prices increased by 2.5% y/y, with dairy and eggs (+3.2%) and meat (+2.9%) higher, while vegetables (-1.1%) and oils and fats (-1.3%) fell. Services prices rose 3.1% y/y, led by combined passenger transport (+11.1%). Excluding food and energy, core inflation remained elevated at 2.7%, unchanged from the previous two months. DAX -0.227% to 23649.89, EURUSD -0.052% to 1.1728, 10y Bund +2.7bp to 2.684%.

U.K. July GDP was flat m/m, following +0.4% in June and -0.1% in May. On a three-month basis, GDP grew 0.2% in the period to July compared with the three months to April, slowing from 0.3% in June and 0.6% in May. Services rose 0.4% in the latest three months and 0.1% in July, remaining the main driver of growth. Construction expanded by 0.6% in the three months to July and 0.2% in July, though this was slower than in June. Production output shrank 1.3% over the three-month period and fell 0.9% in July, marking its second consecutive quarterly decline and offsetting gains in other sectors. FTSE 100 +0.344% to 9329.58, GBPUSD -0.273% to 1.3537, 10y gilt +0.7bp to 4.613%.

U.S. September preliminary University of Michigan consumer sentiment is expected to ease to 58 points, from 58.2. The one-year inflation expectation is projected at 4.7% y/y from 4.8%, while 5-10y inflation is expected to ease to 3.4% from 3.5%.

Mood: iFlow Mood has normalized further, led by a further reduction in demand for core sovereign bonds, against steady demand for equities.

FX: Notable outflows in TRY, ILS, SGD, MXN and USD against broad inflows in the rest of the iFlow universe. HUF, HKD, KRW, THB, JPY and PLN posted the most inflows. Within the G10, USD and SEK were sold, against buying in the rest, led by JPY.

FI: Demand for Eurozone government bonds, U.K. gilts and U.S. Treasurys continued, followed by Colombia and China. Polish government bonds were most sold.

Equities: Asset allocation out of developed markets into emerging markets continues. European, Swiss and Colombian equities were significantly sold, while strong buying was seen in Brazil, Peru and South Africa. Within developed markets, the industrials and consumer staples sectors were most sold, against buying in the communication services sector.

“The number one reason conversations stall out is that you are not listening well enough.” – Max Weiss

“You avoid stalling out in your career by never losing momentum.” – Austin Kleon

U.K. goods imports rose £2.7bn or 5.4% in July 2025, driven by increases from both EU and non-EU countries. Goods exports increased £1.9bn or 6.6% over the same period, also supported by higher trade with both regions. Exports to the U.S., including precious metals, rose £0.8bn in July but remain below pre-tariff levels. In the three months to July, the total goods and services trade deficit widened by £0.4bn to £10.3bn, as imports grew faster than exports. The goods trade deficit expanded £3.0bn to £61.9bn, while the services trade surplus rose £2.6bn to £51.6bn. FTSE 100 +0.344% to 9329.58, GBPUSD -0.273% to 1.3537, 10y gilt +0.7bp to 4.613%.

U.K. production output fell 1.3% in the three months to July 2025, the weakest three-monthly performance since December 2023. The decline was driven mainly by manufacturing (-1.1%), alongside electricity and gas (-5.1%) and mining and quarrying (-1.8%), partly offset by water supply and sewerage (+1.6%). Manufacturing’s fall was broad-based, with nine out of 13 subsectors contracting, marking its first three-month decline since January 2025. On a m/m basis, production was down 0.9% in July after rising 0.7% in June and falling 1.3% in May. The monthly downturn reflected falls in manufacturing (-1.3%) and mining and quarrying (-2.0%), offset by gains in electricity and gas (+2.0%) and water supply (+0.8%). Total construction output is estimated to have grown by 0.6% in the three months to July 2025.

U.K. services output rose 0.4% q/q in the three months to July 2025, with 10 out of 14 sectors expanding. The strongest contributions came from human health and social work activities (+1.5%) and professional and scientific activities (+1.2%), while wholesale and retail trade (-1.3%) was the largest drag. On a monthly basis, services grew 0.1% in July, following +0.3% in June and +0.1% in May. Seven sectors recorded growth in July, led by transportation and storage (+1.4%) and human health and social work (+0.4%). These were partially offset by declines in six sectors, including information and communication (-0.7%) and administrative and support services (-0.6%).

The U.K.’s August 2025 Bank of England/Ipsos survey showed respondents estimated current inflation at 4.8%, up from 4.7% in May. Median expectations rose to 3.6% for one year ahead (3.2% previously), 3.4% for the following year (3.2%) and 3.8% for five years’ time (3.6%). Most respondents (by a margin of 69% to 6%) thought faster price rises would weaken the economy. Views on the inflation target shifted, with 38% saying it was “about right” (41% in May), 33% “too high” and 13% “too low.” Interest rate perceptions were mixed: 35% saw rates rising y/y; 35% expected falls. Looking ahead, 33% expected rates to rise, 26% to hold steady and 29% to fall. Net satisfaction with the Bank’s performance dropped to 2% from 6%.

France’s August CPI rose 0.4% m/m and 0.9% y/y, after +0.2% m/m and +1.0% y/y in July. The slowdown reflected weaker service prices, up 2.1% y/y after +2.5%, particularly in transport (-1.9% vs. +3.7% previously). Energy prices fell 6.2% y/y, less than July’s -7.2%, with petroleum products down 3.6% and electricity sharply lower again at -13.6%. Food inflation was stable at +1.6% y/y, with fresh food at +1.7%. Manufactured goods prices fell 0.3% y/y, following -0.2% in July. Core inflation slowed to 1.2% y/y from 1.5%. The harmonized index (HICP) rose 0.5% m/m and 0.8% y/y, confirming earlier estimates. CAC40 -0.432% to 7789.69, EURUSD -0.052% to 1.1728, 10y OAT +3bp to 3.473%.

Italy’s Q2 2025 labor market recorded rises of 0.2% q/q and 1.7% y/y in total hours worked. Employment was stable at 24.17 million, with declines in permanent (-21,000) and temporary employees (-45,000) offset by growth in the self-employed count (+74,000). The employment rate remained at 62.6%, with gains for women, older workers and the South, and declines for men, under-50s and the North. Unemployment and inactivity rates held steady at 6.3% and 33.0%, respectively. Employee positions in industry and services rose by 0.4% q/q and 1.7% y/y, while agency work fell 1.7% q/q and on-call contracts increased by 1.9% q/q. Labor costs rose 0.6% q/q and 3.6% y/y. FTSEMIB -0.316% to 42298.39, EURUSD -0.052% to 1.1728, 10y BTP +2.6bp to 3.478%.

Spain’s August CPI was unchanged m/m and rose 2.7% y/y, the same rate as in July. Core inflation, excluding unprocessed food and energy, increased 0.3% m/m and stood at 2.4% y/y, up one-tenth vs. the previous month. The harmonized index of consumer prices (HICP) also recorded 0.0% m/m and 2.7% y/y, stable from July. These results confirm that both headline and harmonized inflation held steady, while underlying inflation registered a slight acceleration. IBEX 35 -0.407% to 15250, EURUSD -0.052% to 1.1728, 10y Bono +2.4bp to 3.255%.

Czechia’s July 2025 current account showed a deficit of CZK 14.9bn, with a goods and services surplus of CZK 18.1bn and dividend outflows of CZK 31.1bn on the primary income balance. Net capital outflows on the financial account totaled CZK 10.8bn, as assets rose by CZK 78.8bn and liabilities by CZK 68.0bn. Foreign direct investment recorded a net inflow of CZK 10.7bn, mainly in the form of debt instruments, while portfolio investment posted a net inflow of CZK 39.7bn, led by domestic long-term debt securities issuance. Other investment registered a net outflow of CZK 19.1bn, and international reserves increased by CZK 43.5bn due to transactions. Prague SE -0.126% to 2290.95, EURCZK +0.005% to 24.351, 10y CZGB +0.5bp to 4.35%.

Türkiye’s July export unit value index rose 4.7% y/y, with increases of 10.5% for food, beverages and tobacco, 4.7% for manufactured goods (excluding food, beverages and tobacco), and 0.9% for crude materials (excluding fuels), while fuels fell 6.1%. The export volume index rose 6.0% y/y, led by fuels (+17.9%) and manufactured goods (+9.6%), while food, beverages and tobacco declined by 9.1%. The import unit value index rose 0.4% y/y, with food, beverages and tobacco up 11.2% and fuels down 8.8%. The import volume index increased by 5.0% y/y, with fuels up 6.5% and manufactured goods up 7.6%. Terms of trade improved to 92.2 from 88.4 a year earlier. BI 100 -0.536% to 10327.2, USDTRY +0.105% to 41.3703, 10y TGB +13bp to 32.91%.

Japan’s manufacturing production capacity index rose 0.1% m/m to 96.0 in July, though it declined 1.7% y/y. By sector, capacity increased in production machinery (+1.3%), electronic parts and devices (+2.0%) and iron and non-ferrous metals (+0.2%), while transport equipment (-1.0%) and ceramics, stone and clay products (-0.3%) posted falls. The operating ratio index dropped 1.1% m/m to 102.0 and was down 0.5% y/y. Broken down by sector, transport equipment (-7.7%), ceramics and stone products (-5.1%) and chemicals (-2.1%) declined, while electrical and information communication machinery (+6.7%), production machinery (+4.9%) and iron and non-ferrous metals (+1.9%) improved. The overall machinery industry operating ratio slipped 1.3% m/m, while non-machinery manufacturing was nearly flat. Nikkei +0.892% to 44768.12, USDJPY +0.381% to 147.77, 10y JGB +1.3bp to 1.594%.

New Zealand August card spending rose 0.4% m/m (July: 0.6%), with rises of 0.7% m/m, $45mn (July: 0.2%) for retail and 0.9% m/m ($55mn) for core retail industries. Looking into the details by retail spending category, hospitality was up $21mn (1.4% m/m), with durables up $8.9mn (0.5%), consumables up $7.1mn (0.3%), apparel up $5.9mn (1.8%), fuel down $0.5mn (-0.1%) and motor vehicles (excluding fuel) down $1.7mn (-0.9%). NZX 50 -0.009% to 13227.9, NZDUSD -0.318% to 0.5957, 10y NZGB -2.4bp to 4.274%.

New Zealand August BusinessNZ Manufacturing PMI was back in contraction at 49.9 after a brief month in expansion zone in July (52.8), as industry struggling to regain its footing after an extended period of contraction through 2023 and 2024. Two of the five main sub-index values were in expansion during August. They were led by new orders (55.2), which encouragingly continues to trend upwards, reaching their highest level of activity since August 2022. Deliveries of raw materials (50.5) also remained in expansion, although down from July. In contrast, production (46.6) fell 6.7 points vs. July, while employment (49.1) and finished stocks (47.1) also recorded contractions.

China’s August 2025 financial statistics showed M2 at ¥331.98tn, up 8.8% y/y, with M1 at ¥111.23tn (+6%) and M0 at ¥13.34tn (+11.7%). From January-August, RMB loans rose ¥13.46tn to ¥269.1tn (+6.8% y/y), led by enterprises and public institutions (+¥12.22tn), while household loans rose by ¥711bn. Total deposits reached ¥329.96tn (+8.8% y/y), with RMB deposits at ¥322.73tn (+8.6%); household deposits rose ¥9.77tn and non-bank financial institutions ¥5.87tn. Interbank rates eased, with average lending at 1.40% and pledged repo at 1.41%, both down 5bp m/m, while turnover rose 16.8% y/y to ¥202.68tn. Cross-border RMB settlement totaled ¥1.47tn, including ¥1.11tn in goods trade and ¥0.61tn in direct investment. CSI 300 -0.572% to 4522, USDCNY +0.062% to 7.123, 10y CGB -0.5bp to 1.802%.