Market Movers: Setback

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Geoff Yu, Wee Khoon Chong

Time to Read: 11 minutes

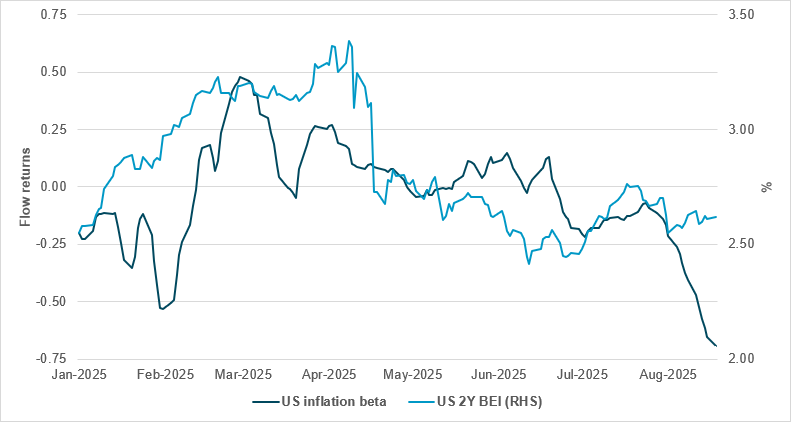

STABLE BREAKEVEN INFLATION NOT HELPING INFLATION-BASED FLOWS

Source: BNY

The U.K. inflation data released overnight provide yet another indication of prevailing stagflation trends globally. Equity markets are generally resilient, but the distribution of equity flows at present does not indicate any marginal gains in preference for inflation protection. For example, in environments in which inflation fears are rising, the energy industry is viewed as offering a degree of inflation protection due to its high correlation with rising prices. If we determine that equity flows are chasing industry groups highly correlated with inflation and shunning those that are less correlated to inflation, then we can reasonably conclude that equity investors are searching for inflation hedges. Using our iFlow Equity styles model, we look at the regression coefficient (beta) between surge flows of industry groups and the industry groups’ correlation with two-year breakeven inflation. This correlation has now reached its most negative level this year, indicating that investors are least interested in sectors whose performance is more highly correlated with two-year breakeven inflation. Such behavior is very different compared with previous rounds of inflation gains, where equity investors strongly added to sectors that normally perform well amid higher inflation. Tech/communication services concentration is a key factor, but equity allocators risk severe imbalances in portfolio construction relative to the inflation cycle.

Sentiment remains tentative, as the tech and AI narrative shows some signs of cooling. Prior single-name and sector leaders in market performance have seen multi-day declines, as a cloudier earnings outlook begins to catch up with lofty valuations. As global central bankers descend on Jackson Hole, where the inflation or stagflation narrative is set to dominate, markets may have little choice but to position for somewhat tighter financial conditions until the September FOMC meeting suggests otherwise. The prospect of a slowdown in easing cycles is equally prominent in Europe, as inflation surged to an 18-month high in the U.K. In Sweden, the Riksbank held rates unchanged and admitted that “developments have deviated” from its June outlook, and specifically that “inflation... has risen more than expected.” While there is some validity in attributing these outcomes to summer seasonality, most developed market central banks will acknowledge that progress on bringing prices and expectations back to target has slowed. Meanwhile, growth outlooks continue to weaken and monetary and fiscal capacity to provide an offset remains constrained. Some greater insight into how the Fed is approaching the growth vs. inflation balance of risks is due when the minutes from the July Fed meeting are released later today. Inflation was characterized as “somewhat elevated” in the Fed statement from the meeting, yet there were two dissenting voices advocating for a 25bp cut. Markets will be looking at their rationale and whether the macro arguments have strengthened enough to convert additional voting members over the coming weeks.

ECB President Christine Lagarde stressed that ECB staff will factor the implications of the EU-U.S. trade deal into September projections, which will guide upcoming policy decisions. She said the global economy had remained resilient in early 2025 despite trade tensions, with IMF data showing Q1 growth 0.3 percentage points above April projections, largely due to frontloading ahead of tariff hikes. While a trade policy uncertainty index has halved since April, it remains above historical averages. Lagarde noted the euro area economy outperformed in Q1 on strong exports – particularly pharmaceuticals to the U.S. – plus firm consumption and investment, with unemployment steady at 6.2% in June. However, she warned growth slowed in Q2 and will likely moderate further in Q3, with the EU-U.S. trade deal imposing effective tariffs of 12-16% on euro area goods. Euro Stoxx 50 -0.313% to 5466.12, EURUSD -0.078% to 1.1638, BBG AGG Euro Government High Grade EUR -1.4bp to 2.885%.

The U.K.’s July CPI rose 3.8% y/y (consensus: 3.7% y/y), accelerating from 3.6% in June and increasing 0.1% m/m, compared with a 0.2% fall a year earlier. CPIH rose 4.2% y/y, up from 4.1% in June, and was flat m/m, unchanged versus July 2024. Core CPI increased 3.8% y/y from 3.7%, with goods inflation rising to 2.7% from 2.4% and services inflation up to 5.0% (consensus: 4.8%) from 4.7%. Core CPIH eased slightly to 4.2% y/y from 4.3%, as goods inflation picked up to 2.7% from 2.4% while services held at 5.2%. Transport, particularly air fares, contributed most to the upward movement, partly offset by lower housing and household services costs. Retail prices also surged by 0.4% m/m (consensus: 0.1% m/m). FTSE 100 -0.207% to 9170.24, GBPUSD +0.06% to 1.3499, 10y gilt -1.9bp to 4.721%.

Sweden’s policy rate was left unchanged at 2% in August, as the Riksbank assessed that inflation, which rose more than expected over the summer and is slightly above target, was mainly driven by temporary factors. Despite the deviation from June’s forecast, the overall outlook was seen as largely intact, with the Executive Board noting weak economic activity, subdued household spending and a labor market yet to show clear improvement. Conditions for recovery remain, supported by earlier rate cuts and higher real wages, but progress is sluggish. The Riksbank maintained vigilance on inflation risks while signaling that there is still some probability of another rate cut later this year. OMX -0.525% to 2645.91, EURSEK -0.014% to 11.1719, 10y Swedish GB +0.9bp to 2.501%.

The RBNZ cut its headline rate by 25bp to 3%. The vote was not unanimous, with two members voting for 50bp. The overall tone of the meeting was dovish, with the RBNZ highlighting that “there is scope to lower OCR further.” This was supported by a broad 25-30bp cut in the OCR projection, which shows the OCR bottoming out at 2.55% in Q1 2026, from a previous forecast of 2.85% in May. Inflation projections were mixed, with inflation projected to drop faster than expected, dipping below 2% in H1 2026 (1.9%, compared with a May forecast of 2.2-2.3%) before drifting above 2% for most of 2027. NZX 50 +1.103% to 13071.3, NZDUSD -1.29% to 0.5817, 10y NZGB -10.8bp to 4.383%.

Bank Indonesia (BI) unexpectedly cut interest rates by 25bp to 5%. This is the first back-to-back interest rate cut since July 2020. Bank Indonesia see 2025 GDP above the mid-point of the 4.6-5.4% projection and is maintaining a dovish bias. It will continue to monitor the scope for further rate cuts based on the two-year inflation outlook, especially for core inflation. Elsewhere, BI sees the current account deficit at -0.5% to -1.3% of GDP, inflation at 1.5-3.5% and lending growth at 8-11% in 2025. It also plans to continue its triple intervention strategy in spot, onshore and offshore domestic non-deliverable forwards (DNDFs). JCI +1.002% to 7941.761, USDIDR +0.154% to 16270, 10y IDGB -0.8bp to 6.406%.

U.S. Treasury to sell $65bn in 17-week bills and $16bn 20y bonds.

U.S. MBA mortgage applications.

FOMC minutes for July meeting, providing details on the Fed discussion where both Governor Chris Waller and Michelle Bowman dissented, voting for a 25bp rate cut.

Central bank speakers: Fed Governor Christopher Waller speaks at Wyoming Blockchain Symposium. Fed Vice Chair for Supervision Michelle Bowman speaks about fostering new technology in the banking system at Wyoming Blockchain Symposium. Atlanta Fed President Raphael Bostic participates in moderated conversation on the economic outlook.

Mood: iFlow Mood drifted further into the risk-off zone to early-May levels. Demand for core sovereign bonds picked up, while equity flows remained neutral.

FX: Currency flows were biased to the sell side and moderate in magnitude. THB, HKD and CHF posted the most outflows. Inflows were focused on TWD, ZAR and CNY, followed by light buying in JPY and EUR.

FI: Peru and Indonesia government bonds, U.S. Treasurys and U.K. gilts posted the most buying, while Israel, Mexico and Norway government bonds were most sold.

Equities: G10 equities were sold, led by Canada, Europe, the U.K. and Norway, while the U.S. and Switzerland were bought. Elsewhere, EMEA, LatAm and APAC were better bid, especially in Türkiye, against moderate buying in South Korea, China and Chile.

“Any teacher who can be replaced by a machine should be.” – Arthur C. Clarke

“No machine has yet replaced the imagination, but machines will compel us to imagine harder.” – Stanisław Lem

Euro area annual inflation was 2.0% in July, unchanged from June and down from 2.6% a year earlier. EU inflation stood at 2.4%, edging up from 2.3% in June but below 2.8% a year earlier. The lowest rates were in Cyprus (0.1%), France (0.9%) and Ireland (1.6%), while the highest were in Romania (6.6%), Estonia (5.6%) and Slovakia (4.6%). Compared with June, inflation declined in eight member states, was stable in six and rose in thirteen. Services made the largest contribution to euro area inflation (+1.46 percentage points), followed by food, alcohol and tobacco (+0.63 percentage points) and non-energy industrial goods (+0.18 percentage points), while energy detracted by 0.23 percentage points. Euro Stoxx 50 -0.313% to 5466.12, EURUSD -0.078% to 1.1638, BBG AGG Euro Government High Grade EUR -1.4bp to 2.885%.

U.K. average private rents rose 5.9% y/y to £1,343 in July, easing from 6.7% in June. England recorded a 6.0% increase to £1,398/month, Wales 7.9% to £807 and Scotland 3.6% to £999, while Northern Ireland rose 7.4% to £855 in May. Within England, the North East saw the highest rental inflation at 8.9%, and Yorkshire and The Humber the lowest at 3.5%. U.K. average house prices rose 3.7% y/y to £269,000 in June, up from 2.7% in May. English house prices went up 3.3% to £291,000, while Wales saw 2.6% growth to £210,000 and Scottish prices climbed 5.9% to £192,000. FTSE 100 -0.207% to 9170.24, GBPUSD +0.06% to 1.3499, 10y gilt -1.9bp to 4.721%.

Germany’s producer prices fell 1.5% y/y in July 2025, following a 1.3% decline in June, and slipped 0.1% m/m. Energy prices were the main drag, down 6.8% y/y, with natural gas (-8.6%), electricity (-7.8%) and mineral oil products (-7.9%) all lower. Intermediate goods also dropped 0.9% y/y, led by cheaper basic chemicals (-2.6%) and metals (-2.2%), with copper down -4.8%. By contrast, capital goods rose 1.8% y/y, non-durable consumer goods 3.5% and durable consumer goods 1.9%. Food prices climbed 4.1% y/y, driven by sharp increases in coffee (+38.4%), beef (+38.0%) and butter (+11.8%), though sugar (-39.5%) and pork (-3.9%) were significantly cheaper. DAX -0.557% to 24287.03, EURUSD -0.078% to 1.1638, 10y Bund -1.3bp to 2.737%.

South Africa’s July CPI rose 3.5% y/y, up from 3.0% in June, while increasing 0.9% m/m, both in line with expectations. Goods inflation accelerated to 3.2% from 2.3%, while services eased slightly to 3.6% from 3.7%. Food and non-alcoholic beverages rose 5.7% y/y, contributing 1.0 percentage point, while housing and utilities increased 4.3%, also contributing 1.0 percentage point. By category, meat prices climbed 10.5% y/y, vegetables 14.6%, and fruits and nuts 9.5%, while dairy slipped 0.8%. Electricity, gas and other fuels rose 8.9% y/y, and water supply charges rose 7.1%. Transport costs fell 1.7% y/y, with fuel down 5.5%. Regionally, inflation was highest in the North West at 4.1% and lowest in Gauteng at 3.0%. JSE TOP40 -0.349% to 93298.86, USDZAR +0.114% to 17.7015, 10y SAGB -0.1bp to 9.656%.

Japan July exports fell -2.6% y/y from -0.5% in June, while imports were down -7.5% y/y from +0.2% y/y in June. The July trade balance came in at a ¥117.5bn deficit. Looking into the breakdown, exports to the U.S., the EU and China were all lower at -10.1% y/y, -3.4% y/y and -3.5% y/y, respectively, while exports to Asia turned negative for the first time since November 2023, at -0.2% y/y. Exports of transportation equipment plunged -11.5% y/y, manufactured goods were down -10% and chemicals -7.3%, while exports of machinery edged up 1.2% y/y. Nikkei -1.51% to 42888.55, USDJPY -0.075% to 147.56, 10y JGB +0.9bp to 1.611%.

Japan June core machine orders rose 3% m/m, 7.6% y/y from -0.6% m/m, 4.4% y/y in May. In the April-June period, core machine orders decreased by 5.3% q/q. Private sector machinery orders, excluding volatile figures for ships and from electric power companies, increased by a seasonally adjusted 3.0% in June and rose by 0.4% in the April-June period. In July-September, the total number of machinery orders is forecast to increase by 3.7%, with private sector orders, excluding volatile elements, forecast to decrease by 4.0% q/q.

The Tokyo metropolitan area’s new condominium market saw 2,006 units launched in July 2025, up 34.1% y/y and 22.2% m/m. The initial contract rate was 68.0%, down 2.9 percentage points y/y but up 7.0 percentage points m/m. Average prices rose 28.4% y/y to ¥100.75mn per unit, with the price per square meter up 30.6% to ¥1.571mn, marking a third consecutive monthly increase. Inventory stood at 5,940 units, slightly below June but higher than a year earlier. High-rise projects (20+ floors) accounted for 668 units across 13 developments, achieving a 78.0% contract rate. Tokyo’s 23 wards dominated supply with 1,045 units, while prices in the area averaged ¥135.32mn, the highest in the region.

China’s loan prime rate (LPR) was unchanged, with the 1y rate at 3.0% and the 5y at 3.5%, holding steady for a third straight month after May’s reduction. The stability reflected unchanged policy rates, in line with market expectations, while the authorities continue to assess the impact of earlier countercyclical support measures. Financing costs have fallen further this year, with interest rates on July new corporate loans averaging 3.2% and new mortgage loans 3.1%, down about 45 and 30 basis points respectively from a year earlier. Social financing costs continue to fall, reducing the urgency for further LPR cuts. Separately, commercial banks’ net interest margin slipped to 1.42% in H1, down 0.01 percentage points from Q1, remaining at a low level. CSI 300 +1.137% to 4271.4, USDCNY -0.044% to 7.1793, 10y CGB +1.2bp to 1.785%.

Taiwanese export orders in July reached USD 57.64bn, up 15.2% y/y (consensus: 16.7%) and 1.5% m/m, though on a seasonally adjusted basis they fell 2.7%. Orders from January to July totaled USD 378.21bn, rising 16.4% y/y. By product group, electronics rose 24.8% y/y to USD 22.59bn and ICT products grew 15.5% to USD 16.32bn, while optical instruments rose 7.5%; traditional goods were weaker, with base metals down 12.6% and plastics down 10.3%. By region, orders from the U.S. surged 25.4% y/y, with rises of 7.3% for Europe, 17.5% for ASEAN and 12.8% for Japan, while orders from China and Hong Kong rose just 3.6%. The Ministry of Economic Affairs noted strong AI, high-performance computing and cloud demand driving growth, though uncertainty from trade policy and geopolitics remains. TAIEX -2.99% to 23625.44, USDTWD +0.621% to 30.302, 10y TGB +4.1bp to 1.411%.

Taiwan’s Q2 current account hit a new high of USD 36.23bn vs USD 29.756bn in Q1 2025. The goods trade surplus rose by USD 15.04bn y/y to USD 36.18bn. This was mainly due to an expansion in exports, underpinned by rising demand for emerging technology applications and inventory frontloading by overseas firms. The services account deficit widened by USD 0.05bn versus a year ago to US$4.27bn, mainly because of an increase in construction expenditure. In terms of portfolio investment flows, residents’ portfolio investment abroad showed a net decrease of USD 7.00bn, mainly because insurance companies reduced overseas debt securities holdings. Non-residents’ portfolio investment recorded a net increase of USD 13.99bn, mainly attributable to an increase in Taiwanese equity holdings by foreign investors.

South Korea’s net international investment position (IIP) stood at $1.0304tn at the end of Q2 2025, down $53.6bn from the previous quarter. Overseas investment assets rose by $165.1bn to $2.6818tn, while foreign investment in South Korea increased by $218.6bn to $1.6514tn. Net external assets in debt instruments fell $10.7bn to $357.2bn, with external assets rising $41.4bn to $1,092.8bn and external debt climbing $52.1bn to $735.6bn. By category, South Korea’s portfolio investment abroad rose $113.2bn, led by a $95.6bn gain in equity securities, while foreign portfolio investment in South Korea expanded $186.0bn, mainly through equity securities, which jumped $147.7bn. KOSPI -0.681% to 3130.09, USDKRW +0.536% to 1398.9, 10y KTB +2.2bp to 2.857%.