Market Movers: Revisions

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

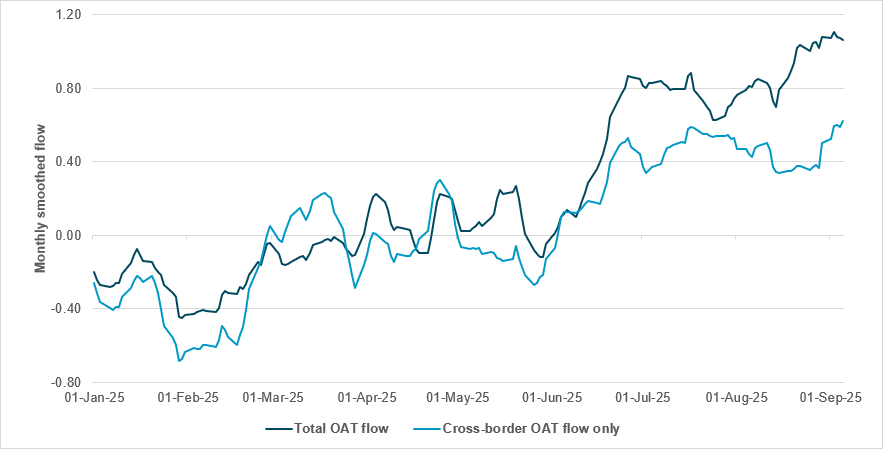

CROSS-BORDER INTEREST IN OATS A POTENTIAL STRESS POINT

Source: BNY

Over the past week, we have observed that despite the gyrations in European politics, general interest in sovereign debt has remained solid. On a daily flow basis, OATs remain net bid, without any indication of outflows, as investors feel adequately compensated for relevant risks. Compared with the asset allocation set up at the end of last year when François Bayrou succeeded Michel Barnier, OAT interest is in a completely different place, and we would add that hedging levels on EUR are only around half of levels during that period. However, we note an important shift in the distribution of client interest. At the end of last year, cross-border OAT flows were generally below the aggregate figure, indicating stronger liquidation activity among international investors. Between March and June this year, the two investor groups broadly offset each other, resulting in more balanced positioning. Over the past three months, however, during the period of surge flows, the gap between total OAT flows and cross-border interest has widened significantly. This does not suggest that international investors are actively selling, but it does indicate that the over-allocations to European exposure which we are seeing in the equity markets, or as a simple diversification play against the U.S., are no longer as prominent. Stronger home bias and domestically funded public investment will be an increasingly prominent asset allocation theme globally, but this doesn’t mean any major government bond market can afford a sharp decline in international participation without a significant impact on financial conditions.

Clarity over policy is driving the day, as risks leave global equities mixed, despite ongoing political uncertainty. Talk of the BoJ hiking rates despite the current political uncertainty following PM Shigeru Ishiba’s resignation has driven JPY higher against USD and sent shares lower. One key reason is that the tariff concerns of H1 are over; there is a limit to the trade policy worries. Witness Taiwan’s trade surplus, with exports up 34.1% y/y, contrasting with Vietnam’s 2% fall in exports to the U.S. The search for a new PM in France leaves equities higher, while OATs are outperforming Bunds. The one exception is Indonesia, where the new Finance Minister Purbaya Yudhi Sadewa promises to grow the economy, despite IMF warnings leaving IDR weaker. U.S. stock market futures are positive again amid ongoing expectations of Fed easing, with today’s revisions from the BLS on the quarterly establishment survey expected to cut more jobs out of the 2025 data. Markets are sanguine, taking the view that the mix of a weaker USD, more supportive Fed policy and reduced trade concerns will drive equity markets higher. Adding to this view is that liquidity remains ample, with the U.S. markets seeing $28bn in IG issuance yesterday and bonds rallying despite the supply. Investor demand for both stocks and bonds is being met by the private sector. Whether economic growth and inflation globally hold will matter, but just not now, as the flows around political worries show. The question for investors into the U.S. open revolves around the role of a weaker dollar and whether there is a limit to the move, as gold, AUD and oil all continue to rally. The search for safety has shifted to a sprint, with investors racing to end the year well. Equities are leading, but not in unhedged terms: the S&P 500 is up 10.4%, near its historic highs, but that performance lags behind the Nikkei (up 16.7% in USD terms in USD terms) or the Euro Stoxx (up 24.2%).

The Bank of Japan looks likely to slightly reduce its government bond purchases in the 10-25y maturity zone in October-December, report multiple sources. While upward pressure on super-long yields persists, the BoJ aims to prioritize market predictability, as its purchase ratio in this zone, i.e., 50.6% of issuance, is significantly higher than the 5-10y range, at 40.4%. The final decision will follow the 20y JGB auction on September 17 and be guided by market conditions. If implemented, this would be the second cut this year, after a ¥45bn monthly reduction in April-June. Officials indicated that reductions are guided by purchase ratios, and further exemptions would require special justification. Separately, Bloomberg reported that the BoJ still sees a chance of a hike this year despite the political situation, but it will likely keep rates unchanged on September 18. Nikkei -0.423% to 43459.29, USDJPY -0.333% to 147.01, 10y JGB +0.3bp to 1.574%.

French Prime Minister François Bayrou is set to submit his resignation to President Emmanuel Macron after losing a confidence vote in the National Assembly, with 194 votes in favor and 364 against. The Elysée confirmed Macron will appoint a new prime minister in the coming days, noting it had taken note of the deputies’ decision under Article 49.1 of the Constitution. Political reactions are expected throughout the day, with figures including Gabriel Attal, Yaël Braun-Pivet and Jordan Bardella due to speak in the media. Meanwhile, ahead of the September 10 “Bloquons tout” (Block Everything) day of national protest, which could see as many as 100,000 people take part, police reported that 200 “Bayrou farewell gatherings” outside town halls drew around 11,000 participants. CAC40 +0.454% to 7769.98, EURUSD -0.145% to 1.1746, 10y OAT +7.8bp to 3.487%.

Norway’s Labor Party secured a narrow victory in the general election, with Prime Minister Jonas Gahr Støre and his center-left allies winning 87 out of 169 parliamentary seats, against 82 for the center-right opposition. The Progress Party surged to 24% of the vote, its best-ever result, overtaking the Conservatives, who posted one of their weakest performances in decades. Conservative leader Erna Solberg accepted responsibility for the loss. Støre hailed the result as proof that social democrats can win despite a right-wing surge across Europe; he is expected to form a government with four left-leaning partners. The campaign centered on cost-of-living pressures, wealth taxes and foreign policy, while Labor’s rebound was credited to Jens Stoltenberg’s return as finance minister. OSE +0.124% to 1634.67, EURNOK -0.16% to 11.7275, 10y NGB +0.5bp to 3.908%.

Indonesian assets remain under pressure following the abrupt removal of Finance Minister Sri Mulyani Indrawati and subsequent cabinet reshuffle. The rupiah slid over 1% to 16,485 to the U.S. dollar, its sharpest drop since April, and Jakarta stocks were down 1%. Bank Indonesia intervened in currency and bond markets to stabilize conditions. Mulyani, seen as a guarantor of fiscal prudence, was replaced by Purbaya Yudhi Sadewa, who has pledged to accelerate growth, including funding President Prabowo’s costly free meals program. Investors fear rising deficits and policy uncertainty, with bond yields rising and foreign holdings of government securities already scaled back to below 14%. Reserves stood at $150.7bn in August, giving the central bank scope to defend the currency. JCI -1.727% to 7632.738, USDIDR +1.049% to 16475, 10y IDGB +5.6bp to 6.445%.

U.S. BLS preliminary benchmark revision to the establishment survey labor data, with a consensus of -575 jobs.

U.S. Treasury sells $85bn in 6-week bills and $58bn in 3y notes.

Mood: Sentiment continues to improve with steady momentum in equity buying, against a slight reduction in demand for core sovereign bonds.

FX: ILS, MXN and SGD posted the most outflows, against most inflows in HUF and HKD. Elsewhere, G10 flows were mixed and light, with USD and EUR selling vs. inflows in AUD, JPY and GBP, and better buying in EMEA and APAC currencies.

FI: Good demand for Eurozone government bonds, U.K. gilts, U.S. Treasurys and Australia government bonds. Poland, Hungary and Singapore government bonds were most sold.

Equities: Clear shift in asset allocation out of developed markets into emerging markets across the Americas, EMEA and APAC regions. Specifically, Eurozone and Colombian equities were significantly sold, against strong buying of Brazilian, Peruvian and South African equities.

“My pencils outlast their erasers.” – Vladimir Nabokov

“Revision is not going back and fussing around, but going forward into the process of creation.” – May Sarton

U.K. retail sales increased by 3.1% y/y in August, supported by record warm weather and a BoE interest rate cut, with strong performance in food, drink and computer sales as parents prepared for the new school year. However, the British Retail Consortium (BRC) noted that the 4.7% rise in food and drink spending was driven by price inflation rather than volume growth, with staples like beef, chocolate and coffee experiencing notable price increases. Furniture and home goods sales also grew for the second consecutive month, aided by new product launches and a prior surge in property transactions. Despite these gains, retailers expressed concern about consumer confidence and spending during the upcoming golden quarter due to tax rise speculation ahead of a delayed budget announcement scheduled for late November. FTSE 100 +0.173% to 9237.35, GBPUSD +0.119% to 1.3561, 10y gilt +2.7bp to 4.632%.

France’s industrial production experienced a decline in July, with manufacturing output falling by 1.7% m/m following a 3.5% increase in June, while overall industrial production decreased by 1.1% m/m after a 3.7% rise. The manufacturing sector showed a 1.3% y/y increase over the three months from May to July, driven primarily by a 10.5% rise in transport equipment production and modest 0.6% growth in electrical, electronic and computer equipment. Conversely, production dropped in extractive industries, energy and water (-1.4%), agro-food industries (-1.7%) and coke and refining (-3.3%). The transport equipment sector saw a sharp 10.7% m/m decline in July, mainly due to a post-peak reduction in aerospace manufacturing. Construction production rebounded by 0.6% m/m in July but was down 3.6% y/y over the May-July period. CAC40 +0.454% to 7769.98, EURUSD -0.145% to 1.1746, 10y OAT +7.8bp to 3.487%.

Norway’s August price index of first-hand domestic sales rose 1.9% y/y and 0.1% m/m, bringing the index to 132.2. Food prices increased 2.2% y/y despite a 0.8% m/m fall, while beverages and tobacco climbed 6.6% y/y. Chemicals rose by 2.4% y/y, manufactured goods by 1.4% y/y and machinery and transport equipment by 2.5% y/y. Crude materials fell 4.5% y/y, and construction-related goods were also down. Meanwhile, the producer price index dropped 3.0% y/y and 0.9% m/m, with energy goods down 9.1% y/y and extraction services off 11.8% y/y. Electricity, gas and steam surged 40.1% y/y, while manufacturing rose 1.7% y/y, led by machinery and equipment (+5.6%) and food products (+3.5%). OSE +0.124% to 1634.67, EURNOK -0.16% to 11.7275, 10y NGB +0.5bp to 3.908%.

Hungary’s consumer prices were 4.3% higher y/y in August 2025, while flat m/m, both in line with expectations. Food prices rose 5.9% y/y, led by eggs (+19.9%), coffee (+18.5%), chocolate and cocoa (+18.3%) and fresh domestic and tropical fruits (+28.9%), though margarine (-29.5%), flour (-11.6%) and sugar (-10.0%) fell. Energy costs increased 11.0% y/y, with natural and manufactured gas up 23.2%. Alcohol and tobacco rose 7.3%, services 5.4% with rents up 10.2%, while consumer durables gained 2.4%, driven by jewelry (+22.2%). Motor fuel prices declined 4.3%. On a monthly basis, services rose 0.5%, food was stable, and alcoholic beverages and tobacco climbed 0.6%, offset by declines in seasonal food (-2.1%), motor fuels (-0.8%) and pharmaceuticals (-0.3%). Budapest SI +0.081% to 103057.3, EURHUF +0.102% to 393.69, 10y HGB -6bp to 7.07%.

Japan’s August machine tool orders totaled ¥119.7bn, down 6.7% m/m but up 8.1% y/y. Domestic orders fell 10.5% m/m and 1.4% y/y to ¥31.7bn, while foreign orders declined 5.3% m/m but rose 12.0% y/y to ¥88.0bn. Cumulatively for January-August, total orders stood at ¥1,025.6bn, up 5.2% y/y. Domestic orders reached ¥289.5bn, close to flat y/y at -1.0%, whereas foreign orders rose 7.9% y/y to ¥736.1bn. Nikkei -0.423% to 43459.29, USDJPY -0.333% to 147.01, 10y JGB +0.3bp to 1.574%.

Australia’s September Westpac Consumer Sentiment Index was down -3.1% m/m to 95.4 points. Outright optimism remains elusive for Australian consumers. The economic outlook deteriorated, with the 12-month sub-index down 8.9% to 92.2 and the five-year outlook falling 5.9% to 92.7. Household finances showed some improvement, with the “family finances vs. a year ago” measure rising 2.6% to 86.3 and the “next 12 months” outlook up 0.9% to 107.7. The “time to buy a major item” index slipped 3.4% to 98.2, while homebuyer sentiment fell 1.7% to 96.1. Unemployment expectations rose 4.6% to 131.4, while house price expectations gained 2.6% to a 15-year high of 168.4. ASX +0.152% to 4998.27, AUDUSD +0.228% to 0.6607, 10y ACGB -1.5bp to 4.265%.

Australia’s NAB business conditions index rose from 5 to 7 points in August, reflecting gains in employment and profitability. While business confidence fell three points in August, this follows four consecutive months of improving sentiment and leaves confidence close to long-run average levels. Forward orders rose again, continuing the upward trend evident over the past year. The series is now in positive territory for the first time in two years. The cyclically sensitive manufacturing and retail sectors both registered improvements in confidence and conditions (in trend terms). Capacity utilization, already at an above-average level, increased over the month and reflects continued tightness in the supply/demand balance. However, measures of costs and prices moderated slightly in August. Purchase costs in August grew at their slowest pace since 2021, while labor costs and product price growth have broadly tracked sideways in recent months. Overall, the survey supports the view that the business outlook has become more positive in recent months, consistent with a better tone to official economic data of late.

New Zealand Q2 manufacturing activity declined by -3% q/q from a downwardly revised 4.8% q/q in Q1 2025. Business financial data for the June quarter showed sales at $196bn, up $4.1bn or 2.1% y/y, while purchases rose 1.9% to $136bn. Salaries and wages reached $32bn, up 1.2%, and operating profit increased by 4.2% to $28bn. On a seasonally adjusted basis, sales rose vs. March in eight out of 14 industries, led by electricity, gas, water and waste services (+$1.1bn), while manufacturing (-$1.0bn) and construction ($720mn) saw falls. Mining recorded the strongest annual rise at 20%, followed by health care and social assistance (+5.9%) and forestry and fishing (+5.1%). Construction posted the largest annual decrease, at -7.1%, while most other sectors saw modest gains. NZX 50 -0.206% to 13253.73, NZDUSD +0.085% to 0.5945, 10y NZGB -3.4bp to 4.308%.

New Zealand’s construction sales decreased by 3.1% in the June 2025 quarter, falling by $720mn q/q to $22.3bn. This decline follows a 0.7% rise in the previous quarter and represents an 11% decrease since June 2023. The value of building work put in place, which accounts for activities requiring building consent, was $7.9bn, or 35% of construction sales, down 14% y/y. Adjusted for inflation, building activity volumes fell by 18% over the two years to June 2025. Manufacturing sales also declined by 3.0% to $33.4bn, with significant decreases in non-metallic mineral product manufacturing (-4.9%), metal product manufacturing (-5.1%) and wood and paper products manufacturing (-3.2%), all closely linked to construction materials.

South Korean banks saw their capital adequacy ratio inch up in Q2 2025. The average capital adequacy ratio of 17 commercial and state-run banks stood at 15.95% as of end-June, up from 15.66% three months earlier. The Financial Supervisory Service (FSS) said that the reduced risk-weighted assets, along with sound earnings, helped jack up the ratio. The ratio, a key barometer of financial soundness, measures a bank’s capital as a proportion of its risk-weighted assets. KOSPI +1.257% to 3260.05, USDKRW +0.127% to 1389.1, 10y KTB -1bp to 2.857%.

In another sign that Beijing is stepping up the battle against “involution” and deflation, China’s State Administration for Market Regulation (SAMR) announced in its Q3 press briefing that it has introduced a set of policies to regulate market order and improve the business environment. These include compliance guidelines for online platform fees and a three-year action plan on industrial product safety. Emphasizing the food delivery sector, the SAMR addressed recent controversies over platform subsidies, stating that major platforms were summoned and have since pledged to comply with laws, avoid unfair competition, curb excessive subsidies and promote orderly market practices. The SAMR will continue to monitor competition in the sector, require improvements in service quality and food safety, push for fairer subsidy policies, enhance support for merchants and strengthen protections for delivery riders, aiming to build a balanced ecosystem for consumers, businesses, riders and platforms. CSI 300 -0.701% to 4436.26, USDCNY -0.055% to 7.1259, 10y CGB +0.7bp to 1.798%.