Market Movers: Removals

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 10 minutes

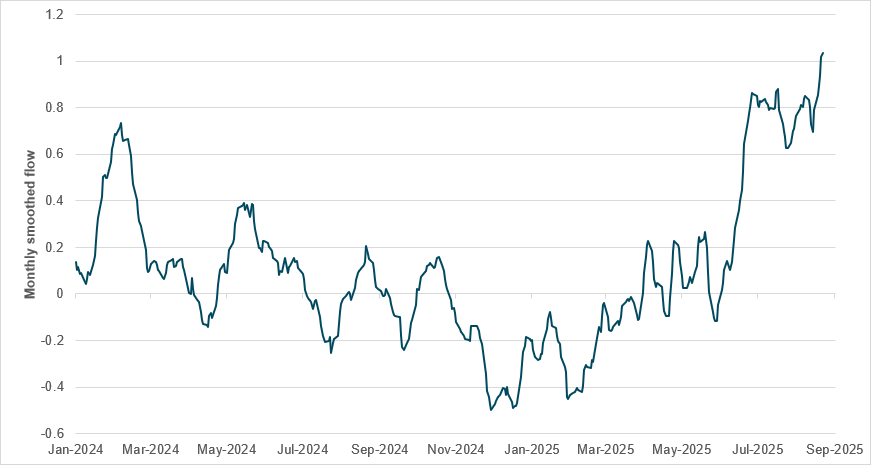

MONTHLY SMOOTHED FLOW, OATS

Source: BNY

It’s déjà vu all over again for Eurozone sovereign bond investors, as French political instability threatens the already-fragile fiscal agenda. What is more concerning for the OAT market ahead of the confidence vote scheduled for September 8 is that flow momentum into OATs is exceptional, even excessive, making the risk of a material correction very high. Parallels with last year – when President Macron’s decision to call snap parliamentary elections led to significant weakness in the OAT market through June 2024 before conditions stabilized – are clear. The selloff then was amplified by relatively crowded positioning in OATs, as the market was viewed as preferable to German Bunds due to yields and liquidity. Some changes in market structure this year, especially greater Bund supply from Germany’s fiscal adjustments, have helped ease some of these pressures. However, the 10y OAT’s 80bp spread over Bunds remains too wide to ignore, especially with real rates in a good position due to relatively contained French inflation. Nonetheless, France’s fiscal risks remain elevated, and recent developments underscore the difficulty of altering the outlook. The current spread between 10y Italian BTPs and French OATs is less than 10bp, and based on current fiscal trajectories we expect BTPs to trade below their OAT equivalents soon. Liquidation of elevated holdings, potentially rotating into Bunds and BTPs, would only accelerate this process.

There is a sea of red numbers today as risk aversion returns, with political worries dominating all assets. The upcoming no-confidence vote in France, coupled with President Trump’s removal of Federal Reserve Governor Lisa Cook, sent stocks lower globally. Higher yields on U.S. and U.K. bonds aren’t helping either. The concerns about rates and debt are clear. The risks of hawkish Fed easing and stall-speed economies in developed markets follow on from that. There is also rising uncertainty, which explains the price action, and Cook’s firing is a historic test of U.S. presidential power. Tariffs and the power of the courts continue to be tested, and businesses’ ability to invest without clarity on import levies and stable interest rate policy makes future investments a crucial marker for confidence, despite the noise. The return of important economic data to the U.S. news agenda sets up markets for a larger test of the summer calm and bull market return. Expect the durable goods and conference board confidence survey announcements to matter a bit more for trading today, as investors need good news to balance out the current doubt. FOMC Chair Jerome Powell’s ability to cut rates and declare victory in the form of a soft landing has passed – and with it the guardrails for investors, as they rethink the summer drop in volatility. September trading appears to have started early. The question for investors today is what to remove from the portfolio to ease volatility risks: with USD vulnerable to a rate cut and U.S. and European bonds seeing yield curve steepening on debt sustainability doubts, there are fewer safe havens today.

The Fed’s John Williams said that the trend toward a low neutral rate hasn’t reversed and the era of low neutral rates is far from over. While r-star (the natural rate of interest) is famously difficult to estimate with precision and estimates vary across models, model-based estimates remain valuable for predicting future real interest rates, especially compared with market-based measures. Drawing on evidence from a variety of models, a reasonable estimate is that r-star has risen by a relatively modest quarter to half a percentage point from its 2018 level. Thus, despite the recent rise in TIPS yields, the evidence suggests that the low r-star era is far from over. S&P Mini -0.174% to 6444.25, DXY -0.012% to 98.419, 10y UST +2bp to 4.295%.

France’s minority government faces a likely collapse as Prime Minister François Bayrou called an extraordinary September 8 confidence vote on his €43.8bn budget squeeze, weeks earlier than expected. Bayrou argued that the country’s dire financial situation required urgent action, but opposition parties across the spectrum have already vowed to bring him down. Far-left France Unbowed and far-right National Rally leaders, including Marine Le Pen, confirmed they would vote against the government. Bayrou’s survival hinges on Socialist support, but party leader Olivier Faure has ruled this out, citing anger over collapsed pension reform talks. The vote comes just before a nationwide shutdown on September 10, with Bayrou acknowledging the risk of triggering his government’s fall but framing it as necessary to safeguard France’s stability, sovereignty and credibility. CAC40 -2.065% to 7681.07, EURUSD -0.009% to 1.1617, 10y OAT -0.8bp to 3.503%.

South Korean companies have pledged an additional $150bn in U.S. investment, adding to the earlier $350bn commitment linked to a recent trade deal that lowered reciprocal tariffs. The announcement was made by Ryu Jin, Chairman of the Federation of Korean Industries, during a Washington roundtable attended by senior officials and business leaders, including Samsung Electronics Chairman Lee Jae-yong, U.S. Commerce Secretary Howard Lutnick and Nvidia CEO Jensen Huang. The investment will target semiconductors, biotechnology, AI, shipbuilding and nuclear energy, with both sides stressing cooperation on supply chains for mobility, batteries and key materials. The meeting also addressed energy demand in the AI era, while reaffirming bilateral commitments to strengthen shipbuilding as a strategic industry. KOSPI -0.95% to 3179.36, USDKRW +0.493% to 1397.4, 10y KTB -0.8bp to 2.852%.

U.S. August Philadelphia Fed non-manufacturing index expected up to -8 after -10.3.

U.S. July preliminary durable goods orders are expected to decline for the second month in a row at -3.8% m/m, from -9.4% in June. The durables ex-transportation measure is expected to be unchanged at 0.2% m/m.

U.S. June FHFA house price index is expected to a record third month of m/m decline at -0.1%, after -0.2% m/m in May and -0.3% m/m in April.

U.S. June CoreLogic CS 20-city is expected to fall -0.2% m/m, +2.09% y/y from -0.34% m/m, +2.79% y/y in May.

U.S. August Richmond Fed manufacturing index is expected to improve from -20 to -11.

U.S. August Conference Board consumer confidence is forecast to ease to 96.5 from 97.2.

U.S. Treasury sells $85bn in 6-week bills and $69bn 2y notes.

Fedspeakers: Richmond Fed Tom President Barkin speaks on the economy with Q&A in Virginia.

Mood: iFlow Mood remains in the risk-off zone but is off its lows. Equity buying flows picked up slightly, while demand for core sovereign bonds was firm.

FX: JPY, EUR, INR and CNY posted the most inflows amid broad selling pressure in the rest of the iFlow universe. IDR, THB and CLP were most sold. IDR scored holdings are approaching neutral, having been in overheld conditions since February 2022.

FI: Good buying of G10, LatAm and EMEA sovereign bonds except for selling in APAC. U.K. gilts, U.S. Treasurys and Eurozone, Chile, Poland sovereign bonds were most bought. Norway, Indonesia and Chinese government bonds were sold.

Equities: Mixed and light flows. Within the G10, U.S., European and U.K. equities were sold against buying in Swedish and Japanese equities. LatAm and EMEA equities were bought, against mixed flows in APAC region, led by selling in Taiwanese equities. Within the DM EMEA region, the consumer staples sector was sold, against most demand for the energy and health care sectors.

“The first condition of progress is the removal of censorship.” – George Bernard Shaw

“Beware of what you let enter your heart. There will come a day when you’d give anything to remove it.” – Yasmin Mogahed

France’s household confidence index fell to 87 in August 2025 from 88 in July, its lowest level since October 2023 and well below the long-term average of 100. Households’ expectations regarding their future financial situation deteriorated, while views on past finances improved slightly. Major purchases were stable but remained subdued. The share of households considering it a good time to save dropped sharply, though saving capacity assessments remained above average. Perceptions of both past and future standards of living declined further, while unemployment fears edged up. Inflation expectations increased, with more households anticipating faster price rises over the next 12 months, the highest level since March 2023. CAC40 -2.065% to 7681.07, EURUSD -0.009% to 1.1617, 10y OAT -0.8bp to 3.503%.

Sweden’s July Producer Price Index rose 1.1% m/m, with equal increases of 1.1% on the domestic and export markets and a 0.9% rise on the import market. The annual PPI rate stood at -0.6%, from -3.1% in June. Domestic prices were supported by rises for trade services of electricity, refined petroleum products and non-metallic minerals, partly offset by decreases for waste services and paper. Export price growth was driven by basic metals, machinery and motor vehicles, while imports rose mainly on refined petroleum and food products. Annually, domestic market prices increased by 1.9%, export prices fell by 3.1% and import prices declined by 2.8%. Consumer goods rose 2.0% in PPI and 3.3% in the Price Index for Domestic Supply, while energy-related products fell 0.8% and 6.7%, respectively. OMX -0.369% to 2658.649, EURSEK +0.157% to 11.1587, 10y Swedish GB -2.4bp to 2.543%.

British Retail Consortium data showed U.K. August shop prices rose 0.9% y/y after 0.7% in July. Food inflation increased to 4.2% y/y from 4.0%, with fresh food up 4.1% compared with 3.2% in July, while the rate for ambient food eased to 4.2% from 5.1%. Non-food prices fell 0.8% y/y after a 1.0% decline in July. On a m/m basis, overall shop prices increased by 0.2%, matching July’s rise. Food prices rose 0.4% m/m compared with 0.1% previously, while non-food prices were flat after 0.3% in July. This marked the third straight month of positive overall m/m growth, driven by food categories against persistent weakness in non-food. FTSE 100 -0.68% to 9258.05, GBPUSD +0.06% to 1.3463, 10y gilt +5bp to 4.743%.

Poland’s registered unemployment rate stood at 5.4% in July 2025, up 0.2 percentage points m/m and 0.4 percentage points y/y. 830,800 people were registered as jobless, 4.2% more than in June and 8.5% more than a year earlier. Average enterprise employment was 6.43 million, down 0.9% y/y, with declines in mining (-3.4%), motor vehicle repair (-2.5%) and transport (-1.4%), while increases were recorded in electricity supply (+1.6%) and accommodation (+1.5%). Regional unemployment rates ranged from 3.3% in Wielkopolskie to 8.7% in Podkarpackie, rising in all voivodeships. Among the unemployed, women accounted for 50.8%, long-term jobless people for 46.8% and those without qualifications for 32.6%. In July, 108,400 new registrations were recorded and 74,600 people exited unemployment, while employers declared 45,900 job offers and 5,500 group layoffs. WIG -0.796% to 107664.3, EURPLN +0.132% to 4.2664, 10y PGB -1.1bp to 5.407%.

South Africa’s composite leading business cycle indicator rose 0.4% in June 2025, following three months of declines. Gains from real M1 money supply growth and higher commodity export prices outweighed drags from a narrower interest rate spread and weaker passenger vehicle sales. On a 12-month basis, the indicator contracted 0.5%. The coincident indicator increased 0.5% in May, supported by higher industrial production and stronger manufacturing capacity utilization, while the lagging indicator rose 1.0% in May. Over the past year, the coincident indicator edged up 0.1% while the lagging indicator fell 1.3%. Key negatives in June included fewer building plans approved and reduced job advertisements. JSE TOP40 -0.725% to 94638.6, USDZAR +0.228% to 17.6474, 10y SAGB +3.7bp to 9.615%.

Japan’s July Services Producer Price Index (SPPI) rose 2.9% y/y after 3.2% in June, while the index excluding international transportation increased 3.0% y/y, from 3.3%. On a m/m basis, overall SPPI gained 0.3% following a 0.2% decline in June. By sector, transportation and postal activities saw a rise of 3.1% y/y, driven by a 24.5% surge for postal services and a 5.7% rise in domestic air passenger transport, though international air freight fell 13.2%. Other services advanced 3.3% y/y, with hotels up 5.4% and meal supply services up 7.9%. Information and communications prices climbed 2.9% y/y, supported by software development and internet-based services. Real estate services rose by 2.2%, leasing and rental by 2.0%, and finance and insurance by 1.4%. Nikkei -0.966% to 42394.4, USDJPY -0.129% to 147.61, 10y JGB +0.6bp to 1.63%.

The Trump administration outlined plans to implement a 50% tariff on products from India in a draft notice. The increased levies would hit Indian products “that are entered for consumption, or withdrawn from warehouse for consumption, on or after 12:01 a.m. eastern daylight time on August 27, 2025.” Trump indicated that he could impose additional tariffs on Russian trading partners or sanctions targeting Moscow if there was no progress on a deal, saying there could be “very big consequences” if nothing happens in the coming weeks. SENSEX -0.634% to 81118.65, USDINR +0.176% to 87.7337, 10y INGB +3.4bp to 6.631%.

South Korean August consumer confidence rose to 111.4 from 110.8, breaking previous highs of 111.1 in June 2021 and hitting its highest level since January 2018. The expected inflation for the next 12 months rose from 2.5% to 2.6%, while 3y and 5y inflation expectations are both at 2.5%. Looking into the details, consumer sentiment regarding current living standards was 96 (July: 94), while the future outlook measure was unchanged at 101. Consumer sentiment relating to future household income and future household spending were both unchanged, at 102 and 111, respectively. Consumer sentiment concerning current domestic economic conditions was 93 (July: 86), and the future domestic economic conditions measure was 100 (July: 106). KOSPI -0.95% to 3179.36, USDKRW +0.493% to 1397.4, 10y KTB -0.8bp to 2.852%.

The RBA’s August monetary policy meeting minutes attributed the 25bp rate cut to 3.60% to inflation returning sustainably to target and labor market conditions nearing balance. Domestic growth remained subdued but was improving, with housing and credit activity picking up. Inflation had eased as expected, though headline figures would temporarily rise due to energy rebate changes. The RBA flagged the potential for further rate cuts, to be guided by incoming data. Members noted that the downward revision to the assumption for medium-term productivity growth was judged not to have implications for the degree of inflationary pressure, and hence for the monetary policy stance. Uncertainty about the degree of spare capacity and the neutral interest rate could warrant a “measured approach” to assess what incoming information reveals about these and other uncertainties. The RBA reaffirmed its strategy of allowing pandemic-era bond holdings to mature without active sales. ASX -0.69% to 5014.63, AUDUSD -0.093% to 0.6476, 10y ACGB +3.1bp to 4.314%.

Singapore’s manufacturing business expectations for July-December 2025 showed a net weighted balance of +5%. 85% of firms expect conditions to remain unchanged, 10% expect improvement and 5% foresee a weaker outlook. Electronics was the most optimistic cluster (+17%), driven by semiconductors on expectations of seasonal order growth and strong AI-related demand. Precision engineering also posted a mildly positive outlook (+4%), while transport engineering remained broadly unchanged and aerospace was supported by steady aircraft MRO demand. Chemicals was the weakest cluster (-7%) amid concerns over trade policy impacts on exports. For July-September 2025, overall output is expected to rise modestly (+2%), led by biomedical manufacturing (+38%) and aerospace (+36%), while chemicals (-21%) and general manufacturing (-22%) anticipate declines. Employment is projected to remain largely stable, with a net weighted balance of +1%. STI -0.297% to 4243.84, USDSGD +0.039% to 1.2861, 10y SGB -5.3bp to 1.857%.