Market Movers: Hard Roads

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 9 minutes

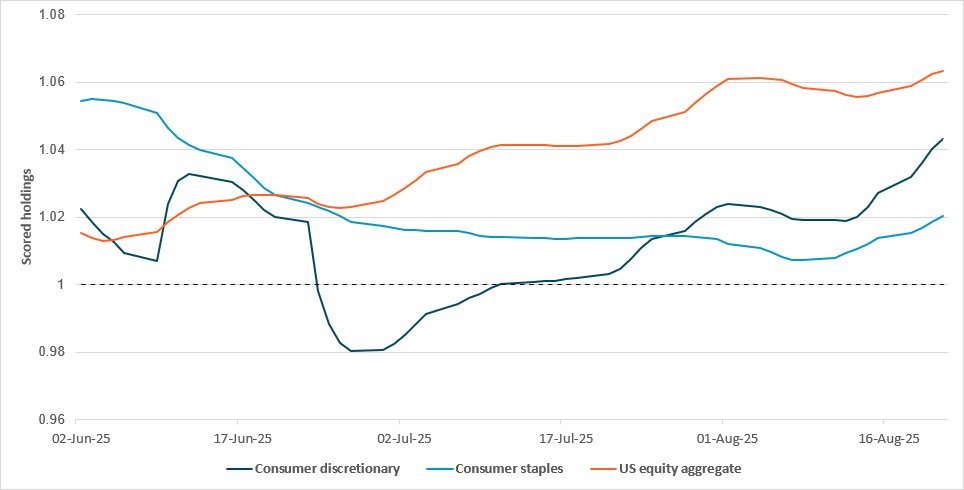

CONSUMER SECTORS LAG BROAD INDEX DESPITE IMPROVED MOMENTUM

Source: BNY

Fed Chair Jerome Powell’s acknowledgement of a “shifting balance of risks” in the labor market means that the state of U.S. consumer spending will be under the microscope for the rest of the year. Secular investment trends in tech continue to support broader equity holdings, but we believe it will be difficult for material sectoral holdings divergence to continue indefinitely. Recent quarters may indicate that capital expenditure is generating more GVA growth, but rebalancing of any economy cannot take place in a handful of quarters, let alone an economy as big and diversified as the U.S. Stagflation scenarios are particularly fraught, as they imply erosion of real earnings at a time when labor market weakness could hurt normal earnings growth. This would not just damage spending intent, but could also put household debt servicing into doubt; this has hitherto been one of the U.S. economy’s strong points post-pandemics. This figure stood at 5.4% of household disposable income as of Q1 2025, around 40bp below pre-pandemic levels but over 100bp above the 2021 low of 4.30%. However, equity markets continue to give households the benefit of the doubt. Both consumer discretionary and staples have underperformed the broader market in holdings terms, but momentum is clearly on the rise, especially in discretionary spending. This chimes with the cautiously optimistic guidance provided by exposed corporates in the most recent earnings season. Impending rate relief will likely support expectations further, but we see the gains more as an indication of prior caution being scaled back than of an imminent strong recovery in household spending.

There has been a mixed tape for equities today: APAC has seen Chinese shares lead a bounce-back in risk, while EU shares have seen a pull-back, rethinking Jackson Hole-related rallies. The bubble risk in China is increasing, with yet another push to fix its property markets. The hard road for U.S. equities ahead links back to the real economy and the fate of the U.S. consumer, along with the investment case for business. The end of summer is approaching fast, and the turn for the week may be in that set-up for investors, as they prepare for September risks ranging from hard economic data to softer hopes of Fed easing. Jerome Powell’s speech will likely still dominate today’s U.S. trading session, and, as the incumbent FOMC chair notes, it’s a “challenging situation.” The choice of whether to constrict rates on higher inflation fears linked to tariff hangovers or to ease them given the slowing, uneven economy sets the stage for risk ahead. U.S. equity futures are bid; the rally has been led by the pricing in of 84% of a September cut. The overnight price action in bonds suggests trouble ahead: Bunds show the reality of a likely ECB hold in September driving on the German Ifo index – now at a 15-month high – which suggests slow improvement from the Q2 slump. Adding to concerns for bonds, we have curve steepening and the return to the old Fed policy framework, ditching the “makeup” strategy of letting inflation run hot. Whether investors see any worries in rates ahead also rests on how USD reacts; carry and trend remain neutral in our iFlow measures, suggesting little appetite for breaking out of the August ranges. The week’s main risk lies with the economic agenda, which includes the core PCE price index on Friday, and the last of the key Q2 earnings reports, with Nvidia on Wednesday. The Fed’s balancing act between full employment and stable prices at 2% CPI hangs heavily on the shoulders of investors as we head in September.

Fitch affirmed the U.K.’s sovereign credit rating of AA- with stable outlook on August 22. The agency cited strong fundamentals including a large, diversified economy, a credible policy framework and sterling’s reserve currency status, offset by high public debt, weak productivity and subdued growth. GDP is forecast at 1.2% in 2025-2026 before rising to 1.5% in 2027, while inflation is projected to fall from 3.8% in July to 2.8% at end-2025. Fitch expects the deficit to narrow from 5.3% of GDP in 2025 to 4.4% in 2027, with debt climbing to 106% of GDP. Interest rates are projected to fall gradually to 3% by 2027. FTSE 100 +0.131% to 9321.4, GBPUSD -0.126% to 1.3508, 10y gilt -3.6bp to 4.693%.

Germany’s Ifo business confidence index rose to 89.0 in August (consensus: 88.8), its highest level since April 2024. The median forecast for business confidence was 88.8, with a range of between 87.5 and 90. The current assessment of the business situation increased slightly to 86.4, while future business expectations improved significantly to 91.6. Sector-wise, manufacturing came in at -12.2, services at +2.6, trade at -21.4 and construction at -15.3. Overall, the business climate reflected a continued recovery across most sectors. Ifo President Clemes Fuest noted that the recovery of the German economy “remains weak” even though company sentiment in Germany has “brightened slightly.” DAX -0.399% to 24265.87, EURUSD -0.12% to 1.1704, 10y Bund +3.5bp to 2.757%.

Singapore July inflation eased further, with the headline and core rates at 0.6% y/y (June: 0.8%) and 0.5% (June: 0.6% y/y), respectively. This was driven by a fall in the prices of retail and other goods, as well as lower electricity and gas inflation. On a m/m basis, core prices fell by 0.1% in July, with the headline rate down -0.4%. The MTI is maintaining its 0.5-1.5% projection for both MAS core inflation and CPI all items inflation. The inflation outlook for the quarters ahead is subject to both upside and downside risks. STI +0.207% to 4261.82, USDSGD +0.024% to 1.2817, 10y SGB -0.8bp to 1.909%.

U.S. July Chicago Fed National Activity Index is expected to remain negative for the fourth straight month, at -0.11 from -0.10.

U.S. July new home sales forecast to improve to 630k from 627k, with sales up 0.5% m/m.

U.S. August Dallas Fed manufacturing activity is expected to drop to -1.7 from 0.9 in July.

Central bank speakers: Fed’s Lorie Logan speaks at Bank of Mexico Centennial Conference.

U.S. Treasury sells $82bn in 13-week bills and $73bn in 26-week bills.

Mood: iFlow Mood showed signs of a reversal, with equity demand gaining momentum while core sovereign bond buying continues. iFlow Mood is in the risk-off zone but off its lows.

FX: Light flows, but biased toward outflows. IDR, THB, SEK and AUD posted the most outflows, followed by light USD, GBP and CLP selling, against moderate buying in EUR, JPY and CNY.

FI: U.K. gilts and Poland, Colombia, Chile and Peru government bonds were most bought, followed by U.S. Treasurys and Eurozone government bonds. Norwegian, Mexican, Malaysian and Chinese government bonds were sold.

Equities: Mixed but without significant flows. U.K., Europe, Canada, Mexico and Taiwan equities were most sold, against buying for Chile, Sweden and Singapore equities. Within DM EMEA, the consumer staples sector was most sold, against strong demand for the healthcare sector.

“It is a rough road that leads to the heights of greatness.” – Seneca

“Remember, the easy road often becomes hard, and the hard road becomes easy.” – Robert T. Kiyosaki

Sweden’s dwelling starts in the first half of 2025 totaled around 15,400, up 3% from 14,928 a year earlier. Construction of multi-dwelling buildings was roughly 12,100 units, down 1% y/y, with about 71% of them rented. One-dwelling to two-dwelling buildings saw 3,300 starts, a 22% y/y increase. Conversions of multi-dwelling buildings produced 750 dwellings, compared with 928 in the same period of 2024. Adjustments raised 2025 new construction figures by 14% and conversion figures by 20% to account for reporting lags. The data follow 15,217 starts in H1 2023 and reflect a modest rebound in small-scale housing alongside weaker multi-dwelling activity. OMX -0.243% to 2682.819, EURSEK +0.101% to 11.1397, 10y Swedish GB +1.7bp to 2.537%.

Spain’s July industrial price index saw a 0.8% monthly increase, while the annual change dropped by 0.7 percentage points to 0.3%. The y/y industrial price increase was 0.8%. Specific sectors reported mixed m/m results: consumer goods prices increased by 0.1%, equipment goods prices rose by 0.2%, intermediate goods fell by 0.3%, and energy prices surged by 2.9%, marking a 1.5% annual increase in the energy sector. IBEX 35 -0.41% to 15370, EURUSD -0.12% to 1.1704, 10y Bono +3.8bp to 3.339%.

Czechia’s composite confidence indicator for August rose by 1.4 points to 101.1, driven by differing trends across components. Business confidence improved by 2.7 points to 101.5, with notable increases in services (+5.9 points), construction (+1.2 points) and trade (+1.1 points), while industry was unchanged. However, consumer confidence declined, falling by 5.1 points to 99.0. A higher share of consumers expected economic and personal financial deterioration in the coming year, while more households reported worse financial situations compared with the previous year. The intention to make large purchases remained stable. Prague SE +0.157% to 2303.26, EURCZK -0.074% to 24.529, 10y CZGB -1.2bp to 4.294%.

Poland’s July retail sales increased by 4.8% y/y at constant prices, slightly surpassing the 4.4% increase in July 2024. Compared with June, retail sales rose by 4.4%. For the January-July 2025 period, retail sales increased by 3.3% y/y, a slowdown from the 4.9% growth seen in the same period of 2024. When adjusted for seasonal factors, retail sales in July 2025 remained steady compared with June 2025 but showed a 4.4% increase y/y. Significant growth was noted in sectors such as furniture, radio, TV and household appliances (up 15.3%), textiles, clothing and footwear (up 14.7%), and motor vehicles (up 10.7%). However, food, beverages and tobacco products saw a slight decrease of 0.4%. The share of online retail sales grew by 2.5% y/y but declined slightly as a percentage of total retail sales. WIG +0.522% to 108210.6, EURPLN -0.099% to 4.2604, 10y PGB +2.1bp to 5.416%.

In the first half of 2025, non-financial enterprises in Poland saw a 5.0% y/y increase in their gross financial results. Total revenues rose by 2.6%, reaching PLN 2.5692tn, while costs increased by 2.4%. Their gross financial results totaled PLN 122.7bn, up 5.0%, while net profit rose by 4.5% to PLN 136.6bn. Notably, the financial result from sales of products, goods and materials increased by 2.9%, while the result from other operating activities grew by PLN 1.4bn. However, investment outlays decreased by 1.2% y/y, with significant reductions in sectors such as mining and manufacturing. Despite this, construction, information and communication, and transportation saw increased investment.

Türkiye’s confidence indices for August showed mixed results across sectors. The overall confidence index increased by 1.1% in the services sector, reaching 111.1, while retail trade confidence rose by 0.8% to 108.8. In contrast, the construction sector saw a decline of 4.0%, bringing its index down to 85.3. More specifically, services confidence grew due to a 3.4% rise in the “demand-turnover expectations” measure, while retail trade confidence was driven by a 6.3% increase in “business activity-sales expectations”. However, the construction sector experienced a drop in business activity expectations and a significant decrease in the outlook for employment in the sector. BI 100 +0.914% to 11476.26, USDTRY +0.076% to 40.9964, 10y TGB +3bp to 31.38%.

Japan’s June coincident index (CI) was revised to 116.7 from the preliminary 116.8, while the leading index was cut to 105.6 from 106.1 and the lagging index raised to 113.3 from 112.0. The Cabinet Office said the CI indicates that the economy is bottoming out. The three-month moving average for the leading index stood at 104.9, down 0.66 points from May, and its seven-month average at 106.6, down 0.30 points. The coincident index’s three-month average was 116.2, up 0.30 points, while its seven-month average rose 0.22 points to 116.3. The lagging index’s three-month average gained 0.76 points to 113.3, with the seven-month average rising 0.58 points to 111.8. Nikkei +0.409% to 42807.82, USDJPY +0.245% to 147.3, 10y JGB -0.1bp to 1.624%.

Japanese retail sales dropped by 6.2% y/y in July, with a 1.7% decrease in store counts. This followed a trend of lower consumer spending, despite growth in the food and furniture sectors. The data showed a fall across various product categories: clothing and fashion items saw a 10.4% drop, while food sales decreased by 6.5%. Services such as dining and restaurants were also impacted, declining by 12.3%. In particular, food services, including dining, experienced a 2.4% drop, and the trend indicated that these declines have been ongoing for six consecutive months. The report highlighted regional variation, with areas outside Japan’s ten largest cities seeing a smaller drop than major urban centers. The ongoing downturn in sales across multiple sectors points to a broader economic slowdown.

New Zealand Q2 retail sales ex-inflation increased by 0.5% q/q from 0.8% y/y in Q1. Electrical and electronic goods (+4.6% q/q), supermarkets and grocery stores (+1.3% q/q), and pharmaceutical retailing (+1.2% q/q) saw the largest increases this quarter. Eight of the 15 retail industries had higher retail sales volumes in the June 2025 quarter than in the March 2025 quarter, after adjusting for price and seasonal effects. NZX 50 +0.282% to 13079.5, NZDUSD +0.086% to 0.5871, 10y NZGB -1.2bp to 4.37%.

Thailand’s July customs exports came in better than expected at 11.0% y/y from 15.5% y/y in June. Imports grew 5.1% y/y, leaving a trade surplus of $322mn. Thai exports have been resilient at 14.4% y/y YTD but are expected to slowdown from August as front-loading activities fades. Elsewhere, car production in Thailand fell in July for the first time in three months, as tariff uncertainty hurt export demand, while sales extended recent gains, helped by strong growth in electric vehicles. SET +0.736% to 1262.61, USDTHB -0.674% to 32.425, 10y TGN -1.1bp to 1.341%.