Market Movers: Cognitive Dissonance

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 11 minutes

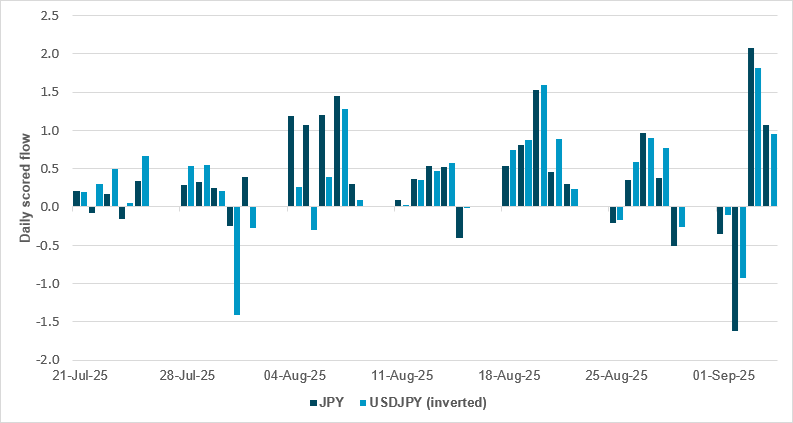

JPY LOOKS OVERBOUGHT HEADING INTO POLITICAL UNCERTAINTY

Source: BNY

Japanese Prime Minister Shigeru Ishiba has resigned, ushering in a period of heightened political uncertainty for the country and its assets. While the next Bank of Japan meeting is still nearly two weeks away, broader drivers such as the U.S. dollar’s trajectory and Federal Reserve policy will likely exert a greater influence on JPY in the near term. Nevertheless, flows since the upper house election in late July highlight underlying vulnerabilities. JPY has seen minimal selling over the past two months, but the past week has witnessed a clear build-up of defensive positions. This suggests that while momentum remains strong, supported in part by previously attractive valuations, the risk of pronounced mean reversion has now increased. Unsurprisingly, the USDJPY flow broadly matches flows in JPY over the same period, but the magnitude is slightly softer, indicating there has been some additional JPY buying on the crosses as carry trades unwind. The last five trading sessions have also generated the first three-day buying streak in USDJPY since the upper house election, just as political uncertainty was starting to pick up. This points to some investors already anticipating a shift in the political outlook. If there is to be any form of mean reversion in JPY, it will have to be USDJPY-generated. If the upcoming Fed decision proves no more dovish than expected, then positioning and flow are clearly aligning for a strong reversal.

Equity markets have rallied despite political worries from France, Argentina and Japan. The uncertainty over fiscal policy has been countered by Fed rate cut expectations. The central question for investors is how bad economic data will drive policy responses. The blackout period for Fed speakers ahead of next week’s meeting has started, meaning Nick Timiraos’s article in the WSJ, suggesting consecutive cuts to the terminal rate with the caveat of inflation surprises, will be widely watched. Also lost in the political headlines overnight were the economic data, where weaker Chinese imports sent the country’s trade surplus back above $100bn and Q2 Japanese GDP was revised up despite the election noise there. In Germany, the trade surplus narrowed even as industrial production jumped into positive territory for the first time in four months. Markets are starting the week in risk-on mood, with global growth hopes returning despite the U.S. jobs report undershooting expectations on Friday. The OPEC+ decision to slow output increases to 137,000 barrels/day has sent oil up 1%, supported by the weaker USD and nascent growth hopes. The day ahead will test whether the “bad news is good” thinking can hold across markets. First, Ukraine returns to the agenda as Russian strikes on Kyiv make any peace efforts harder, with President Trump again meeting EU leaders, then speaking with Vladimir Putin. Second, we are all awaiting the French vote of no-confidence and then the Japanese LDP leadership election on October 4. As for Argentina, the ruling party’s stinging loss to the Peronists in the Buenos Aires provincial election turns the spotlight onto the reform agenda and Milei’s corruption scandal ahead of mid-term voting next month. Politics trumps economics, but growth concerns drive both. This leaves the lack of significant U.S. data this week as a test of cognitive dissonance, where holding long positions for risk across the world linked to politics or policy seems at odds with the future expectations. For those looking to measure the pain ahead, watch USD as JPY, EUR and emerging markets reprice the balance of politics ahead.

France faces heightened political instability, as Prime Minister François Bayrou is expected to be ousted in a confidence vote. This was triggered by his €44bn deficit-cutting fiscal package, which includes plans to eliminate two public holidays, raise taxes on some pensioners and freeze government spending except for defense. Bayrou’s move to call the vote before presenting the 2026 budget sparked opposition backlash amid a fragmented parliament that has lacked a majority since the June 2024 elections. President Emmanuel Macron must now seek a new prime minister capable of navigating a divided legislature, with the Socialist Party’s 66 MPs holding a pivotal role. Macron’s options include forming a fragile coalition or calling early elections, despite his unpopularity and the far-right’s growing strength. The government aims to reduce the deficit to 5.4% of GDP in 2025 and meet the EU’s 3% limit by 2029, but fiscal compromises appear inevitable amid deep political divisions. CAC40 +0.158% to 7686.92, EURUSD +0.111% to 1.173, 10y OAT -0.9bp to 3.439%.

The EU is considering new sanctions targeting around six Russian banks and energy companies as part of its 19th sanctions package since Russia’s invasion of Ukraine. The measures may also include restrictions on Russia’s payment and credit card systems and its crypto exchanges, plus further limitations on its oil trade. Coordination with the U.S. is planned, with EU officials set to meet their U.S. counterparts to discuss joint actions. The package could extend sanctions on Russia’s shadow fleet and oil traders in third countries, and potentially ban re-insurance of listed tankers. Additional export bans on goods and chemicals used by Russia’s military, as well as trade restrictions on foreign suppliers, particularly from China, are also under consideration. The EU may deploy its anti-circumvention tool against Kazakhstan to prevent diversion of military-related machinery to Russia. Further measures could include visa restrictions and sanctions on ports and military-related services. Euro Stoxx 50 +0.388% to 5338.78, EURUSD +0.111% to 1.173, BBG AGG Euro Government High Grade EUR -2.7bp to 2.911%.

German exports reached €130.2bn in July, down 0.6% m/m (consensus: +0.1% m/m) but up 1.4% y/y, while imports totaled €115.4bn, down 0.1% m/m and up 4.3% y/y. This resulted in a seasonally adjusted trade surplus of €14.7bn, lower than June’s €15.4bn and July 2024’s €17.7bn. Exports to EU countries increased by 2.5% m/m to €74.8bn, with imports up 1.1% to €60.3bn. Exports to non-EU countries fell 4.5% m/m to €55.3bn, and imports shrank by 1.3% to €55.1bn. Exports to the U.S. dropped 7.9% m/m to €11.1bn, marking the fourth consecutive monthly decline and a 14.1% y/y fall. Imports from China, the largest source, fell 2.4% m/m to €14.3bn. The trade balance remained positive but contracted slightly. DAX +0.609% to 23740.71, EURUSD +0.111% to 1.173, 10y Bund -0.8bp to 2.654%.

Japanese Prime Minister Shigeru Ishiba has resigned following a series of election losses that eroded his ruling coalition’s parliamentary majorities, amid voter dissatisfaction over rising living costs. Having been in power for less than a year, Ishiba delayed stepping down until he had finalized a trade deal with the U.S. aimed at reducing tariffs. His resignation has raised concerns about policy uncertainty, triggering a sell-off in the yen and government bonds, with 30y bond yields reaching record highs. Potential successors include fiscal dove Sanae Takaichi, who advocates looser fiscal and monetary policies, and Shinjiro Koizumi, seen as less likely to enact major changes. The ruling Liberal Democratic Party plans an emergency leadership election, though the next leader may face a snap general election to secure a mandate amid a fragmented opposition and rising influence of the far-right Sanseito party. Nikkei +1.453% to 43643.81, USDJPY +0.129% to 147.62, 10y JGB -0.9bp to 1.571%.

French National Assembly to hold confidence vote in Prime Minister François Bayrou – process begins 15:00 CEST/09:00 ET.

U.S. New York Federal Reserve consumer 1y inflation expectations expected up 3.15% from 3.09%.

U.S. Treasury sells $82bn in 13-week bills and $73bn in 26-week bills.

Mood: iFlow Mood continues to normalize, with an acceleration in equity buying momentum along with steady core sovereign bond demand.

FX: Notable flows included significant ILS outflows and HUF inflows. Currency flows were mixed in the G10 and APAC, against better selling in LatAm and buying in EMEA. USD and EUR were lightly sold, against small inflows in GBP and JPY. Elsewhere, ZAR, AUD, CZK, INR and KRW posted moderate inflows.

FI: Good demand for U.S. Treasurys, U.K. gilts and Eurozone government bonds, against selling in Polish, Singapore, Mexican, Japanese and Danish government bonds.

Equities: Eurozone and Colombian equities were most sold, followed by U.K., Japanese, Canadian and U.S. equities. There was notable demand for Brazilian, Peruvian, Singapore and South Korean equities. Within DM EMEA, the health care sector was most bought, against selling in the materials and industrial sectors.

“Wisdom is the tolerance of cognitive dissonance.” – Robert Thurman

“We have a habit of distorting the facts until they become bearable to our own views.” – Charlie Munger

The Eurozone’s Sentix Economic Index declined sharply by 5.5 points to -9.2 in September, reflecting a significant deterioration in both current conditions and future expectations. This takes sentiment to its lowest level since March. Germany’s index fell 9.4 points to -22.1, indicating a continued downward trend with no signs of recovery in Europe’s largest economy. The U.S. also showed clear signs of slowdown, with expectations dropping to -10.8 points and the current situation eroding to -0.3 points. In contrast, the Asia region, including Japan, remained comparatively robust, serving as a stabilizing factor that is helping to maintain the global economic growth momentum despite widespread concerns in Western economies. Euro Stoxx 50 +0.388% to 5338.78, EURUSD +0.111% to 1.173, BBG AGG Euro Government High Grade EUR -2.7bp to 2.911%.

Germany’s industrial production rose by a seasonally and calendar-adjusted 1.3% m/m in July, following a revised 0.1% decline in June. Compared with July of the previous year, production increased by 1.5% on a calendar-adjusted basis. The growth was primarily driven by a 9.5% m/m surge in machinery manufacturing, alongside gains in the automotive (+2.3%) and pharmaceutical (+8.4%) sectors, while energy production fell by 4.5%. Excluding energy and construction, industrial output rose 2.2% m/m, with investment goods up 3.0%, consumer goods up 2.1% and intermediate goods up 0.8%. Construction output increased by 0.3%. Energy-intensive industries saw a modest 0.4% m/m rise but remained 4.8% lower y/y, with a 2.6% q/q decline in the three-month period from May to July. DAX +0.609% to 23740.71, EURUSD +0.111% to 1.173, 10y Bund -0.8bp to 2.654%.

The latest KPMG and REC, U.K. Report on Jobs: London survey noted that the downturn in hiring activity continued into August, with both permanent placements and temporary billings falling further. Permanent placements fell for a fifth successive month, although the rate of reduction reached a four-month high, outperforming the national average. Meanwhile, temp billings dropped for a 20th month in a row, but at the softest pace in three months. Demand weakened, with permanent vacancies shrinking at the sharpest rate since October 2020 and temp vacancies contracting for a twelfth consecutive month. Candidate availability surged, driven by redundancies, with permanent staff supply rising at the fastest pace in over two years and temp supply recording the sharpest increase since December 2020. Permanent salary growth remained subdued, while temp pay rose for an 11th month, at the strongest rate in two years. FTSE 100 +0.171% to 9223.98, GBPUSD +0.015% to 1.3511, 10y gilt 0bp to 4.646%.

Sweden’s SEB Housing Price Indicator declined by six points to 29 in September, from 35 in August, falling below the historic average and marking the weakest reading since early 2024. The decline was primarily driven by a reduced percentage of respondents expecting higher home prices, while the proportion anticipating unchanged prices has increased since mid-2024, mirroring recent actual price trends. The percentage expecting price declines has remained largely stable since summer 2024, with a slight rise since spring. Mäklarstatistik data for August indicate home prices are up 1% YTD, but seasonally adjusted prices show a near 2% decrease. Despite cautious household behavior, record-high supply of existing homes persists, with turnover normalizing but remaining low. The supply of apartments has risen steadily, with recent months showing a lower sales/available apartments ratio than the May peak, suggesting turnover may now be influencing supply levels. OMX +0.035% to 2627.571, EURSEK +0.076% to 11.01, 10y Swedish GB -2.5bp to 2.554%.

Czechia’s trade balance of goods in July registered a deficit of CZK 1.7bn, improving by CZK 5.5bn y/y. The overall trade balance benefited from higher surpluses for motor vehicles (up CZK 5.1bn), other transport equipment (up CZK 3.0bn) and machinery and equipment (up CZK 2.3bn). Conversely, the deficit widened due to a reversal in fabricated metal products (down CZK 5.2bn) and larger deficits in agricultural products and basic metals of CZK 1.2bn and CZK 1.0bn, respectively. The positive trade balance with EU countries grew by CZK 2.4bn y/y, while the deficit with non-EU countries narrowed by CZK 6.5bn. Exports rose 4.7% y/y to CZK 375.2bn and imports increased 3.1% to CZK 376.9bn, though seasonally adjusted exports and imports fell by 4.2% and 3.8% m/m. Year to date, the trade surplus stands at CZK 136.7bn, down CZK 9.4bn y/y. Prague SE +0.042% to 2285.6, EURCZK +0.058% to 24.402, 10y CZGB -0.3bp to 4.367%.

The Czech labor market saw nominal average wage growth of 7.8% y/y and real wage growth of 5.3% in Q2 2025, with economic activity and female employment in particular rising. Total employment increased by 1.5% y/y to 5.243.5 million, driven mainly by a 52.2k rise in workers aged 60+, particularly women. Employment growth was concentrated in the tertiary sector, which added 88k jobs, especially in arts, entertainment and recreation (+24.3%). The employment rate for ages 15-64 rose by 0.4 percentage points to 75.7%, with female employment increasing by 1.9 percentage points to 71.2%. Unemployment increased slightly to 2.8%, with 146.1k job seekers, including a rise in long-term unemployed. Registered full-time equivalent employees grew by 0.4% y/y, with sectoral shifts showing declines in manufacturing and mining but gains in health, education and real estate.

Japan’s Economic Watchers survey for August showed the current conditions diffusion index (DI) rising by 1.5 points m/m to 46.7 (seasonally adjusted). This was driven by increases in household-related DI, notably in dining and related sectors, despite a decline in housing. The corporate-related DI also increased due to gains in the non-manufacturing sector, while the employment-related DI decreased. The leading conditions DI edged up by 0.2 points m/m to 47.5, supported by rises in household and corporate DIs, although employment DI fell. Unadjusted data showed the current conditions DI increasing by 0.8 points to 46.3, while the leading conditions DI decreased by 0.3 points to 46.7. The overall assessment indicated a recovery trend in the economy, with cautious optimism for the future despite concerns over price rises and U.S. trade policy. Nikkei +1.453% to 43643.81, USDJPY +0.129% to 147.62, 10y JGB -0.9bp to 1.571%.

Japan Q2 final GDP came in better than expected at 0.5% q/q, 2.2% y/y against a flash estimate of 0.3% q/q, 1.0% y/y (Q1 2025: 0.1% q/q, 0.3% y/y). Q2 private consumption was revised up to 0.4% q/q (flash: 0.2%), while business spending was revised down to 0.6% q/q (flash: 1.3% q/q). Elsewhere, Japan August bank lending grew by 3.6% y/y including trusts, or by 3.9% y/y excluding trusts, from 3.2% y/y, 3.5% y/y in July. The country also registered a current account surplus of ¥2.68tn in July (consensus: ¥3.35tn), according to data released by the Ministry of Finance. The trade deficit came in at ¥189.4bn, partially reversing June’s ¥469.6bn surplus.

China’s August exports came in lower than expected at 4.4% y/y, from 7.2% y/y in July. Imports slowed from 4.1% y/y to 1.3% y/y, producing a trade balance of $102.33bn. YTD export growth is 5.9% y/y (July: 6.1%), while imports are down -2.2% (July -2.7%). By destination, exports to the U.S. decreased further to -33.1% y/y (-15.5% YTD y/y), followed by -16.6% y/y (-9.7% YTD y/y) to Russia and -1.3% y/y (-1.2% YTD y/y) to South Korea. Exports to ASEAN grew strongly, up 22.8% y/y (22.1% YTD y/y), their best figure since 25% y/y in May 2024. They were followed by 17.8% y/y to Hong Kong, 10.4% y/y to the EU and 6.9% y/y to Japan. China’s trade surplus with the U.S. narrowed to $20.3bn in August, while the trade surplus with the EU went to $28.86bn. The trade surpluses with ASEAN and Hong Kong were $24.3bn and $23bn, respectively. CSI 300 +0.162% to 4467.57, USDCNY -0.021% to 7.1313, 10y CGB +1.1bp to 1.787%.