Gold fortunes begin to diverge

iFlow > FX: G10 & EM

Published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

iFlow > FX: G10 & EM

Published every Thursday, provides a detailed analysis of global foreign exchange movements in major and emerging economies around the world together with macro insights.

Geoff Yu

Time to Read: 5 minutes

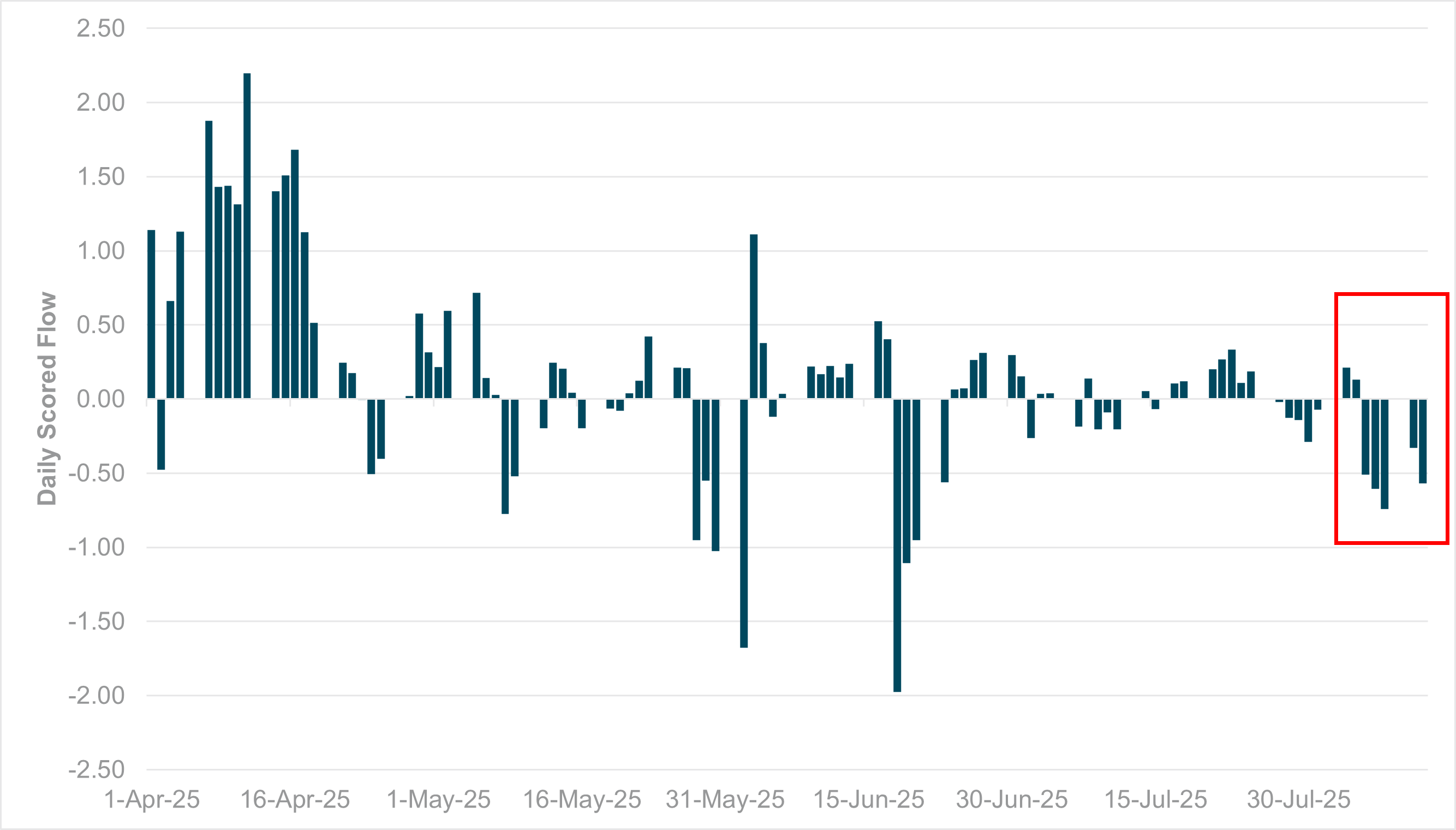

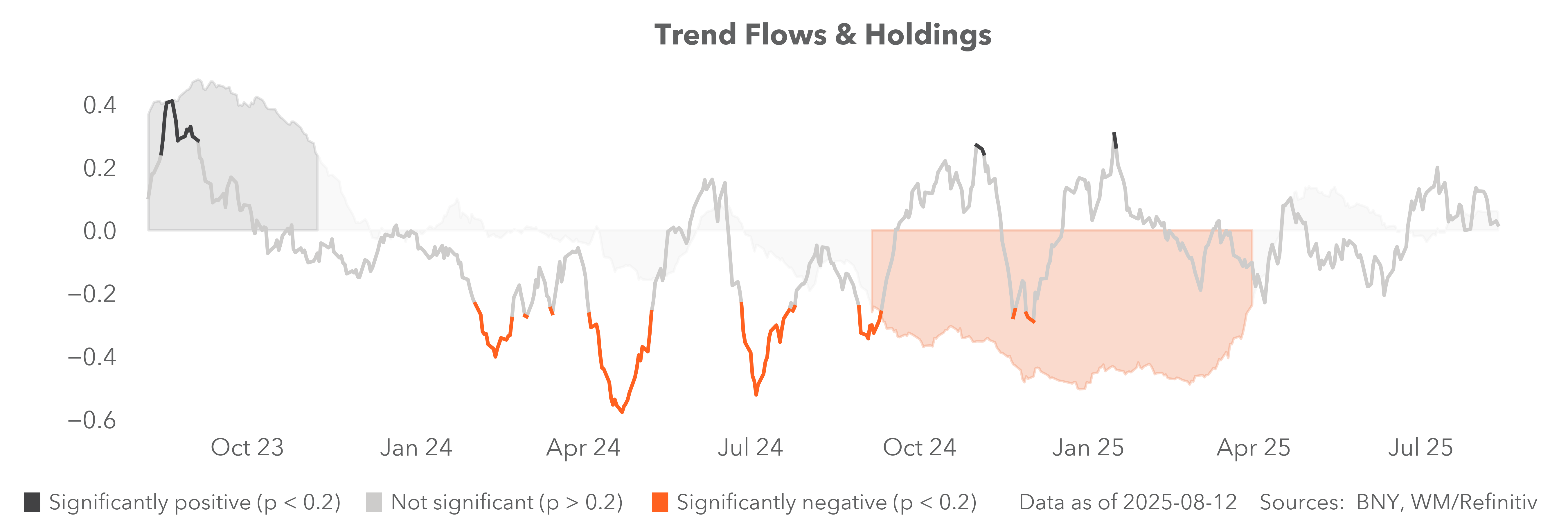

EXHIBIT #1: SCORED DAILY FLOWS IN CHF

Source: BNY, Macrobond

Our take

For much of H1, we held the view that the Swiss franc was one of the best “minor” destinations for diversification away from dollar exposures. In the immediate aftermath of the original “Liberation Day” tariffs, we can see that the franc enjoyed its best period of inflows this year. We believe that this was largely driven by international investors removing their hedges on Swiss assets, hoping to capture outright currency gains during flight to safety. However, these flows were predicated on the attributes which qualified the franc for safety status in the first place – namely strong balance of payments, particularly anchored by a large trade surplus. However, Switzerland’s surpluses have long been concentrated in a handful of sectors, and we highlighted that any form of tariffs which would jeopardize Switzerland’s pharmaceutical industry would justify a change in views, even de-rating. As things stand, the trade situation for the country has exceeded worst-case scenarios, and flows are starting to shift (Exhibit #1) as the implications of the 39% headline rate and sectoral tariffs on refined gold and pharmaceuticals sink in.

Forward look

Before the tariff shock on August 1, despite spot levels moving toward new lows, in real terms we did not view the franc as strongly overvalued. Years of favorable inflation differentials had kept down the franc’s value in real terms, and the SNB’s surprising optimism regarding the inflation outlook – validated by the July price growth prints – also provided a rate buffer. We don’t see the SNB taking a firm view on policy until the last possible moment as a deal with a tariff ceiling across all sectors will make a huge difference to the Swiss economic outlook, but the lack of dialogue between Bern and key officials in D.C. has clearly perturbed markets at the prospect of any progress being made in the coming month. Switzerland’s economy remains diverse and dynamic enough to weather such structural shocks and there are other sources of balance of payments strength, such as a strong financial account. Nonetheless, precautionary flows will likely dominate for now and we expect a flattening out of CHF’s flow averages in the near term.

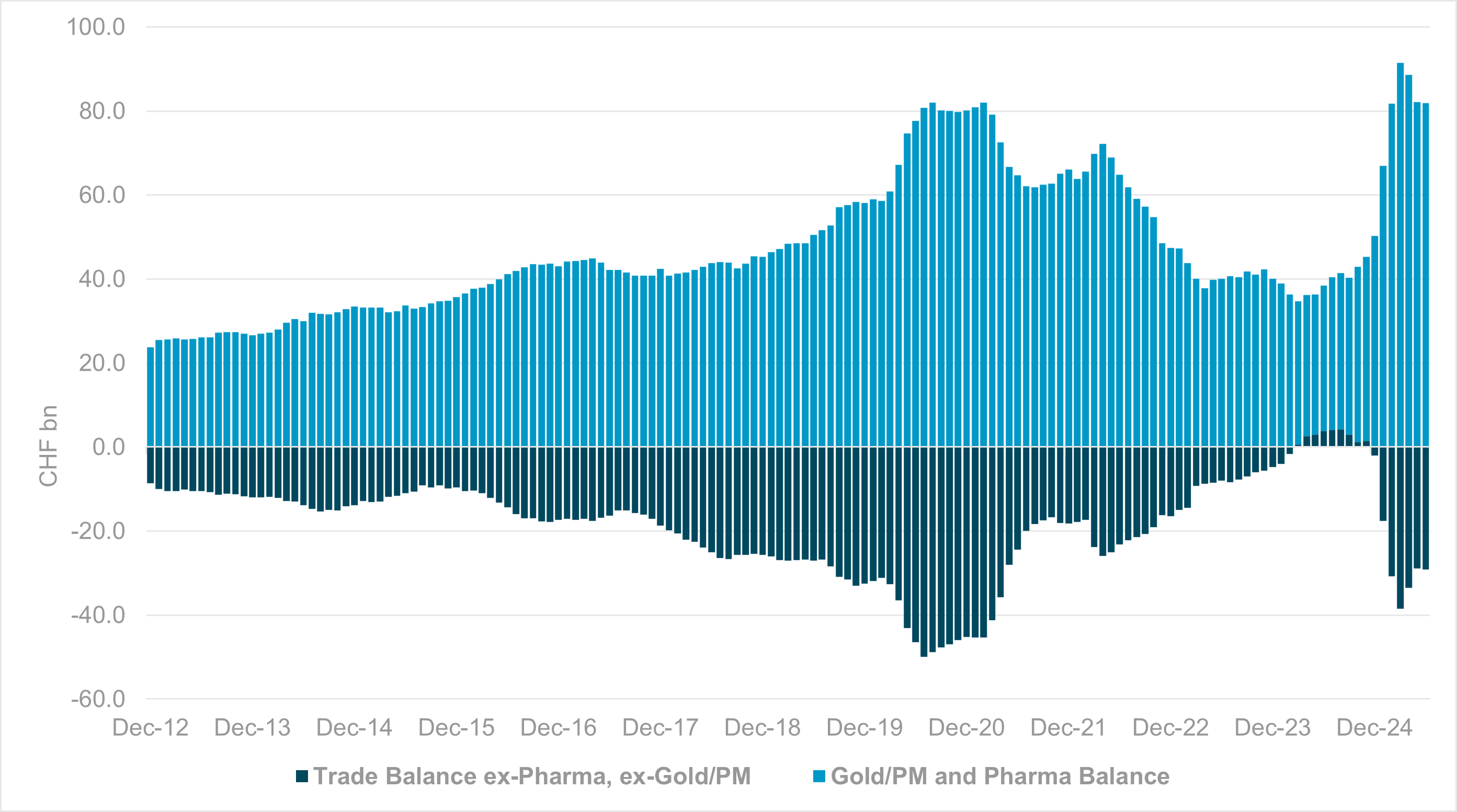

EXHIBIT #2: ROLLING 12-MONTH CUMULATIVE SWISS TRADE SURPLUS, DECOMPOSED

Source: BNY, Bloomberg

Our take

We have long highlighted the risk of the franc facing de-rating should pharmaceutical exports to the U.S. fall significantly, and the sudden risks arising from refined gold bullion exports has only compounded the risks. President Trump’s quip this week that “gold will not be tariffed” is not sufficient as the market is seeking clarity on the specific types of refined gold bullion which will be subject to duties – and the Swiss State Secretariat for Economic Affairs believes that the country accounts for at least one-third of global refined gold. Exhibit #2 shows that without gold/precious metal and pharmaceutical surpluses, Switzerland’s trade deficit would currently be running at around CHF 30bn. There has been some front-loading of these exports ahead of tariffs, while bullion demand earlier this year also surged due to idiosyncratic factors, but ultimately these flows matter for currency valuations. Furthermore, given the structural changes necessary to maintain U.S. market access, there is no guarantee that simple currency depreciation can compensate for lost market share. This is particularly the case for pharmaceuticals, where the Trump administration is outright seeking lower costs and re-shoring of production back to the U.S.

Forward look

On balance, we expect the Swiss government and SNB to be far more focused on the risks from pharmaceutical tariffs. Although they are currently exempt, the level of peak tariffs suggested by President Trump (up to 250%) is prohibitively high and would incentivize significant offshoring of one the most value-added employers for the Swiss economy. Considering the broader growth and revenue implications due to multiplier effects, significant de-rating of the economy is possible, though domestic observers note that this also represents an opportunity to rethink Switzerland’s economy, including its economic relationship with the European Union. All of this is well beyond the remit of the SNB, but if there is no negotiated settlement over the next month, we expect the SNB to put all options on the table.

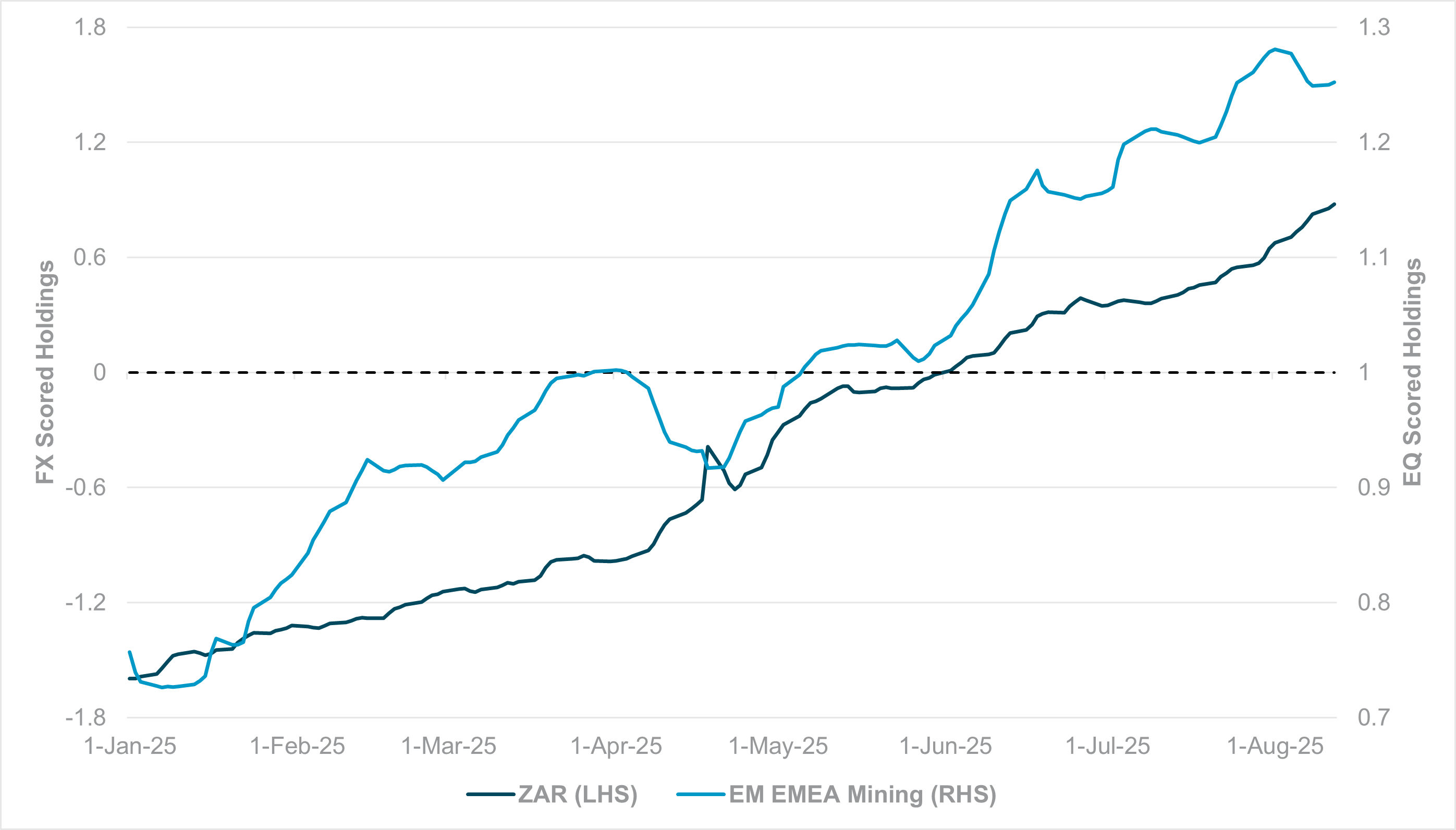

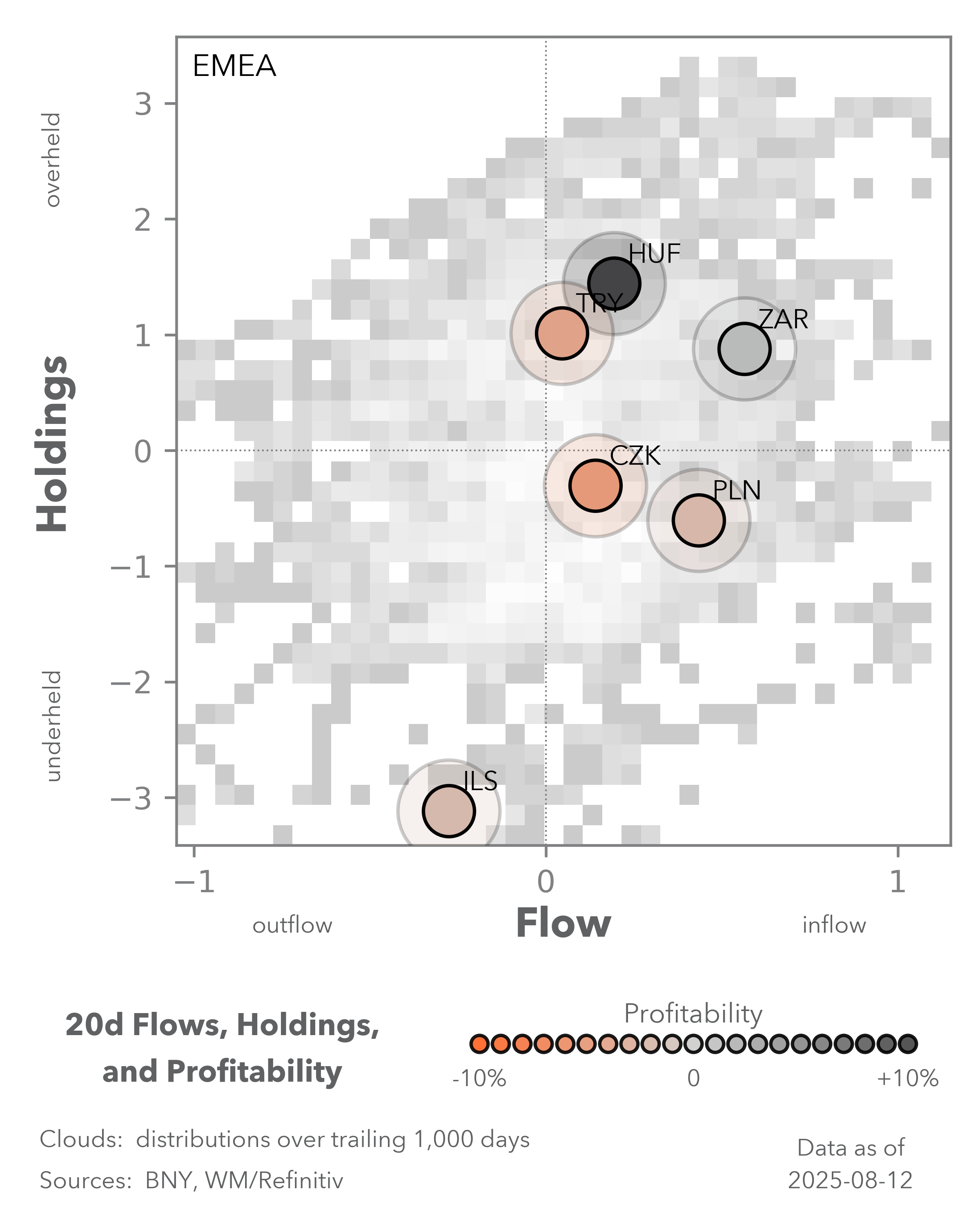

EXHIBIT #3: ZAR AND EM METALS AND MINING EQUITY HOLDINGS

Source: BNY, Macrobond

Our take

As soon as the CBP clarifies the tariff situation with bullion, gold prices and transatlantic price spreads can settle at the requisite levels. While Switzerland will need to reassess its refining capabilities, underlying producers are unlikely to adjust their demand projections, or the corresponding impact on their own terms of trade. In recent weeks, significant price volatility has materialized in various industrial metals relating to policy adjustments in the U.S. and China, such as copper and iron ore. However, gold’s anchoring demand from central banks and private-sector investors remains in place, especially in an environment where real rates are likely to decline. ZAR is one of the biggest beneficiaries, as terms of trade have complemented strong domestic real rate credibility, notwithstanding recurring domestic political uncertainty and the impact of U.S. tariffs.

Forward look

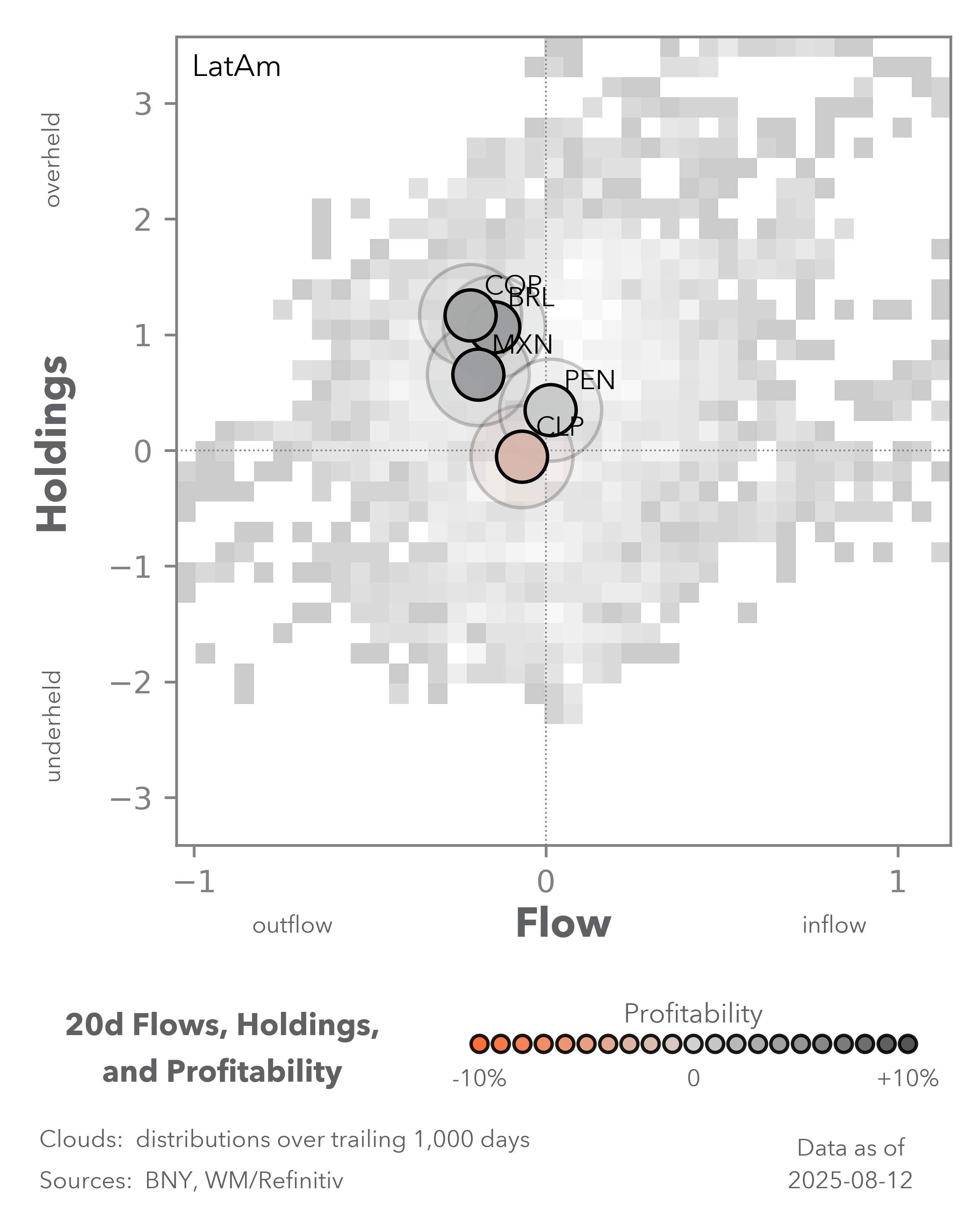

Our data show that ZAR has been a rare case of an EM commodity currency moving from materially underheld at the beginning of the year to comfortably overheld (Exhibit #3). Currently, along with HUF and TRY, high-yielders in EMEA are looking far more resilient than carry stalwarts in Latin America. Furthermore, we note that this is taking place amid even stronger total return exposure in underlying equities. Currently, EM EMEA’s metals and mining industry equities are close to 30% above the rolling 12-month average in holdings, having started the year 10% below the same benchmark. This is one of the strongest industry-level performances across EM. Given South Africa is the only economy with a sufficiently large metals and mining industry, we believe the bulk of the gains are aligned with flows into the South African market. Furthermore, the level of FX interest also indicates that hedge ratios are very contained and investors are comfortable with total return exposure. South Africa will have strong growth exposure to China akin to Chile and Australia, but the nature of gold demand at present is a likely core flow driver for ZAR exposures.

For now, we believe it’s best to characterize franc performance in terms of opportunity cost. If a trade deal along the lines of the EU had been reached, especially with tariff ceilings for key exports, then the franc would have likely resumed its status as a favored diversification play. Now, it is somewhat caught in a limbo, along with SNB policy. Consequently, the number of destinations for dollar diversification has shrunk even further, and gold is now caught up in the process. Unlike the franc, markets are giving commodity exposures in equities and FX the benefit of doubt, but the situation will remain volatile. The past few weeks have shown that no asset is immune to tariff gyrations and risks should be managed accordingly.