End of Summer

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Start of the Week previews activities across global financial markets, providing useful charts, links, data and a calendar of key events to help with more informed asset allocation and trading decisions.

Bob Savage

Time to Read: 13 minutes

The last week of August delivered a weaker USD, a higher stock market, and a flat bond market despite heavy note and bill supply. Expectations for a Federal Reserve rate cut in September remained a key driver. Economic data were mixed, and uncertainty about fiscal and monetary policy remains high. Nvidia earnings, the core PCE price index, and the ongoing threat of further Trump policy shifts dominated the news. The two standout market movers were the rise in French bond yields, which matched Italy’s as political risks grew, and the growing role of gold in central bank reserves, where holdings of the precious metal beat U.S. bonds for the first time in 30 years. The week provided three key themes: complacency vs. uncertainty, political risks vs. easy policy, and inflation vs. jobs.

Rising risks for summer trend reversals — low volatility, higher uncertainty

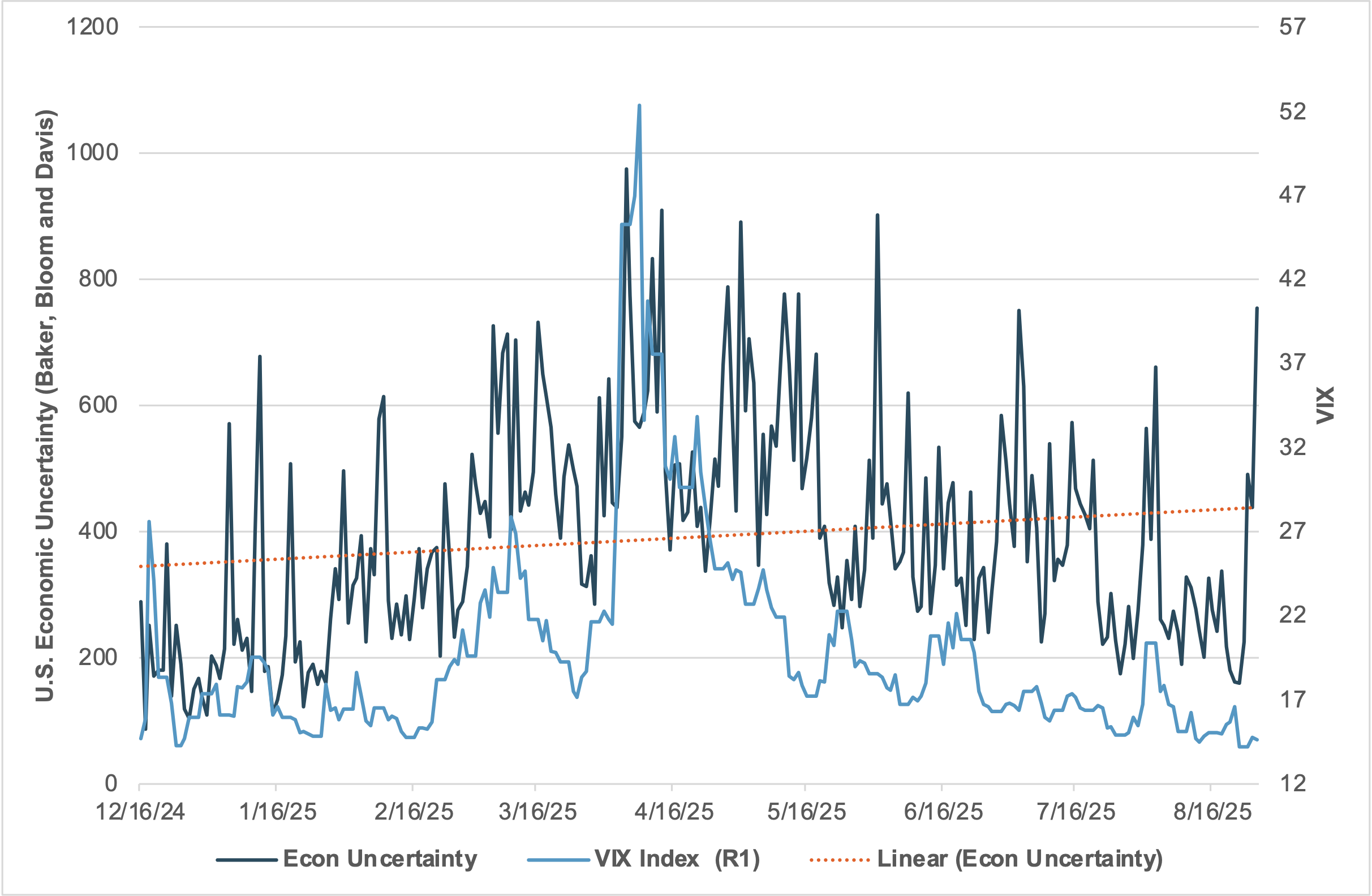

EXHIBIT #1: U.S. ECONOMIC UNCERTAINTY VS. VIX INDEX

Source: BNY, Bloomberg

Our take: Markets learned something over the summer: Noise around Trump’s policy shifts matters less than the FOMC’s response. Key to trading risk this summer was the certainty that Q2 earnings beats would lift U.S. equities to historic highs. In the post-earnings period, weaker U.S. data supported hopes for a Fed rate cut, hopes reinforced by Chair Powell’s comments at Jackson Hole. As Exhibit #1 shows, fears about economic uncertainty in 2025 are declining. Tariff policy shifts appear mostly complete, while pressure on the FOMC and ongoing deregulation efforts support growth, despite lingering doubts about economic outcomes.

Forward look: Beyond U.S. economic data, market risk centers on the upcoming French no-confidence vote, the return of the U.S. Congress with pressure to pass either a budget or continuing resolution, and the Bank of Japan rate decision. Other factors include ongoing tariff negotiations, peace-talk hopes, and key economic data from EMEA and APAC in the week ahead. The biggest risk is that volatility and market positioning are too complacent in the face of rising uncertainty. The long-term average for economic uncertainty is 100, but the current trend is above 400. The cost of uncertainty will eventually show up in the real economy and in markets, with the end of summer a potential turning point.

U.S. Labor markets and ISM set tone for Fed-easing expectations

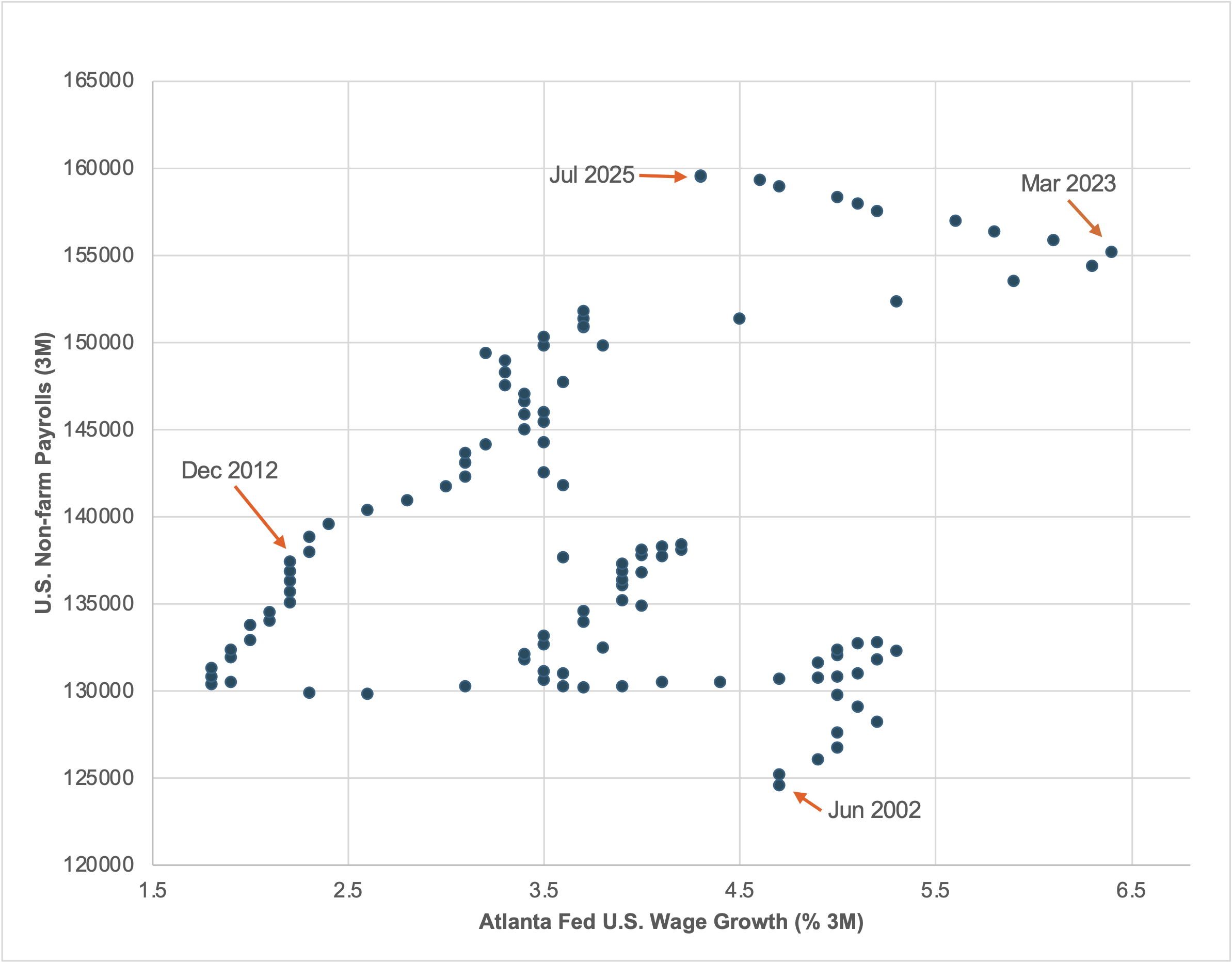

EXHIBIT #2: U.S. WAGE GROWTH VS. JOB GROWTH

Source: BNY, Bloomberg

Our take: The U.S. Labor Day holiday will not calm the week ahead. Markets are nervous about the risks to U.S. growth and unemployment. Expectations for the Sept. 5 jobs report have consensus forecasting 75,000 private jobs, with the unemployment rate rising to 4.3%. More important for hopes of a Fed rate cut, wage growth is expected to slow to 3.7% from 3.9% in July. The relationship between job growth and wages has a long history. Tight labor markets can drive up wages, and, indirectly, inflation, while weak job growth has the opposite effect. The composition trap is that sudden job losses can spike average hourly earnings, as seen in 2020 during the COVID-19 pandemic. As highlighted in Exhibit #2, the 2000 and 2008 recessions had significant market impacts. Nonfarm payrolls (NFP) falling below 80,000 (the replacement rate under the new birth/death model) is a distress signal, making Friday’s report critical to market growth expectations.

Forward look: The ISM manufacturing and services reports next week will be critical as well. Their focus on prices paid and received will help measure margin pressures, and both reports will be released ahead of the labor report. The Job Openings and Labor Turnover Survey (JOLTS) will also draw attention, given hopes for a balanced labor market and the “no hire, no fire” narrative of the summer. The anecdotal Beige Book for the upcoming Fed meeting will also be important, as it offers insights on jobs, inflation and mood. A weaker-than-expected jobs report could prompt calls for more than 25bp of easing. This prospect makes wage data critical to inflation risks and places additional importance on the ISM reports in shaping the outlook. The potential for large data revisions could also fuel significant volatility.

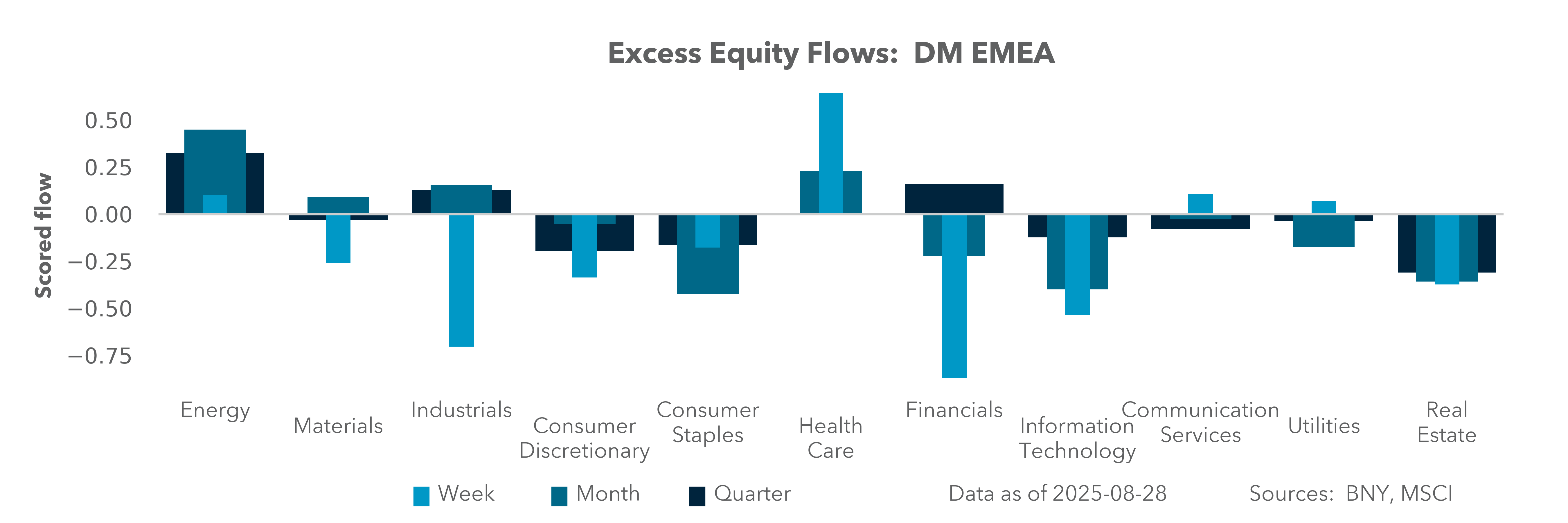

EMEA – European CPI, PMI, NBP decision

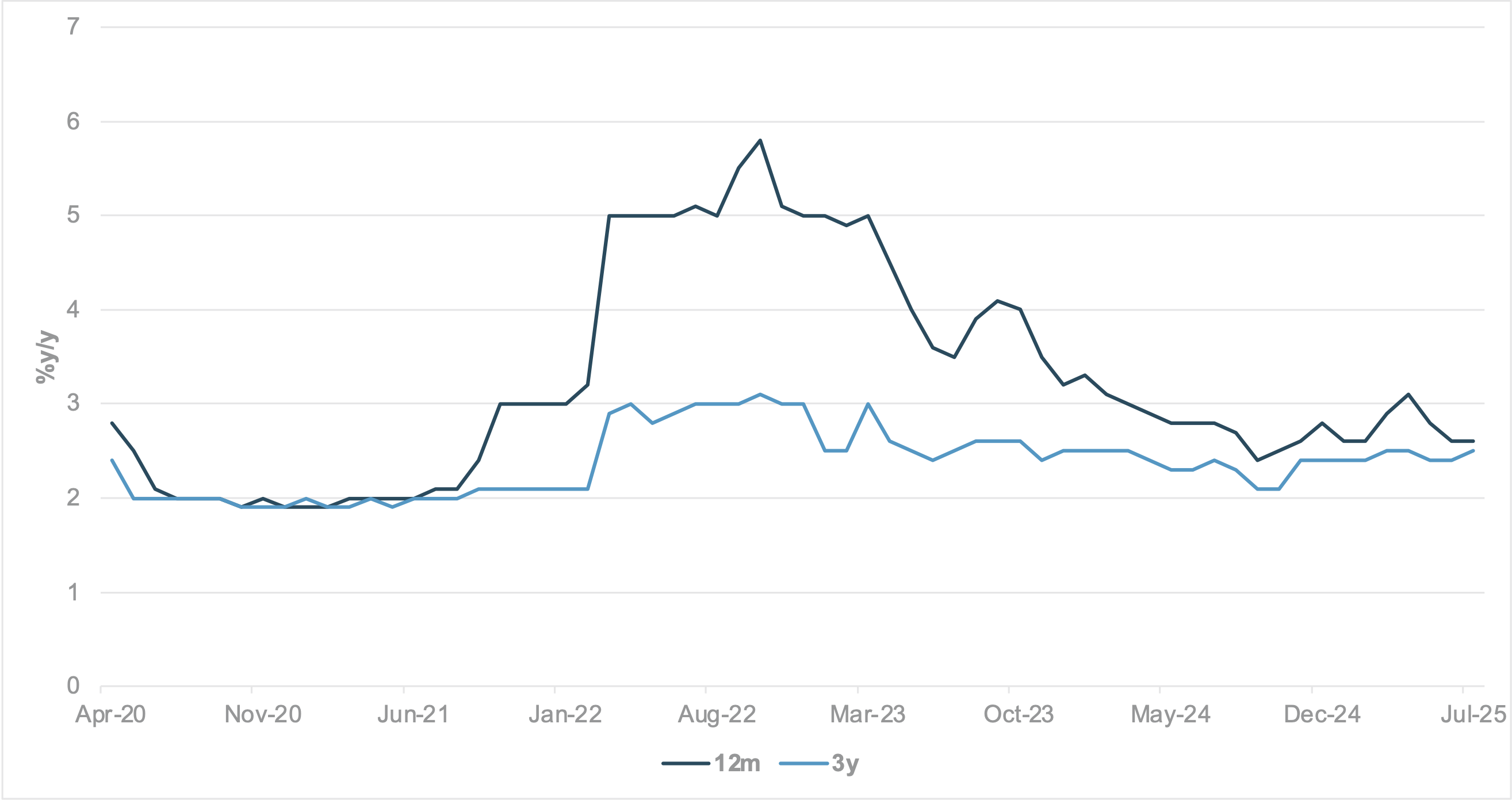

EXHIBIT #3: ECB INFLATION EXPECTATIONS OVER THE NEXT 12M AND 3Y

Source: BNY

Our take: August inflation figures are not sufficient to justify a cut in September, and upside surprises in regional German prints validated Bundesbank President Joachim Nagel’s statement at Jackson Hole that the “bar is high” for another rate reduction. Meanwhile, the ECB’s latest survey results indicate that policymakers are not making much headway in anchoring inflation expectations (Exhibit #3), with both one- and three-year inflation expectations still running above the target rate. We acknowledge that recent soft data, including the Independent Fiscal Office report and the PMI readings, indicate improving trends in output, even though headline indicators remain in contraction territory. The industry appears to be cautiously optimistic about trade relations with the U.S., which may explain why the European Commission is accelerating efforts to formalize sections of their trade agreement. The latest reports point to EU moves to slash U.S. industrial tariffs in exchange for relief for auto manufacturers, which have been “bleeding a lot of cash” in recent months, according to EU Trade Commissioner Maroš Šefčovič. iFlow indicates that equity holdings for automakers and luxury goods, two underperforming European anchor industries, have started to diverge in favor of the former. The recent mixed round of earnings reports from Chinese carmakers and a shift in Beijing’s industrial policy toward margin over price may have created an opening for European automotive growth, valuations are starting to look more attractive. However, risk remains high for other segments, especially pharmaceutical exports to the U.S., where the 15% tariff cap under the EU-U.S. deal needs to be formalized. Although the lack of a U.S.-Switzerland trade deal is dominating proceedings, the EU’s pharmaceutical exports to the U.S. exceed those from Switzerland, and the bloc will face similar current account pressures without a proper settlement.

Forward look: With national CPIs being released over the coming sessions, Eurozone CPI is expected to soften slightly to 2.2% y/y from 2.3% y/y previously, and the Q2 Eurozone GDP is expected to be confirmed at 1.4%. Final PMIs are also due across the continent, with most composite figures expected to be confirmed at barely above the 50.0 level. Otherwise, the bulk of the attention will be on French political developments, as Premier François Bayrou attempts to keep his government in place ahead of the Sept. 8 confidence vote. Our data continue to indicate very elevated flows into OATs, which could correct sharply if adverse scenarios such as fresh parliamentary elections materialize, even more so than during similar episodes in H2 2024. Meanwhile, the NBP decision is expected to indicate another rate cut in Poland, as inflation moves toward contraction on a monthly basis. There is clear capacity to cut rates, but we would be vigilant regarding increased hedging flow in Poland and CEE, as assets in the region are among the most overheld in iFlow. PLN and HUF are anchor currencies in the carry trade due to favorable real rates, while Polish equities are tracking the performance of European defense stocks, indicating a strong geopolitical theme that supports [CF1] rerating. We expect these assets to continue performing well, but total return profiles look excessive.

APAC: Regional growth, inflation and Japan earnings in focus

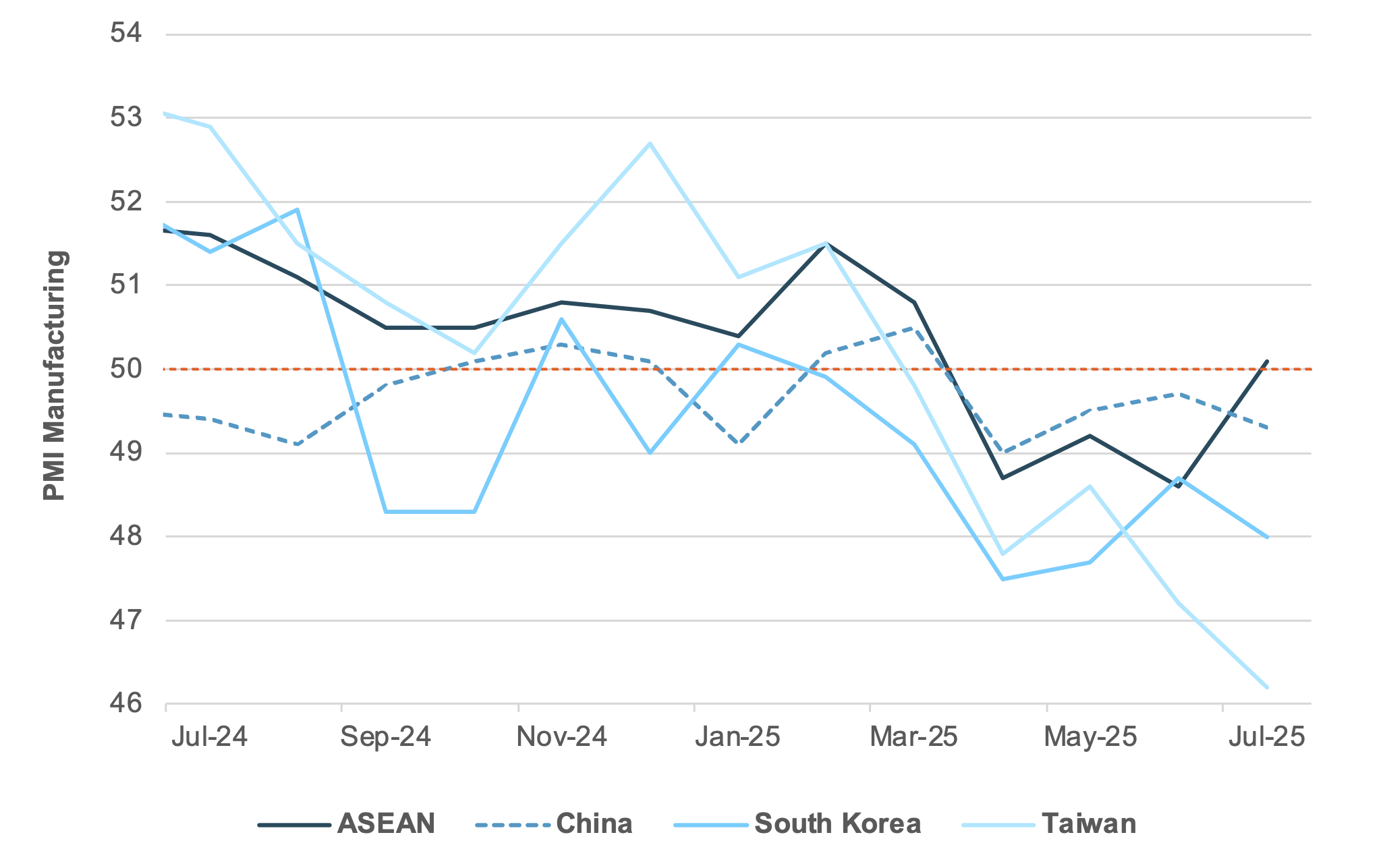

EXHIBIT #4: DIVERGENCE BETWEEN PMI IN NORTH ASIA AND ASEAN

Source: BNY, Bloomberg

Our take: In APAC, this week’s focus is on August PMI data, regional inflation, Japan’s labor cash earnings and household spending, export figures from South Korea, Indonesia and Australia, and regional reserves data. Regional PMI will be closely monitored this week, especially in China, Taiwan and South Korea. China’s business sentiment remains sluggish, with July PMI manufacturing in contraction at 49.3 and non-manufacturing dipping to 50.01, the lowest since November 2024, despite strong domestic confidence in the equity complex. We will be closely monitoring three key subcomponents: new orders at 49.4, new export orders at 47.1, and imports at 47.8, which are all in contraction. Surging Taiwanese semiconductor exports and the positive trade agreement between South Korea and the U.S. have yet to be reflected in business sentiment. Taiwan’s July PMI is at 46.2, its weakest since August 2023, and South Korea’s eased to 48.0 from 48.7 in June. In contrast, sentiment in ASEAN posted a strong rebound into expansion, led by strength in Thailand, Vietnam, Malaysia, Indonesia and Singapore. Lastly, India’s sentiment accelerated to recent highs in August, with manufacturing PMI at 59.8 and services PMI at 65.6. The September reading will be closely watched for any potential negative impact from U.S. tariffs.

This week also brings inflation releases from South Korea, Taiwan, Thailand, the Philippines, and Indonesia. Regional headline inflation has been on a downward trend this year, driven mainly by food and transportation components, while core inflation has gone the opposite direction, drifting higher over the past few months. In the near term, low headline inflation continues to provide a necessary argument for monetary policy easing, depending on the growth momentum into H2 2025 after front-loaded strength in the first half.

Elsewhere, Japan’s July labor cash earnings and household spending will be closely watched. Ongoing upward momentum and elevated inflationary pressure continue to support tighter BoJ policy rates. Australia’s Q2 GDP and July household spending would be crucial in shaping RBA-rate expectations, especially following the spike in monthly July inflation to 2.8% y/y (June: 1.9%), with the trimmed mean at 2.7% y/y (June: 2.1% y/y).

On the monetary policy front, Bank Negara Malaysia (BNM) will convene this week. We expect BNM will hold rates at 2.75% after a pre-emptive cut in July.

Forward look: Two key events in China this week are the Shanghai Cooperation Organization summit in Tianjin and the “Victory Day” military parade on Sept. 3, which will be attended by leaders from Russia, North Korea and Iran. The DXY will probably stay range-bound ahead of Friday’s U.S. data. In the meantime, domestic relative value and differentiation will be in play. Renewed fiscal loosening in South Korea, with government spending expected to rise 8.7% y/y in 2026 and debt-to-GDP projected to hit 58% by 2029, combined with 50% tariffs on Indian exports to the U.S., may exert depreciation pressure on the KRW and INR in the near term. We will also be monitoring the political unrest in Indonesia, which triggered some market volatility in Indonesian assets last Friday. Lastly on flows, we are closely monitoring foreign investors’ flows, which turned to net outflows in August following strong inflows from May to July.

Markets enter September at an inflection point. Complacency built on summer’s low volatility and rate-cut optimism faces multiple catalysts: U.S. labor data, ISM surveys, and European inflation prints all feed directly into central bank policy paths. Political risk, especially France’s confidence vote, could generate outsized moves in European fixed income and spill over into broader risk sentiment. In Asia, weak North Asia PMIs vs. resilient ASEAN and India highlight a risk of policy divergence, creating sharper FX volatility, particularly if tariffs or geopolitical tensions flare.

The overarching risk is that volatility has been systematically underpriced: economic uncertainty remains historically elevated, political fragility is spreading across both developed and emerging markets, and central bank independence is increasingly in question. The week ahead may test whether markets can continue to lean on policy support narratives, or if September delivers the long-awaited turn in volatility and positioning.

Central bank decisions

Poland, Narodowy Bank Polski (NBP) (Wednesday, Sept. 3) — The NBP is expected to cut the reference rate by 25bp to 4.75%, continuing its easing cycle as inflation continues to soften, with August preliminary numbers showing a contraction of 0.1% m/m. Minutes from the July 2 meeting reported a majority view that an improved inflation outlook justified July’s adjustment. They also stated that subsequent decisions will depend on incoming data, with uncertainty tied to fiscal policy and administered energy prices. The minutes noted that inflation could remain consistent with the target in Q4 if the electricity price freeze is extended. There is still sufficient space for many CEE central banks to ease independently of the ECB. However, asset holdings remain strong, so incremental FX hedging may pick up as rate differentials become less attractive.

Malaysia, Bank Negara Malaysia (BNM) (Thursday, Sept. 4) — Market consensus is for BNM to maintain status quo at 2.75%. While low inflation warrants monetary policy easing, we see no urgency for aggressive easing unless there is a sharper deceleration of growth momentum. BNM recently lowered its 2025 GDP and CPI forecasts. GDP was revised from a range of 4.5% to 5.5% (midpoint: 5%) to 4% to 4.8% (midpoint: 4.4%), which is still a respectable growth pace. The 2025 inflation forecast was reduced substantially to a range of 1.5 to 2.3% (midpoint: 1.9%), down from 2.0 to 3.5% (midpoint 2.75%).

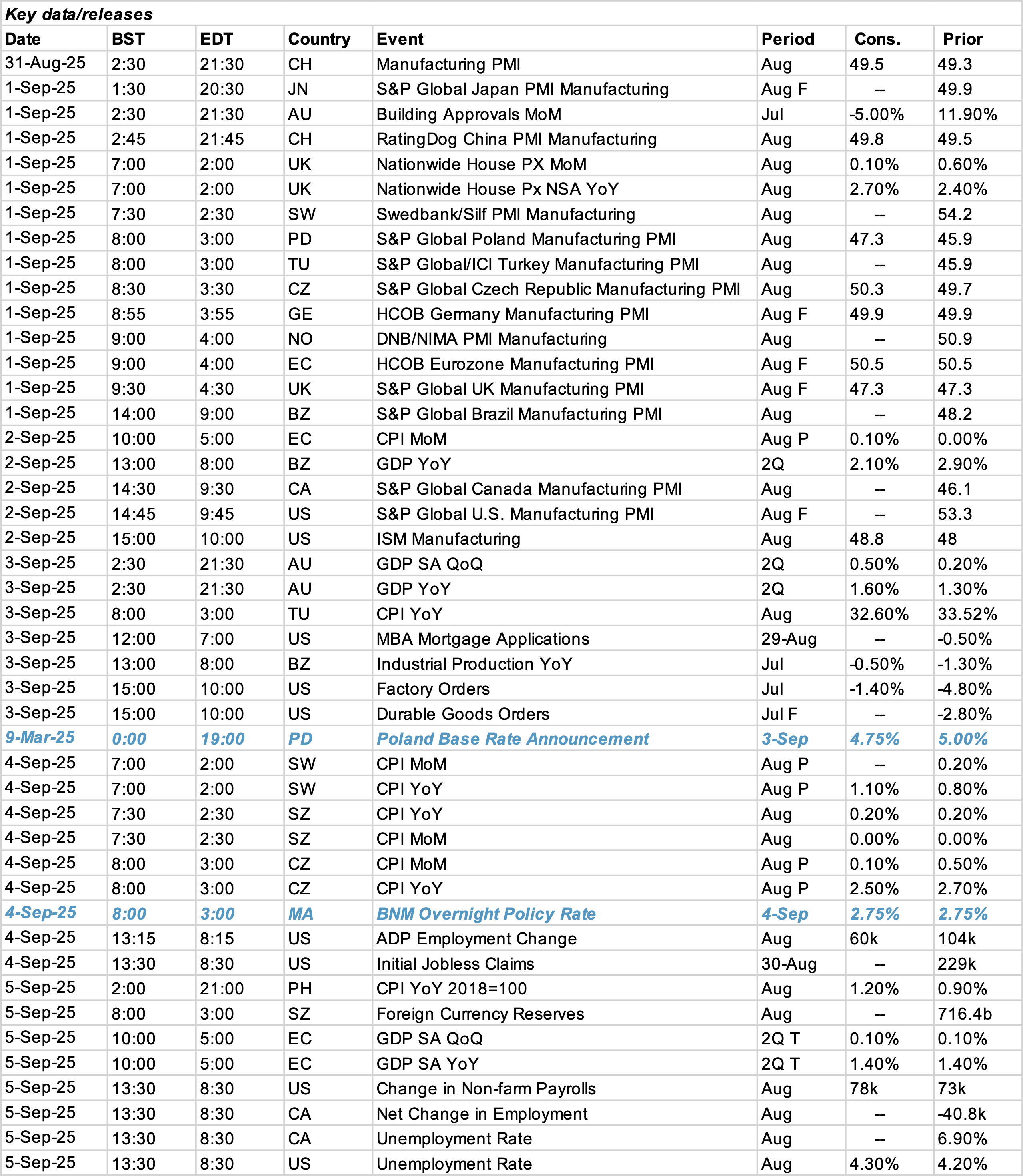

Data Calendar

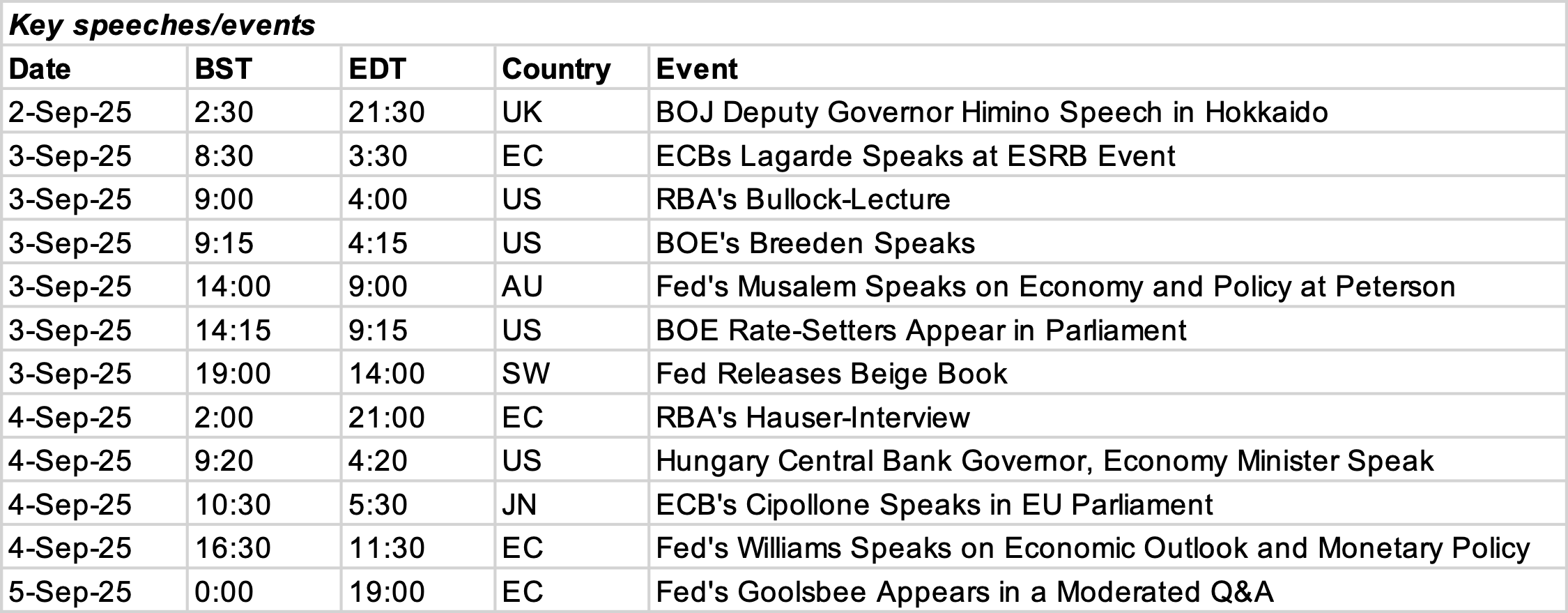

Event Calendar