Market Movers: Wandering

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Market Movers highlights key activities and developments before the U.S. market opens each morning.

Bob Savage

Time to Read: 8 minutes

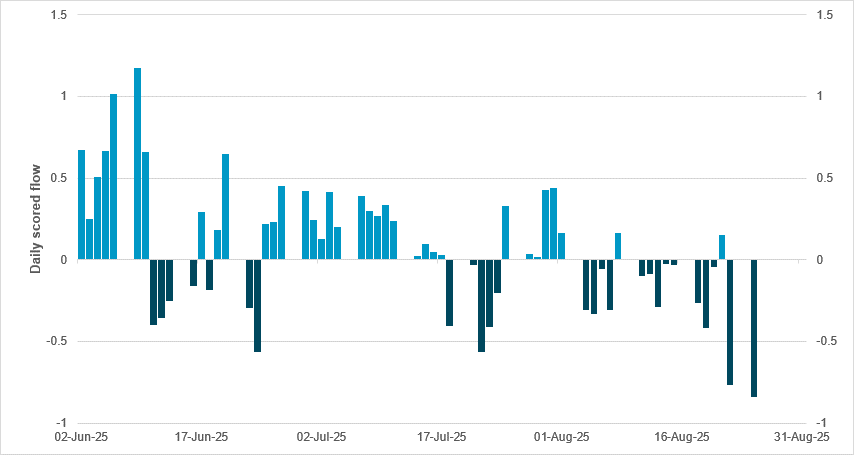

INDIAN EQUITY FLOWS SEE MATERIAL REVERSAL BUT HOLDINGS UNDER LIMITED STRESS

Source: BNY

As the 25% additional tariff on Indian exports to the U.S kicks in, Indian asset markets are starting to react. Although currency holdings are still comfortable and INR can benefit from its higher carry status in APAC (one of only two currencies in the region to enjoy this status, alongside INR), we suspect some of the recent flows are due to material equity market outflows, which have led to a reduction in hedges. The past two trading sessions were the worst in the last six months and come after a period of very consistent inflows since March, though rebalancing may have contributed to some of the excess. Current holdings of Indian equities are not significant, however, which is indicative of the strong underperformance seen this year. Furthermore, despite the strong index inclusion flows into the country’s bond market over the past two years, fixed income holdings have also dropped sharply this year, declining from nearly 40% above the rolling 1y average to 5% below. Some of the unwinding of hedges in fixed income may have also contributed to the light level of underheld positions in the currency. On an asset allocation basis, we believe international investors are generally in a holding pattern on Indian assets, but some progress on trade will be needed for any recovery. The domestic growth narrative will matter far more over the medium term, as India’s final exposure to trade and U.S. demand is limited. A credible policy response to current challenges, coupled with light asset positioning, is conducive to strong recovery flow.

Investor sentiment is mixed, as APAC equities focus on the aftermath of the MSCI index changes and as Xi’s purge of the military sparks questions about politics in China. Europe remains on watch for a political shift in France, with polls suggesting a majority of voters want a fresh election. The Dutch government now faces a no-confidence vote. The U.S. markets are in a holding pattern, with the focus on Nvidia earnings after the close. Consumer sentiment is less friendly for trading today, as falls in Germany and Switzerland make it clear this has been a summer of discontent for Europe. The focus for the day is on India and the 50% tariffs imposed on its exports to the U.S. FX and stocks are suffering accordingly. Fixed income markets are bid, but hardly enough to offset the pain as political concerns make fiscal policy clash with monetary policy for many developed markets. There are also idiosyncratic exceptions, with Hong Kong seeing a funding squeeze and Australia seeing sticky inflation that is slowing hopes of faster rate normalization. We are all waiting for more data, and that reactive quality to markets translates into a wandering tape where trend and other factors fail to work. The implications for the U.S. session ahead are that any surprise could lead to further risk reductions, as cash and other safe havens beckon. The correlations between USD up and stocks down or between bonds up and USD down are not working either, and that makes the search for the right path ahead a difficult one.

The EU will propose legislation this week to remove all tariffs on U.S. industrial goods. This comes in response to President Trump’s demand, which he made a condition of the U.S. lowering duties on EU automobile exports. The plan includes preferential tariff rates on certain seafood and agricultural products, despite the EU acknowledging that the deal favors the U.S. European Commission President Ursula von der Leyen described it as “a strong, if not perfect deal,” emphasizing stability for businesses. Currently, EU cars and auto parts face a 27.5% U.S. tariff; if legislation is advanced by month-end, the tariff cut to 15% will be backdated to August 1. Germany exported $34.9bn in cars and parts to the U.S. in 2024. Euro Stoxx 50 -0.089% to 5378.87, EURUSD -0.456% to 1.1589, BBG AGG Euro Government High Grade EUR -2.5bp to 2.86%.

Australia July CPI rose more strongly than expected, up 2.8% y/y from 1.9% y/y in June, the highest since July 2024. The trimmed mean, which is the country’s preferred measures, rose from 2.1% y/y to 2.7% y/y. The largest contributors to this rise were housing (+3.6% y/y, within which electricity costs rose 13.1% y/y), food and non-alcoholic beverages (+3.0% y/y), and alcohol and tobacco (+6.5% y/y). Note that the reason behind the large electricity cost increase was that households in NSW and ACT did not receive payments from the extended Commonwealth Energy Bill Relief Fund (EBRF) in July. Payment of rebates to these households will instead commence in August. ASX +0.103% to 5022.3, AUDUSD -0.385% to 0.647, 10y ACGB +1.1bp to 4.325%.

Germany’s September GfK consumer climate came in at -23.6, down 1.9 points from August, marking the third consecutive decline. Income expectations fell sharply by 11.1 points to 4.1, the lowest since March, as rising unemployment and job security fears weighed on sentiment. Economic expectations also dropped for the second month in a row, down 10.1 points to -7.4, their weakest level in six months. Willingness to buy declined slightly by 0.9 points to -10.1, remaining at one of the lowest levels since February. Propensity to save eased marginally by 0.6 points to 15.8. Concerns over inflation, energy prices and geopolitical uncertainty, including U.S. tariff policy, further dampened consumer outlook, reinforcing the ongoing summer slump. DAX -0.384% to 24060.14, EURUSD -0.456% to 1.1589, 10y Bund -2.4bp to 2.699%.

Swiss economic expectations as measured by the UBS-CFA indicator have fallen sharply to -53.8, the lowest level since the height of the energy crisis in Q4 2022. This marks a sharp reversal from the positive print in July, when cautious optimism had prevailed. Clearly, trade issues have had an impact, as the April print registered a similar balance of -51.6. The report noted that nine out of ten respondents now expect Swiss export momentum to deteriorate in the next six months, with the export outlook indicator collapsing by 54.7 points to -89.8. Such a steep decline has only previously occurred during major shocks such as the SNB’s currency floor removal in 2015 and the Covid-19 crisis. Switzerland’s failure to secure a trade deal is plainly the biggest factor behind the deterioration, while impending sector-specific tariffs on the pharmaceutical industry threaten further declines in the Swiss economy outright. SMI +0.208% to 12186.21, EURCHF -0.07% to 0.93467, 10y Swiss GB -5bp to 0.274%.

Central bank speakers: Richmond Fed’s Tom Barkin, repeating yesterday’s speech but with more Q&A, in North Carolina.

U.S. Treasury sells $65bn in 17-week bills, $28bn in 2y FRNs and $70bn in 5y notes

U.S. Q2 earnings: Nvidia earnings forecast at $1.01 per share, revenues expected at $46bn, with Chinese sales and earnings the key focus.

Mood: iFlow Mood continues its gradual ascent with a pick-up in equity momentum along with easing demand for core sovereign bonds.

FX: IDR, CLP and SEK were most sold within the iFlow universe, while EUR, JPY and CNY posted the most inflows. EUR and JPY scored holdings rose to 0.78 and 2.1, respectively.

FI: Chilean and Polish government bonds, U.K. gilts and U.S. Treasurys posted the most inflows, including cross-border investors. Indonesian, Chinese and Mexican government bonds were most sold.

Equities: Mixed flows across the region. Within the G10, Swedish, Danish and Norwegian equities were bought, against selling in U.K., European and U.S. equities. Elsewhere, notable flows included buying in Chile, Israel and Singapore equities, against selling in Taiwan equities. Within DM EMEA, the energy and health care sectors were bought, against selling in the consumer staples, financials and information technology sectors.

“Not all those who wander are lost.” – J.R.R. Tolkien

“We wander for distraction, but we travel for fulfillment.” – Hilaire Belloc

Sweden’s July MFI lending to households grew 2.6% y/y. Housing loans, which accounted for 83% of total household lending, rose 2.4% versus 2.2% in June. Consumer loans, representing 6% of household lending, grew 4.6% compared with 4.0% in June. Lending to non-financial corporations increased 2.7%, bringing total MFI lending to households and corporates to SEK 8.094tn, with a 63%/37% households/corporates split. Mortgage rates eased, with the average housing loan rate at 2.84% (June: 3.01%), with floating rates down to 2.86% and fixed 1-5y terms to 2.87%. Deposits from households totaled SEK 2.856tn, with 75% of that figure on demand. M3 money supply reached SEK 5.031tn, up 4.4% y/y. Interest rates on new loans averaged 2.84% for mortgages and 3.83% for corporates, while interest rates on household deposit fell to 0.62% from 0.67% in June. OMX -0.433% to 2645.352, EURSEK +0.045% to 11.1331, 10y Swedish GB +1.3bp to 2.573%.

Norway’s July unemployment rate was flat versus June at 4.6%, with 141,000 unemployed people, up 1,000 m/m. The number of employed people reached 2.91 million, an increase of 3,000, keeping the employment rate steady at 69.7%. Seasonally adjusted data showed the number of employees rising by 6,106 or 0.2% between June and July, while the number of jobs increased by 6,876, also up 0.2%. Average monthly cash remuneration grew by NOK 220 m/m, equivalent to a 0.4% increase. Compared with the previous period, when job and employee figures were broadly unchanged, July saw modest gains in both employment and wages. OSE -0.438% to 1652.27, EURNOK +0.068% to 11.7994, 10y NGB +0.1bp to 3.989%.

South Korea’s Business Survey and Economic Sentiment Index for manufacturers climbed 1.4 points m/m to 93.3 in August, while the non-manufacturers index advanced 0.7 points to 89.4. The outlook for manufacturers and non-manufacturers stood at 91.0 and 86.8, respectively. Tariff-related uncertainty has eased following the conclusion of negotiations with the U.S., and exports, particularly in semiconductors and automobiles, performed strongly. In the non-manufacturing sector, business conditions have improved, especially in the transportation, warehousing and retail fields, supported by the summer holiday season and the government’s stimulus measures. KOSPI +0.245% to 3187.16, USDKRW +0.23% to 1397.15, 10y KTB +0.3bp to 2.855%.

South Korea’s July retail sales at major distributors rose 9.1% y/y, with offline sales up 2.7% and online sales increasing 15.3%. Department store sales grew 5.1% y/y, led by luxury goods, food and a rebound in clothing and sports items, while convenience store sales advanced by 3.9% after four months of decline, supported by hot summer weather and consumer coupon use. By contrast, sales at large supermarkets fell 2.4% y/y as visitors and purchase amounts declined, while SSMs recorded a 1.8% rise, extending growth to a fifth month. By category, offline sales rose in food (2.7%), services (4.4%) and luxury brands (11.3%). Online growth was led by services such as food delivery, e-coupons and travel (24.9%), alongside food (24.2%) and apparel (14.2%). Overall, offline accounted for 45.7% of sales and online 54.3%.

Korea Investment & Securities Co. plans to buy unhedged super-long Japanese government bonds for the first time to take advantage of generous yields and its expectation that the yen will maintain gains against the dollar. The company, which has more than $60bn of assets, was buying three-month and six-month Japanese notes about a decade ago, and this will be its first foray into longer maturities.

Australia’s Westpac-MI Leading Index rose 0.14% m/m in July from -0.03% in June. This is the best monthly gain since October 2024 (0.17% m/m). The leading index still points to sluggish growth momentum in the second half of 2025 and early 2026. The recovery that started to take shape last year continues to proceed slowly. Westpac expects the Australian economy to grow by just 1.7% this year, a marginal improvement on the 1.3% gain in 2024. Growth is only expected to return to a trend pace of 2.2% by the end of 2026. Elsewhere, Australia Q2 construction work done rose strongly at 3.0% q/q, 4.8% y/y from -0.3% q/q in Q1 2025. Engineering work rose 6.1% q/q, 8.5% y/y. Building work done rose 0.2% q/q, 1.6% y/y. ASX +0.103% to 5022.3, AUDUSD -0.385% to 0.647, 10y ACGB +1.1bp to 4.325%.

Chinese industrial profit extended its decline in July, at -1.5% y/y from -1.8% y/y in June. The government has introduced measures to bolster domestic consumption and curb price wars, but these efforts have yet to produce significant results amid ongoing deflationary pressures and a prolonged housing downturn. The news comes as the $1tn stock rally in China is sparking concerns over growing risks to investors, prompting some brokerages and fund managers to cut back on financing and limit purchases. Shanghai-based Sinolink Securities Co. has raised its margin deposit ratio on new client financing contracts for some securities to 100%, and some domestic mutual fund houses have imposed daily purchasing restrictions on some portfolios. CSI 300 -1.493% to 4386.13, USDCNY +0.111% to 7.1607, 10y CGB +0.2bp to 1.77%.