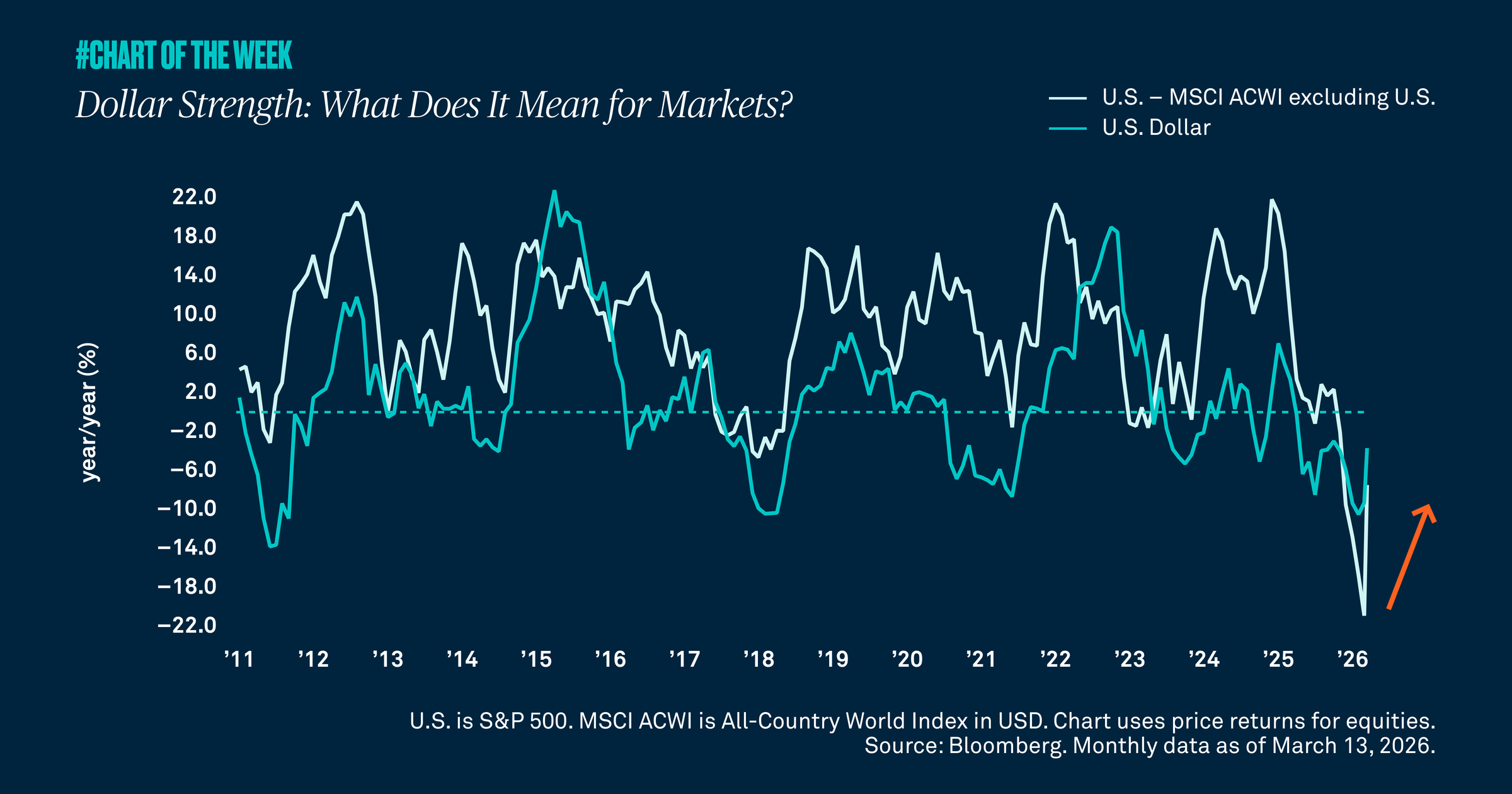

Dollar strength: what does it mean for markets?

Geopolitical tensions have lifted oil prices, sent U.S. stocks slightly lower and driven flows into the safety of the U.S. dollar, which has strengthened versus peers. While a weaker dollar previously supported international equity outperformance, dollar stabilization now suggests that tailwind is fading, underscoring the importance of diversification across regions and asset classes.

The conflict in the Middle East has seen oil prices rise, equities fall slightly, and investors flock to safe haven assets. In times of turmoil, investors often seek the stability of the U.S. dollar (USD) because of its reserve currency status and liquidity, as well as the perceived credit strength of the U.S. This episode of geopolitical uncertainty is proving to be no different with the USD gaining strength relative to global peers.

Historically, the performance gap between U.S. equities and the rest of the world has hinged on the relative strength of the USD. While a weaker USD makes U.S. exports more competitive, this has often coincided with the outperformance of major non-U.S. indices on a relative basis. That pattern has been evident over the last year, with international equity benchmarks outperforming the S&P 500.

In our view, signs of USD stabilization suggest the tailwind from dollar weakness to non‑U.S. outperformance has likely peaked. The USD is near its highest level since May 2025, and the combination of sticky inflation, U.S. energy independence and resilient growth could limit further dollar softness and challenge the recent leadership of international markets. Diversifying across geographies and asset classes remains prudent to capture potential upside amid today’s varied global conditions.

902639 Exp : 17 March 2027

YOU MIGHT ALSO LIKE

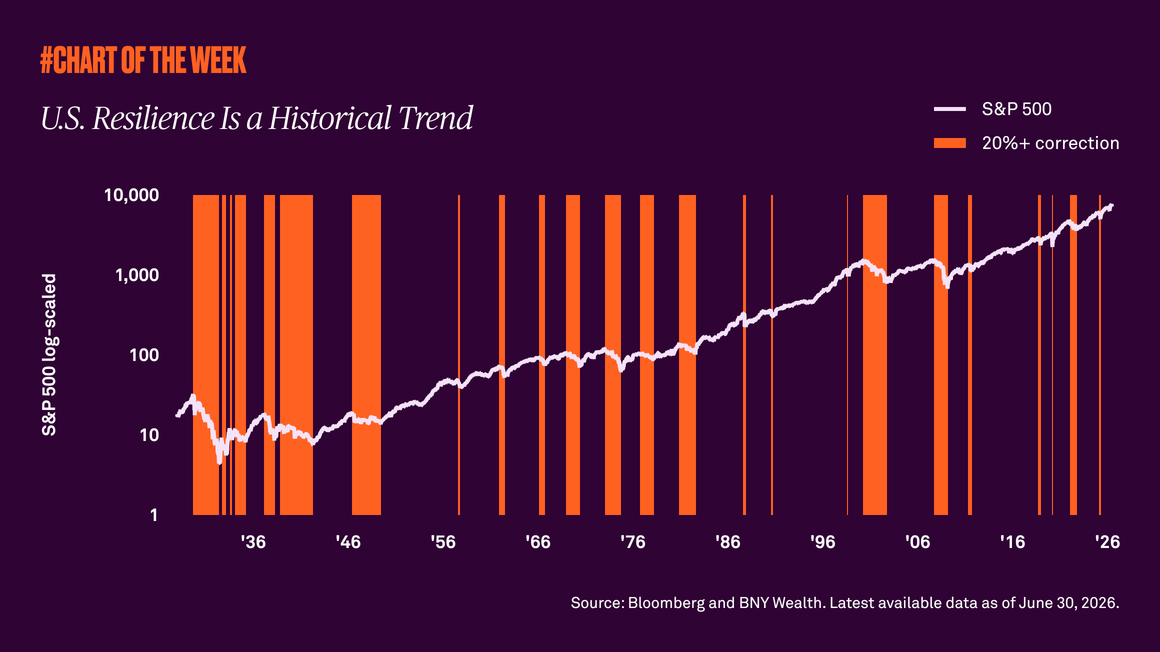

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

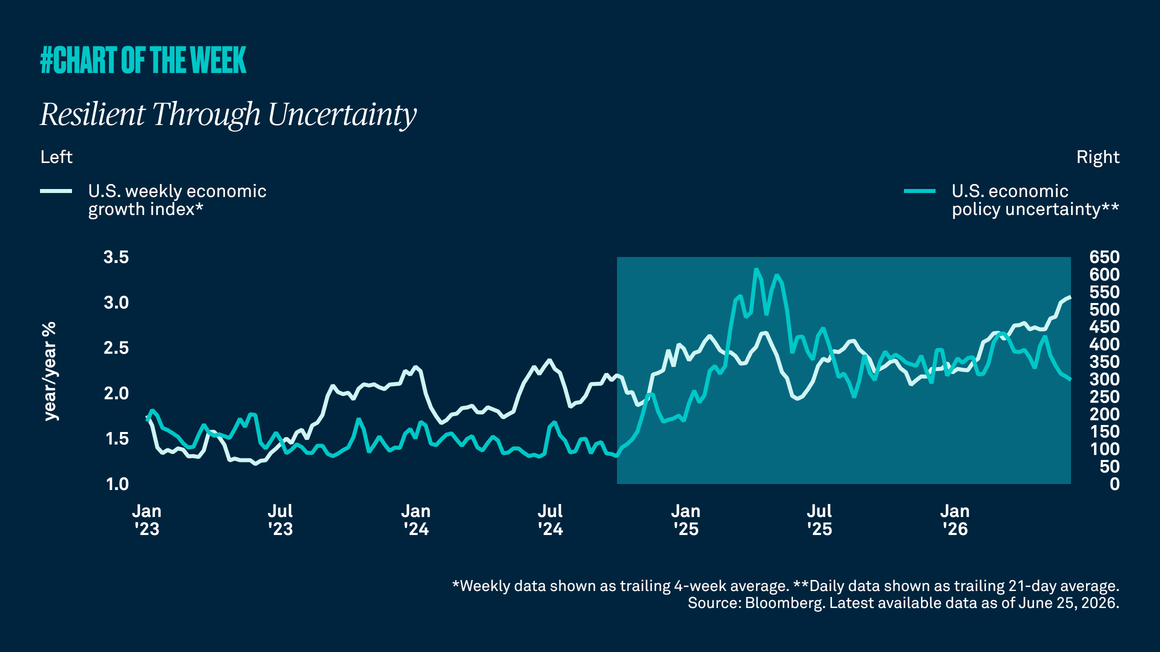

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.

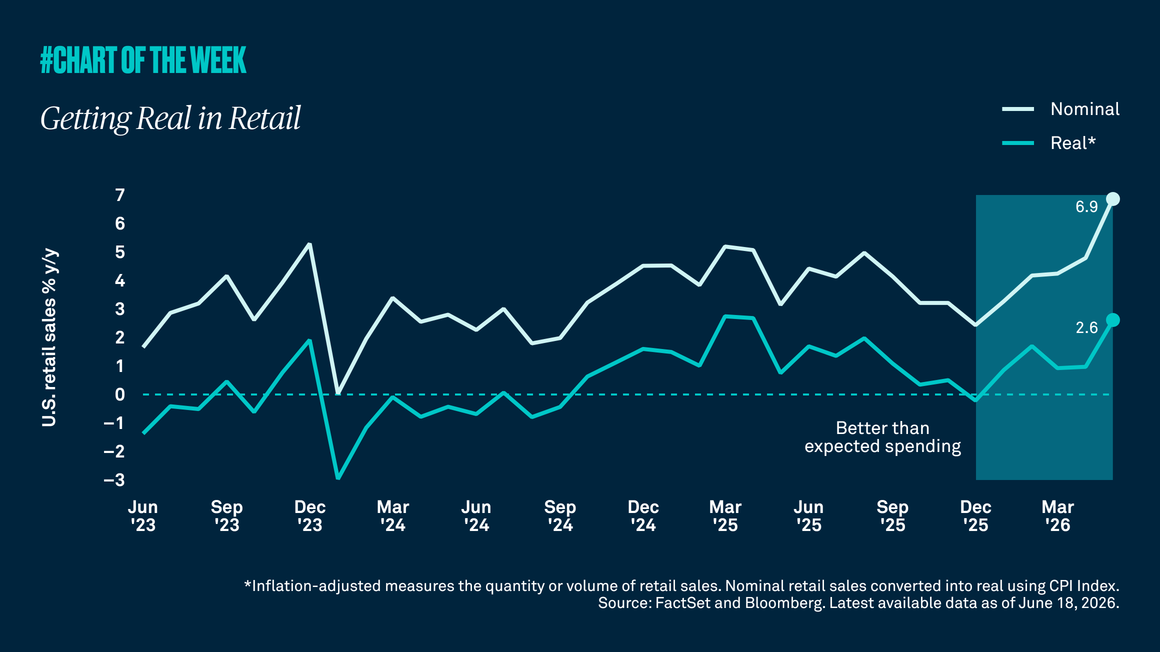

Despite persistent concerns that sticky inflation would erode purchasing power and drag consumer spending lower, the May retail sales data tells a different story. Spending is up not just in dollar terms, but in quantity, highlighting continued consumer resilience.

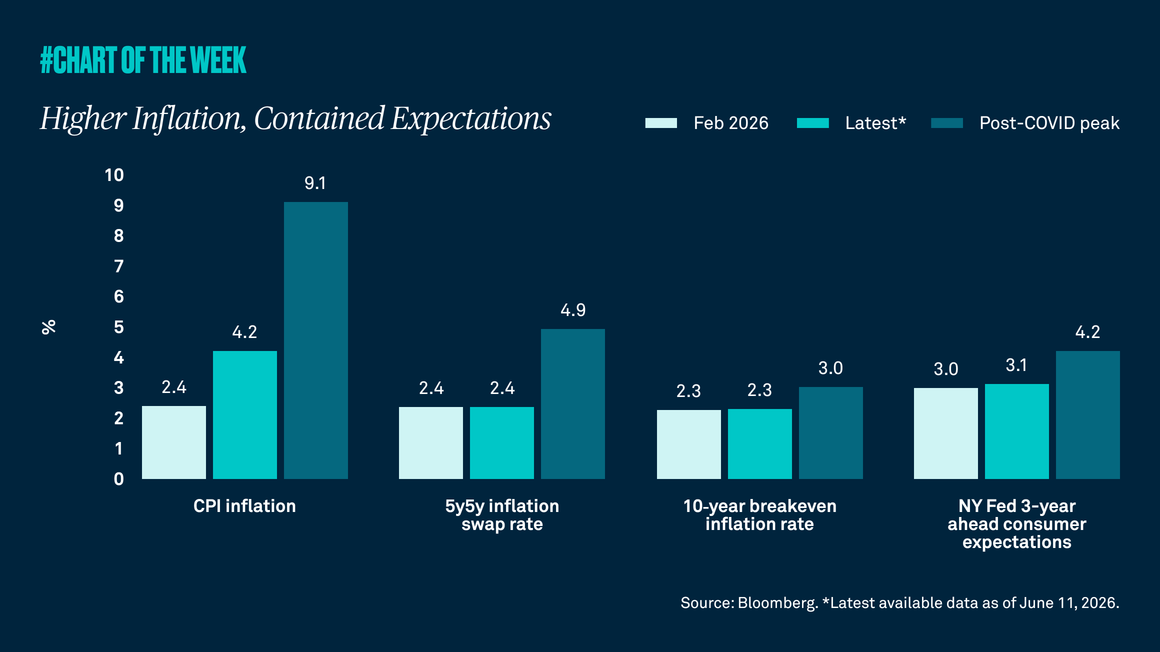

Inflation has jumped since the Strait of Hormuz closed, squeezing consumers through higher gas and utility bills and pressuring businesses with higher freight and operating costs. Yet, longer-term inflation expectations remain contained, suggesting this looks more like a temporary energy shock than a lasting inflation upswing.