Capital Market Assumptions

Endurance Under Pressure

Pressure creates resilience or strain. Our CMAs provide a disciplined, long-term view to help investors build enduring portfolios.

Capital Market Assumptions

Endurance Under Pressure

Pressure creates resilience or strain. Our CMAs provide a disciplined, long-term view to help investors build enduring portfolios.

Shifts in geopolitics, technology, and macroeconomic policy are compressing global markets. Effectively navigating these changing dynamics requires a long-term lens and a durable framework.

Our 10-Year Capital Market Assumptions (CMAs) are the building blocks for the development of an investor’s strategic asset allocation. We assess how today’s markets are adapting to structural pressures including sovereign debt burdens, evolving currency dynamics, rapid advances in artificial intelligence (AI), and the continued expansion of private capital. Together, these forces are shaping a landscape where flexibility, durability, and diversification matter more than ever.

Key Highlights

When forming long-term expectations, it’s essential to look beyond cyclical fluctuations and focus on the structural forces shaping trend growth, inflation, and interest rates. Several structural themes are poised to influence the decade ahead.

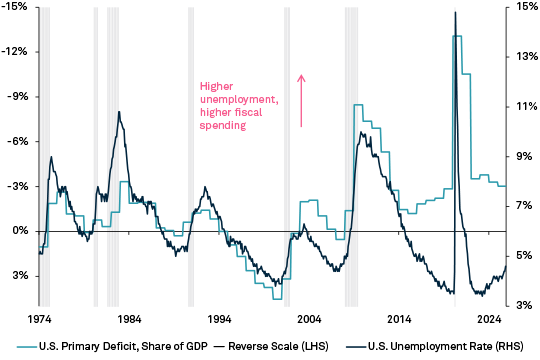

Developed markets face fiscal strain as higher borrowing costs meet persistent deficits and rising issuance.

Fiscal policy tends to be countercyclical (loosened during economic downturns when the unemployment rate tends to rise) as governments step in to boost aggregate demand. However, we observe that U.S. fiscal policy has become more procyclical (higher government spending during higher GDP growth and lower unemployment), circa the passing of the Tax Cuts and Jobs Act (TCJA). The UK, Germany, and Japan are also seeing elevated debt burdens and fiscal pressures.

Prepare for steeper yield curves and bond market volatility. Stay active in duration and across global sovereign markets.

Sources: BNY Investments, BLS and CBO. Data as of September 22, 2025.

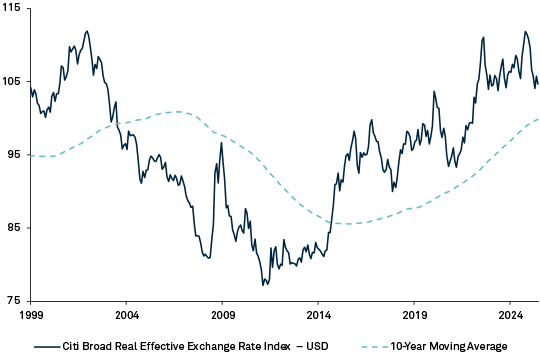

Shifting trade policies, rising FX hedging activity, and narrowing global growth differentials are eroding support for the U.S. dollar.

With policy shifts reducing the degree of U.S. outperformance relative to the rest of the world, and capital flows becoming more diversified, dynamics reinforce a weaker dollar over the long term.

Over time, we expect the U.S. dollar’s real effective exchange rate (REER) to revert toward its 10-year moving average, driven by the ongoing convergence of global growth rates and rebalancing of trade, the structural rise in FX hedging by international investors, and the dollar’s continued overvaluation relative to long-term benchmarks.

Reassess global currency exposure, hedge ratios and the diversification role of non-U.S. assets as capital flows broaden.

Sources: BNY Investments and Bloomberg. Data as of October 31, 2025.

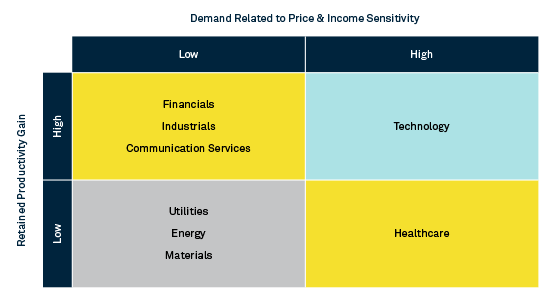

The impact of AI on productivity and competitive dynamics will become more visible.

The biggest beneficiaries of AI adoption won’t simply be the fastest adopters. Winning firms will likely leverage two advantages: strong productivity gains even after widespread adoption and the ability to capture unmet demand where lower prices translate into higher volumes. Sectors that pair these two dynamics together can become important plays in the AI theme. While information technology remains a favored sector under this framework, it also faces disruption with wide dispersion between winners and laggards.

Look toward firms and sectors that can both retain productivity gains and convert lower costs into sustained demand and earnings growth.

Source: BNY Investments

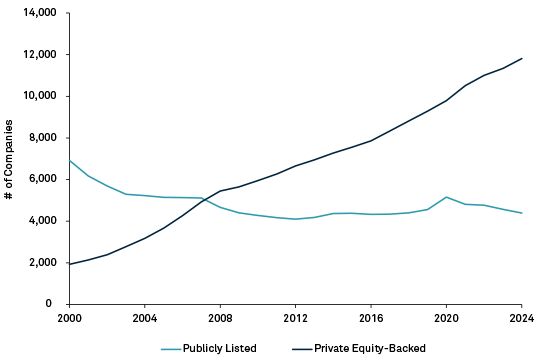

Private markets are at the center of an AI-driven capital expenditure boom, facilitating AI adoption and creating significant opportunities for investors.

Private equity and venture capital remain key funders of startups and are well-suited for long-term, active investments in AI infrastructure. They are increasingly complemented by private infrastructure and real estate funds, which offer inflation-linked returns and exposure to secular trends in energy and data. Aligning with the surge in AI adoption, more companies are choosing to remain private for longer, allowing more growth to occur before reaching public markets.

Look beyond traditional public markets to access the full growth opportunity set and be mindful of increasing market concentration in public equities.

Source: World Bank. Data as of December 31, 2024. Note: Publicly listed data from before 2024 is from World Bank and Statista; 2024 data is from Morningstar.

Capital Market Assumptions

Our 10-Year Capital Market Assumptions explore how a disciplined, forward-looking approach to strategic asset allocation — grounded in robust capital market assumptions and an understanding of structural changes — will be essential for navigating this environment and capturing long-term value.

Our methodology incorporates projected 10-year returns for each asset class, with expectations driven by key themes across equities, fixed income, alternatives, and currencies. We conclude with guidance on our model construction, detailing how we calculate volatility and correlation, adjust for private markets, and reconcile arithmetic with geometric return measures.

✓ Sovereign Debt

✓ U.S. Dollar

✓ AI Adoption

✓ Private Markets

Dig Deeper into the Data

Access our capital market assumptions denominated in various currencies below to support portfolio construction, scenario analysis, and strategic planning. Data files include our expected arithmetic returns, geometric returns, volatility and correlations across 33 asset classes for a 10-year horizon.

Unless otherwise stated, the assumptions expressed in local currency terms do not incorporate currency hedging decisions, which should be considered separately at the portfolio level.

Related Research

Essential Questions for Investors

In our annual outlook, investment and market leaders across BNY tackle six key questions we believe will define the year ahead.

The Capital Market Assumptions materials include important disclaimers, disclosures and definitions. Those should be read in its entirety.

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy.

Opinions and views expressed are subject to change without notice.

Past performance is no guarantee of future results.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE |

BABR-865800-2026-01-14 GU-781 – 15 February 2027