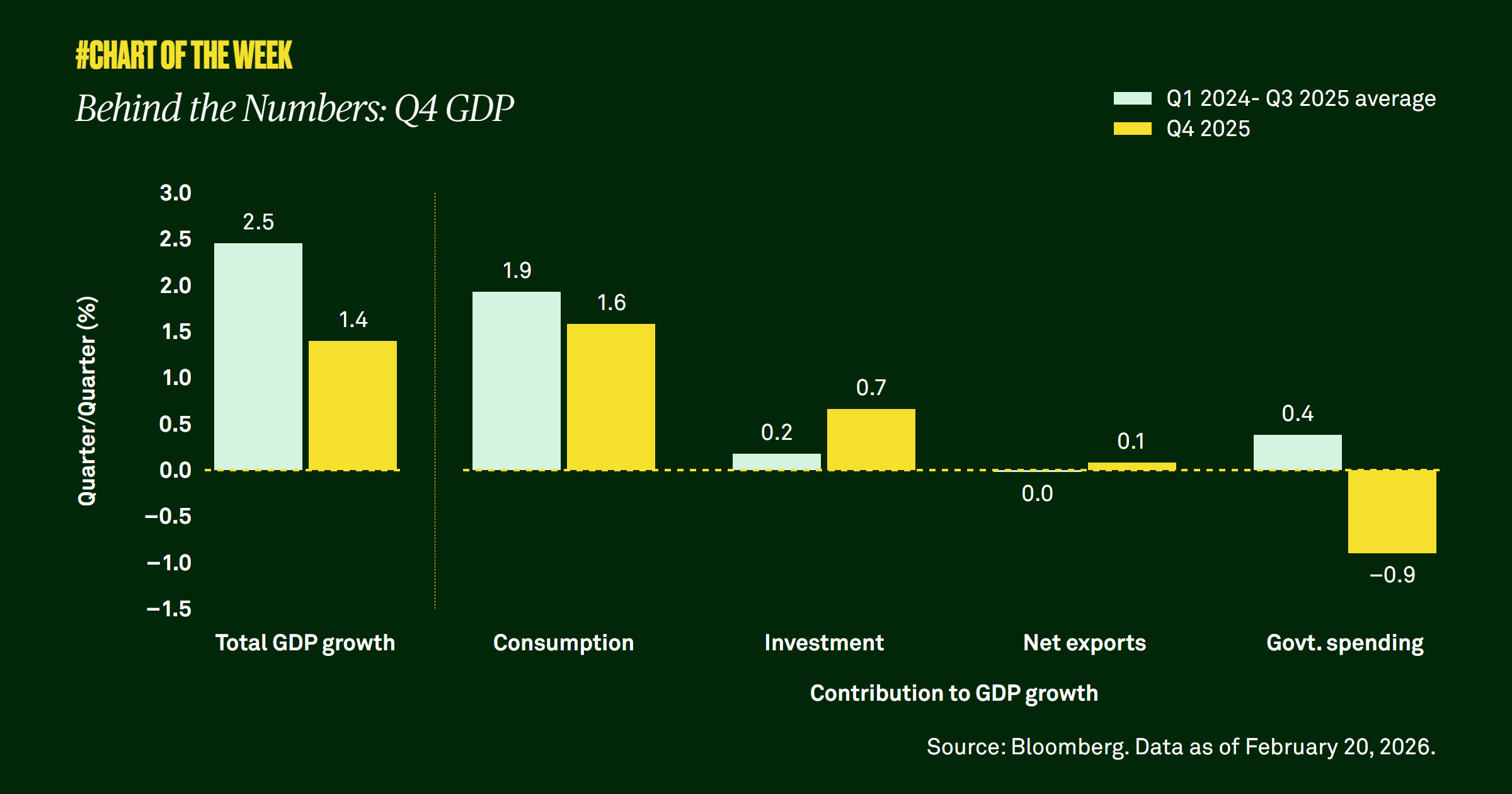

Behind the numbers: Q4 GDP

Gross domestic product undershot expectations last quarter, but the shortfall appears driven more by the temporary government shutdown than broad-based weakness. Consumer demand remains resilient, and with supportive fiscal policy, easing financial conditions and a steady labor market, the outlook points to a modest acceleration in economic activity this year.

Last week’s fourth quarter gross domestic product (GDP) report came in at annualized pace of 1.4%, disappointing many Wall Street analysts who had anticipated 2.8%. For some investors, the news renewed concerns about an economic slowdown.

Growth was indeed softer than the 3% or more recorded in the previous two quarters, but the drivers of the miss are clear. The biggest drag was government spending at −0.9%, an unusually weak contribution that suggests the fourth quarter could have ended near 2.3% — above trend — absent the 43‑day government shutdown.

Consumption, the largest driver of GDP with a 70% share, slowed slightly to 1.6%, yet it remains resilient and in line with the average since 2024. We believe fiscal stimulus, lower interest rates and a steady job market will support household balance sheets and spending going forward.

Taken together, the evidence suggests the government shutdown — rather than a broad slowdown — drove the shortfall. Consensus GDP is 2.5% this year, and our target of 2.3% closely matches, reflecting our confidence in the economy amid a steady job market and sustained consumer spending.

891108 Exp : 24 February 2027

YOU MIGHT ALSO LIKE

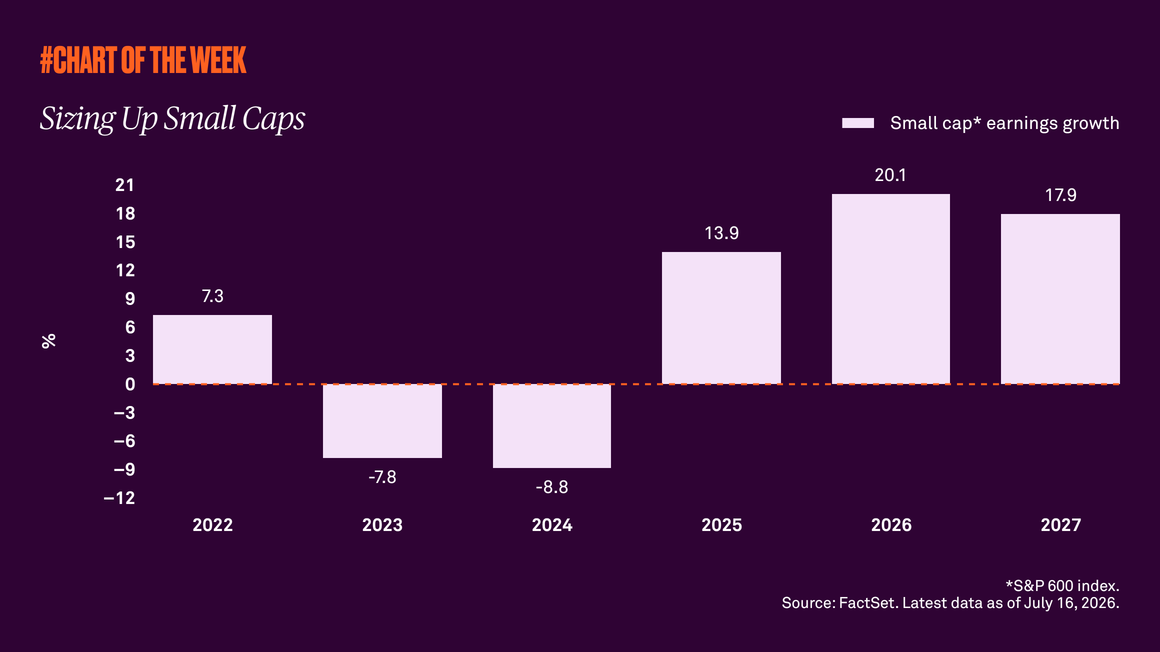

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

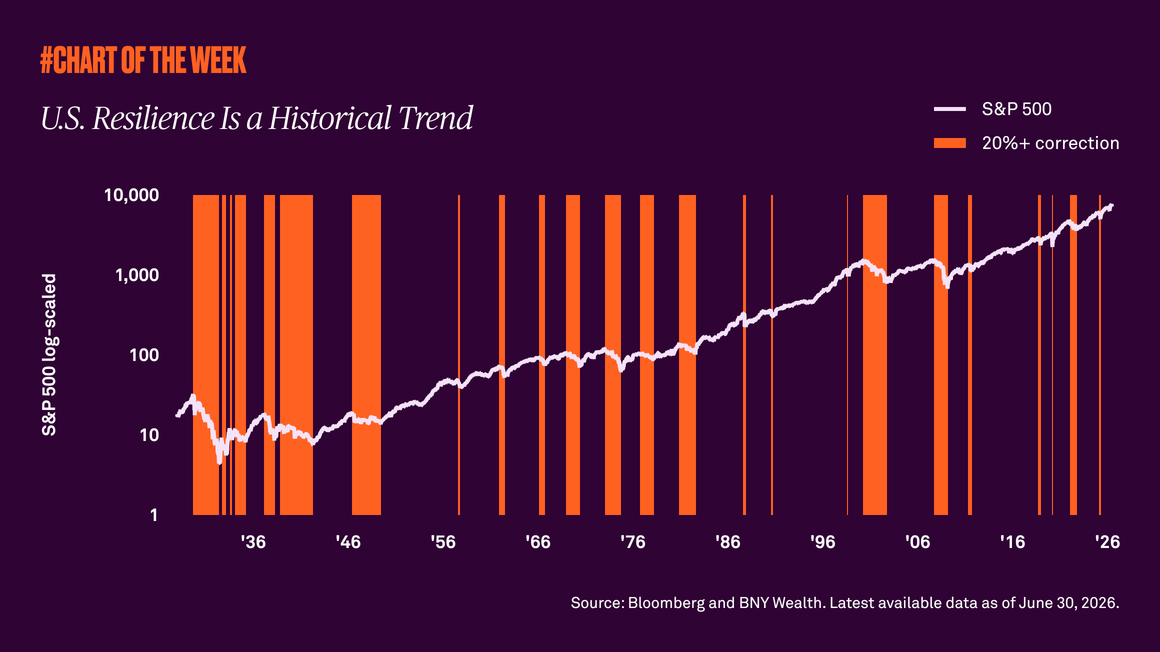

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

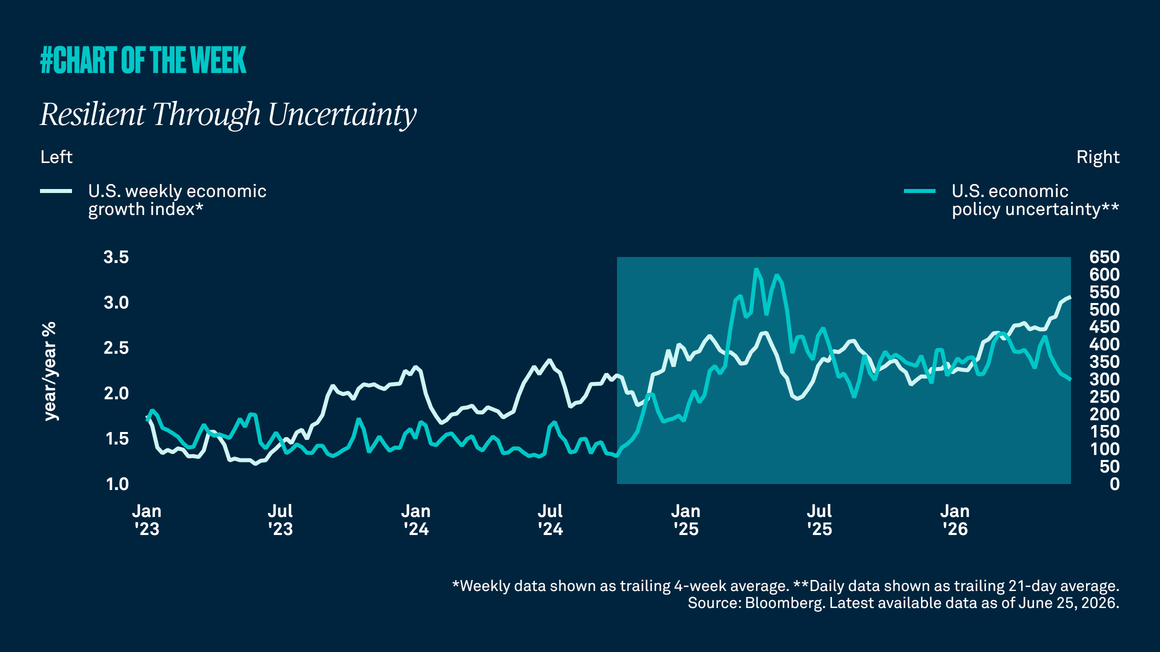

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.