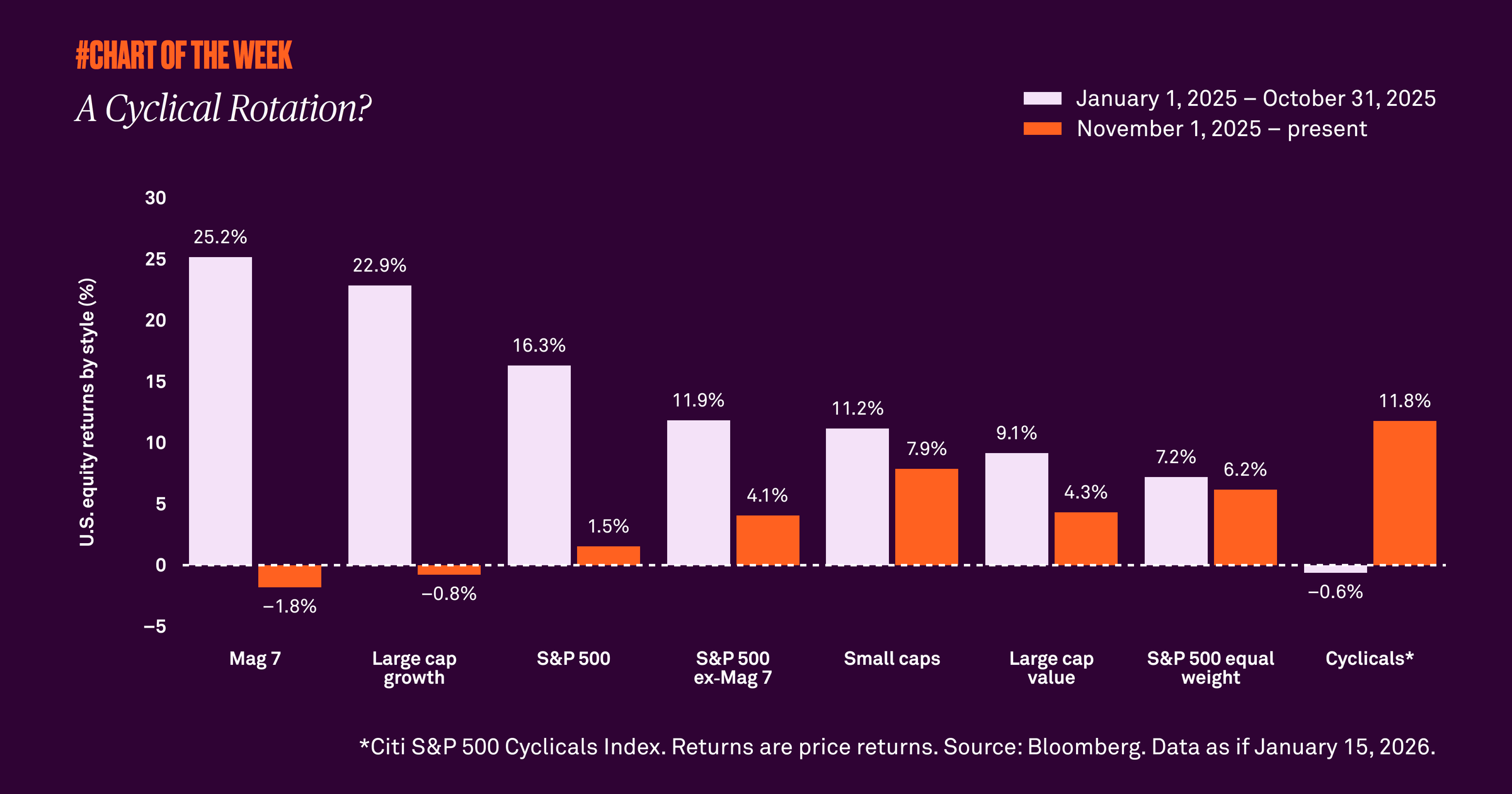

A cyclical rotation?

Stronger growth expectations are driving a global rotation out of growth-oriented and mega cap technology stocks, and into cyclical companies. At a time when geopolitical tensions and tariff discussions continue to simmer, we remind investors to stay invested despite the headline noise.

The Magnificent Seven and large cap growth stocks outperformed the S&P 500 for the majority of 2025, but equity leadership shifted at the end of October. Cyclical stocks — those that are more economically sensitive — lagged large cap growth stocks and shares of mega cap technology companies until November 1, when we first detected a broadening in markets.

It was the beginning of a global rotation out of those growth-oriented and technology businesses into cyclical areas, such as small cap and large cap value stocks. Since November, cyclicals are up 11.8% compared to the negative returns for growth stocks and big tech in the S&P 500.

What changed? Markets are pricing in a stronger global growth outlook despite current events around geopolitics and tariffs. Many factors support improved economic activity, such as increasing capital expenditures, resilient consumer spending, improving productivity, easing financial conditions and solid earnings growth.

Even given these tailwinds, it is often hard to ignore headline noise. Nonetheless, we reiterate one of our core investing principles: don’t get distracted by headlines and stay invested. Over the long run, wealth is built by staying the course, remaining invested and keeping diversified.

869830 Exp : 21 January 2027

YOU MIGHT ALSO LIKE

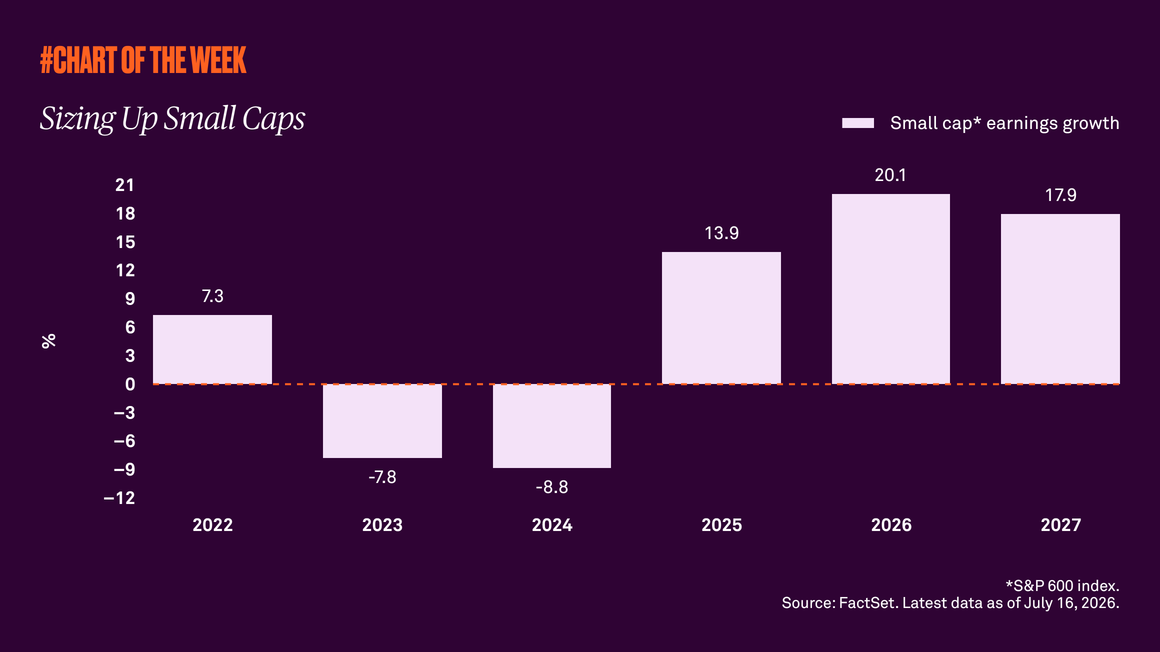

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

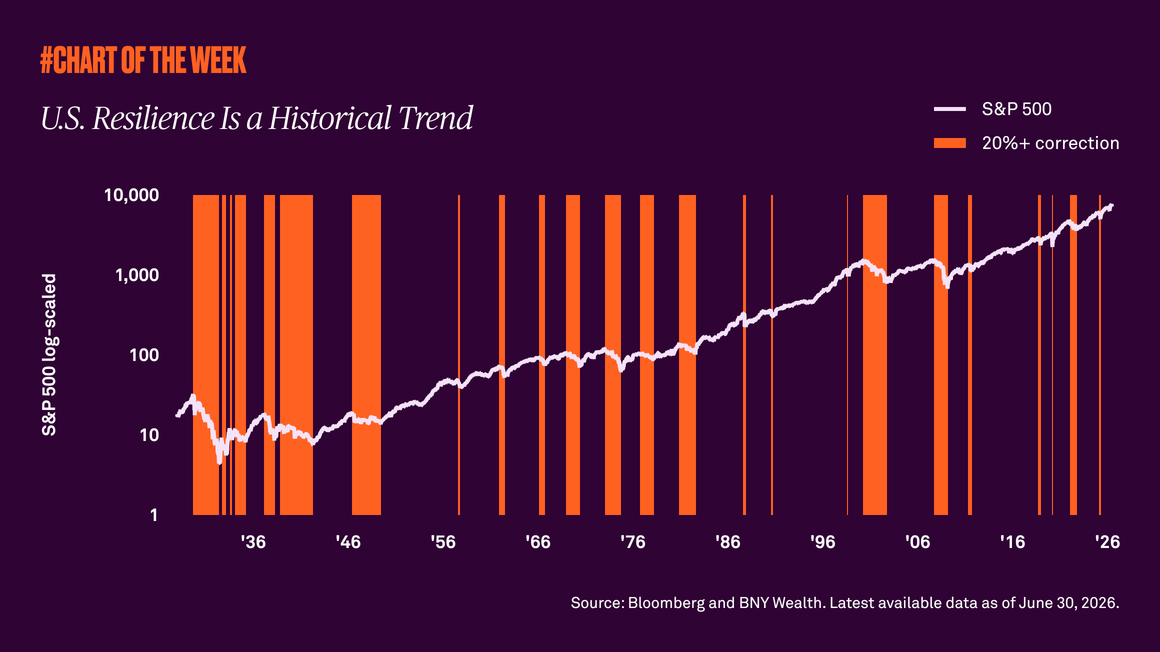

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

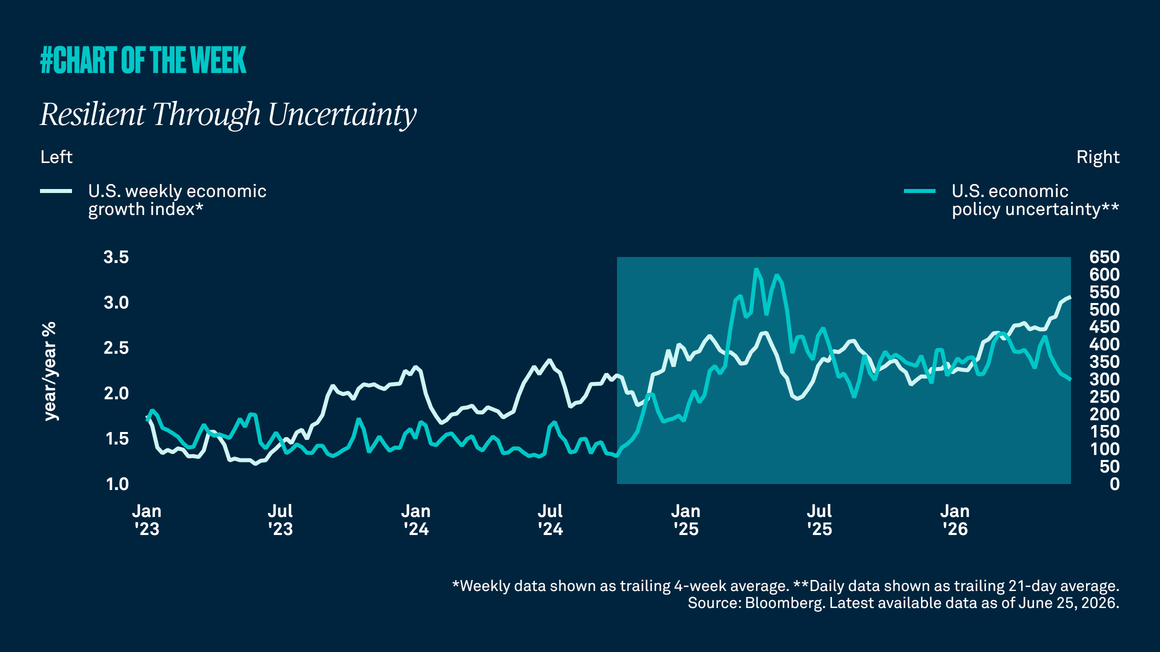

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.