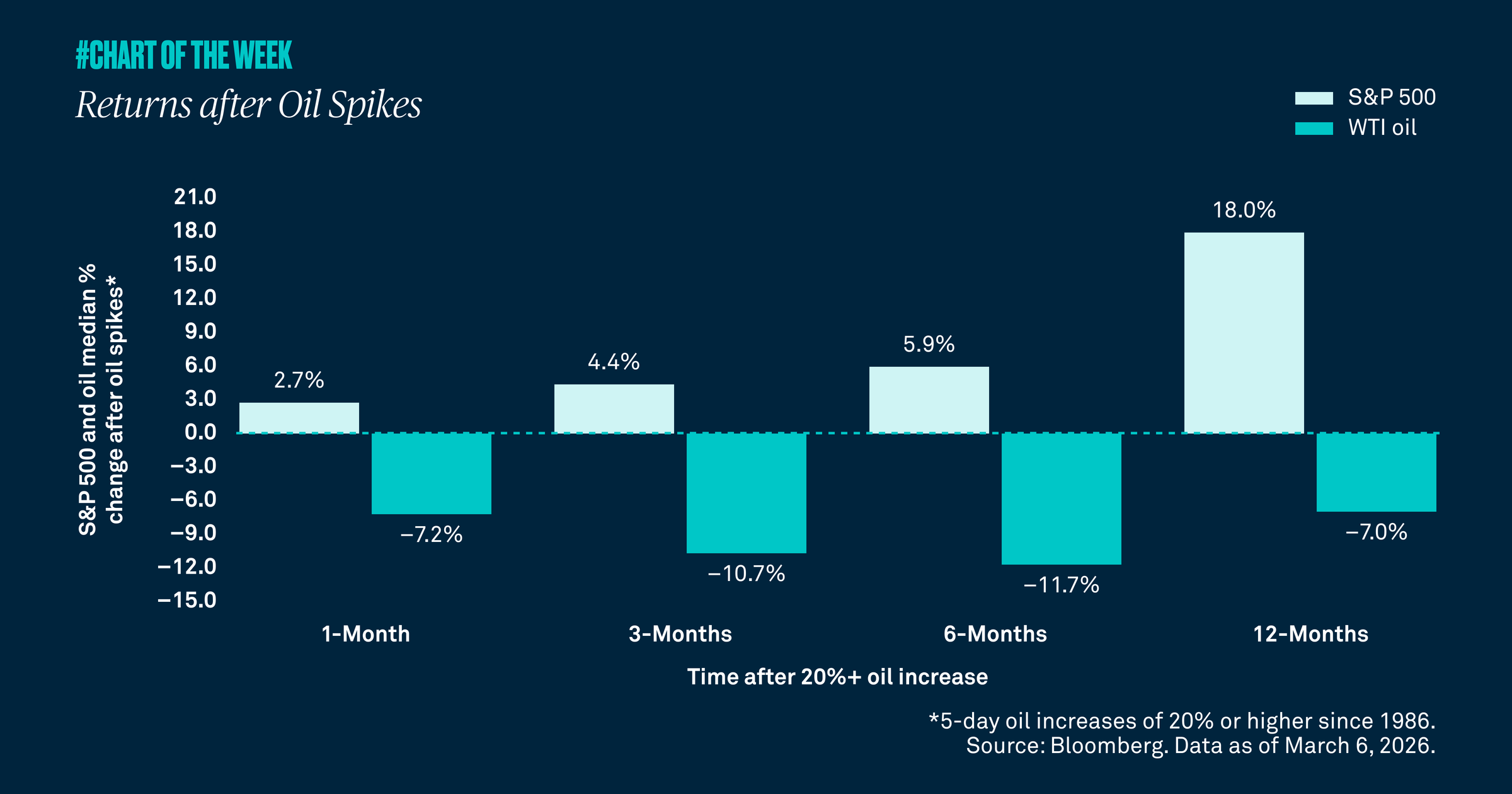

Returns after oil spikes

The Strait of Hormuz, which moves about 20% of global oil, has seen many ships that normally travel through it curtail their activity. Consequently, WTI oil was up over 36% in the five days after the oil supply shock began. Yet equities barely budged, signaling a temporary supply shock, not a larger crisis. Historically, after similar price spikes equities tend to move higher while oil prices decline — further evidence for avoiding emotion-driven investing.

The Strait of Hormuz, which links the Persian Gulf to the Indian Ocean, sits at the heart of today’s Middle East tensions. It moves roughly 20% of global oil, yet ships are increasingly skirting the route amid Iranian attack risk. WTI oil surged more than 36% in the five days after the initial shock. Despite the hit to supply, the S&P 500 is down just 2.0% and energy stocks are up only 1.0%. These moves suggest markets see a temporary oil supply shock, not a broader crisis. If it were systemic, equities would sell off more sharply and energy would rally harder.

Our research supports this. After five‑day oil spikes of 20%+, equities have typically risen while oil prices declined. Since the 1980s, the median six‑month S&P 500 gain is about 6% as oil has fallen nearly 12% following such shocks.

Historically, equities have looked right through oil shocks and geopolitics — and we expect the same this year as Middle East shipping normalizes and markets refocus on oversupply combined with softer long‑term demand. It’s a reminder: emotion-driven investing doesn’t pay because markets often tune out oil headlines that tend to rattle investors.

898673 Exp : 09 March 2027

YOU MIGHT ALSO LIKE

Markets are reacting to the Middle East conflict with sharp moves across asset classes, signaling broad risk repricing and shifting safe‑haven behavior. While volatility is elevated, fundamentals like earnings growth continue to support our constructive outlook.

Credit spreads have risen yet remain historically low, reinforcing our view that the oil shock is likely temporary — not a driver of long-term growth concerns.

Geopolitical tensions have lifted oil prices, sent U.S. stocks slightly lower and driven flows into the safety of the U.S. dollar, which has strengthened versus peers. While a weaker dollar previously supported international equity outperformance, dollar stabilization now suggests that tailwind is fading, underscoring the importance of diversification across regions and asset classes.

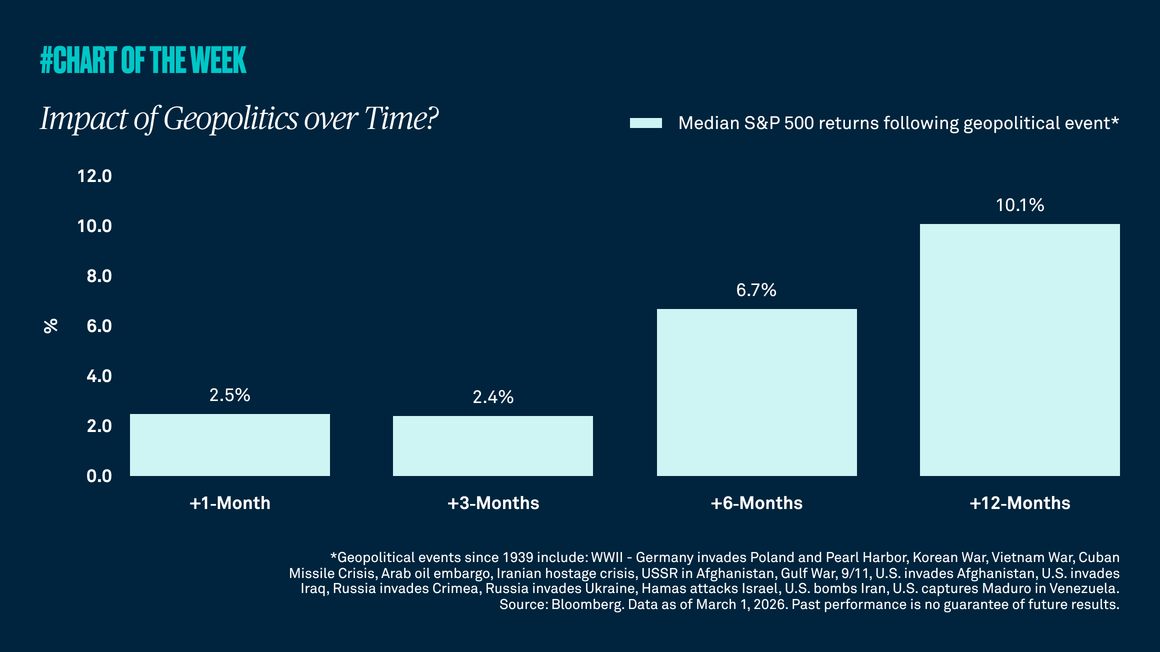

Tensions between the U.S./Israel and Iran have recently boiled over into a military conflict, which has given many investors the jitters. However, our research shows that equity market pullbacks resulting from geopolitical events are often short lived with the S&P 500 typically higher in the months following these events.