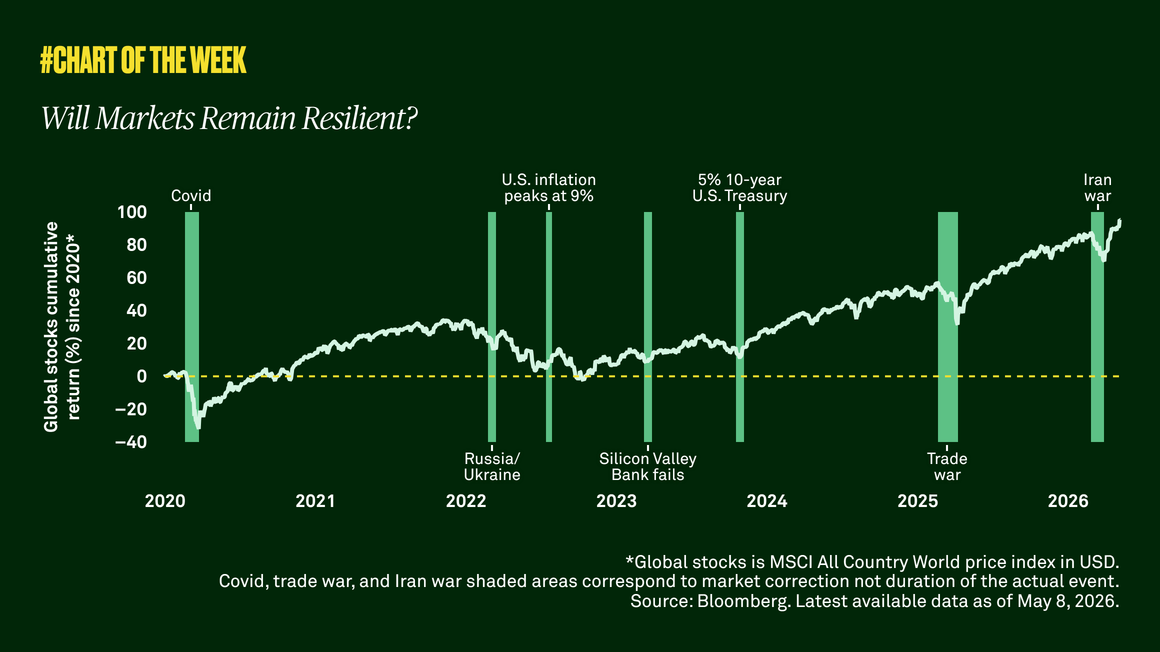

Will markets remain resilient?

Global equities have risen an annualized 11% since 2020 despite repeated shocks, as resilient growth and earnings have helped markets recover from periods of volatility. While the U.S.-Iran conflict poses near-term inflation and growth risks, markets remain constructive as earnings expectations continue to improve.

Since 2020, global equities have delivered strong gains of an annualized 11% even after absorbing a series of shocks, including the pandemic, the Russia-Ukraine war, inflation spikes, aggressive central bank rate hikes, and tariffs. Each of these events drove volatility and selloffs, but markets repeatedly recovered as growth proved more durable than anticipated and investors continued to look through near-term turbulence.

Now, with the U.S. entangled in conflict with Iran, investors face a geopolitical shock that could push energy prices higher, reignite inflation and weigh on global growth in the near term. Even so, markets appear to be pricing this as a temporary event rather than the start of something associated with a longer downturn.

In the U.S., resilient economic growth and stronger-than-expected earnings are supporting higher equity prices this year despite these risks. A renewed inflation wave or disappointing returns on AI-related capital spending could still pressure profits and growth, but for now, earnings expectations are increasing. As a result, we believe risk sentiment in the U.S. and globally remain constructive.

935825 Exp : 12 May 2027

YOU MIGHT ALSO LIKE

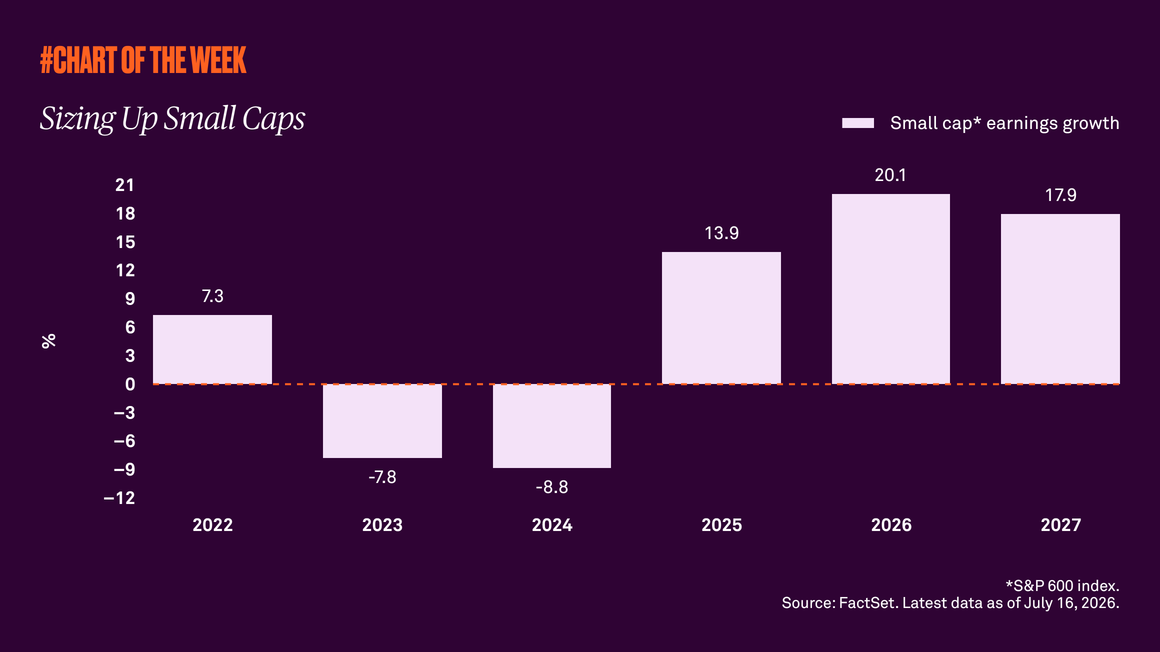

Small caps have outperformed this year despite the threat of higher interest rates, suggesting the rally is being driven by more than just diversification away from large cap tech stocks. Improving earnings expectations and a resilient U.S. economy support our view that small caps have further upside from here.

Signs from sales

Signs from Sales

Year-to-date stock market returns have been driven by robust earnings growth. But when assessing the equity outlook, it’s important to ask what’s supporting the strong earnings trend.

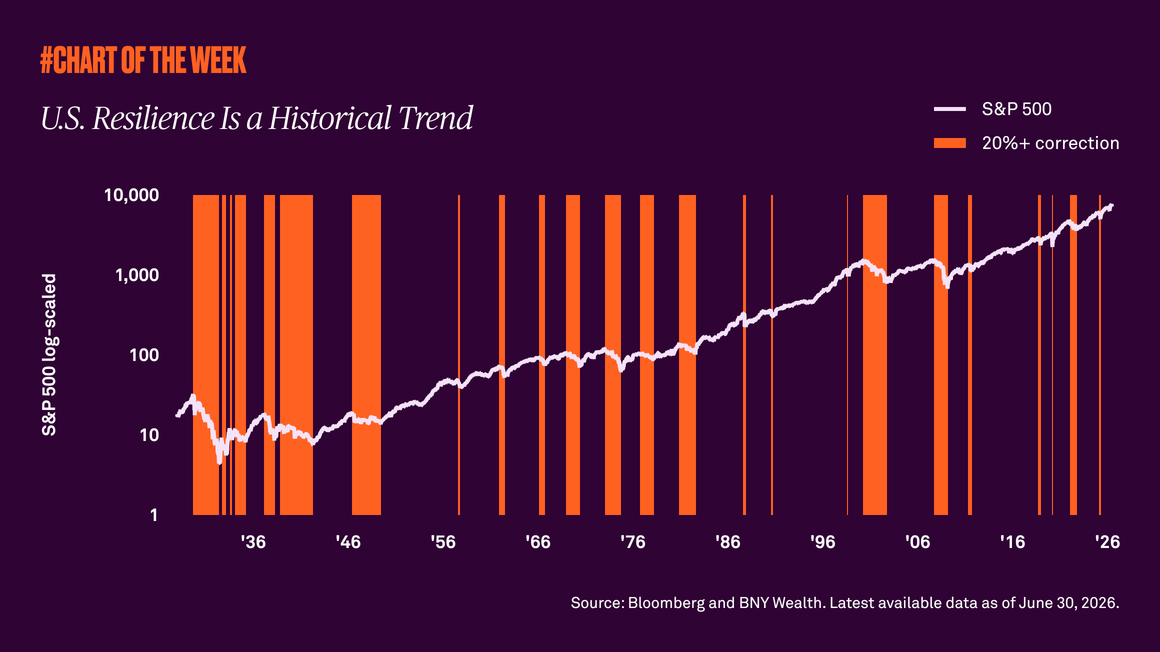

The S&P 500’s history shows that despite recessions, wars, inflation, and corrections, the market’s long-term trajectory has remained upward. As the U.S. marks 250 years of resilience, the lesson for investors is clear: wealth is built through patience, discipline and staying invested.

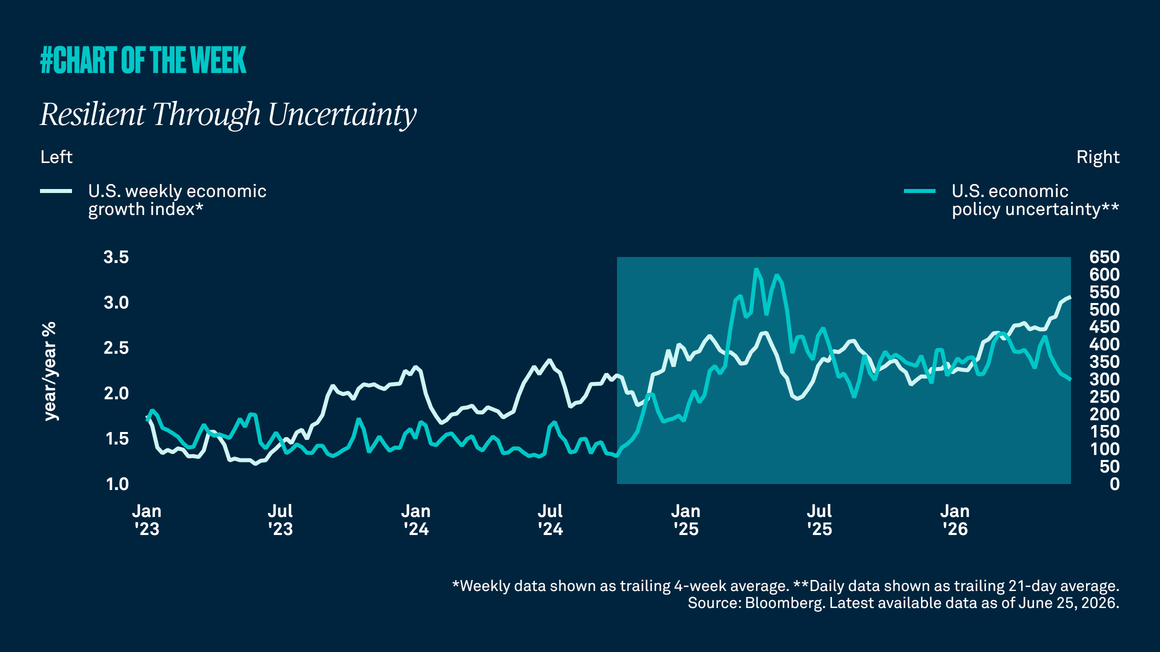

U.S. policy uncertainty has remained elevated and consumer sentiment has weakened. Even so, the economy has stayed resilient, and because growth has held up better than sentiment and headlines suggest, we continue to forecast 2% U.S. growth in 2026, in line with trend.