Managing sequence-of-returns risk in retirement portfolios

Decisions for clients approaching retirement or in retirement have become more complex in the wake of the 2015 “pension freedoms” in the UK. This is particularly so for clients who do not want to buy an annuity and want to retain the flexibility and access to capital that an invested solution can provide.

The Financial Conduct Authority’s (FCA) thematic review of retirement income advice (TR24/1) – published in 2024 amid the seismic shift towards retirement income solutions – shone a spotlight on the need for advisers to consider having a clear withdrawal (income) strategy for clients in the decumulation phase, as well as a risk-profile appropriate investment strategy.1

A focus on the decumulation stage – when clients are no longer accumulating savings and are generating a retirement income through selling assets or taking a Natural Income – remains timely.2 Many clients still harbour fears about running out of money in retirement and look for a solution that addresses not only their specific needs and the financial market uncertainties that lie ahead, but one that is readily understandable to them.

In the view of the FCA, some advisory firms have adapted well to the post 2015 “pension freedoms” landscape, but some are not effectively considering sustainability of income withdrawal (e.g., are not using cash flow modelling or not using it in a consistent or appropriate manner, or are determining income withdrawals without fully considering individual circumstances or using justified assumptions). The FCA’s concern is that many firms blur the line between accumulation and decumulation, fail to differentiate their retirement process meaningfully and use the same investment propositions and fund selections at retirement as during the accumulation phase.

Navigating a sea of uncertainty

Clearly, decisions for clients approaching or in retirement have become more complex. This is particularly so for clients who do not want to buy an annuity and want to retain the flexibility and access to capital that an invested solution can provide.

One complexity relating to retirement income investing is the array of unknowns. Investment markets and the economic environment are inherently uncertain; clients may have some idea of the income they are likely to need, but this may change due to inflation or changes in circumstances; tax rates and regulations change; and so on.

One way to think about investing for retirement income is to focus on two key areas of decision-making:

- How assets are invested to support retirement income for those approaching or in retirement.

- The withdrawal strategy – how much income is taken, when it is taken and where it is taken from.

These two aspects of retirement advice are closely connected. However, we also need to focus on the more often-used approach of selling assets to generate income - specifically, the sequence in which assets are sold to generate income.

The sequence in which assets are sold – which can also be thought of as the sequence of withdrawals – has a direct bearing on income sustainability in retirement. For instance, in a worst-case scenario, selling risk assets at a time of depressed valuations may result in the client exhausting their capital earlier than expected or having to reduce future income to ensure that they do not.

Sequence of returns risk, or sequencing risk for short, was a much-discussed topic when the subject of freer access to pension savings was mooted in 2014, then resurfacing as a major topic in 2022 when equity and bond markets fell sharply while inflation spiked. Clients were suddenly faced with needing to take a higher income from a much-reduced pool of assets.

So, how can we mitigate sequencing risk? Here are some thoughts that may help.

Portfolios balancing growth with capital loss buffers

Reducing the impact of early negative returns (which, combined with withdrawals can accelerate capital losses and threaten retirement income sustainability), is particularly important to mitigate withdrawal risk.

If we can build a portfolio that can grow while also reducing the potential for capital losses and/or the size of potential losses, then only a smaller proportion of total capital will need to be sold to generate a certain level of income. This results in capital lasting longer.

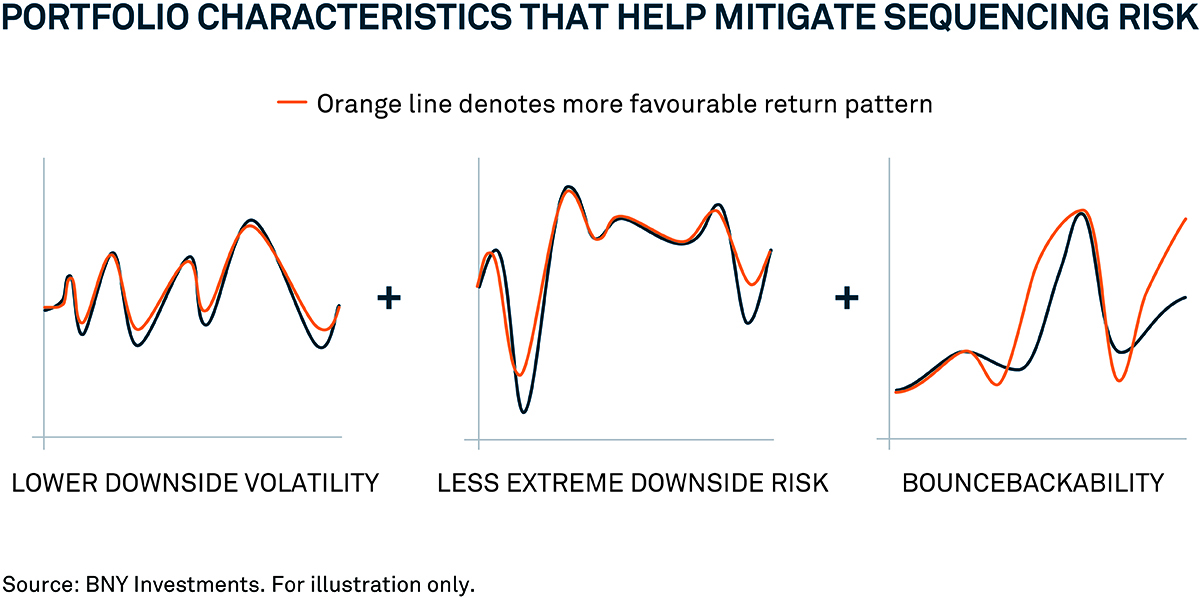

In our view, such a portfolio will need to consider three characteristics relating to loss mitigation: the downside volatility of assets, the absolute extent of the downside risk and how quickly an asset can recover following a market fall.

We need to consider not just how far capital values fall, but how long they remain depressed. The longer it takes to recover from a market fall, the longer we spend selling assets at reduced prices to fund income, which will eat further into capital.

Also, assets that have higher downside risk but have better “bouncebackability” – that is, they recover more quickly after a market fall – may be preferable to assets with less downside risk but which recover more slowly.

Building portfolios that capture all these characteristics is not easy. Simply reducing equity exposure to limit volatility and downside risk could be counterproductive as this could reduce return potential and the ability to match inflation over the medium to long term.

These considerations were at the forefront of the development of BNY’s multi-asset, dynamically managed retirement income fund range (FutureLegacy). The funds in the range align to different Dynamic Planner risk profiles – facilitating ease of use in planning – and are designed with flexibility in mind: each can be used as a standalone vehicle or as a complementary building block in UK-advised retirement income strategies.3

Buffers and buckets: Matching investments to income needs

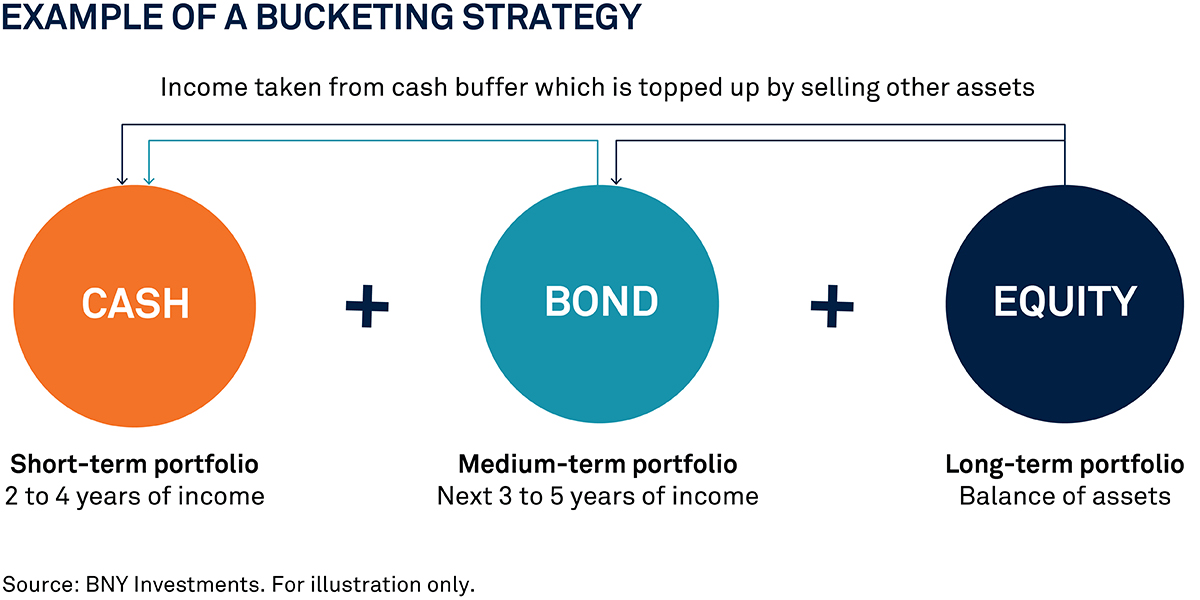

One popular way advisers have sought to mitigate sequencing risk is to use cash buffers and bucketing strategies. A cash buffer is used to provide some protection against sequencing risk by allowing income withdrawals to be made without having to sell assets during times of market stress. Typically, the cash buffer is held in conjunction with a long-term equity allocation though it may also be held alongside an income-generating investment strategy.

According to recent research from BNY/NextWealth, half of all UK advisers use a cash buffer of one to two years of income, with only 9% of advisers not using them at all.4 Typically, income is taken from the cash buffer and then the buffer is topped up by selling other investments either systematically, as part of a broader portfolio review, depending on certain conditions such as a certain rate of return having been achieved, or based on market conditions.

Bucketing strategies take this idea a step further by dividing the growth portfolio into two or more “buckets” alongside the cash buffer.

Again, the aim is to match a client’s income requirements with investments of appropriate risk given when the income will be taken.

Cash is used for income that will be needed in the near term. Bonds, or bond-oriented portfolios, will be used for income that is needed in the medium term. The expectation is that these assets will generate better returns than cash but can reasonably be relied upon to protect capital value over the medium term. Remaining assets are invested in more volatile assets with higher growth potential, to generate returns over the medium to long term.

In a future article, we will dive into some practical guidance on using buffers and buckets strategies. We will look at both the pros as well as some significant implementation pitfalls that can result in worse outcomes than if a multi-asset portfolio with a comparable asset allocation was used.

BNY Mellon FutureLegacy funds – key investment risks

- Objective/Performance Risk: There is no guarantee that the Fund will achieve its objectives.

- Currency Risk: This Fund invests in international markets which means it is exposed to changes in currency rates which could affect the value of the Fund.

- Derivatives Risk: Derivatives are highly sensitive to changes in the value of the asset from which their value is derived. A small movement in the value of the underlying asset can cause a large movement in the value of the derivative. This can increase the sizes of losses and gains, causing the value of your investment to fluctuate. When using derivatives, the Fund can lose significantly more than the amount it has invested in derivatives.

- Changes in Interest Rates & Inflation Risk: Investments in bonds/money market securities are affected by interest rates and inflation trends which may negatively affect the value of the Fund.

- Credit Ratings and Unrated Securities Risk: Bonds with a low credit rating or unrated bonds have a greater risk of default. These investments may negatively affect the value of the Fund.

- Credit Risk: The issuer of a security held by the Fund may not pay income or repay capital to the Fund when due.

- Emerging Markets Risk: Emerging Markets have additional risks due to less-developed market practices.

- Share Class Currency Risk: Where a share class is denominated in a different currency from the base currency of the Fund, changes in the exchange rate between the share class currency and the base currency may affect the value of your investment.

- China Interbank Bond Market and Bond Connect risk: The Fund may invest in China interbank bond market through connection between the related Mainland and Hong Kong financial infrastructure institutions. These may be subject to regulatory changes, settlement risk and quota limitations. An operational constraint such as a suspension in trading could negatively affect the Fund's ability to achieve its investment objective.

- Volcker Rule Risk: The Bank of New York Mellon Corporation or one of its affiliates ("BNYM") has invested in the Fund. As a result of restrictions under the "Volcker Rule," which has been adopted by U.S. Regulators, BNYM must reduce its shareholding percentage so that it constitutes less than 25% of the Fund within, generally, three years of the Fund's establishment (which starts when the Fund's manager begins making investments for the Fund). Risks may include: BNYM may initially own a proportionately larger percentage of the Fund, and any mandatory reductions may increase Fund portfolio turnover rates, resulting in increased costs, expenses and taxes. Details of BNYM's investment in the Fund are available upon request.

- CoCos Risk: Contingent Convertible Securities (CoCos) convert from debt to equity when the issuer's capital drops below a pre-defined level. This may result in the security converting into equities at a discounted share price, the value of the security being written down, temporarily or permanently, and/or coupon payments ceasing or being deferred.

- Responsible Investing Risk: The investment policy for this Fund places restrictions on its exposure to certain sectors or types of investments to reflect its responsible investing approach. The Fund's performance may be negatively impacted due to these restrictions in comparison to funds which do not have these restrictions. The Fund will not engage in securities lending activities and, therefore, may forego any additional returns that may be produced through such activities.

- Counterparty Risk: The insolvency of any institutions providing services such as custody of assets or acting as a counterparty to derivatives or other contractual arrangements, may expose the Fund to financial loss.

BNY Mellon FutureLegacy 3 Fund

Investment Objective: To achieve capital growth and potential for income over the long term (5 years or more) while being managed to a pre-defined level of risk. The Fund will aim to maintain a risk profile classification of 3 from a scale of 1 (lowest) to 10 (highest) which is assessed against the risk ratings scale provided by an external third-party risk rating agency.

Performance Benchmark: The Fund is actively managed without benchmark-related constraints. The Fund will measure its performance against the Investment Association's Mixed Investment 0-35% Shares NR Sector Average as a comparator benchmark (the "Benchmark"). The Fund will use the Benchmark as an appropriate comparator because it includes a broad representation of funds with levels of equity and bond exposure similar to those of the Fund.

Effective 1 August 2025, the Fund’s benchmark changed from 15% SONIA GBP, 55% ICE BofA Global Broad Index GBP Hedged and 30% MSCI ACWI GBP NR to the Investment Association's Mixed Investment 0-35% Shares NR sector average. Benchmark performance shown for all time periods is that of the Investment Association's Mixed Investment 0-35% Shares NR sector average.

BNY Mellon FutureLegacy 4 Fund

Investment Objective: To achieve capital growth and potential for income over the long term (5 years or more) while being managed to a pre-defined level of risk. The Fund will aim to maintain a risk profile classification of 4 from a scale of 1 (lowest) to 10 (highest) which is assessed against the risk ratings scale provided by an external third-party risk rating agency.

Performance Benchmark: The Fund is actively managed without benchmark-related constraints. The Fund will measure its performance against the Investment Association's Mixed Investment 20-60% Shares NR Sector Average as a comparator benchmark (the "Benchmark"). The Fund will use the Benchmark as an appropriate comparator because it includes a broad representation of funds with levels of equity and bond exposure similar to those of the Fund.

Effective 1 August 2025, the Fund’s benchmark changed from 10% SONIA GBP, 45% ICE BofA Global Broad Index GBP Hedged and 45% MSCI ACWI GBP NR to the Investment Association's Mixed Investment 20-60% Shares NR sector average. Benchmark performance shown for all time periods is that of the Investment Association's Mixed Investment 20-60% Shares NR sector average.

BNY Mellon FutureLegacy 5 Fund

Investment Objective: To achieve capital growth and potential for income over the long term (5 years or more) while being managed to a pre-defined level of risk. The Fund will aim to maintain a risk profile classification of 5 from a scale of 1 (lowest) to 10 (highest) which is assessed against the risk ratings scale provided by an external third-party risk rating agency.

Performance Benchmark: The Fund is actively managed without benchmark-related constraints. The Fund will measure its performance against the Investment Association's Mixed Investment 40-85% Shares NR Sector Average as a comparator benchmark (the "Benchmark"). The Fund will use the Benchmark as an appropriate comparator because it includes a broad representation of funds with levels of equity and bond exposure similar to those of the Fund.

Effective 1 August 2025, the Fund’s benchmark changed from 5% SONIA GBP, 35% ICE BofA Global Broad Index GBP Hedged and 60% MSCI ACWI GBP NR to the Investment Association's Mixed Investment 40-85% Shares NR sector average. Benchmark performance shown for all time periods is that of the Investment Association's Mixed Investment 40-85% Shares NR sector average.

BNY Mellon FutureLegacy 6 Fund

Investment Objective: To achieve capital growth and potential for income over the long term (5 years or more) while being managed to a pre-defined level of risk. The Fund will aim to maintain a risk profile classification of 6 from a scale of 1 (lowest) to 10 (highest) which is assessed against the risk ratings scale provided by an external third-party risk rating agency.

Performance Benchmark: The Fund is actively managed without benchmark-related constraints. The Fund will measure its performance against the Investment Association's Mixed Investment 40-85% Shares NR Sector Average as a comparator benchmark (the "Benchmark"). The Fund will use the Benchmark as an appropriate comparator because it includes a broad representation of funds with levels of equity and bond exposure similar to those of the Fund.

Effective 1 August 2025, the Fund’s benchmark changed from 25% ICE BofA Global Broad Index GBP Hedged and 75% MSCI ACWI GBP NR to the Investment Association's Mixed Investment 40-85% Shares NR sector average. Benchmark performance shown for all time periods is that of the Investment Association's Mixed Investment 40-85% Shares NR sector average.

BNY Mellon FutureLegacy 7 Fund

Investment Objective: To achieve capital growth and potential for income over the long term (5 years or more) while being managed to a pre-defined level of risk. The Fund will aim to maintain a risk profile classification of 7 from a scale of 1 (lowest) to 10 (highest) which is assessed against the risk ratings scale provided by an external third-party risk rating agency.

Performance Benchmark: The Fund is actively managed without benchmark-related constraints. The Fund will measure its performance against the Investment Association's Flexible Investment NR Sector Average as a comparator benchmark (the "Benchmark"). The Fund will use the Benchmark as an appropriate comparator because it includes a broad representation of funds with levels of equity and bond exposure similar to those of the Fund.

Effective 1 August 2025, the Fund’s benchmark changed from 10% ICE BofA Global Broad Index GBP Hedged and 90% MSCI ACWI GBP NR to the Investment Association's Flexible Investment NR sector average. Benchmark performance shown for all time periods is that of the Investment Association's Flexible Investment NR sector average.

Important information

This is a financial promotion. For Professional Clients only.

Any views and opinions are not investment advice or a research recommendation.

BNY is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally.

BNY Mellon Investment Funds is an open-ended investment company with variable capital (ICVC) with limited liability between sub-funds. Incorporated in England and Wales: registered number IC27. The Authorised Corporate Director (ACD) is BNY Mellon Fund Managers Limited (BNY MFM), incorporated in England and Wales: No. 1998251. Registered address: BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Authorised and regulated by the Financial Conduct Authority.

Issued in the UK by BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority.

Disclosures

The value of investments and the income received can fall as well as rise and investors may not get back the original amount invested.

Please refer to the prospectus, KID/KIID or KFS where applicable and other fund documents for a full list of risks and before making any investment decisions. Documents are available in English and in selected local languages where the fund is registered. Go to bny.com/investments.

The BNY Mellon FutureLegacy funds are actively managed typically by using forward-looking expectations of volatility. In doing so, the Investment Manager uses its own internal risk model, whilst also considering external independent risk profiling methodologies. Based on a risk profile scale of 1 (lowest) to 10 (highest), the funds target a risk profile of 3, 4, 5, 6 or 7 but this is not guaranteed. The risk profile targeted by each of these funds can be identified through the number included in the respective fund name. This risk profile is not the same as the risk and reward category shown in the KIID. The risk profiles are assessed against the risk rating scale provided by Dynamic Planner but are subject to change.

Dynamic Planner Risk Ratings should not be used for making an investment decision and it does not constitute a recommendation or advice in the selection of a specific investment or class of investments.

The funds can invest more than 35% of net assets in different transferable securities and money market instruments issued or guaranteed by the UK or an EEA State, its local authorities, a third country or public international bodies of which the UK or one or more EEA States are members.

1Financial Conduct Authority, Thematic Review TR24/1, Retirement income advice thematic review, March 2024

2Natural income is where the client’s income comes from the income generated by the underlying assets.

3The BNY Mellon FutureLegacy funds are actively managed, typically by using forward-looking expectations of volatility. In doing so, the Investment Manager uses its own internal risk model, while also considering external independent risk profiling methodologies. Based on a risk profile scale of 1 (lowest) to 10 (highest), the funds target a risk profile of 3, 4, 5, 6 or 7, but this is not guaranteed. The risk profile targeted by each of these funds can be identified through the number included in the respective fund name. This risk profile is not the same as the risk and reward category shown in the KIID. The risk profiles are assessed against the risk rating scale provided by Dynamic Planner but are subject to change. Dynamic Planner Risk Ratings should not be used for making an investment decision and it does not constitute a recommendation or advice in the selection of a specific investment or class of investments.

4Source: Research conducted by NextWealth for BNY Investments, based on responses to surveys with 207 retirement-focused financial advisers and 260 consumers of financial advice conducted in November 2025. “When investing to support retirement income, to what extent do you use a cash buffer (i.e. allocating part of the portfolio to cash to support income payments)?”

RELATED FUNDS

Easy access to our funds and related content

BNY Mellon FutureLegacy 3 Fund (UK domiciled)

BNY Mellon FutureLegacy 4 Fund (UK domiciled)

BNY Mellon FutureLegacy 5 Fund (UK domiciled)

BNY Mellon FutureLegacy 6 Fund (UK domiciled)

BNY Mellon FutureLegacy 7 Fund (UK domiciled)

3301859 Exp : 30 June 2027

YOU MIGHT ALSO LIKE

The retirement landscape is evolving rapidly. While today’s retirees may appear much the same as before, their financial resources and confidence are shifting significantly. As reliance on traditional, secure income sources like defined benefit schemes and personal pensions declines, responsibility increasingly falls on individuals to manage their own retirement outcomes. This shift presents new challenges—and opportunities—for financial advisers.

Retirement planning in the UK has never stood still, but the ground is shifting more quickly and more meaningfully than many clients – and some firms – might expect.

Market shifts, rising risks and AI-driven volatility are challenging retirement income stability. BNY Investments Newton multi-asset portfolio manager Paul Byrne discusses why dynamic risk management and active multi-asset strategies are essential for steadying the ship.

With artificial intelligence evolving at pace, is it finally ready to enhance how advisers plan, test and deliver retirement strategies?