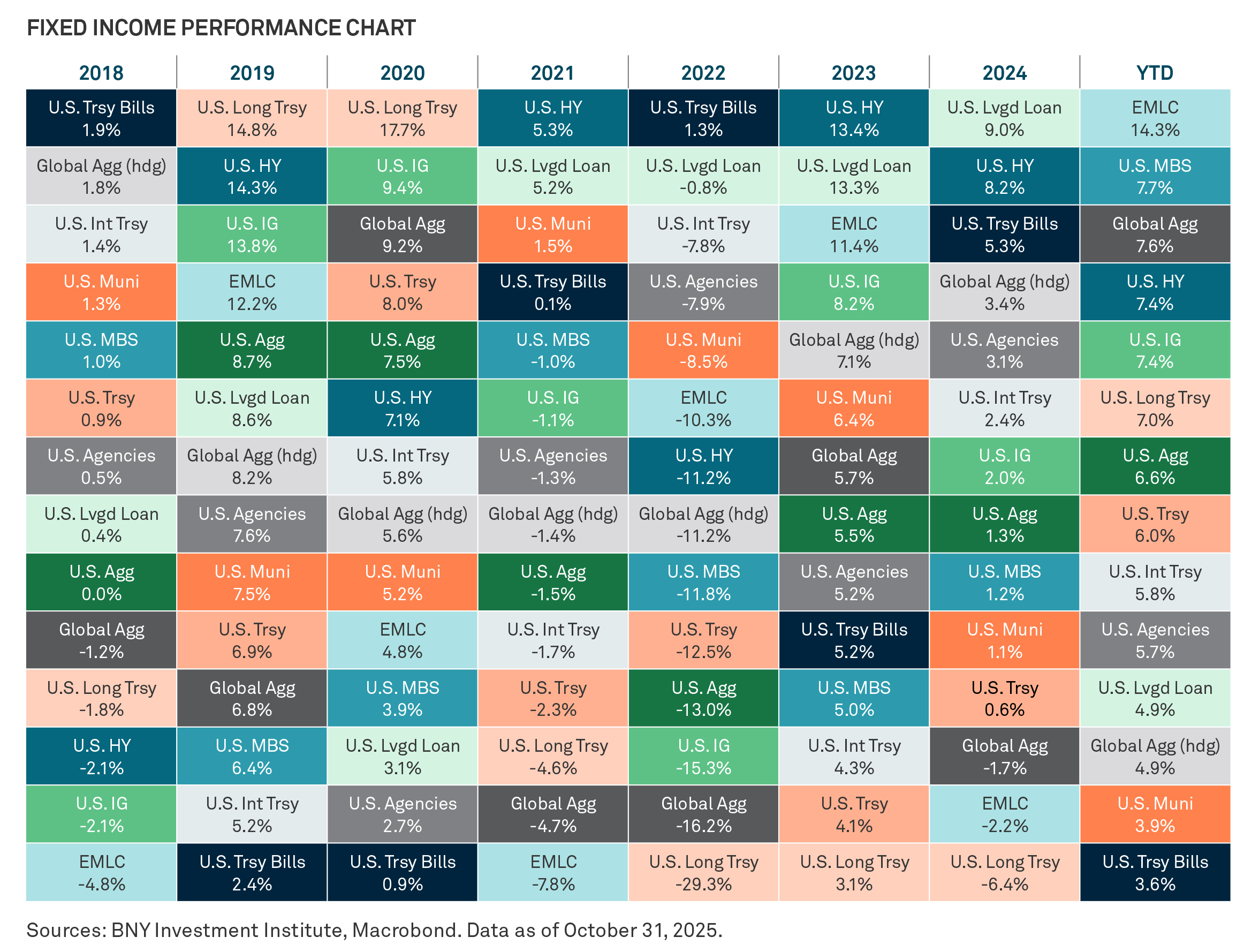

Musical Chairs in Fixed Income

Leaders rotate in and out. No single fixed income sector consistently dominates performance over time, and strong performance in one sector rarely carries over from one year to the next. For example, U.S. Treasury bills led in 2018 and 2022 but are one of the weakest performers year-to-date.

Meanwhile, emerging markets local debt and global bonds, two of 2024’s worst performing sectors, have topped performance so far this year. Timing fixed income markets and predicting which sector will lead next is extremely difficult.

The key takeaway: diversification is essential. A well-balanced and active fixed income strategy with diverse exposure across sectors, credit, and geography may provide ballast to equities, be a potential source of income, and help mitigate risk.

This is an extract from Checkpoints, a comprehensive monthly chartbook that provides insights into major themes affecting financial markets. For additional analysis, read the full report.

About the BNY Investment Institute

Drawing upon the breadth and expertise of BNY Investments, the Investment Institute generates thoughtful insights on macroeconomic trends, investable markets and portfolio construction.

GLOSSARY

EM Local Currency Government 10% Country Capped: The Bloomberg EM Local Currency Government 10% Country Capped Index is a country-constrained version of the flagship Emerging Markets Local Currency Government Index, which is designed to provide a broad measure of the performance of local currency emerging markets (EM) debt.

Global Aggregate: The Bloomberg Global Aggregate Total Return (USD hedged) Index is a broad-based measure of the global investment-grade fixed income market.

U.S. Agencies: Bloomberg U.S. Agencies Total Return Unhedged USD measures U.S. dollar–denominated agency debt.

U.S. Aggregate: Bloomberg U.S. Agg Total Return Value Unhedged USD Index is a widely accepted, unmanaged total return index of corporate, government and government-agency debt instruments, mortgage-backed securities and asset-backed securities with an average maturity of 1–10 years.

U.S. Corporates: Bloomberg U.S. Corporate Total Return Value Unhedged USD Index tracks the investment-grade, fixed-rate, taxable corporate bond market.

U.S. High Yield: Bloomberg U.S. Corporate High Yield Total Return Index Value Unhedged USD Index tracks the performance of U.S. dollar–denominated below-investment-grade-rated corporate debt publicly issued in the U.S. domestic market.

U.S. Leveraged Loans: The Morningstar LSTA U.S. Leveraged Loan Index is a market-value weighted index designed to measure the performance of the U.S. leveraged loan market.

U.S. MBS: The Bloomberg U.S. Mortgage Backed Securities (MBS) Index tracks fixed-rate agency mortgage backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA) and Freddie Mac (FHLMC).

U.S. Munis: Bloomberg Municipal Bond Index Total Return Index Value Unhedged USD Index tracks the municipal fixed income market in the United States.

U.S. Treasury: The Bloomberg U.S. Treasury Index is the U.S. Treasury component of the U.S. Aggregate Index and uses public obligations of the U.S. Treasury with a remaining maturity of one year or more.

U.S. Treasury Bills: The Bloomberg U.S. Treasury Bill 3-6 Months Index tracks the market for treasury bills with 3 to 5.9 months to maturity issued by the U.S. government. U.S. Treasury bills are issued in fixed maturity terms of 4, 13, 26 and 52 weeks.

U.S. Treasury Intermediate: The Bloomberg U.S. Treasury Intermediate Index measures U.S. dollar–denominated, fixed-rate, nominal debt issued by the U.S. Treasury with maturities of 1 to 9.9 years to maturity.

U.S. Treasury Long: The Bloomberg U.S. Treasury: Long Index measures U.S. dollar–denominated, fixed-rate, nominal debt issued by the U.S. Treasury with 10 years or more to maturity.

Asset allocation and diversification cannot ensure a profit or protect against a loss.

DISCLAIMER

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy.

Opinions and views expressed are subject to change without notice.

Past performance is no guarantee of future results.

ISSUING ENTITIES

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue Eugène Ruppert L-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia: BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manage and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

© 2025 THE BANK OF NEW YORK MELLON CORPORATION

MARK-841543-2025-11-17

GU-754 Exp : 30 November 2026

YOU MIGHT ALSO LIKE

Insight Investment sees resilience in the global short-dated high yield bond market. Here’s why.

Flexible, low-risk bond strategies that are unconstrained by benchmarks have multiple applications in today’s markets

Fixed income investors are dealing with a choppy, data driven market with rate volatility, inflation uncertainty and mixed growth signals. These dynamics make traditional bonds more sensitive to duration and credit spreads, while tighter lending and sector specific risks continue to add pressure.

AI, resilient trade and a weaker dollar are turning heads towards the countries driving global growth. Emerging economies haven’t looked this promising in years.