In 2025, the passage of the One Big Beautiful Bill Act (OBBBA) permanently increased the federal estate and gift tax exemption, providing greater legislative certainty and new opportunities to preserve wealth across generations. Yet estate planning for ultra-high-net-worth families continues to grow more complex. In BNY’s latest survey of estate planning and tax advisors conducted at the 60th Heckerling Institute on Estate Planning, advisors emphasized the increasing importance of technical expertise amid evolving planning strategies, as well as their clients’ most pressing concerns. The insights that follow highlight where advisors see the greatest planning opportunities and where ultra-high-net-worth clients are focusing their priorities in 2026.

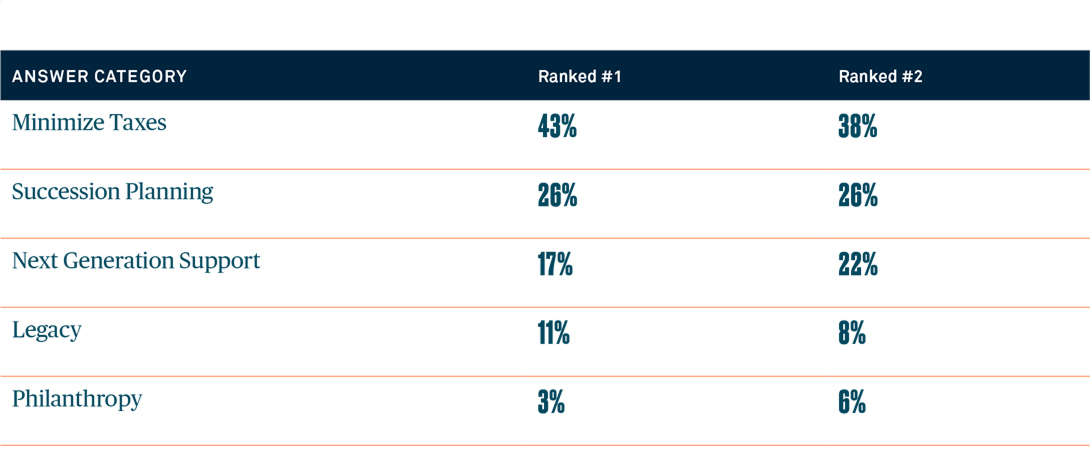

What are the top two concerns expressed by your clients’ around wealth transfer planning heading into 2026?

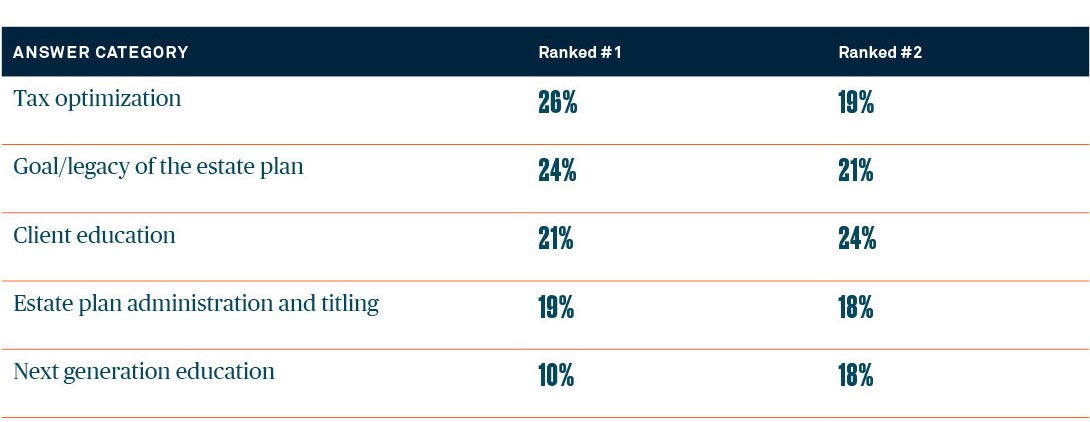

Those polled believe that tax optimization is the best way to support clients when it comes to making sure their estate plan is effective following passage of the OBBBA. Client education, legacy planning, estate plan administration and titling, and next-generation education are other ways to help ultra-wealthy families plan their estates to maximize benefits of the legislation.

Where do you think clients' need the most support in making sure their estate plan is effective following the passing of the OBBBA?

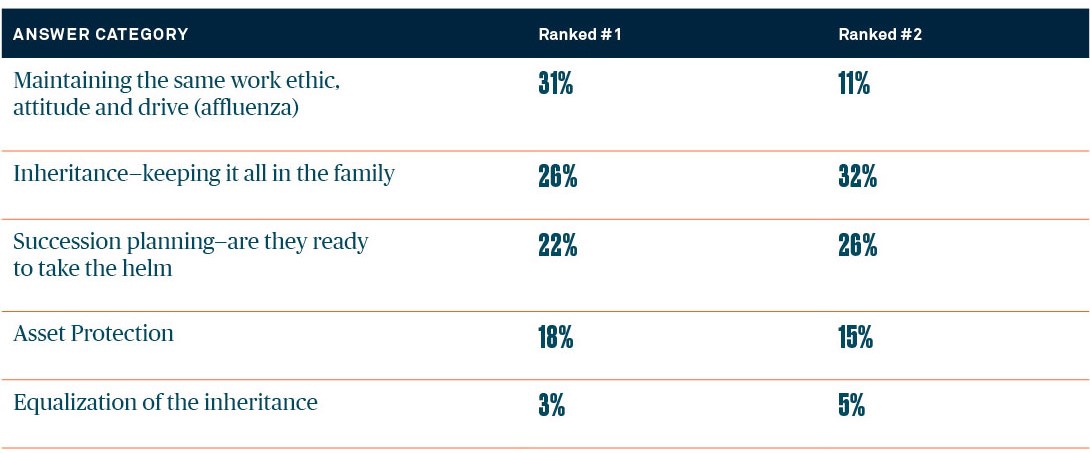

What are your clients' current biggest concerns around next-generation planning?

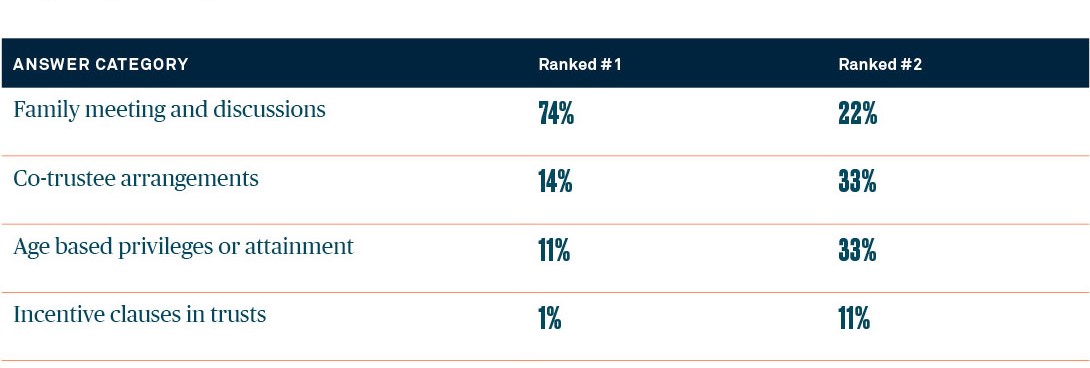

In next-generation planning, one of the biggest concerns professionals identified is “affluenza” — an excessive focus on wealth and material possessions without having to work for them. In other words, there is concern about whether the next generation will maintain the same work ethic, ambition, and drive. Inheritance ranked as their second-largest concern, particularly whether families will be able to preserve their wealth across generations. Additionally, 74% of the advisors we polled said family meetings or discussions were most effective for educating and guiding the next generation.

For the next generation, what trust drafting or financial education approaches do you find most effective in educating and guiding the next generation?

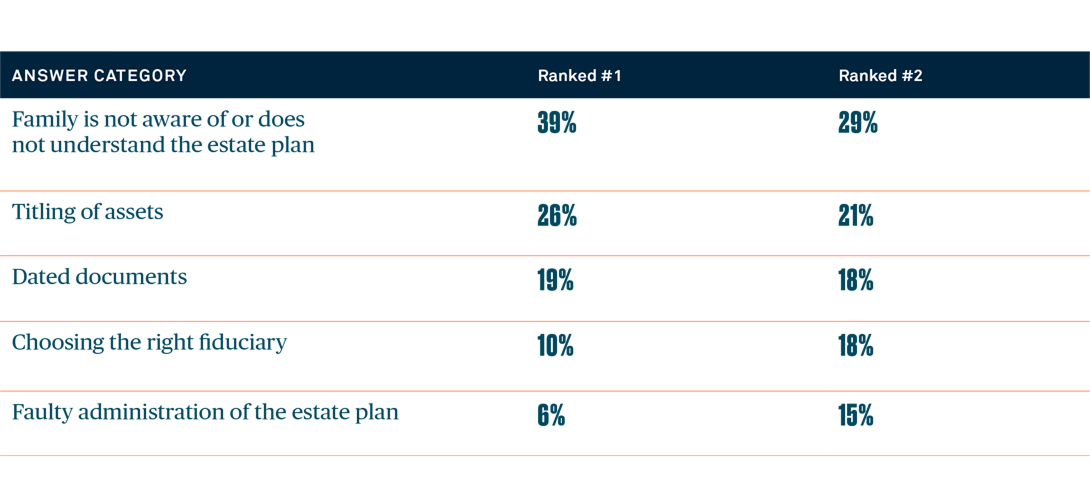

The estate planning professionals surveyed also identified concerns around their clients' estate plans this year.

Focus areas include:

- A lack of awareness or understanding of the estate plan

- Proper titling of assets

- Out-of-date estate planning documents

- Choosing the right fiduciary

Of particular note: 39% of the professionals said that families they work with were not aware of or did not understand their estate plan in 2025.

What are the most common mistakes or issues you’ve seen with your client’s estate plan in the past year?

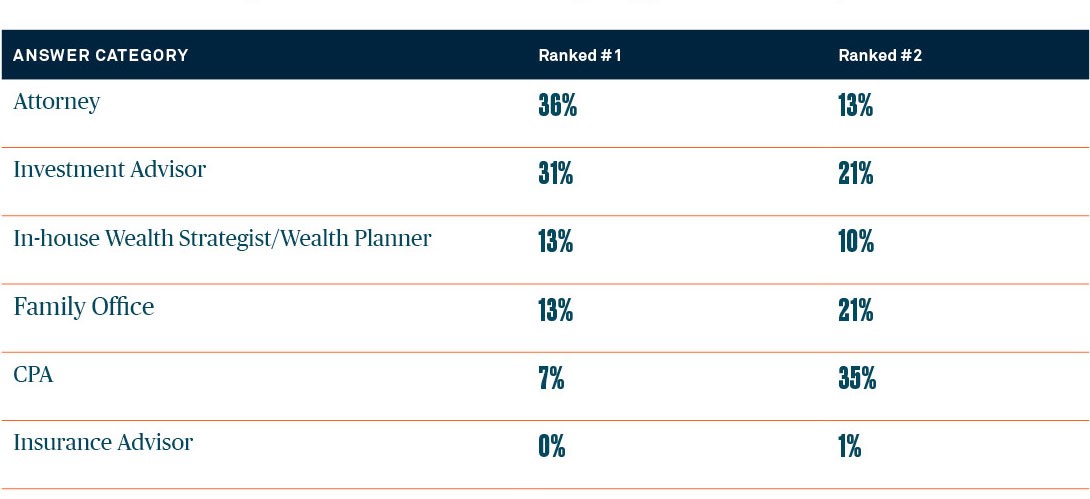

Our survey participants also usually coordinate with an investment advisor, attorney, CPA and family office when working on their clients’ estate plans.

Who are the advisors that you most often coordinate with regarding your client's estate plan?

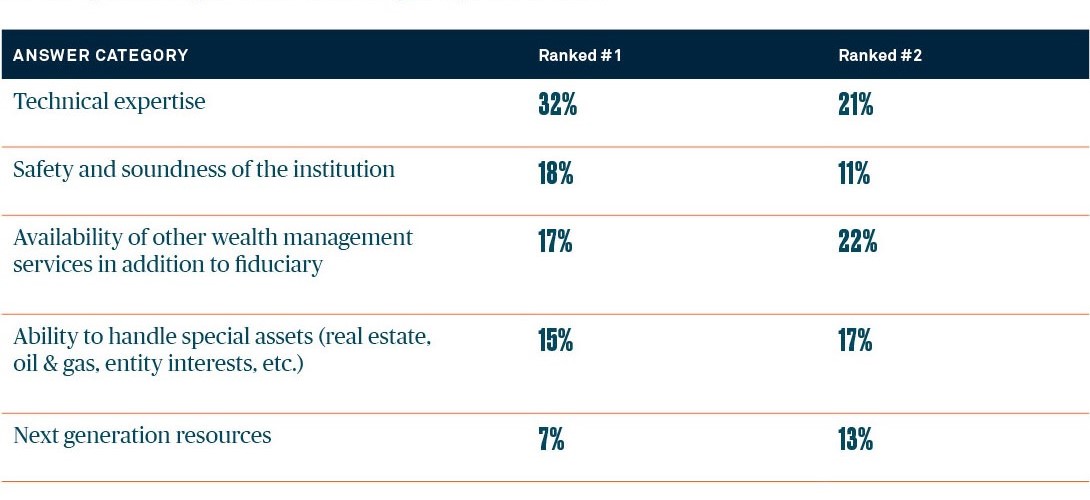

What are you looking for when considering a corporate trustee?

The main attribute when considering a corporate trustee was identified as technical expertise. Safety and soundness, ability to handle special assets, availability of other wealth management services, and next-generation resources are other important corporate trustee considerations.

Why Technical Expertise Matters

Technical expertise is especially important when administering complex trust structures and multigenerational wealth plans. Ultra-wealthy families often hold concentrated business interests, private investments, real estate and other illiquid assets that require careful oversight. A corporate trustee with deep fiduciary, tax and administrative expertise can help ensure trusts are executed according to their governing documents while navigating evolving tax rules, reporting obligations and family dynamics. This level of technical capability helps reduce operational risk and provides continuity across generations.

How BNY Wealth Can Help

Administering trusts for ultra-wealthy families requires deep fiduciary, tax and administrative expertise. BNY Wealth works closely with families and their advisors to deliver disciplined trust administration and integrated wealth management solutions designed to support multigenerational objectives. Contact us to learn more.