While wealthy families have many options for managing assets, those with $250 million or more establish private wealth management firms called family offices, which provides them with more control, privacy and customization.

Family offices deliver centralized oversight of investments, reporting, taxes, philanthropy and more. When structured correctly, they not only preserve wealth but also strengthen family bonds through shared decision-making and long-term stewardship.

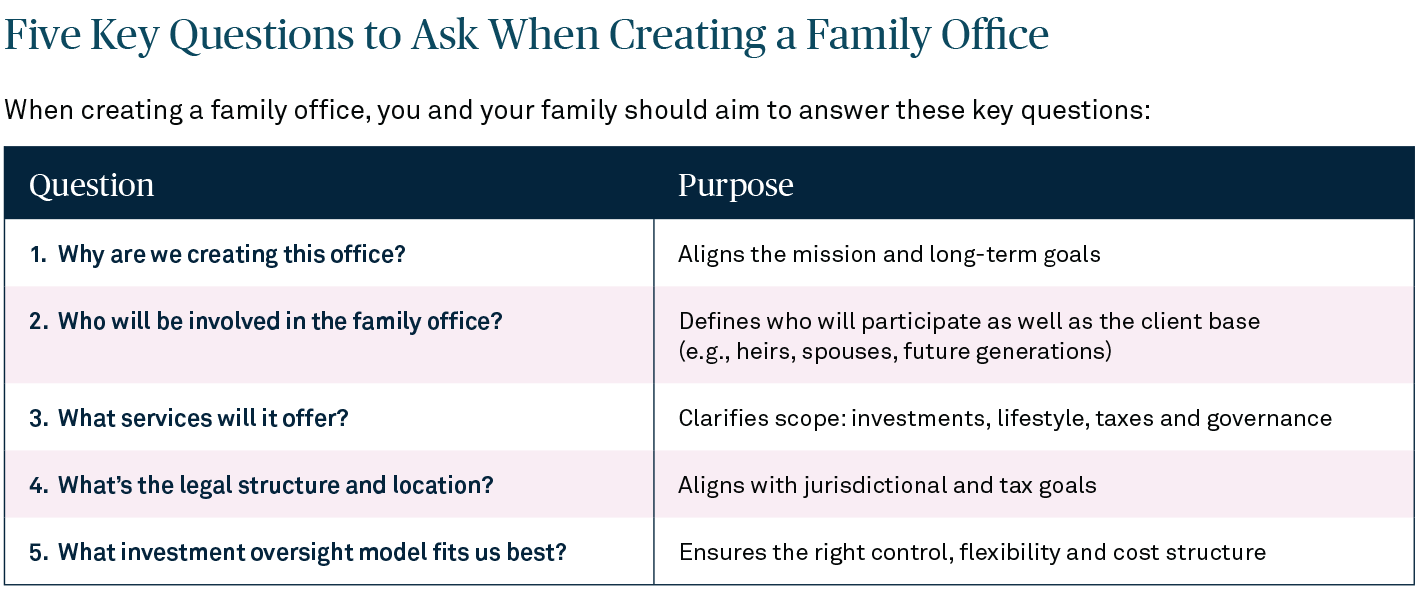

Laying the Foundation

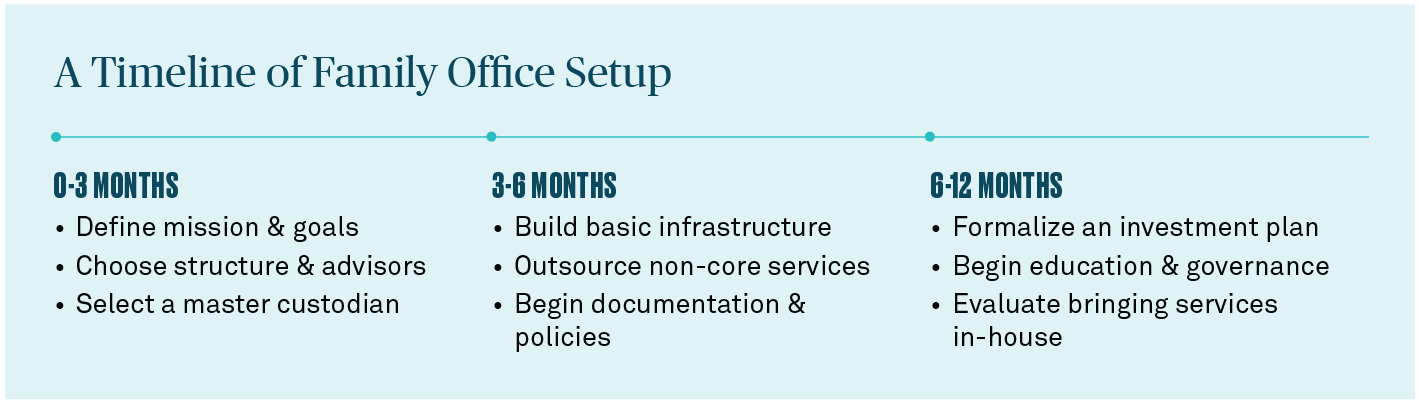

The most effective family offices are established well before a major liquidity event, such as a business sale or generational wealth transfer. Some families spin off a structure from the operating company while others build them from scratch. In either case, advanced planning reduces risk and ensures a smooth execution.

When anticipating a significant liquidity event, it’s critical to identify where the wealth will be held and by whom it will be managed, at least for the first year. Safe custody, institutional-grade reporting and a short-term investment strategy should be decided upon well before the liquidity event.

A phased approach is often most effective. Begin by focusing on core family office functions, such as custody, reporting and consolidated accounting, while outsourcing more specialized services. This will keep early-stage operations efficient and cost-effective. As the family builds confidence, additional capabilities can be brought in-house.

Acting early also provides a practical advantage. Selecting a master custodian in advance ensures assets from a liquidity event flow directly into secure, consolidated accounts overseen by the family office. Families that fail to do this, however, may have to rely on retail solutions, which can complicate asset management and introduce external pressure to retain funds.

Understanding the Cost of Operating a Family Office

A single family office offers tailored governance, investment oversight and operational control. However, it also requires a dedicated operating infrastructure, including professional staff, technology platforms, consolidated reporting systems, compliance oversight and administrative support. These costs reflect the institutional framework required to coordinate complex and often global wealth structures.

Data from the 2026 J.P. Morgan Private Bank Global Family Office Report indicates that operating costs generally increase as family offices expand their capabilities and internal teams. Larger families often build more sophisticated organizations that include investment professionals, governance specialists and enhanced reporting infrastructure.

The report suggests the following approximate annual operating costs across asset levels:

At first glance, one might expect operating costs to decline significantly in basis-point terms as assets grow. In practice, however, the economics are shaped by two structural dynamics.

First, many of the core components of a family office—senior investment professionals, governance structures, reporting infrastructure, and operational oversight—represent largely fixed institutional costs. Two family offices with similar staffing and infrastructure may therefore operate with comparable budgets even if their asset bases differ significantly.

For example, if two family offices each operate with an annual budget of roughly $6.5 million, but one manages $250 million while the other manages $1 billion, the smaller office would operate at approximately 260 basis points, while the larger office would operate at roughly 65 basis points, despite having essentially the same organizational structure.

Second, as wealth grows, families often choose to expand the capabilities of their family office rather than simply dilute fixed costs across a larger asset base. Many large family offices evolve from coordination platforms into institutional investment organizations, adding internal investment teams, direct investment sourcing capabilities, and more robust governance infrastructure.

As a result, some families continue to operate their offices at 50–65 basis points or more, even as their wealth grows substantially.

Importantly, families do not evaluate these costs solely through the lens of investment performance. While some may expect internal investment capabilities to generate incremental alpha, many view the family office primarily as providing a governance premium—strengthening oversight, improving risk management, and enabling better coordination across investment, tax, estate, and generational planning.

In many cases, the greatest value of a family office lies not in generating additional returns, but in avoiding costly mistakes. For families managing substantial wealth, preventing a single poorly structured investment, governance dispute, or tax inefficiency can preserve more value than the annual operating cost of the office itself.

In this sense, the family office should not be viewed solely as an investment management expense, but rather as the institutional infrastructure required to steward wealth across generations.

For many families, the value of a family office lies less in generating alpha and more in avoiding negative alpha.

Where Should You Locate Your Family Office—And What Legal Structure Should You Use?

Choosing the right location and legal structure shapes how your family office operates and accesses opportunities worldwide. Most families start near their business or primary residence, but as the family’s needs evolve, the office may need to adapt.

Key considerations when selecting a location and legal structure include:

• Political stability and rule of law

• Privacy regulations

• Tax and regulatory environment

• Access to skilled staff and advisors

• Availability of preferred legal structures (LLC, FLP, PTC, purpose trust, non-charitable foundation, etc.)

Six Best Practices for Family Office Management

Running a family office requires more than just financial expertise. It calls for strategic planning, strong governance and disciplined operations.

These best practices can help ensure a well-run, enduring enterprise:

1. DEFINE THE FAMILY OFFICE’S MISSION

It’s essential to be clear about why the family office exists. Is the focus on managing investments, facilitating philanthropic giving, preparing the next generation or overseeing wealth transfer? Some offices concentrate on a single goal while others support multiple objectives. A defined mission helps shape everything from staffing and service providers to reporting and decision-making.

2. ESTABLISH GOVERNANCE EARLY

Well-run offices clearly delineate roles and responsibilities between family members, staff and advisors. A governance structure, such as a family council, board or investment committee, can help ensure decisions are made efficiently and reflect the family’s goals. Clear bylaws and policies help reduce ambiguity and support accountability.

3. EDUCATE THE NEXT GENERATION EARLY AND OFTEN

Preparing rising generations to manage wealth is one of the most important—and overlooked—functions of a family office. Education shouldn’t be a one-time seminar or a last-minute handoff. Instead, it should be an ongoing process that builds financial literacy, decision-making skills and a deep understanding of the family’s values and legacy. This may include formal training, mentorship, participation in committees and exposure to the office’s day-to-day operations.

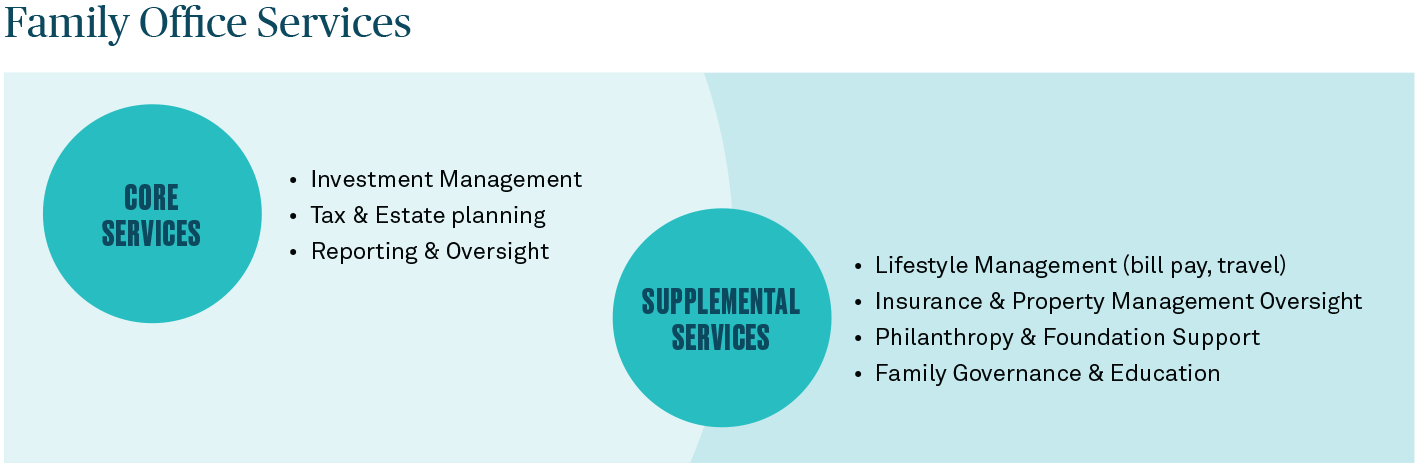

4. CLEARLY DEFINE THE SCOPE OF SERVICES

Family offices can offer a wide range of services, from investment oversight and tax planning to bill pay, trust administration and lifestyle support. Being specific about which services the family office will provide helps set expectations. It also allows the family to identify when additional specialists are needed. And as the family office evolves, revisiting the service menu ensures alignment with the family’s needs and priorities.

5. DEFINE STAFF ROLES AND RESPONSIBILITIES

Written policies that clearly define the roles and responsibilities of each staff member help ensure the family office runs smoothly. These should outline job descriptions, decision-making authority and reporting lines to avoid confusion or overlap. Policies should also include whether family members can be employees of the office.

6. ESTABLISH A TECHNOLOGY ROADMAP

A thoughtful technology roadmap supports the operations, security and reporting needs of a family office. This includes systems for accounting, performance reporting, document management and secure communication.

The Human Capital Equation—Succession and Alignment

Once a family office has been operating for five years or more, a new set of questions arises. How do you ensure leadership continuity? And how do you structure compensation in a way that enables the family office to attract and retain talent, even as it remains aligned with family objectives?

Many successful family offices plan for internal succession and promote talented professionals who understand their family’s values, history and goals. At the same time, external recruitment is common if a family office is looking for specialized expertise, such as CIO leadership, experience with alternative investments, or complex tax issues. Like any corporate enterprise, compensation plays a key role for both attracting, retaining and aligning talent. In addition to base salary, family offices also rely on performance-based incentives, deferred compensation, and even co-investment opportunities as a way to align their professionals with the family’s long-term outcomes.

Regardless of the structure a family office takes, the key best practice is to formalize succession and compensation frameworks as part of governance planning, and to also review them periodically. Doing so will mitigate key-person risk and the family office’s sustainability across generations.

BNY Wealth Global Family Office Can Help

For more than two centuries, we’ve helped families build, manage and preserve wealth through initial liquidity events, family office creation and generational transitions. Backed by BNY, our Global Family Office Group delivers tailored solutions to help navigate the complexities of exceptional wealth.