For families who want to build and protect wealth across generations, a Family Limited Partnership (FLP) or a Family Limited Liability Company (FLLC) may be the best solution. These legal structures help ensure assets remain within the family while offering benefits like tax savings, asset protection and streamlined succession planning.

What Is a Family Limited Partnership (FLP)?

An FLP is a legal entity typically owned by family members, such as spouses, parents, children or other descendants. A trust set up for the benefit of family members can also serve as a limited partner. FLPs allow families to consolidate ownership of businesses, real estate, marketable securities or other assets, making it easier to manage those assets and pass them onto future generations. In addition to providing structure, FLPs help families pool their resources to fund new ventures, grow existing businesses or manage long-term investments.

How an FLP is structured

- General Partner (GPs): These partners manage the FLP’s operations and make key decisions. GPs are usually the parents or founders, who contribute most of the assets. They retain control of day-to-day management tasks, business activities and critical decisions.

- Limited Partners (LPs): LPs are passive owners with an economic interest in the partnership but no control over management or decision-making. LP interests are often held by the parents, children, grandchildren or trusts established for the benefit of descendants.

The partnership agreement details how the FLP will operate, including the roles of each partner, management guidelines and terms for transferring interests. Since every family’s situation is unique, it is critical to work with qualified legal and tax advisors to create an agreement that aligns with the family’s goals while protecting their interests.

Preserving Control, Saving Taxes

An additional benefit of consolidating assets in an FLP is the ability to gift LP units to family members or family trusts. Typically, the senior generation creates the FLP and contributes assets in exchange for GP and LP interests. Over time, they can gift LPv interests to their children, grandchildren or trusts established for their benefit.

When such gifts are made, either during life or as part of an estate event, questions often arise about how to properly value the interests. Under current law, the standard for determining value is what a willing buyer and a willing seller—both with reasonable knowledge of the facts and under no pressure to transact—would pay for the interests.

Decades of case law have clarified that because LP units typically lack marketability and control, their value is often discounted compared to the proportional value of the partnership’s assets. As a result, qualified appraisers frequently apply valuation discounts. This creates an opportunity to transfer wealth to future generations at a value below the full market value of the underlying assets, which helps to reduce estate and gift taxes.

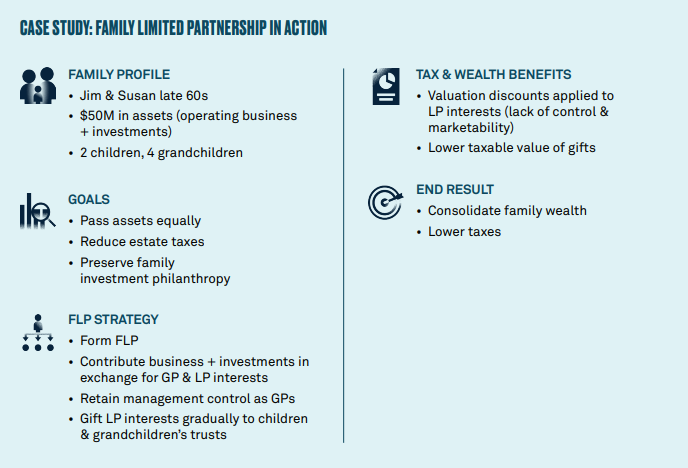

Transferring an Operating Business

To see how an FLP might work in practice, consider the following example:

As illustrated with Jim and Susan, a Family Limited Partnership can be a flexible way for families to consolidate assets, manage wealth across generations, and reduce potential estate and gift tax liabilities.

By working with experienced legal, tax and valuation professionals, families can structure an FLP that not only transfers wealth efficiently but also helps preserve family values while ensuring the continuity of financial stewardship.