Thoughtful planning can maximize value and preserve your legacy.

When selling or transitioning a business, few factors are as important as taxes. With the recent tax changes made by the One Big Beautiful Bill Act (OBBBA), strategic planning can make a significant difference in what business owners keep and what they pass on.

The lifetime gift and estate tax exemption has been increased to $15 million, made permanent and will be adjusted annually for inflation. This pending change makes it even more urgent to consider strategies that mitigate taxes not only on the sale itself, but also on the long-term transfer of wealth.

We’ve outlined several proven tax strategies, which are organized around three core planning objectives: reducing income tax, taking advantage of rollovers and exclusions, and transferring ownership in tax-efficient ways.

Three Pillars of Tax-Smart Business Transitioning

Effective tax planning typically falls into three categories: Income Tax Mitigation, Rollover and Exclusion Strategies, and Estate Freezing and Transfer Techniques.

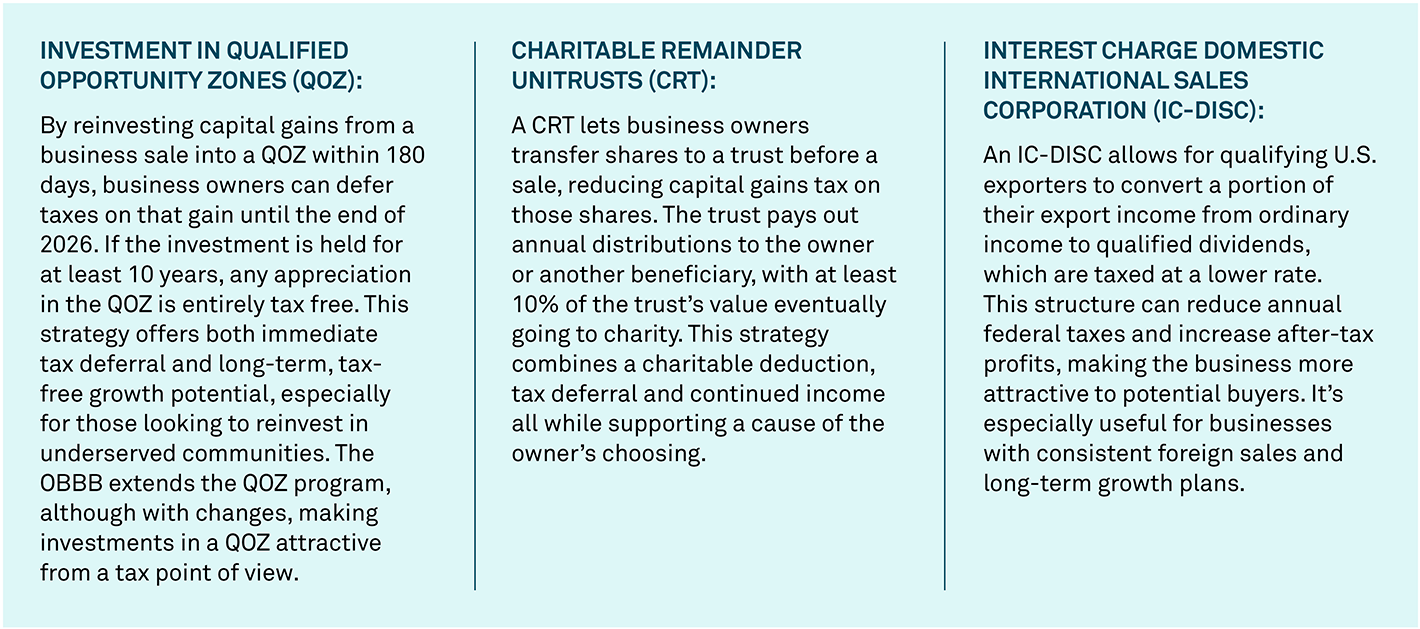

1. Income Tax Mitigation: Keep More of What You Earn

Several advanced strategies can reduce or defer federal and state income taxes on a business sale:

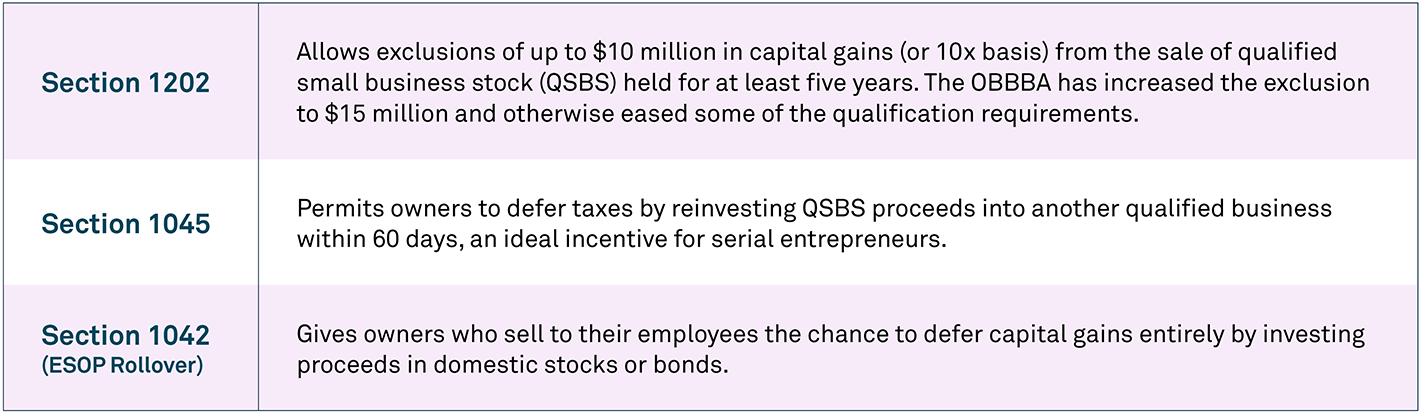

2. Rollover and Exclusion: Preserve Gains, Reinvest for Growth

The IRS offers several incentives to roll gains into other qualified assets.

3. Estate Freezing: Pass the Business on Without the Tax Bill

Passing a growing business to your children while minimizing taxes is best done by “freezing” its current value. Transfer ownership now, then sell later as the business appreciates, shifting future growth out of your taxable estate.

Key strategies include:

- Annual Gifting: Transfer up to $19,000 per year ($38,000 for couples) of company stock to each child, gradually reducing your estate.

- Installment Sale to an Intentionally Defective Grantor Trust (IDGT): Sell all or part of your business to an irrevocable grantor trust for your children in exchange for a promissory note years before a sale. When the business is sold, the trust repays the note, and any appreciation stays in the trust, free of gift and estate tax. Business profits can fund interest payments on the note, shifting future growth out of the taxable estate.

- Private Annuities: Exchange your business for lifetime payments from your children, providing income now while transferring ownership. This approach requires confidence in your children’s management abilities.

- Grantor Retained Annuity Trust (GRAT): Transfer shares to a trust that pays you an annuity. Any future growth passes to heirs tax-free. This is popular technique in a low-interest rate environment.

- Charitable Lead Annuity Trust (CLAT): Support charity with annual payments now, then pass the remaining value to your heirs tax-free, combining philanthropy with tax-efficient wealth transfer.

- Family Limited Partnership (FLP) & Recapitalization: Retain voting control while gifting non-voting shares (often at a discount) to heirs, effectively shifting future appreciation out of our estate.

Maximize Wealth, Minimize Taxes

With trillions in assets transferring to the next generation in the coming decades, proactive tax planning is essential to protect your legacy. Partner with experienced advisors—attorneys, accountants and wealth managers—to craft a tax-smart plan that reflects your vision and protects your children.