Billionaires multiply their wealth by borrowing against their assets to pay for new investments. But they aren’t the only ones who can use leverage to their benefit.

A few years ago, a ProPublica article shed light on the fact U.S. billionaires pay little to no tax.1 Yet it’s not because of tax loopholes as much as it is their ability to leverage their extraordinary wealth. Borrowing against their assets to pay for expenses, and more importantly to reinvest in assets that return more than the cost of borrowing, is how ultra-wealthy individuals run their lives—and increase their net worth.

“Millionaires and billionaires manage their personal financial affairs the way they would run a business—by utilizing their entire balance sheet—including the use of leverage—to fund their spending and their investing,” explains Rick Calero, Chief Revenue Officer at BNY Wealth.

Billionaires generally derive most of their income from asset appreciation, rather than salaries or bonuses. Unlike ordinary income, asset appreciation is not taxed until a gain is realized through the sale of the asset. To avoid or delay the hefty tax obligation resulting from the capital gains incurred, they borrow against their wealth and use the proceeds to not just pay for their expenses but also to reinvest in new ventures. In this way they keep their tax bills low, continue to benefit from the appreciation of their invested assets, plus increase their overall net worth with the additional investments made with the loan proceeds.

But it’s not just the ultra-rich who can use leverage to their benefit. Homeowners can borrow against the equity in their property or utilize leverage to cover tax liabilities or other large one-time expenses. And other wealthy investors can use similar borrowing strategies to preserve and grow their assets.

Using Leverage to Maximize Gains

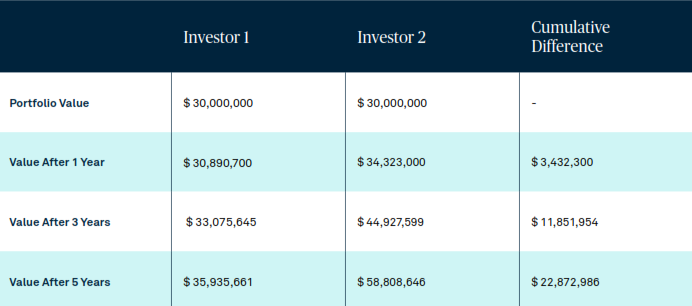

To illustrate how wealthy investors can benefit from the use of leverage, Calero gives the example of two investors, each with $30 million invested in the S&P 500, earning an average annualized return of 14.41%.2 Both investors have an annual tax bill of $3 million.

To pay the tax bill each year, Investor 1 liquidates $3 million from his investment portfolio, giving up some of the gains, whereas Investor 2 borrows against the value of her investment portfolio, allowing it to fully appreciate.

Here’s how they would net out:

After five years, Investor 2’s portfolio value is more than $22.8 million higher than Investor 1’s portfolio. However, after paying roughly $2.34 million in annual interest payments on the loan, Investor 2’s portfolio value at the end of the five-year period is just over $56 million, equating to a cumulative difference of more than $20 million.3 Even with annual interest payments accumulating to more than $2 million, the cost of borrowing is far lower than missing out on the appreciation of a fully intact investment portfolio4. This type of strategy provides even more robust returns when rates are trending lower, as there is essentially less of a cost associated with borrowing.

While this strategy can carry enormous benefits under the right circumstances, securities-based loans may not be appropriate for all investors and do carry the risk of maintaining appropriate levels of collateral in an account during times of heightened volatility. Investors are best suited to develop a plan with their team of advisors to be better prepared and positioned to capitalize on leverage when the correct opportunity presents itself.

Minimize Tax Due by Maximize Interest Deductions

The ability to deduct interest expense is another way to enhance potential return, allowing for the IRS to share in the borrowing costs.5 When appropriate, clients can take advantage of this benefit and offset their other income with up to 37% of their interest cost when applying the highest federal tax bracket.6 This can compound returns in their portfolio beyond what they are already achieving through a borrowing strategy.

Conclusion

Taxes generally can’t be avoided forever. But using leverage to control the timing of gains while implementing Active Wealth can have tremendous benefits to investors over the long run. By Active Wealth, we mean using your full team of advisors to identify specific opportunities that match long-term investments and leverage with shortterm business obligations and other lifestyle needs. This includes strategic borrowing, dynamic spending, and meticulous tax management to help build and preserve wealth.