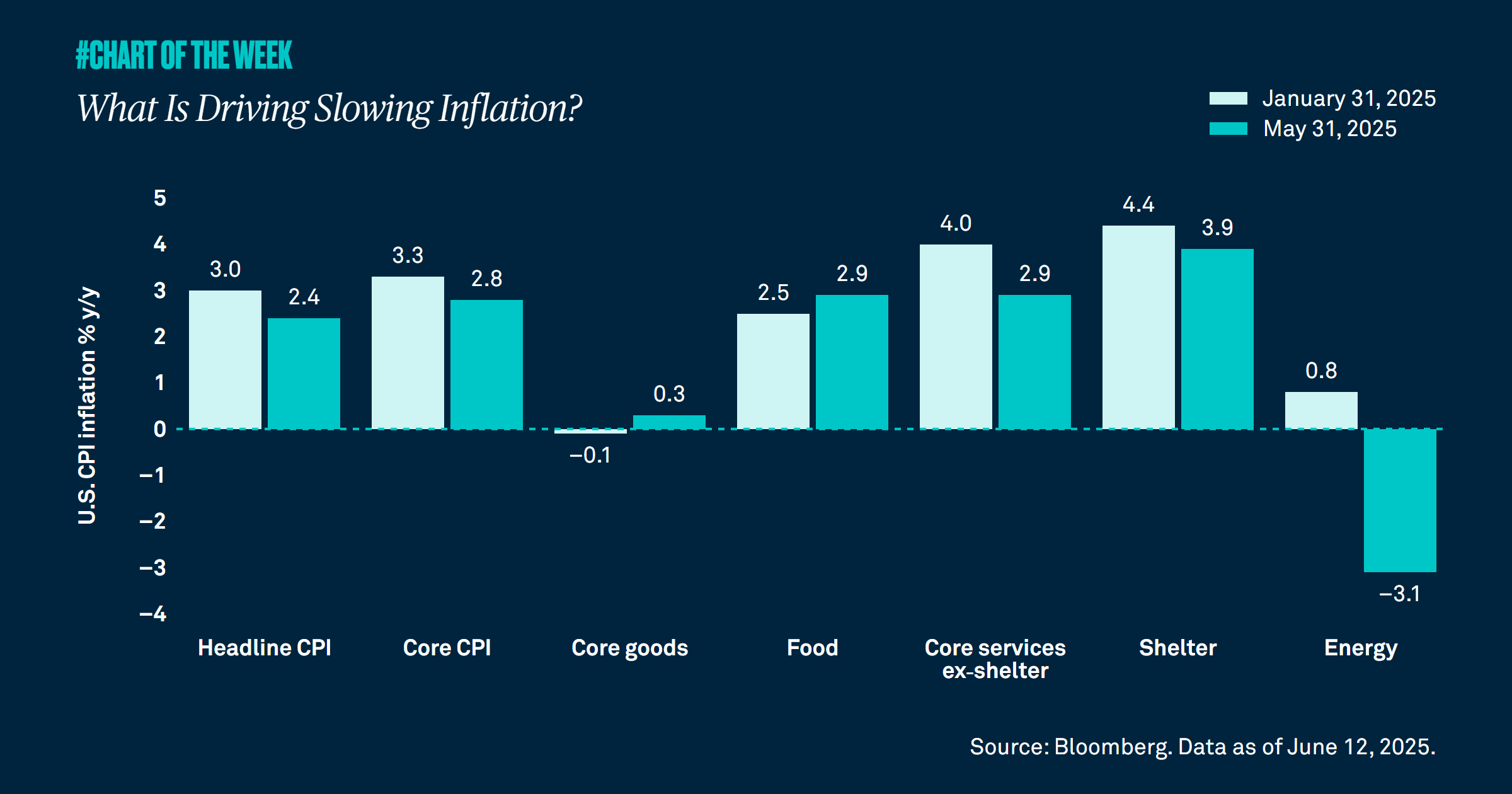

Inflation came in cooler than expected in May. In fact, it’s down from January’s growth rate of 3.0% year over year to 2.4%. While stickier services components such as shelter have driven this decline, could the recent uptick in oil prices and higher tariffs pose headwinds?

While we expected inflation to slow, it is encouraging to see the stickier components of services and shelter inflation driving the decline.

Led by services, the disinflation trend has been notable, with prices declining from a growth rate of 3.0% from a year ago in January to 2.4% in May. At 3.9% year over year, shelter inflation is the lowest it has been since November 2021, while core services at 2.9% is the lowest in more than four years.

However, could tariff-related price hikes and the recent increase in oil prices due to tensions in the Middle East hamper the downward path of inflation? We believe the impact of tariffs will amount to a one-time price adjustment as opposed to a long-term trend. Despite the roughly $17 increase in the price of oil since early May to $74 a barrel, it is only up 0.4% from a year ago. If there are no significant supply disruptions or if tensions de-escalate, the additional impact to energy prices or overall inflation should be limited. While the disinflation trend may slow from here, we maintain our year-end inflation forecast of 2.5-3.5%.