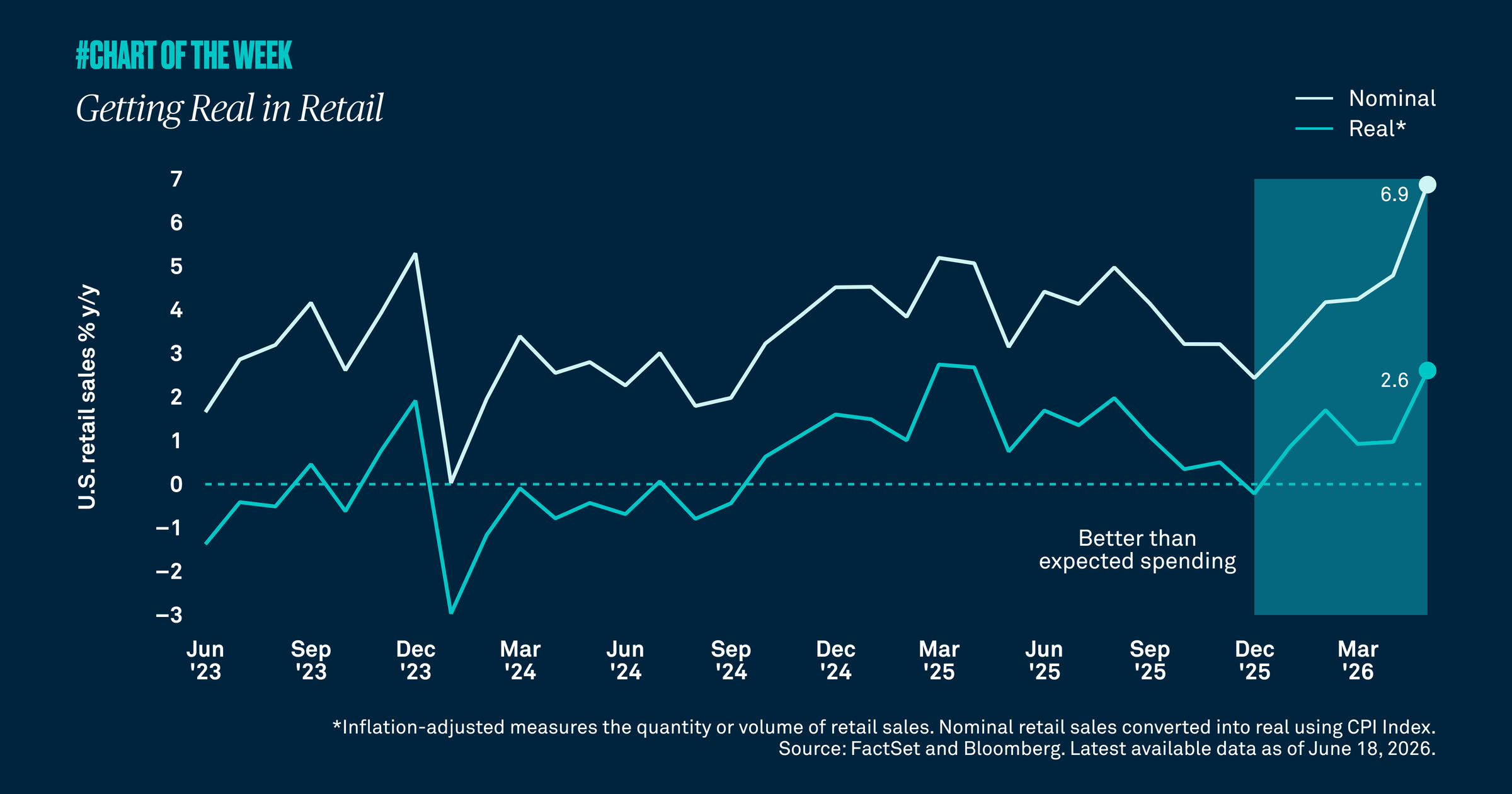

Despite persistent concerns that sticky inflation would erode purchasing power and drag consumer spending lower, the May retail sales data tells a different story. Spending is up not just in dollar terms, but in quantity, highlighting continued consumer resilience.

Nominal retail sales rose 6.9% year-over-year in May, the strongest growth rate in several years and more than double the average pace recorded since 2023. Importantly, this was not simply a reflection of higher prices. Real, inflation-adjusted retail sales grew 2.6% year-over-year — roughly 2% above the average — confirming that consumers are buying more, not just paying more.

However, U.S. consumer spending has not been uniform. The K-shaped dynamic (where higher-income households continue to spend while lower-income consumers face more meaningful pressure) is real and ongoing. While pockets of stress exist, total spending has held up and increased.

That said, the picture is not without risk. Higher inflation could weaken the spending momentum and lead to slower economic growth. For now, the increase in total consumer buying activity supports our constructive forward outlook and justifies remaining invested.