Insights

MOST RECENT

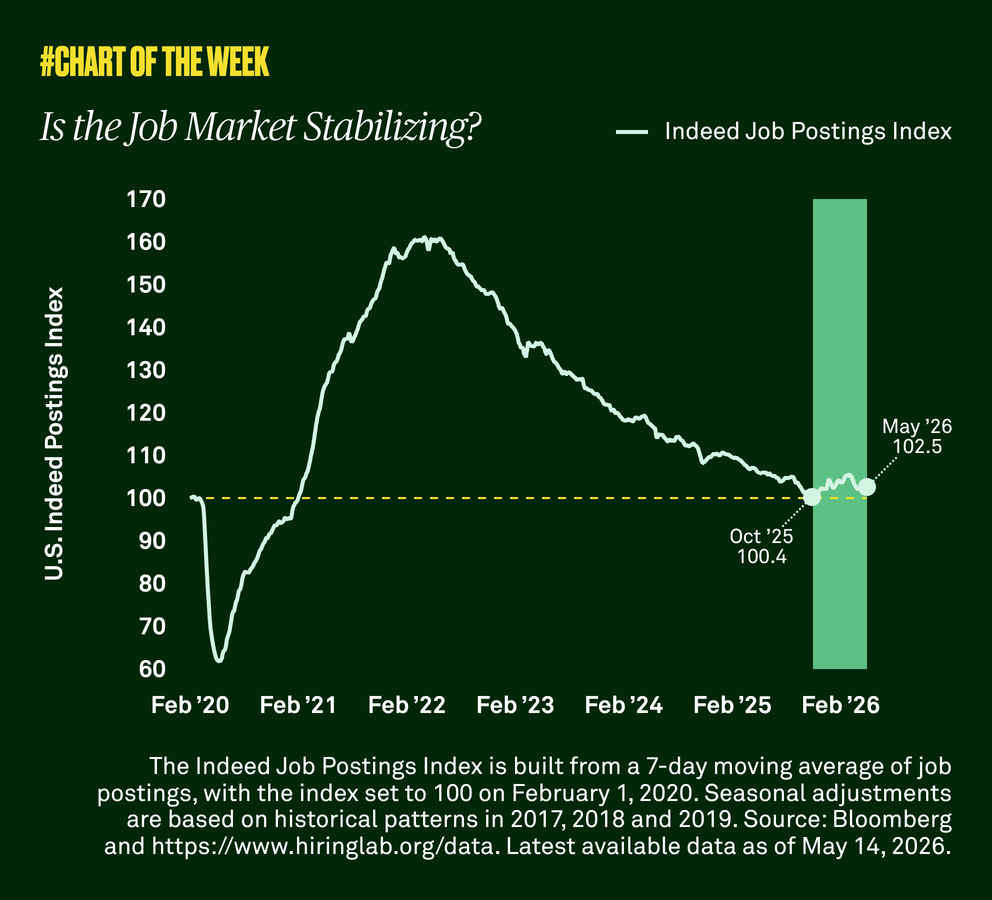

Is the Job Market Stabilizing?

After sluggish job growth in 2025, investors are looking for signs that the labor market may be stabilizing. With consumer spending driving 70% of economic activity, an improving labor market is essential to sustaining economic growth.