Insights

MOST RECENT

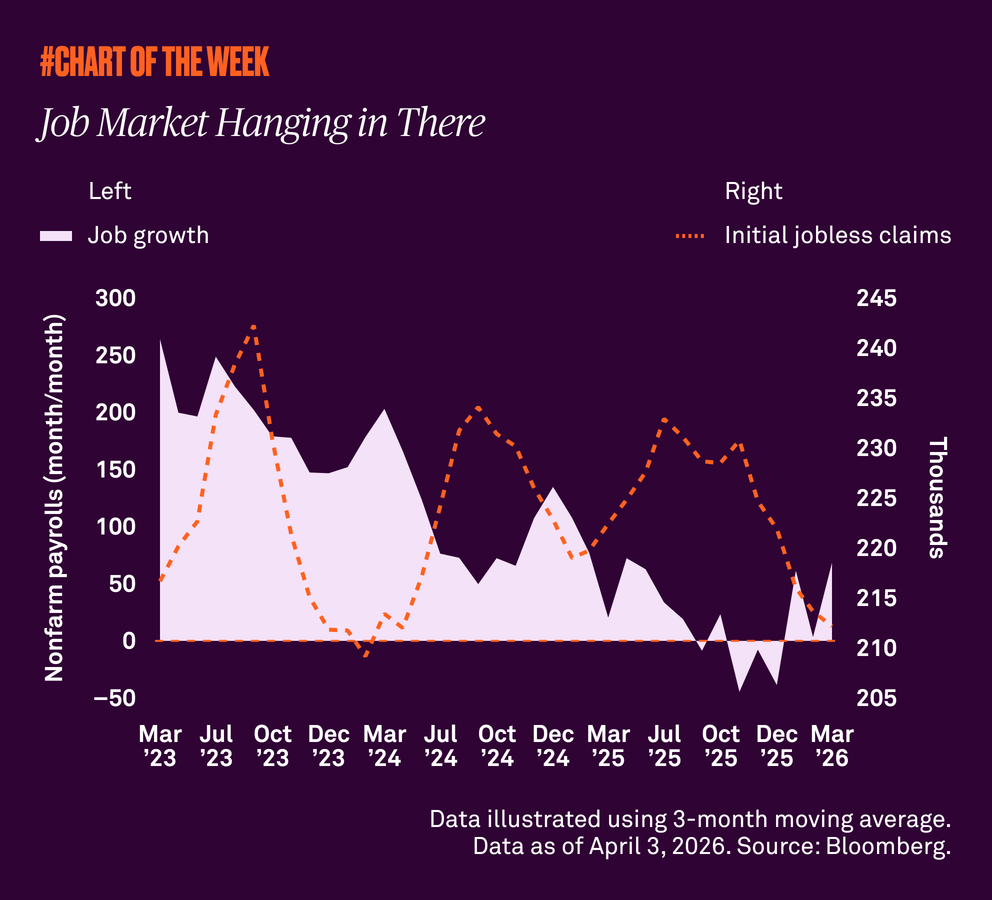

Job Market Hanging in There

Recent jobless claims data point to a resilient U.S. labor market, with both initial and continuing claims remaining low and signaling that unemployment is still contained. Although job growth has softened and remains subdued, March’s job growth of 178,000, the highest since 2024, is encouraging. Our constructive outlook still holds despite continued uncertainty related to the war in the Middle East.