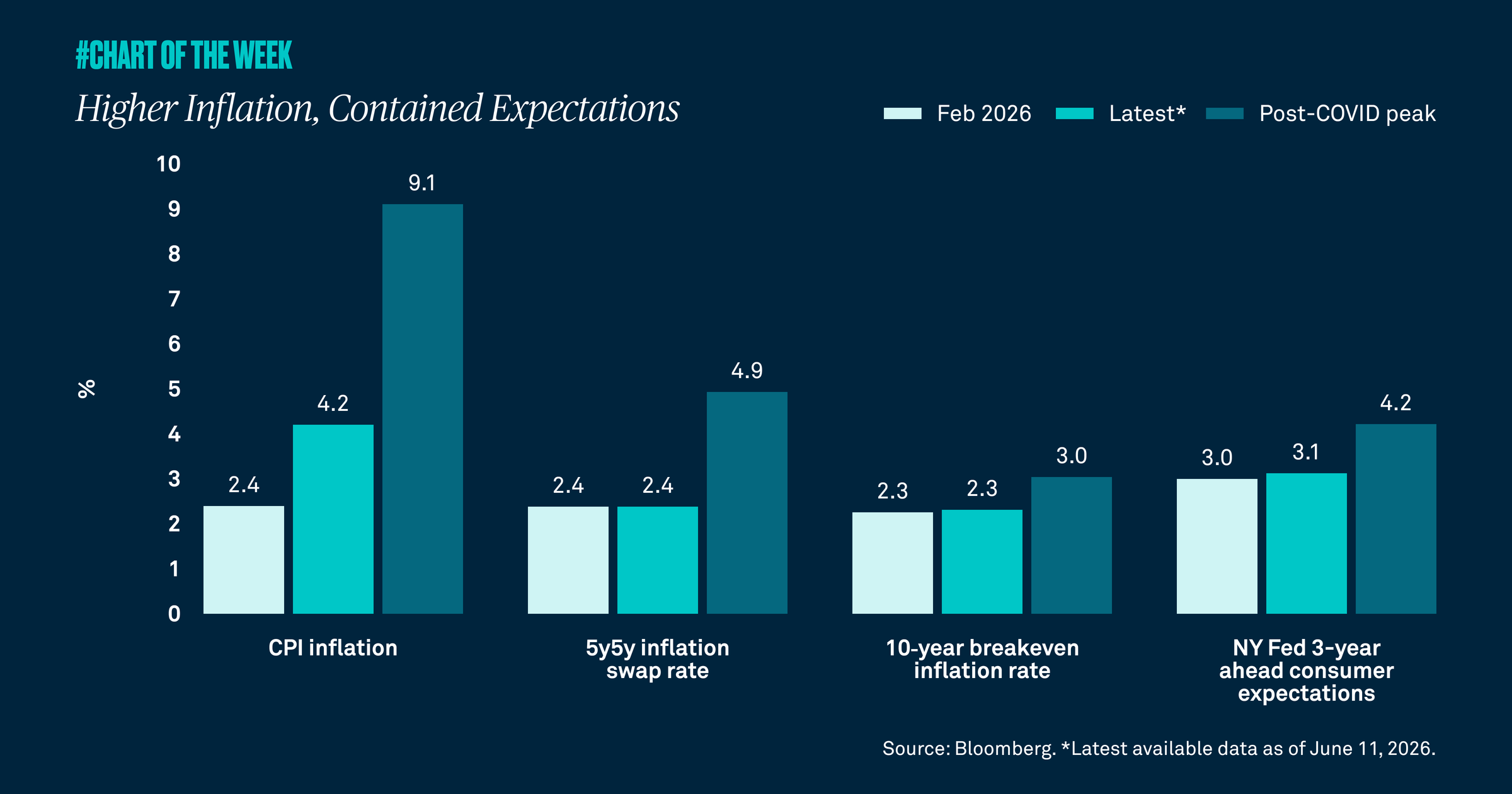

Inflation has jumped since the Strait of Hormuz closed, squeezing consumers through higher gas and utility bills and pressuring businesses with higher freight and operating costs. Yet, longer-term inflation expectations remain contained, suggesting this looks more like a temporary energy shock than a lasting inflation upswing.

Inflation has risen since the start of the Iran conflict and the closure of the Strait of Hormuz, driven largely by higher energy costs. Consumers are feeling it through higher gasoline and utility bills, while business owners are facing higher freight, utility and operating costs.

Since February, annual inflation has increased to 4.2% from 2.4%. Yet, longer-term inflation expectations have stayed well anchored, suggesting households and markets still view this as an energy-driven shock rather than the start of a lasting inflation upswing. We share this view, and believe Middle East tensions should ease sooner rather than later given the pending peace deal, which will allow energy prices to normalize over time. Still, we could see higher inflation prints over the next several months, which, combined with a resilient economy, should keep the Federal Reserve on hold.

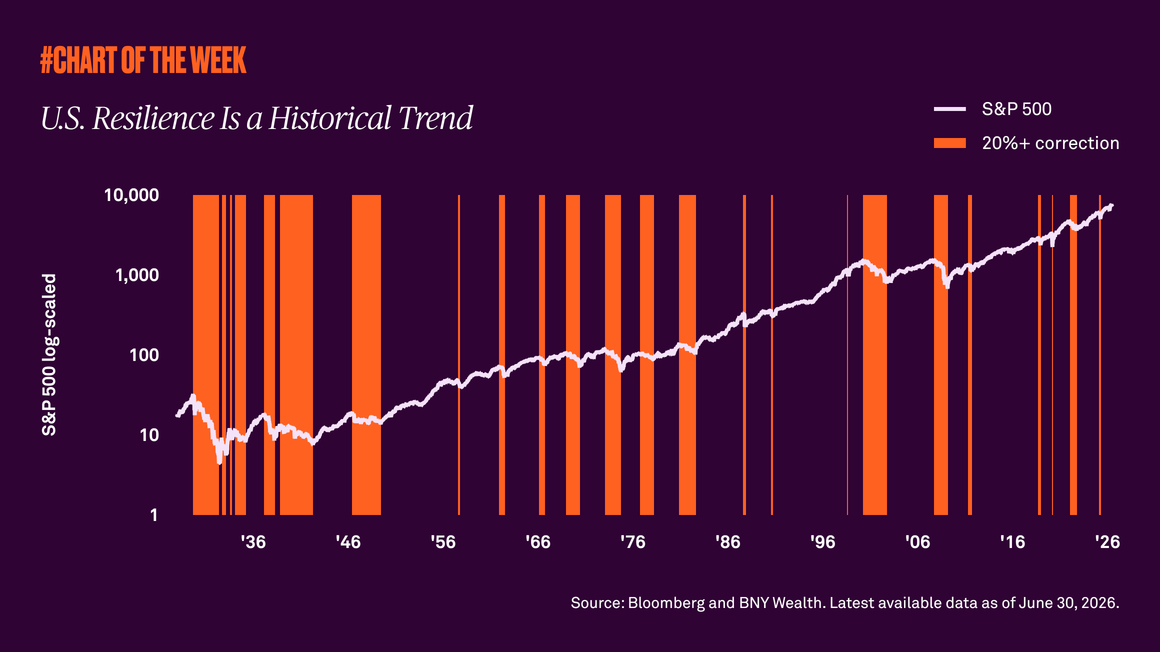

While near-term volatility is possible, we remain constructive on U.S. equities, supported by resilient earnings, solid capital spending and a stabilizing labor market over the long term.