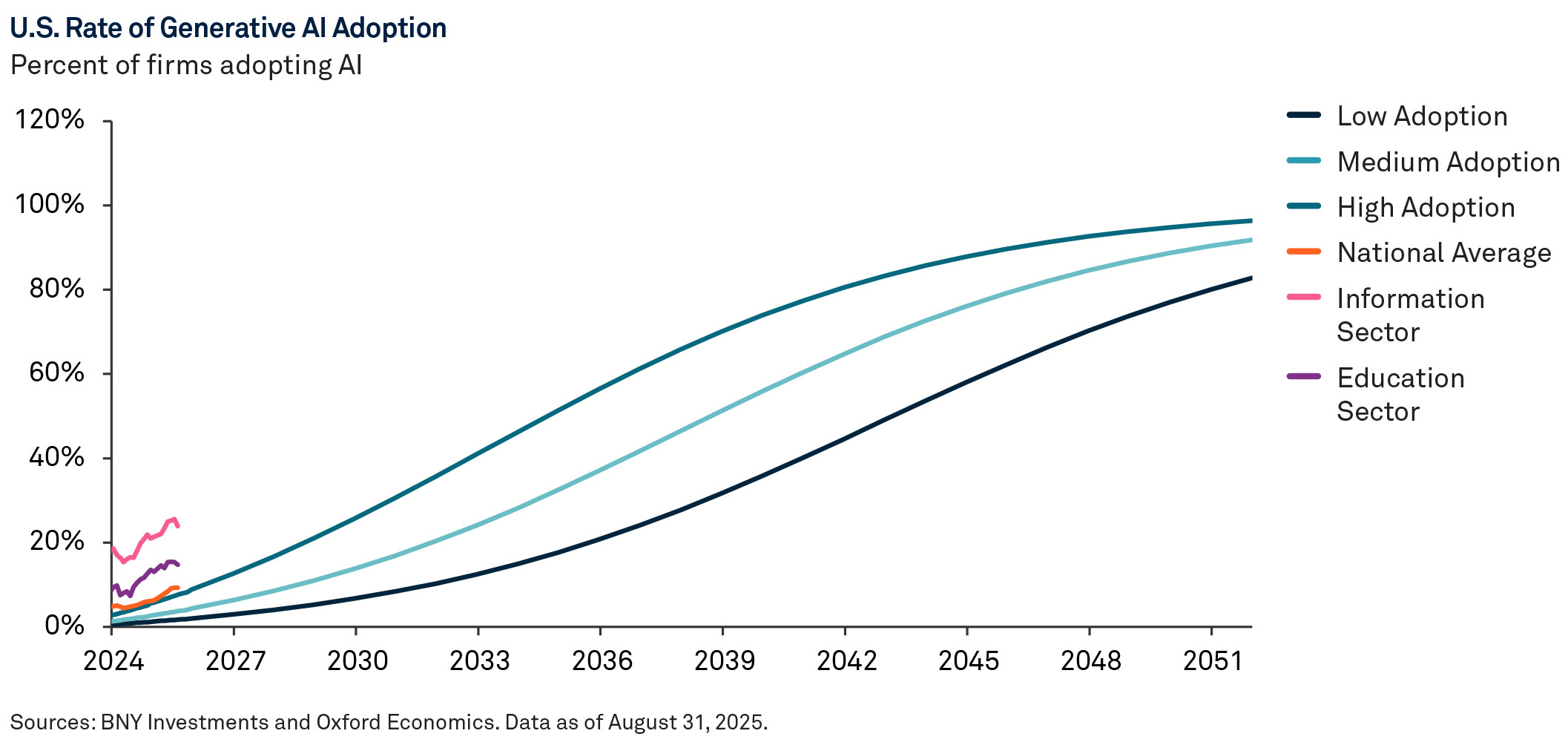

In a short period, AI has advanced from novelty to an integral part of workflows, often matching or surpassing human performance in areas such as image classification, algorithm design, and data analysis.

Rapid Adoption Drives Infrastructure Demand

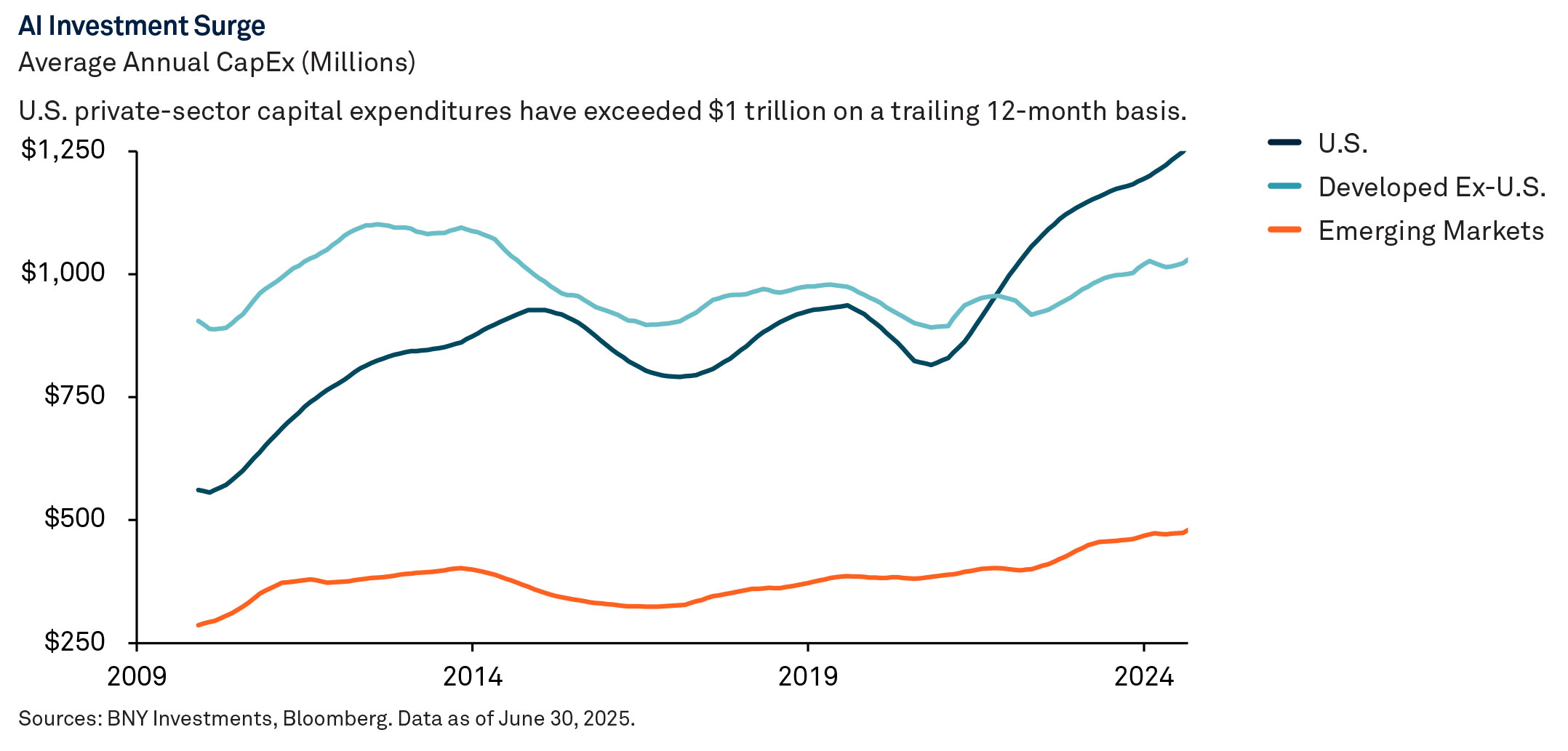

The rapid uptake and deployment of the technology require substantial infrastructure investment, including the construction of data centers, semiconductor facilities, and an energy grid capable of supporting AI’s significant computational demands. These prerequisites have created a geopolitical race to accelerate AI deployment in pursuit of potential growth opportunities. U.S. private-sector capital expenditures have exceeded $1 trillion on a trailing 12-month basis, the most pronounced post-pandemic investment surge among major economies. This positions the U.S. to achieve earlier and potentially more rapid productivity gains.

Productivity Is Not the Only Factor

While productivity gains may be on the horizon, we believe it’s key to look beyond early productivity gains to see which firms and sectors can turn technological advantage into lasting market power. As adoption expands, the impact on productivity and competitive dynamics will become more visible. We expect the market to shift focus from who is building and using AI to who can truly capture value from AI.

AI lowers the cost of accessing and transforming information, reducing the scarcity that underpins information-based competitive advantages. Sectors whose advantages stem from physical assets, regulatory barriers, or network effects may find their advantages preserved, and AI-related productivity gains in these sectors could more likely accrue to shareholders. Sectors that rely heavily on information processing, such as software, search engines, and health care diagnostics, could see competitive dynamics intensify as AI levels the playing field. Several large, public companies have already faced market concerns over how generative AI may negatively affect their existing business models.

Tapping Unmet Demand

AI-driven shifts in profit margins are only part of the story; another part of the story lies in demand. As the price falls, demand for a given good or service typically rises. Even sectors facing margin and price compression due to AI may still see an increase in overall profits — if the rise in demand outweighs the decline in prices.

Over time, as AI boosts productivity and lowers prices, aggregate real incomes could rise — potentially driving further outsized demand in some sectors. Health care, for example, is a sector with significant unmet demand. Most people want good health care, but many can’t afford it. Lower-cost diagnostics and treatments would likely drive volume growth, potentially boosting overall profits.

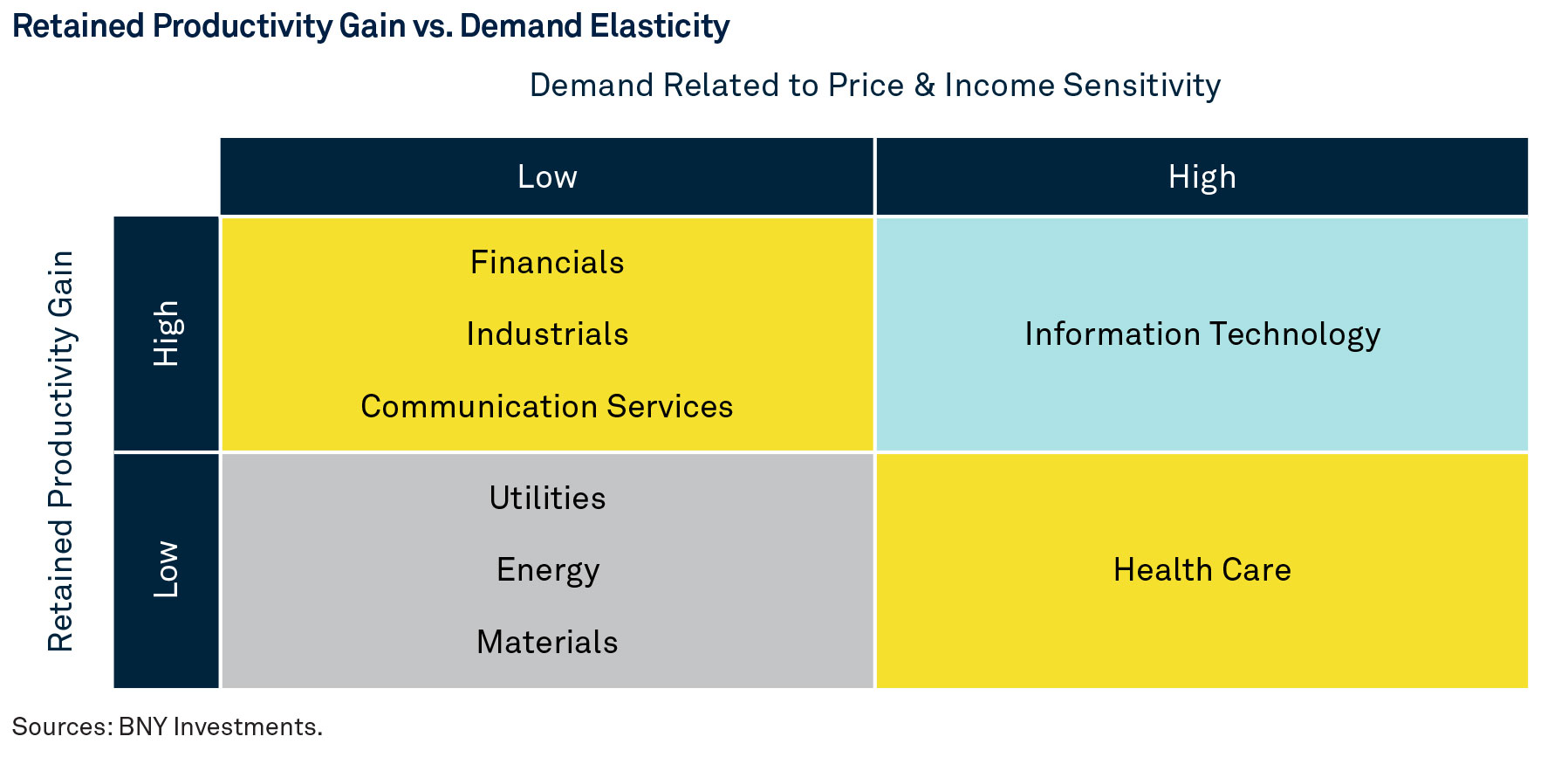

Dynamics That Determine Durability

The biggest beneficiaries of AI adoption won’t simply be the fastest adopters. Winning firms will likely leverage two advantages: strong productivity gains even after widespread adoption and the ability to capture unmet demand where lower prices translate into higher volumes. Sectors that pair these two dynamics together can become important plays in the AI theme. While information technology remains a favored sector under this framework, it also faces significant disruption with wide dispersion between winners and laggards.

This is an excerpt from our 2026 report, Capital Market Assumptions: Endurance Under Pressure

For further discussion and in-depth analysis, read the full report.

FOR INSTITUTIONAL, PROFESSIONAL, QUALIFIED INVESTORS AND QUALIFIED CLIENTS ONLY.

CAPITAL MARKET ASSUMPTIONS

The capital market assumptions are BNY Advisors’ estimates based upon historical market performance and the current market environment. References to future expected returns are not promises of actual returns that may be realized and should not be relied upon. Actual returns may vary significantly. In addition, the historical returns used as a basis for this analysis are based on information gathered by BNY or from third-party sources and have not been independently verified.

The forecasts contained herein are for illustrative purposes only and are not guarantees of performance. The forecasts have inherent limitations because they are not based on actual transactions. The forecasts are based upon historical returns of the selected investments and subjective estimates and assumptions about circumstances and events that may not have taken place and may never do so.

Some of the factors that could impact these forecasts include, but are not limited to:

• General economic conditions

• Financial market performance

• Interest rate levels

• Changes to current laws or regulations, and

• Future geopolitical conditions

Asset class returns are not reflective of anticipated returns for associated indexes.

The results do not represent, and are not necessarily indicative of, the results that may be achieved in the future.

Robust Strategic Asset Allocation (RSAA) is a framework for classifying the market environment with a combination of macroeconomic and market indicators with judgment. BNY Advisors has defined historical regimes for the period starting in May 1973.

The asset classes referenced in our capital market assumptions are represented by broad-based indices which have been selected because they are well known and are easily recognizable by investors. Indices have limitations because indices have volatility and other material characteristics that may differ from an actual portfolio. For example, investments made for a portfolio may differ significantly in terms of security holdings, industry weightings and asset allocation from those of the index. Also, the indices noted in this presentation are unmanaged, are not available for direct investment, and are not subject to management fees, transaction costs or other types of expenses that a portfolio may incur. Finally, the performance of the indices reflects reinvestment of dividends and, where applicable, capital gain distributions. Therefore, investors should carefully consider these limitations and differences when evaluating the index performance.

The indices may be trademarks of various organizations and in those cases have been licensed for use by BNY and are used solely herein for comparative purposes. The foregoing index licensers are not affiliated with BNY, do not endorse, sponsor, sell or promote the investment strategies mentioned in this presentation and they make no representation regarding advisability of investing in the strategies described herein. Description of the indices are available upon request.

Past performance is no guarantee of future results.

Important Information

For sole and exclusive use by Institutional Investors, Accredited Investors and Professional Investors only. Not for further distribution. This is a financial promotion and is not investment advice. Any views and opinions are those of the investment manager, unless otherwise noted. The value of investment can fall. Investors may not get back the amount invested. BNY Investments is the brand name for the investment management business of BNY and its investment firm affiliates worldwide. BNY is the corporate brand of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole or its various subsidiaries generally. In Hong Kong, the issuer of this document is BNY Mellon Investment Management Hong Kong Limited, which is registered with the Securities and Futures Commission (Central Entity Number: AQI762). In Singapore, this document is issued by BNY Mellon Investment Management Singapore Pte. Limited, Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore (MAS). This advertisement has not been reviewed by the Monetary Authority of Singapore.

GU-793 - 15 February 2027