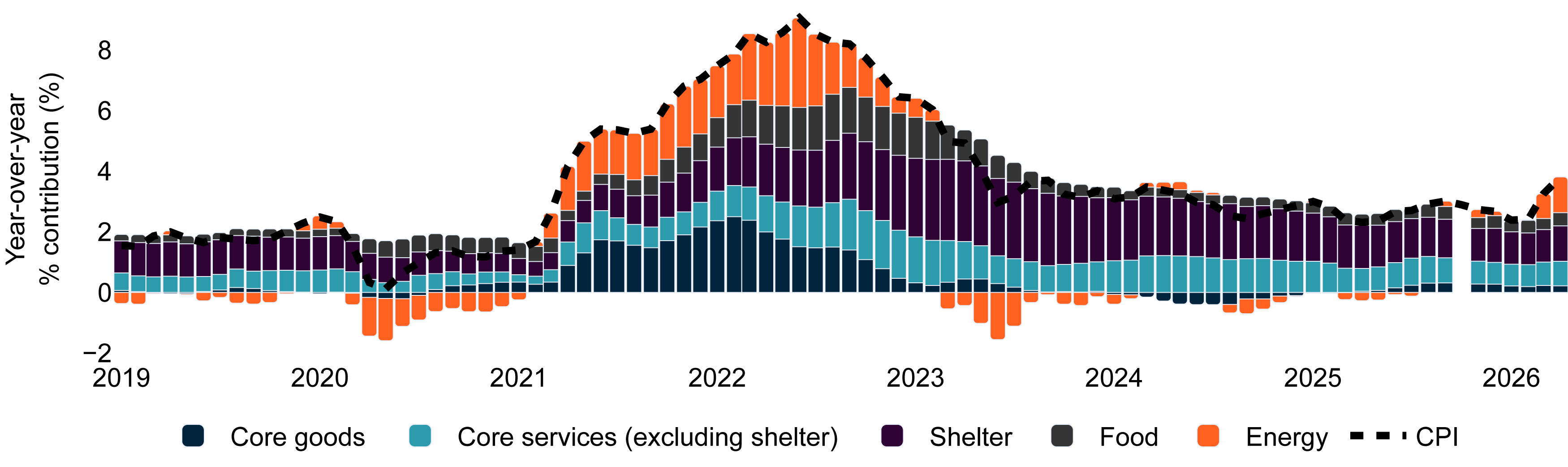

Consumer prices rose 0.6% in April, taking headline CPI (Consumer Price Index) from 3.3% to 3.8% year-over-year, the highest since May 2023. Core prices rose 0.3% in April, or from 2.6% to 2.8% year-over-year, the highest since October 2025. Although a “hot” print, we believe it is unlikely to shift the Federal Reserve (the Fed) from its easing bias for now..

Energy prices continue to hit consumers

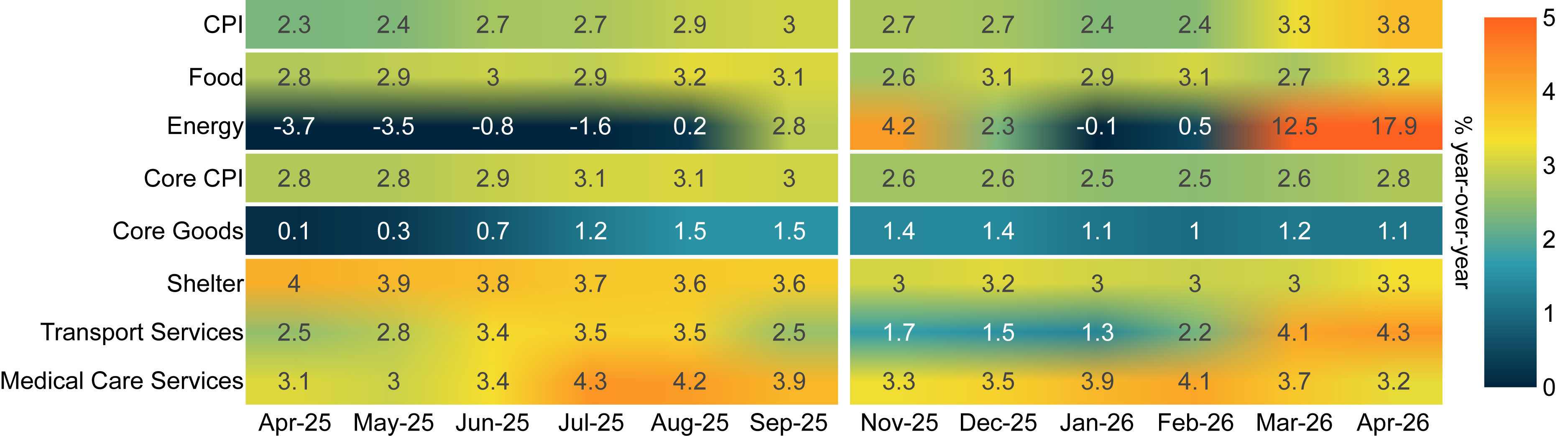

Outside of energy, most categories were relatively contained. Core goods prices were flat in April, with tariff-sensitive goods categories rising just 0.1% during the month, indicating a potentially waning impact from trade policy.

Food inflation rose 0.5% in April, with grocery prices like meats, poultry, fish, and fresh fruits and vegetables showing notable gains, although “food away from home” inflation was relatively muted.

Energy drives inflation, while most other categories remain largely contained

Source: Bureau of Labor Statistics, Macrobond, Insight Investment, May 2026. A CPI report was not produced for October 2025 due to the government shutdown. Charts are for illustrative purposes only.

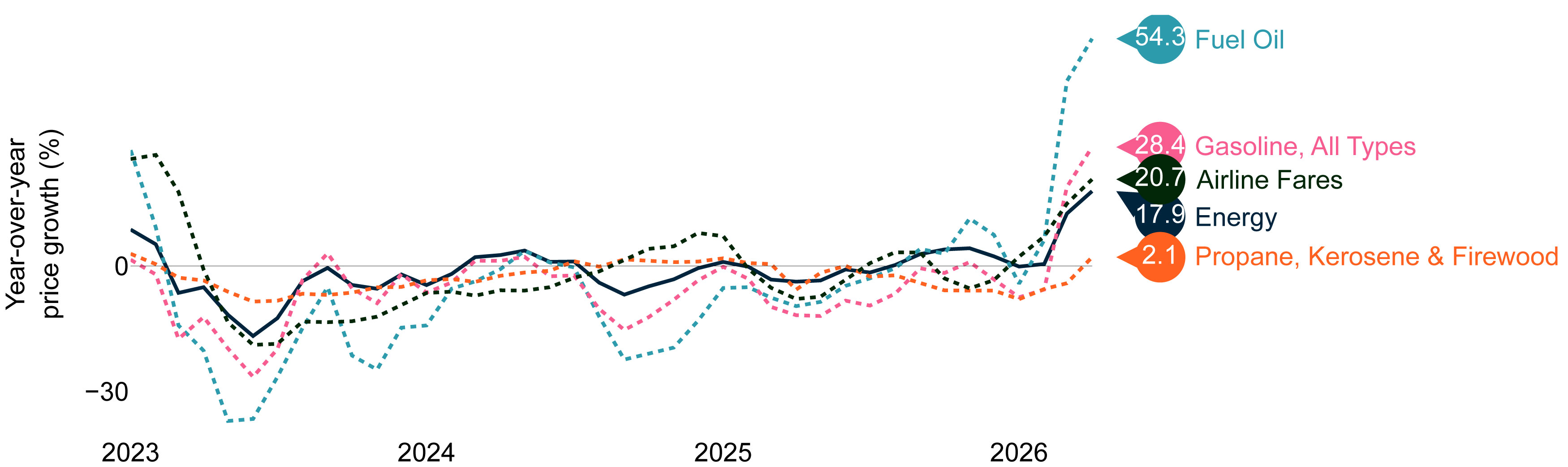

Energy inflation continued to be driven by supply chain disruptions in the Middle East. Energy goods categories (particularly gasoline and fuel oil) continued to be impacted the most. Transportation services also continued to be impacted through airline fares.

Strait of hormuz disruption continues to impact energy goods and services

Source: Bureau of Labor Statistics, Macrobond, Insight Investment, May 2026. A CPI report was not produced for October 2025 due to the government shutdown. Charts are for illustrative purposes only.

Shelter rises as government shutdown disruption finally unwinds

Shelter, the largest component of the CPI, accelerated from 3% to 3.3% year-over-year, the highest since October 2025. However, this reflects the final lingering effects of last year’s government shutdown. Due to the way shelter is calculated, it has been artificially depressed since the shutdown, but the effect finally unwound in April. Ultimately, we expect shelter to continue its disinflationary trend, in line with leading rental market indicators.

Shelter provides a potentially temporary boost to CPI

Source: Bureau of Labor Statistics, Macrobond, Insight Investment, May 2026. A CPI report was not produced for October 2025 due to the government shutdown. Charts are for illustrative purposes only.

CPI better than headlines suggest?

The longer the energy shock lasts, the risks of it feeding through to more durable core services will rise.

For now, we believe the Fed will still be minded to “look through” energy prices while longer-dated inflation expectations remain anchored and second-round effects appear muted.

While the Fed may increasingly be inclined to switch from an easing bias to a neutral one, we believe it would take a high hurdle to put a potential rate hike on the agenda.

INVESTMENT VIEWS FROM INSIGHT INVESTMENT

Insight Investment is a leading global investment manager and fixed income specialist firm within BNY Investments.

IMPORTANT INFORMATION

Investment advisory services in North America are provided by Insight North America LLC, a registered investment adviser and regulated by the U.S. Securities and Exchange Commission (SEC). Insight North America LLC is associated with other global investment managers that also (individually and collectively) use the corporate brand Insight Investment and may be referred to as “Insight” or “Insight Investment.” Insight is a subsidiary of BNY.

The information contained herein reflects general views and is provided for informational purposes only. This material is not intended as investment advice nor is it a recommendation to adopt any investment strategy.

Opinions and views expressed are subject to change without notice.

Past performance is no guarantee of future results.

Issuing entities

This material is only for distribution in those countries and to those recipients listed, subject to the noted conditions and limitations: • United States: by BNY Mellon Securities Corporation (BNYSC), 240 Greenwich Street, New York, NY 10286. BNYSC, a registered broker-dealer and FINRA member, has entered into agreements to offer securities in the U.S. on behalf of certain BNY Investments firms. • Europe (excluding Switzerland): BNY Mellon Fund Management (Luxembourg) S.A., 2-4 Rue EugèneRuppertL-2453 Luxembourg. • UK, Africa and Latin America (ex-Brazil): BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. Authorised and regulated by the Financial Conduct Authority. • South Africa: BNY Mellon Investment Management EMEA Limited is an authorised financial services provider. • Switzerland: BNY Mellon Investments Switzerland GmbH, Bärengasse 29, CH-8001 Zürich, Switzerland. • Middle East: DIFC branch of The Bank of New York Mellon. Regulated by the Dubai Financial Services Authority. • South East Asia and South Asia BNY Mellon Investment Management Singapore Pte. Limited Co. Reg. 201230427E. Regulated by the Monetary Authority of Singapore. • Hong Kong: BNY Mellon Investment Management Hong Kong Limited. Regulated by the Hong Kong Securities and Futures Commission. • Japan: BNY Mellon Investment Management Japan Limited. BNY Mellon Investment Management Japan Limited is a Financial Instruments Business Operator with license no 406 (Kinsho) at the Commissioner of Kanto Local Finance Bureau and is a Member of the Investment Trusts Association, Japan and Japan Investment Advisers Association and Type II Financial Instruments Firms Association. • Brazil: ARX Investimentos Ltda., Av. Borges de Medeiros, 633, 4th floor, Rio de Janeiro, RJ, Brazil, CEP 22430-041. Authorized and regulated by the Brazilian Securities and Exchange Commission (CVM). • Canada: BNY Mellon Asset Management Canada Ltd. is registered in all provinces and territories of Canada as a Portfolio Manager and Exempt Market Dealer, and as a Commodity Trading Manager in Ontario. All issuing entities are subsidiaries of The Bank of New York Mellon Corporation. BNY Investments is the brand name for the investment management business of BNY and its investment firm affiliates worldwide.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. All information contained herein is proprietary and is protected under copyright law.

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

©2026 THE BANK OF NEW YORK MELLON CORPORATION

MARK-936469-2026-05-12 | GU-859 - 31 December 2026